Semi-Annual Market Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

3Rd Quarter Holdings

Calvert VP Russell 2000® Small Cap Index Portfolio September 30, 2020 Schedule of Investments (Unaudited) Common Stocks — 95.2% Security Shares Value Auto Components (continued) Security Shares Value Aerospace & Defense — 0.8% LCI Industries 2,130 $ 226,398 Modine Manufacturing Co.(1) 4,047 25,294 AAR Corp. 2,929 $ 55,065 Motorcar Parts of America, Inc.(1) 1,400 21,784 Aerojet Rocketdyne Holdings, Inc.(1) 6,371 254,139 Standard Motor Products, Inc. 1,855 82,826 AeroVironment, Inc.(1) 1,860 111,619 Stoneridge, Inc.(1) 2,174 39,936 Astronics Corp.(1) 2,153 16,621 Tenneco, Inc., Class A(1)(2) 4,240 29,426 Cubic Corp. 2,731 158,862 Visteon Corp.(1) 2,454 169,866 Ducommun, Inc.(1) 914 30,089 VOXX International Corp.(1) 1,752 13,473 Kaman Corp. 2,432 94,775 Workhorse Group, Inc.(1)(2) 8,033 203,074 Kratos Defense & Security Solutions, Inc.(1) 10,345 199,452 XPEL, Inc.(1) 1,474 38,442 (1) Maxar Technologies, Inc. 5,309 132,406 $2,100,455 Moog, Inc., Class A 2,535 161,049 Automobiles — 0.1% National Presto Industries, Inc. 420 34,381 PAE, Inc.(1) 5,218 44,353 Winnebago Industries, Inc. 2,733 $ 141,214 Park Aerospace Corp. 1,804 19,700 $ 141,214 Parsons Corp.(1) 1,992 66,812 Banks — 6.8% Triumph Group, Inc. 4,259 27,726 (1) Vectrus, Inc. 987 37,506 1st Constitution Bancorp 623 $ 7,414 $ 1,444,555 1st Source Corp. 1,262 38,920 Air Freight & Logistics — 0.4% ACNB Corp. -

Steward Small-Mid Cap Enhanced Index Fund Holdings Page 2 of 25

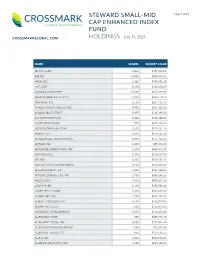

STEWARD SMALL-MID Page 1 of 25 CAP ENHANCED INDEX FUND CROSSMARKGLOBAL.COM HOLDINGS July 31, 2021 NAME SHARES MARKET VALUE 3D SYS. CORP 6,800 $187,272.00 8X8 INC 12,850 $328,446.00 AAON INC 6,268 $389,556.20 AAR CORP 4,150 $148,404.00 AARON'S CO INC/THE 10,815 $312,229.05 ABERCROMBIE & FITCH CO 6,950 $262,779.50 ABM INDS. INC 5,630 $261,738.70 ACADIA HEALTHCARE CO INC 4,990 $307,982.80 ACADIA REALTY TRUST 5,897 $126,195.80 ACI WORLDWIDE INC 6,600 $226,380.00 ACUITY BRANDS INC 1,700 $298,146.00 ADDUS HOMECARE CORP 2,630 $228,257.70 ADIENT PLC 6,040 $254,465.20 ADTALEM GBL. EDUCATION IN 4,890 $177,702.60 ADTRAN INC 2,480 $55,576.80 ADVANCED ENERGY INDS. INC 6,270 $650,512.50 ADVANSIX INC 7,020 $234,819.00 AECOM 8,222 $517,657.12 AEROJET ROCKETDYNE HLDGS. 3,960 $186,832.80 AEROVIRONMENT INC 4,880 $493,368.00 AFFILIATED MGRS. GRP. INC 2,150 $340,646.00 AGCO CORP 3,100 $409,541.00 AGILYSYS INC 6,310 $350,583.60 AGREE REALTY CORP 3,320 $249,498.00 ALAMO GRP. INC 1,790 $262,718.30 ALARM.COM HLDGS. INC 9,590 $798,079.80 ALBANY INTL. CORP 1,580 $136,433.00 ALEXANDER & BALDWIN INC 5,813 $116,376.26 ALLEGHANY CORP 687 $455,549.70 ALLEGHENY TECHS. INC 8,380 $172,041.40 ALLEGIANCE BANCSHARES INC 1,040 $37,928.80 ALLEGIANT TRAVEL CO 656 $124,718.72 ALLETE INC 3,000 $210,960.00 ALLIANCE DATA SYS. -

