Healthcare Transactions: Year in Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Spendesk Raises €100M Series C to Bring Spend Management to Every finance Team in Europe

Spendesk raises €100M Series C to bring spend management to every finance team in Europe Round led by global growth equity firm General Atlantic to accelerate product innovation and grow headcount internationally. Paris, FR - July 21, 2021 Spendesk, the leading all-in-one spend management platform for finance teams, has raised €100M in Series C funding led by global growth equity firm General Atlantic. All previous investors, including Index Ventures and Eight Roads Ventures, also participated in this round, bringing Spendesk’s total funding to €160M. With the additional investment, Spendesk will focus on hiring top talent and accelerating product innovation to bring more automation and insights to every aspect of business spending. Spendesk offers an intuitive SaaS spend management solution that provides full visibility and control on all company spending — with every purchase trackable to a person, a project, and a budget. The platform combines payments, processes and data into one source of truth, with virtual and physical cards for employees, expense reimbursements, invoice management, automated spend approvals, and budgets. The solution aims to liberate finance teams from day-to-day admin tasks, freeing them to focus on proactive and strategic value-add. “Work culture is becoming increasingly informed by our private lives. Employees crave more empowerment, agility and faster decision-making to be effective in their roles. And traditionally, finance teams haven’t been equipped with the tools that can support this transformation,” said Spendesk’s co-founder and CEO, Rodolphe Ardant. “In the past few years we have built the reference spend management solution for finance teams in Europe, which frees businesses and their people from administrative constraints of spending and managing money at work. -

Tpg to Invest ₹ 4,546.80 Crore in Jio Platforms Tpg's Deep

TPG TO INVEST ₹ 4,546.80 CRORE IN JIO PLATFORMS TPG’S DEEP CAPABILITIES IN TECH INVESTING TO SUPPORT JIO’S INITIATIVES TOWARDS DEVELOPING THE DIGITAL SOCIETY JIO PLATFORMS FUND RAISING FROM MARQUEE GLOBAL TECHNOLOGY INVESTORS CROSSES ₹ 1 LAKH CRORE Mumbai, June 13, 2020: Reliance Industries Limited (“Reliance Industries”) and Jio Platforms Limited (“Jio Platforms”), India’s leading digital services platform, announced today that global alternative asset firm TPG will invest ₹ 4,546.80 crore in Jio Platforms at an equity value of ₹ 4.91 lakh crore and an enterprise value of ₹ 5.16 lakh crore. The investment will translate into a 0.93% equity stake in Jio Platforms on a fully diluted basis for TPG. With this investment, Jio Platforms has raised ₹ 102,432.45 crore from leading global technology investors including Facebook, Silver Lake, Vista Equity Partners, General Atlantic, KKR, Mubadala, ADIA, and TPG since April 22, 2020. Jio Platforms, a wholly-owned subsidiary of Reliance Industries, is a next-generation technology platform focused on providing high-quality and affordable digital services across India, with more than 388 million subscribers. Jio Platforms has made significant investments across its digital ecosystem, powered by leading technologies spanning broadband connectivity, smart devices, cloud and edge computing, big data analytics, artificial intelligence, Internet of Things, augmented and mixed reality and blockchain. Jio Platforms’ vision is to enable a Digital India for 1.3 billion people and businesses across the country, including small merchants, micro-businesses and farmers so that all of them can enjoy the fruits of inclusive growth. TPG is a leading global alternative asset firm founded in 1992 with more than $79 billion of assets under management across a wide range of asset classes, including private equity, growth equity, real estate and public equity. -

80 Acres Farms Secures $160 Million in Series B Led by General Atlantic to Accelerate Global Farm Expansion & Product Development

80 Acres Farms Secures $160 Million in Series B Led by General Atlantic to Accelerate Global Farm Expansion & Product Development Hamilton, OH - August 9, 2021 80 Acres Farms, an industry-leading vertical farming company, has secured $160 million in additional funding in a round led by General Atlantic and joined by Siemens Financial Services, Inc. (the U.S. financing arm of global technology company Siemens). The company intends to utilize the capital for continued expansion and product development, building from its current footprint of vertical farms that yield a diverse offering of high-quality produce. The funding round also included Blue Earth (formerly PG Impact Investments) and General Atlantic’s Beyond Net Zero team, in addition to participation from existing investors including Barclays and Taurus. 80 Acres Farms’ vertical farm systems grow a wide variety of produce commercially sold at scale, including leafy greens, herbs, tomatoes, cucumbers, and microgreens. The company’s breakthrough growing technologies and advanced data analytics capabilities have enabled this industry-leading product breadth, driving over 450% revenue growth since the end of 2020. 80 Acres Farms now services over 600 retail and food service locations, including its recent expansion with Kroger, announced earlier this year to 316 stores in the U.S. Midwest and to the e-commerce channel powered by Kroger – Ocado Solutions’ partnership. With farms co-located near customers, 80 Acres Farms’ produce travels significantly fewer food miles, shortening the farm-to-table footprint and reducing overall food waste. Growing methods at 80 Acres Farms use 97% less water than traditional farming practices and are powered by renewable energy. -

