Healthcare Disruptive Technologies & Innovations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

3Rd Quarter Holdings

Calvert VP Russell 2000® Small Cap Index Portfolio September 30, 2020 Schedule of Investments (Unaudited) Common Stocks — 95.2% Security Shares Value Auto Components (continued) Security Shares Value Aerospace & Defense — 0.8% LCI Industries 2,130 $ 226,398 Modine Manufacturing Co.(1) 4,047 25,294 AAR Corp. 2,929 $ 55,065 Motorcar Parts of America, Inc.(1) 1,400 21,784 Aerojet Rocketdyne Holdings, Inc.(1) 6,371 254,139 Standard Motor Products, Inc. 1,855 82,826 AeroVironment, Inc.(1) 1,860 111,619 Stoneridge, Inc.(1) 2,174 39,936 Astronics Corp.(1) 2,153 16,621 Tenneco, Inc., Class A(1)(2) 4,240 29,426 Cubic Corp. 2,731 158,862 Visteon Corp.(1) 2,454 169,866 Ducommun, Inc.(1) 914 30,089 VOXX International Corp.(1) 1,752 13,473 Kaman Corp. 2,432 94,775 Workhorse Group, Inc.(1)(2) 8,033 203,074 Kratos Defense & Security Solutions, Inc.(1) 10,345 199,452 XPEL, Inc.(1) 1,474 38,442 (1) Maxar Technologies, Inc. 5,309 132,406 $2,100,455 Moog, Inc., Class A 2,535 161,049 Automobiles — 0.1% National Presto Industries, Inc. 420 34,381 PAE, Inc.(1) 5,218 44,353 Winnebago Industries, Inc. 2,733 $ 141,214 Park Aerospace Corp. 1,804 19,700 $ 141,214 Parsons Corp.(1) 1,992 66,812 Banks — 6.8% Triumph Group, Inc. 4,259 27,726 (1) Vectrus, Inc. 987 37,506 1st Constitution Bancorp 623 $ 7,414 $ 1,444,555 1st Source Corp. 1,262 38,920 Air Freight & Logistics — 0.4% ACNB Corp. -

Steward Small-Mid Cap Enhanced Index Fund Holdings Page 2 of 25

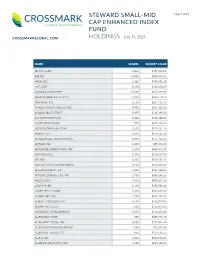

STEWARD SMALL-MID Page 1 of 25 CAP ENHANCED INDEX FUND CROSSMARKGLOBAL.COM HOLDINGS July 31, 2021 NAME SHARES MARKET VALUE 3D SYS. CORP 6,800 $187,272.00 8X8 INC 12,850 $328,446.00 AAON INC 6,268 $389,556.20 AAR CORP 4,150 $148,404.00 AARON'S CO INC/THE 10,815 $312,229.05 ABERCROMBIE & FITCH CO 6,950 $262,779.50 ABM INDS. INC 5,630 $261,738.70 ACADIA HEALTHCARE CO INC 4,990 $307,982.80 ACADIA REALTY TRUST 5,897 $126,195.80 ACI WORLDWIDE INC 6,600 $226,380.00 ACUITY BRANDS INC 1,700 $298,146.00 ADDUS HOMECARE CORP 2,630 $228,257.70 ADIENT PLC 6,040 $254,465.20 ADTALEM GBL. EDUCATION IN 4,890 $177,702.60 ADTRAN INC 2,480 $55,576.80 ADVANCED ENERGY INDS. INC 6,270 $650,512.50 ADVANSIX INC 7,020 $234,819.00 AECOM 8,222 $517,657.12 AEROJET ROCKETDYNE HLDGS. 3,960 $186,832.80 AEROVIRONMENT INC 4,880 $493,368.00 AFFILIATED MGRS. GRP. INC 2,150 $340,646.00 AGCO CORP 3,100 $409,541.00 AGILYSYS INC 6,310 $350,583.60 AGREE REALTY CORP 3,320 $249,498.00 ALAMO GRP. INC 1,790 $262,718.30 ALARM.COM HLDGS. INC 9,590 $798,079.80 ALBANY INTL. CORP 1,580 $136,433.00 ALEXANDER & BALDWIN INC 5,813 $116,376.26 ALLEGHANY CORP 687 $455,549.70 ALLEGHENY TECHS. INC 8,380 $172,041.40 ALLEGIANCE BANCSHARES INC 1,040 $37,928.80 ALLEGIANT TRAVEL CO 656 $124,718.72 ALLETE INC 3,000 $210,960.00 ALLIANCE DATA SYS. -