2019-2020 Membership

HARRY PHILLIPS AMERICAN INN OF COURT 2019-2020 MEMBERSHIP A Olatayo Atanda, Esq. Waller Lansden Dortch & Davis 511 Union Street, Suite 2700 Nashville, TN 37219 615-850-8861 [email protected] Barrister (2022) BPR No. 031007 B Kathryn Barnett, Esq. Morgan & Morgan 810 Broadway, Suite 500 Nashville, TN 37203 615-490-0944 [email protected] Master (2020) BPR No. 015361 Membership Chair Alan Stuart Bean, Esq. Starnes Davis Florie LLP 3000 Meridian Blvd., Suite 170 Franklin, TN 37067 615-905-7200 [email protected] Barrister (2022) BPR No. 026194 Raquel L. Bellamy, Esq. Bone McAllester Norton PLLC 511 Union Street, Suite 1600 Nashville, TN 37219 615-636-5781 [email protected] Barrister (2020) BPR No. 030636 Christen Blackburn, Esq. Lewis Thomason King Krieg & Waldrop 424 Church Street, Suite 2500 Nashville, TN 37219 615-574-6732 [email protected] Barrister (2021) BPR No. 027104 19 Gen. Andrée S. Blumstein Solicitor General Office of the Attorney General & Reporter P.O. Box 20207 Nashville, TN 37202-0207 615-741-3492 [email protected] Master (2023) BPR No. 009357 Counselor Seannalyn Brandmeir, Esq. State of Tennessee, Benefits Administration 1320 West Running Brook Road Nashville, TN 37209 615-532-4598 [email protected] Associate (2021) BPR No. 034158 Mr. Cole W. Browndorf [email protected] Student (2020) VU C Gen. Sarah K. Campbell Office of the Attorney General & Reporter P.O. Box 20207 Nashville, TN 37202-0207 615-532-6026 [email protected] Barrister (2021) BPR No. 034054 Rebecca McKelvey Castañeda, Esq. Stites & Harbison 401 Commerce Street, Suite 800 Nashville, TN 37219 615-782-2204 [email protected] Barrister (2022) BPR No. -