General Atlantic Leads $100 Million Investment in Fresha, Leading Global Beauty and Wellness Platform, to Fuel Continued Growth

General Atlantic leads $100 million investment in Fresha, leading global beauty and wellness platform, to fuel continued growth New York, NY - June 11, 2021 Fresha, a top beauty and wellness software platform, announced today a $100 million Series C investment led by General Atlantic, a leading global growth equity firm, with strategic participation from Huda Kattan of HB Investments and the founder of Huda Beauty, as well as Michael Zeisser of FMZ Ventures, former Chairman Investments at Alibaba Group, and Jonathan Green of Lugard Road Capital. Fresha’s existing global investors Partech, Target Global and FJ Labs also participated in the round, bringing the company’s total fundraising to $132 million to date. Fresha will leverage the new funds to further broaden its global community of partner salons and spas, scale product development, deepen its marketplace bookings and pursue strategic M&A. Fresha allows consumers to discover, book and pay for beauty and wellness appointments with local businesses via its marketplace, while salons, spas and barbershops can leverage Fresha to manage their operations with its intuitive, subscription-free business software. The Fresha platform removes the critical pain points that service- based businesses often encounter by seamlessly facilitating the acceptance of online appointment bookings, processing of card payments and management of customer records, along with automations for marketing, staffing, product inventory and accounting, all in one place. In addition to its free offering, Fresha Plus provides partners with additional advanced features; rather than a traditional subscription model, the company collects fees on the usage of features for card payment processing and online bookings. -

Anish Batlaw Joins General Atlantic As Operating Partner

Anish Batlaw Joins General Atlantic as Operating Partner New York, NY - March 31, 2015 General Atlantic (‘GA’), a leading global growth equity firm, announced today that Anish Batlaw, former Operating Partner with TPG Capital, has joined GA as Operating Partner. Mr. Batlaw will be part of the firm’s Resources Group, leading GA’s human capital efforts in support of its global portfolio companies. He will be based in GA’s New York office. GA’s Resources Group is composed of experienced senior executives who collaborate with the firm’s investment teams and portfolio companies to execute global growth strategies. The Resources Group provides functional expertise in areas such as human capital development, pricing and salesforce effectiveness, global M&A, technology, finance, tax and capital markets and lead development through the GA Network. General Atlantic’s global team is dedicated to identifying attractive, high-growth companies and providing capital and strategic support to build market leaders. “We are very pleased to welcome Anish to the GA team as an operating partner,” said Bill Ford, CEO of General Atlantic. “Building high-performance management teams and world class boards of directors is a key part of how we add value to our portfolio companies, and we expect Anish to make valuable contributions in this area.” Mr. Batlaw said, “I am impressed with General Atlantic’s commitment to building industry leaders and excited about helping the GA portfolio companies build and scale their organizations.” Prior to joining GA, Mr. Batlaw was an Operating Partner with TPG Capital and Head of Human Capital for Asia. -

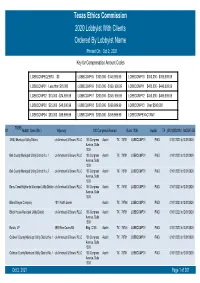

Texas Ethics Commission 2020 Lobbyist with Clients Ordered by Lobbyist Name Printed on Oct 2, 2021 Key for Compensation Amount Codes

Texas Ethics Commission 2020 Lobbyist With Clients Ordered By Lobbyist Name Printed On Oct 2, 2021 Key for Compensation Amount Codes LOBBCOMPEQZERO $0 LOBBCOMP05 $100,000 - $149,999.99 LOBBCOMP10 $350,000 - $399,999.99 LOBBCOMP01 Less than $10,000 LOBBCOMP06 $150,000 - $199, 999.99 LOBBCOMP11 $400,000 - $449,999.99 LOBBCOMP02 $10,000 - $24,999.99 LOBBCOMP07 $200,000 - $249, 999.99 LOBBCOMP12 $450,000 - $499,999.99 LOBBCOMP03 $25,000 - $49,000.99 LOBBCOMP08 $250,000 - $299,999.99 LOBBCOMP13 Over $500,000 LOBBCOMP04 $50,000 - $99,999.99 LOBBCOMP09 $300,000 - $349,999.99 LOBBCOMPEXACTAMT 70358 #1 Abbott, Sean (Mr.) Attorney 100 Congress Avenue Suite 1300 Austin TX (512)4352334 MODIFIED 3 B&J Municipal Utility District c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Bell County Municipal Utility District No. 1 c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Bell County Municipal Utility District No. 2 c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Berry Creek Highlands Municipal Utility District c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Blake Magee Company 1011 North Lamar Austin TX 78704 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Block House Municipal Utility District c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Bonzo, LP 3939 Bee Caves Rd. -