Healthcare Market Monitor

Mergers & Acquisitions Capital Raise Strategic Advisory Healthcare Market Monitor Q1 2021 CTIVITY Q1 2021 M&A A Mergers & Acquisitions Capital Raise Strategic Advisory Highlights Total M&A Volume: Q1 2020 vs. Q1 2021 ▪ In Q1 2021, total Healthcare M&A volume was up 65.1% compared to Q1 2020. 600 515 M&A Volume ▪ The eHealth segment continues to be an attractive space with total deal 500 volume increasing by 44 transactions in Q1 2021 over Q1 2020. Physician Medical Groups also experienced a large increase in volume largely due to 400 private equity buyers or their sponsored companies targeting small 312 Notable physician groups. 300 Transactions ▪ Much of the increase in total Q1 2021 volume could be attributed to the roll- 200 out of COVID-19 vaccines and the uncertainty around presidential election subsiding. 100 Public Indexes ▪ Additionally, aggregate deal value among the segments was up 340.5% over - Q1 2020, reaching $56.8B in Q1 2021. Q1 2020 Q1 2021 M&A Volume by Segment: Q1 2020 vs. Q1 2021 HCA Overview 120 Q1 2020 110 102 95 100 Q1 2021 94 Services 77 80 58 60 49 40 35 Experience 25 28 26 18 20 17 16 17 20 20 10 4 6 0 Behavioral eHealth Home Health / Hospitals Labs / Managed Care Other Services Physician Post-acute Senior / Assisted Contact Us Health Care Hospice Diagnostics Medical Groups Care/Rehab Living Source: CapitalIQ, Healthcare M&A News 2 ELECT OTABLE CTIVITY S , N M&A A Mergers & Acquisitions Capital Raise Strategic Advisory $ in millions Announce Transaction Date Category Target Acquirer/Investor Short Description Value Mar-21 Senior / Assisted Living All Assets of Henry Ford Village, Inc. -

The State of the Mental Health Marketplace

The State of the Mental Health Marketplace A Report for Employers Seeking to Implement High- Value Mental Health Strategies Table of Contents INTRODUCTION ........................................................................................ 3 HISTORY OF MENTAL HEALTH CARE IN THE U.S. ................................................... 4 A FOCUS ON MORE COMMON MENTAL HEALTH ISSUES ............................................ 4 ENSURING SUFFICIENT ACCESS TO MENTAL HEALTH CARE ....................................... 5 MEASURING AND IMPROVING QUALITY OF CARE ................................................... 8 PUSHING FOR A HOLISTIC, INTEGRATED APROACH ............................................... 10 NEXT STEPS AND ADDITIONAL RESOURCES FOR EMPLOYERS..................................... 13 APPENDIX: MENTAL HEALTH TREATMENT OPTIONS .............................................. 14 Thank you to CPR’s Contributors whose support helped make this report possible. Note: Contributors did not have direct editorial input into the content presented here within. “Improving access, quality, and integration with medical care are key areas to consider for an improved mental health experience.” Over the past several years, mental health has started to gain the attention it deserves as an essential element of our overall health and productivity. The INTRODUCTION prevalence of mental health conditions reached an all-time high in 2016, when 44.7 million Americans reported living with a mental illness. This translates to nearly one in five people. As a result, the U.S. spends over $201 billion annually on treatment for mental health conditions, and yet, mental illness still costs the country $193 billion in lost earnings and productivity each year. We are either not spending enough or not deriving value from what we do spend. For all these reasons, employers and other health care purchasers have made mental health a priority. However, even the most committed purchasers face sizable barriers to delivering high-value mental health care to the members of their populations. -