Healthcare Report 1H 2021

Investment Banking & Securities Offered Through SDR Capital Markets, Inc., Member FINRA & SIPC. ❑ ❑ ❑ ❑ ❑ ❑ 200 174 150 100 78 41 46 50 21 Financial Strategic - 52% 48% Amount TEV/ TEV/ Date Target B uyer(s) Segment ($ in Mil) Rev EB ITDA 6/25/2021 Alliance HealthCare Services Akumin Inpatient/Hospitals 820.00 - - 6/16/2021 23andM e VG Acquisition Pharma and Lab Services 3,500.00 14.2x - 6/15/2021 Springstone M edical Properties Trust Inpatient/Hospitals 950.00 - 14.1x 6/14/2021 University Health Care Cano Health Inpatient/Hospitals 600.00 - - 6/14/2021 One Homecare Solutions Humana Long Term & Behavioral Care - - - 6/7/2021 Iora Health One M edical Inpatient/Hospitals 2,100.00 - - 6/7/2021 Newport Academy Onex Inpatient/Hospitals 1,300.00 - - 6/1/2021 Veterans Evaluation Services M aximus Outpatient/Clinics 1,400.00 - - 6/1/2021 M ercy Quest Diagnostics Pharma and Lab Services - - - 5/13/2021 Redmond Regional M edical Center AdventHealth Inpatient/Hospitals 635.00 - - 5/6/2021 M eM D Walmart Outpatient/Clinics - - - 5/5/2021 Axia Women's Health Partners Group Outpatient/Clinics 800.00 - 20.0x Strategic Buyer Inv. Date Select Corporate Acquisitions IMAC Regeneration Center 6/25/2021 ▪ Active M edical Center (M edical Center) 6/14/2021 ▪ Fort Pierce Chiropractic 3/1/2021 ▪ NCH Chiropractic 2/4/2021 ▪ Willmitch Chiropractic Skylight Health Group 6/24/2021 ▪ The Doctors Center (US) 2/4/2021 ▪ River City M edical Associates 1/7/2021 ▪ Rocky M ountain Urgent Care Pennant Group 6/16/2021 ▪ First Call Hospice 5/1/2021 ▪ CardioVascular Home Care 4/1/2021 ▪ Pasco SW 1/16/2021 ▪ Sacred Heart Health LHC Group 6/2/2021 ▪ Heart of Hospice 1/5/2021 ▪ Grace Hospice of Oklahoma 1/5/2021 ▪ East Valley Hospice CRH Medical 5/27/2021 ▪ Northern Indiana Anesthesia Associates 4/1/2021 ▪ M iddle Arkansas Sedation Associates 3/14/20172/9/2021 ▪ Oak Tree Anesthesia Associates The Ensign Group 5/1/2021 ▪ WindsorDermatology Rehabilitation Center PC and Health Care Center 4/1/2021 ▪ The Ensign Group (3 Skilled Nursing Facilities in Colorado) 2/1/2021 ▪ San Pedro M anor 1/1/2021 ▪ St. -

Healthcare Market Monitor

Mergers & Acquisitions Capital Raise Strategic Advisory Healthcare Market Monitor Q1 2021 CTIVITY Q1 2021 M&A A Mergers & Acquisitions Capital Raise Strategic Advisory Highlights Total M&A Volume: Q1 2020 vs. Q1 2021 ▪ In Q1 2021, total Healthcare M&A volume was up 65.1% compared to Q1 2020. 600 515 M&A Volume ▪ The eHealth segment continues to be an attractive space with total deal 500 volume increasing by 44 transactions in Q1 2021 over Q1 2020. Physician Medical Groups also experienced a large increase in volume largely due to 400 private equity buyers or their sponsored companies targeting small 312 Notable physician groups. 300 Transactions ▪ Much of the increase in total Q1 2021 volume could be attributed to the roll- 200 out of COVID-19 vaccines and the uncertainty around presidential election subsiding. 100 Public Indexes ▪ Additionally, aggregate deal value among the segments was up 340.5% over - Q1 2020, reaching $56.8B in Q1 2021. Q1 2020 Q1 2021 M&A Volume by Segment: Q1 2020 vs. Q1 2021 HCA Overview 120 Q1 2020 110 102 95 100 Q1 2021 94 Services 77 80 58 60 49 40 35 Experience 25 28 26 18 20 17 16 17 20 20 10 4 6 0 Behavioral eHealth Home Health / Hospitals Labs / Managed Care Other Services Physician Post-acute Senior / Assisted Contact Us Health Care Hospice Diagnostics Medical Groups Care/Rehab Living Source: CapitalIQ, Healthcare M&A News 2 ELECT OTABLE CTIVITY S , N M&A A Mergers & Acquisitions Capital Raise Strategic Advisory $ in millions Announce Transaction Date Category Target Acquirer/Investor Short Description Value Mar-21 Senior / Assisted Living All Assets of Henry Ford Village, Inc. -