Private Equity Buyouts in Healthcare: Who Wins, Who Loses? Eileen Appelbaum and Rosemary Batt Working Paper No

Private Equity Buyouts in Healthcare: Who Wins, Who Loses? Eileen Appelbaum* and Rosemary Batt† Working Paper No. 118 March 15, 2020 ABSTRACT Private equity firms have become major players in the healthcare industry. How has this happened and what are the results? What is private equity’s ‘value proposition’ to the industry and to the American people -- at a time when healthcare is under constant pressure to cut costs and prices? How can PE firms use their classic leveraged buyout model to ‘save healthcare’ while delivering ‘outsized returns’ to investors? In this paper, we bring together a wide range of sources and empirical evidence to answer these questions. Given the complexity of the sector, we focus on four segments where private equity firms have been particularly active: hospitals, outpatient care (urgent care and ambulatory surgery centers), physician staffing and emergency * Co-Director and Senior Economist, Center for Economic and Policy Research. [email protected] † Alice H. Cook Professor of Women and Work, HR Studies and Intl. & Comparative Labor ILR School, Cornell University. [email protected]. We thank Andrea Beaty, Aimee La France, and Kellie Franzblau for able research assistance. room services (surprise medical billing), and revenue cycle management (medical debt collecting). In each of these segments, private equity has taken the lead in consolidating small providers, loading them with debt, and rolling them up into large powerhouses with substantial market power before exiting with handsome returns. https://doi.org/10.36687/inetwp118 JEL Codes: I11 G23 G34 Keywords: Private Equity, Leveraged Buyouts, health care industry, financial engineering, surprise medical billing revenue cycle management, urgent care, ambulatory care. -

Investor Relations Marketing & Communications Forum

Investor Relations Marketing & Communications Forum Virtual experience 2020 September 2-3 | Available anywhere The largest global event for PE Investor Relations, Marketing & Communications A new virtual experience Customize your agenda Available anywhere Industry leading IR and Mix and match 3 think tank Enjoy the Forum from the marketing content selections, 3 interactive comfort of your home office and The Forum’s in-depth sessions are discussion rooms, 12 breakouts on-demand access for up to 12 designed to help you formulate and panel sessions to your liking months after the event is over effective plans and develop crucial for a personalize event strategies to attract investors experience A new kind of networking Built-in calendar and Networking lounges Gain early access to the attendee automated reminders Explore and meet with industry list and start scheduling 1-to-1 Easily download and sync your service providers to discover the or small group meetings or direct event agenda with preferred latest trends and technologies message fellow attendees in tracks and 1-to-1 meetings to your advance own work calendar Speakers include Marilyn Adler Nicole Adrien Christine Anderson Mary Armstrong Michael Bane Managing Partner Chief Product Officer Senior Managing Senior Vice President, Head of US Investor Mizzen Capital and Global Head of Director, Global Head Global Head of Relations Client Relations of Public Affairs & Marketing and Ardian Oaktree Capital Marketing Communications Blackstone General Atlantic Devin Banerjee Charles Bauer Gina -

Healthcare Real Estate

VALUE FOCUS REAL ESTATE Sector Focus: Healthcare Real Estate Second Quarter 2017 Healthcare Facilities 1 Macro Indicators 3 Industry Performance and M&A Activity 6 Publicly Traded Companies Hospitality 9 Residential 11 Healthcare 12 Commercial Real Estate 16 About Mercer Capital 22 www.mercercapital.com Mercer Capital’s Value Focus: Real Estate Industry Second Quarter 2017 Healthcare Facilities As of the most recent data in 2015, healthcare spending in the United States was $3.2 trillion. Average annual growth in national healthcare expenditures from 2015 to 2025 is expected to be approximately 5.6%. As a share of gross domestic product, national healthcare expenditure is expected to increase from 17.8% in 2015 to 19.9% by 2025. Demand for medical office buildings (MOBs) is driven primarily by demographic characteristics, rather than economic trends. This has contributed to more stable performance for the medical office building segment during a period when office space in general has underperformed. Consolidation continued in the industry during 2016, spurred by efforts to cut costs and offset lower insurance reimbursement rates. This trend has encouraged demand for larger office space and weakened the market for smaller, individual healthcare facilities, although ambulatory centers associated with larger hospitals are an exception. Merger and acquisition activity is expected to pick up in 2017, following an 8.0% increase in transactions in the first quarter. Of 27 transactions during the first quarter, three included organizations with revenues of $1 billion or greater. Average rents in the medical office space were $24.00 per square foot in 2016, which represents an 8.0% increase over the prior year and 8.3% above the $22.16 low observed in early 2013. -