American Enterprise Institute Health Care That Matters: Real Choices For

American Enterprise Institute Health care that matters: Real choices for real competition Introduction: Thomas P. Miller, AEI Address: Promoting choice and competition Brian Blase, National Economic Council Panel I: Revisiting and redefining choice and competition Panelists: Jeff Goldsmith, Navigant Healthcare Mark Hall, Wake Forest University Scott Harrington, University of Pennsylvania David Hyman, Georgetown University Barak Richman, Duke Law School Moderator: Thomas P. Miller, AEI Panel II: Can choice and competition theories work in practice? Panelists: Rajiv Bhatt, HCG Cancer Centre India Neil de Crescenzo, Change Healthcare Lewis Levy, Teladoc Health Tony Miller, Bind Thomas Moriarty, CVS Health Moderator: Regina Herzlinger, Harvard Business School Introduction: Michael R. Strain, AEI Address: A new direction for health care: Choice and competition Alex Azar, US Department of Health and Human Services Discussion and Q&A: Alex Azar, US Department of Health and Human Services Thomas P. Miller, AEI 9:00 a.m.–12:50 p.m. Tuesday, December 4, 2018 Event Page: http://www.aei.org/events/health-care-that-matters-real-choices- for-real-competition Thomas P. Miller: Good morning, everyone. Welcome to the American Enterprise Institute. Our conference today is “Health care that matters: Real choices for real competition.” I’m Tom Miller, chief entertainment critic for health policy here at AEI. Here’s what we’re going to do today. Yesterday, the Trump administration released its multi- departmental report on reforming America’s health care system through choice and competition. We’ll start with an address by Brian Blase, the White House adviser on health policy at the National Economic Council, about how the report came about, why it’s needed, and what sort of policy reforms based on greater choice in competition could help provide higher-quality health care at more affordable prices. -

Integrated Benefits Institute Members September 2019 1,200+ Member Organizations Stakeholder • Abbvie • Prudential Financial, Inc

Integrated Benefits Institute Members September 2019 1,200+ member organizations Stakeholder • Abbvie • Prudential Financial, Inc. • AMGEN • Sanofi • Anthem, Inc. • Sedgwick • Aon • Standard Insurance • Buck • Sun Life Financial • Cigna • Teladoc Health • Exact Sciences • The Hartford • Health Care Service Corporation • Trion-MMA • Lincoln Financial Group • UnitedHealthcare • Mercer • UPMC WorkPartners • Novo Nordisk • Willis Towers Watson • Pfizer • Zurich Charter • Alliant Insurance Services • Metropolitan Life Insurance Company • Broadspire • PhRMA • Curant Health • ReedGroup • ESIS • Reliance Standard/Matrix Absence Management • Hologic • The Guardian Life Insurance Company • Lockton Companies • York • Merck Associate • AbsenceSoft • Symetra Life • ComPsych • Unum Group • Gallagher Benefit Services • USI Insurance Services • Kentuckiana Health Collaborative • Virgin Pulse • Pacific Resources Benefit Advisors • Voya Financial • Piper Jordan • Walgreens • Spring Consulting Group Affiliate • Abbott • Hello Heart • CoreHealth Technologies • Hinge Health • DiagnoEconomics • Inspera • EPIC (Edgewood Partners) • Kaiser Permanente • Genentech • National Pharmaceutical Council • GlaxoSmithKline • PA Chamber Insurance • Health Data & Management Solutions • Precision for Value (HDMS) • Healthstat Inc Integrated Benefits Institute Members September 2019 Employers • 24 Hour Fitness USA, Inc. • AmeriGas, Inc. • AAA Club Alliance • Ampla Health • ABM • Amy's Kitchen, Inc. • ABQ Health Partners • ANSYS, Inc. • Accenture AG • Apicore US LLC • Accident -