RRP Sector Assessment

OrbiMed Asia Partners III, LP Fund (RRP REG 51072) OWNERSHIP, MANAGEMENT, AND GOVERNANCE A. The Fund Structure 1. The Asian Development Bank (ADB) proposes to invest in OrbiMed Asia Partners III, LP Fund (OAP III), which is a Cayman Islands exempted limited partnership seeking to raise up to $500 million in capital commitments. It is managed by OrbiMed Asia GP III, LP (the general partner), a Cayman Islands exempted limited partnership. The sole limited partner of the general partner is OrbiMed Advisors III Limited, a Cayman Islands exempted company. OrbiMed Advisors LLC (the investment advisor), a registered investment advisor with the United States (US) Securities and Exchange Commission, will provide investment advisory services to OAP III. This structure is illustrated in the figure below. Table 1 shows the ultimate beneficial owners (UBOs) of the general partner and the investment advisor. Table 1: Ultimate Beneficial Owners of the General Partner and the Investment Advisor (ownership stake, %) Name Investment Advisor General Partner Sven H. Borho (~10–25%) (~8%) Alexander M. Cooper (~8%) Carl L. Gordon (~10–25%) (~8%) (also Director) Geoffrey C. Hsu (<5%) (~8%) Samuel D. Isaly (~50–75%) (~8%) W. Carter Neild (<5%) (~8%) (also Director) Jonathan T. Silverstein (~5–10%) (~8%) (also Director) Sunny Sharma (~8%) (also Officer) Evan D. Sotiriou (~8%) David G. Wang (~8%) (also Officer) Jonathan Wang (~8%) (also Officer) Sam Block III (~8%) Source: OrbiMed Group. 2 2. Investors. The fund held a first closing of approximately $233.5 million on 1 March 2017, and a second closing of approximately $137.6 million on 26 April 2017. -

Regional Economic Development Guide Tabletable of Contents

NASHVILLEREGIONAL ECONOMIC DEVELOPMENT GUIDE TABLETABLE OF CONTENTS Location 4 - 6 Economy 7 - 9 Accessibility & Transportation 10 - 11 International Business 12 - 15 Demographics 16 - 17 Talent & Workforce 18 - 25 Target Industries 26 - 27 Corporate Services 28 - 29 Health Care Management 30 - 32 Information Technology 33 - 35 Music & Entertainment 36 - 37 Advanced Manufacturing 38 - 39 Distribution & Trade 40 - 41 Livability 42 - 46 Contact Us 47 2 - TABLE OF CONTENTS TABLE OF CONTENTS - 3 LOCATIONLOCATION NASHVILLE Strategically located in the heart of the Tennessee Valley, the Nashville region is where businesses thrive and the creative spirit resonates across industries and communities. The Nashville economic market has 10 counties and a population of more than 1.9 million, making it the largest metro area in a five-state region. Many corporate headquarter giants call Nashville home, including Nissan North America, Bridgestone Americas, Dollar General, HCA Healthcare, AllianceBernstein, and Amazon. A national hub for the creative class, Nashville has the largest concentration of the music industry per capita in America. The Nashville region’s educated workforce not only provides an abundant talent pool for companies, but also bolsters the region’s vibrancy, artistic and musical essence, and Portland Springfield competitive edge in technology and Clarksville White Robertson House innovation. The Nashville region is Montgomery Sumner defined by a diverse economy, low Gallatin cost of living and doing business, a Goodlettsville Cheatham Hendersonville creative culture and a well-educated Ashland City population. Cultural diversity, unique neighborhoods, a variety of industries Charlotte Mt. Juliet Lebanon Davidson Wilson and a thriving creative community make Dickson Nashville Nashville’s economic market among the Dickson nation’s best locations for relocating, Brentwood La Vergne expanding and startup companies. -