Robert Swan Joins General Atlantic As Operating Partner

Robert Swan Joins General Atlantic as Operating Partner Former eBay CFO joins leading global growth equity firm PALO ALTO and NEW YORK - September 8, 2015 General Atlantic, a leading global growth equity firm, announced today that Robert Swan, former Chief Financial Officer of eBay, Inc., has joined General Atlantic as an Operating Partner. Mr. Swan will be part of the firm’s Resources Group, leading the firm’s efforts in supporting global portfolio companies as they grow through strategic mergers and acquisitions and develop their finance functions, as well as working with the firm’s investment team in the internet and technology sector. He will be based in General Atlantic’s Palo Alto office. “We are thrilled to have Bob join us to assist our portfolio companies in developing world-class finance organizations,” said Bill Ford, Chief Executive Officer of General Atlantic. “Beyond his extraordinary talent as a proven CFO, Bob’s deep expertise in the internet and technology sector will make him an exceptional asset to our portfolio companies and prospective new investments around the world.” General Atlantic’s Resources Group is composed of experienced senior executives who collaborate with the firm’s investment teams and portfolio companies to execute global growth strategies. The Resources Group provides functional expertise in areas such as human capital development, pricing and salesforce effectiveness, global M&A, technology, marketing, finance, tax and capital markets, and lead development through the General Atlantic Network. General Atlantic’s global team is dedicated to identifying attractive, high-growth companies and providing capital and strategic support to build market leaders. -

051820 Tractor Supply

OFFERING MEMORANDUM TRACTOR SUPPLY – HOHENWALD, TN 608 E Main Street • Hohenwald, TN 38462 Representative Photo NON- ENDORSEMENT AND DISCLAIMER NOTICE Confidentiality and Disclaimer The information contained in the following Marketing Brochure is proprietary and strictly confidential. It is intended to be reviewed only by the party receiving it from Marcus & Millichap and should not be made available to any other person or entity without the written consent of Marcus & Millichap. This Marketing Brochure has been prepared to provide summary, unverified information to prospective purchasers, and to establish only a preliminary level of interest in the subject property. The information contained herein is not a substitute for a thorough due diligence investigation. Marcus & Millichap has not made any investigation, and makes no warranty or representation, with respect to the income or expenses for the subject property, the future projected financial performance of the property, the size and square footage of the property and improvements, the presence or absence of contaminating substances, PCB's or asbestos, the compliance with State and Federal regulations, the physical condition of the improvements thereon, or the financial condition or business prospects of any tenant, or any tenant's plans or intentions to continue its occupancy of the subject property. The information contained in this Marketing Brochure has been obtained from sources we believe to be reliable; however, Marcus & Millichap has not verified, and will not verify, any of the information contained herein, nor has Marcus & Millichap conducted any investigation regarding these matters and makes no warranty or representation whatsoever regarding the accuracy or completeness of the information provided. -

Tilting Point Raises $235 Million to Fuel Expansion and Acquisitions

Tilting Point Raises $235 Million to Fuel Expansion and Acquisitions First Equity Raise Led by General Atlantic to Accelerate Company’s Progressive Game Publishing Model, M&A, International Growth New York, NY - July 20, 2021 Tilting Point, a leading free-to-play games publisher, has raised $235 million in the company’s first-ever equity financing. The funding was led by General Atlantic, a leading global growth equity firm, with participation from strategic investor Red Ventures and Kamerra. The company will use the investment to accelerate its progressive publishing model by signing more developers in live publishing, co-developing more titles, acquiring more studios and partnering with developers on top IP launches. Tilting Point will also leverage the funding to continue to expand across geographies, platforms and audiences. “We are ready to take Tilting Point to the next level,” said Kevin Segalla, founder and Co-CEO of Tilting Point. “With this financing, we plan to expand our operations and aggressively pursue larger M&A opportunities with our top developer partners. We are very excited to have premier investors coming aboard our journey.” Tilting Point has consistently accelerated success for mobile game developers (the company currently has more than 40 developer partners), scaling their games through UA funding and management, app store optimization (ASO), ad monetization, platform deployment and more, then teaming up with existing partners to deepen relationships through co-development and M&A. “We have spent years perfecting our innovative model of helping developers grow their games, working with select partners closely and bringing new studios into the Tilting Point family, all without any traditional capital funding,” said Samir Agili, president and Co-CEO of Tilting Point.