IHI Patient Safety Congress G

IHI/NPSF Patient Safety Congress Free from Harm May 23–25, 2018 • Boston, MA Welcome ihi.org/Congress #IHICongress General Information The Learning & Simulation Download the Mobile App Center To get full details about the Patient Safety Congress, Join us in the Learning & Simulation Center including presenter biographies, download our mobile (Exhibit Hall C) for receptions, lunches, live app titled CrowdCompass Attendee Hub. The app is simulations, the Innovation Theater, exhibits, available on both Google Play and iTunes Store. Once posters, and prize drawings. you have downloaded the Attendee Hub app, search for IHI/NPSF Congress 2018 under the events tab Thank You to Our and download the event. Passcode: 2018boston Supporters and Exhibitors Internet Access Check out the Supporter Guide on page 18 During Congress, connect to: Mallinckrodt and the Exhibitor Guide on page 26. password: 2018boston Videographers and Continuing Education Photographers See page 32 to learn about earning CE and Please note that IHI will have videographers and CME credits. photographers at the Congress. We may capture your image for use on the IHI website or in other IHI materials. @TheIHI will be tweeting. Join us! Use #IHICongress. Program details are subject to change. 2 Mobile app: See the instructions on page 2. Welcome It’s been a remarkable two decades in the history of patient safety. To Err Is Human caught the public’s attention and catalyzed a movement to make care safer. IHI’s 100,000 and 5M Lives Campaigns brought thousands of hospitals together to pursue the shared goals of saving lives and eliminating harm. -

Program Npsfcongress.Org Your Vision

Program THE 15TH ANNUAL NPSF PATIENT SAFETY CONGRESS May 8–10, 2013 New Orleans DON’T MISS! Welcome Reception, Wednesday, 4:30–6:30 PM Networking Reception, Thursday, 4:45–6:45 PM In the Learning & Simulation Center Visit the NPSF PHOTO BOOTH! Share your patient safety perspectives and bring home a photo memory of your Congress experience. See NPSF at booth 107 in the Learning & Simulation Center. npsfcongress.org Please see the centerfold of this booklet for your convenient Schedule At A Glance, including locations of all events. Be sure to visit the Learning & Simulation Center in Elite Hall AB for Simulations, Exhibits, Posters, Receptions, Lunches, and Prize Drawings. Your vision. Our commitment. Together, we will move healthcare forward. Hospira shares in The National Patient Safety Foundation’s vision to improve the safety of patients and move healthcare forward. World’s leading provider of injectable drugs Hospira, Inc., 275 North Field Drive, Lake Forest, IL 60045 P13-4076-8.5x11-Apr., 13 and infusion technologies Pre-Congress May 8 | Congress May 9–10, 2013 | Hyatt Regency, New Orleans, LA Welcome to New Orleans and the 15th Annual NPSF Patient Safety Congress The NPSF Congress is the only national conference dedicated solely to patient safety, and we are honored to be hosting leading experts who are here to share emerging patient safety evidence and best practices. Whether this is your first time attending the NPSF Congress or your fifteenth, we hope that you make the most of the experience. During the next few days, there will be ample opportunities to network with the best and brightest in the industry, to learn about practical solutions to the problems you confront every day, and to acquire the knowledge and skills that can help you transform your organization’s patient safety efforts. -

THOMAS F. FRIST, JR., MD in First Person

THOMAS F. FRIST, JR., M.D. In First Person: An Oral History American Hospital Association Center for Hospital and Healthcare Administration History and Health Research & Educational Trust 2013 HOSPITAL ADMINISTRATION ORAL HISTORY COLLECTION THOMAS F. FRIST, JR., M.D. In First Person: An Oral History Interviewed by Kim M. Garber On January 17, 2013 Edited by Kim M. Garber Sponsored by American Hospital Association Center for Hospital and Healthcare Administration History and Health Research & Educational Trust Chicago, Illinois 2013 ©2013 by the American Hospital Association All rights reserved. Manufactured in the United States of America Coordinated by Center for Hospital and Healthcare Administration History AHA Resource Center American Hospital Association 155 North Wacker Drive Chicago, Illinois 60606 Transcription by Chris D‘Amico Photos courtesy of the Frist family, HCA, the American Hospital Association, Louis Fabian Bachrach, Micael-Renee Lifestyle Portraiture, Simon James Photography, and the United Way of Metropolitan Nashville EDITED TRANSCRIPT Interviewed in Nashville, Tennessee KIM GARBER: Today is Thursday, January 17, 2013. My name is Kim Garber, and I will be interviewing Dr. Thomas Frist, Jr., chairman emeritus of HCA Holdings, Inc. In the 1960s, together with his father, Dr. Thomas Frist, Sr., Dr. Frist conceived of a company that would own or manage multiple hospitals, providing high quality care and leveraging economies of scale. Founded in 1968, the Hospital Corporation of America, now known as HCA, has owned or managed hundreds of hospitals. Known as the First Family of Nashville, the Frists have made substantial contributions to Music City through their work with the Frist Foundations and other initiatives. -

Orbimed Partners

The Biotech Growth Trust Annual General Meeting July 2021 This document does not constitute an offer to sell, or the solicitation of an offer to purchase, any security or fund, including shares of the Biotech Growth Trust PLC (the “Fund”). Any such offer may only be made by means of a prospectus or other appropriate offering document. This presentation is as of the date noted above and may be changed without notice. © 2021 OrbiMed Advisors LLC. All Rights Reserved. CONFIDENTIAL 1 BIOG Performance since Inception 18 May 2005 through 30 June 2021 £1,600 £ % BIOG +1333.5% £1,400 BIOG NAV (£) NBI (£) FTSE (£) £1,200 NBI £1,000 +902.3% £800 16 Years £600 £400 FTSE +188.2% £200 £0 Source: Frostrow, Bloomberg. Note: See Endnotes for additional information, including with regard to the calculation of these results and the index shown above. BIOG June NAV return figures are estimates as provided by Frostrow/Morningstar as of July 1, 2021. © 2021 OrbiMed Advisors LLC. All Rights Reserved. CONFIDENTIAL 2 Proven Health Flexible 25+ year strong 100% healthcare, Investing across returns across including stages, sub- public and private biopharma, devices, sectors, equity and debt Global diagnostics, digital Leader geographies and markets health, services capital structures 11 locations, ~$20 billion AUM including New York, ~100 San Francisco, professionals Hong Kong, Shanghai, Mumbai, ~15 former Herzliya CEOs/founders 128 20+ 30 Global New Hires Colleagues with Employees in 2020/21 M.D. / Ph.D. Past performance is no guarantee of future results. Assets Under Management estimated as of 30 June 2021 © 2021 OrbiMed Advisors LLC. -

Healthcare Disruptive Technologies & Innovations

22 March 2020 Equity Research Americas | United States Healthcare Technology 3rd Healthcare Disruptive Technologies & Innovations (HCDT&I) Virtual Day Recap Healthcare Technology & Distribution | Management Meeting Last week, we hosted our 3rd Healthcare Disruptive Technologies & Innovations (HCDT&I) day Research Analysts virtually. Presenters included executives from Altruista Health, Buoy Health, Livongo, Quartet Health, Somatus, Welltok, Iora Health, and Heal. We also hosted sessions with Will Brady, the Jailendra Singh Chief of Staff to HHS Deputy Secretary, and Dr. Sylvia Romm, Atlantic Health System’s CIO. 212 325 8121 [email protected] Technology Playing a Critical Role in Dealing with the COVID-19 Pandemic. Dealing with the COVID-19 pandemic was a key discussion topic at our HCDT&I day. Jermaine Brown Artificial Intelligence (AI) focused companies, such as Buoy Health, released a COVID-19 212 325 8125 screening tool that took the CDC guidelines and layered them on top of the AI. Companies [email protected] such as Livongo and Somatus serve chronic care populations, which are most vulnerable to Adam Heussner the coronavirus. Their role and solutions in these circumstances vary from helping members 212 325 4727 manage stress/anxiety to sharing a detailed picture of member’s underlying conditions with [email protected] the appropriate provider to best inform the treatment (if needed). Livongo has not seen any disruption to date in sales activity. Quartet Health, which serves individuals with mental health conditions, is focused on the rapid acceleration of digital care options to help its members deal with fear and anxiety related to the pandemic.