SILVANT LARGE-CAP GROWTH STOCK FUND SCHEDULE of INVESTMENTS (Unaudited) SEPTEMBER 30, 2020

SILVANT LARGE-CAP GROWTH STOCK FUND SCHEDULE OF INVESTMENTS (Unaudited) SEPTEMBER 30, 2020 ($ reported in thousands) Shares Value Shares Value Shares Value COMMON STOCKS—100.1% Health Care—continued Information Technology—continued Becton Dickinson and Co. 1,781 $ 414 Mastercard, Inc. Class A 8,546 $ 2,890 Communication Services—14.2% (1) Bristol-Myers Squibb Co. 18,444 1,112 Microsoft Corp. 58,926 12,394 Alphabet, Inc. Class A 2,382 $ 3,491 (1) (1) DexCom, Inc. 3,440 1,418 NVIDIA Corp. 6,542 3,541 Alphabet, Inc. Class C 2,461 3,617 Edwards Lifesciences Paycom Software, Inc.(1) 2,381 741 Comcast Corp. Class A 35,594 1,646 (1) (1) Corp. 22,646 1,808 QUALCOMM, Inc. 19,739 2,323 Facebook, Inc. Class A 19,018 4,981 (1) (1) (1) Exact Sciences Corp. 9,375 956 salesforce.com, Inc. 9,882 2,484 Netflix, Inc. 4,849 2,425 Insulet Corp.(1) 2,083 493 Splunk, Inc.(1) 4,573 860 Walt Disney Co. (The) 4,476 555 Intuitive Surgical, Inc.(1) 1,698 1,205 Twilio Inc. Class A(1) 2,153 532 16,715 Mettler-Toledo Universal Display Corp. 5,383 973 International, Inc.(1) 1,234 1,192 Visa, Inc. Class A 24,444 4,888 Consumer Discretionary—15.7% Teladoc Health, Inc.(1) 5,332 1,169 Workday, Inc. Class A(1) 7,188 1,546 (1) Amazon.com, Inc. 3,472 10,932 Thermo Fisher Scientific, 50,319 Chipotle Mexican Grill, Inc. 1,776 784 (1) Inc. 724 901 UnitedHealth Group, Inc. -

Telehealth Research Analysts COMMENT Jailendra Singh 212 325 8121 [email protected] Review of 2019 Employer Benefit Guides A.J

17 January 2019 Americas/United States Equity Research Managed Care & Healthcare Facilities Telehealth Research Analysts COMMENT Jailendra Singh 212 325 8121 [email protected] Review of 2019 Employer Benefit Guides A.J. Rice 212 325 8134 ■ We have conducted a review of 2019 Employer Benefit Guides in an [email protected] effort to better understand the competitive environment for Eduardo Ron Telehealth. We analyzed 145 open enrollment benefit guides (including 212 325 7491 many from the Fortune 100). This note summarizes the key themes [email protected] emerging for 2019, and we have developed a spreadsheet that tracks the Caleb Harris, CPA changes we have seen for Teladoc Health, the lone public company in the 212 325 7458 [email protected] space currently. Please e-mail us if you want access to the detailed spreadsheet summarizing our findings from the employer guides (not just those relevant to TDOC) we have reviewed. ■ Telehealth Offerings Steady in Large Employer Market. The large group employer market is highly penetrated, underscoring our view that any benefit of incremental telehealth adoption remains limited. Additionally, large employers seem to be maintaining the status quo on telehealth offerings, underscoring the sticky nature of these contracts. We have come across a few instances where large employers have narrowed the number of telehealth vendors (if contracted directly). For example, Home Depot offered Teladoc Health and Doctor on Demand to its employees in 2018 but is offering only Teladoc Health in 2019. Additionally, in the majority of cases, large employers continue to rely on their medical plans for telehealth offerings (instead of contracting directly). -

Integrated Benefits Institute Member List January 2021 1230+ MEMBER ORGANIZATIONS

1901 Harrison Street, Suite 1100 Oakland California 94612 415-222-7280 www.ibiweb.org Integrated Benefits Institute Member List January 2021 1230+ MEMBER ORGANIZATIONS STAKEHOLDERS • AbbVie • Pfizer • Aflac • Prudential Financial, Inc. • AMGEN • Sedgwick • Anthem, Inc. • Standard Insurance • Aon • Sun Life Financial • Arthur J. Gallagher & Co. • Teladoc Health • Exact Sciences • The Guardian Life Insurance • Health Care Service Corporation Company of America/ReedGroup • Johnson & Johnson • The Hartford • Lincoln Financial Group • Trion-MMA • Lockton Companies • UnitedHealthcare • Mercer • UPMC WorkPartners • Novo Nordisk • Willis Towers Watson CHARTERS • AbleTo • New York Life • Alliant Insurance Services • PhRMA • Broadspire • Reliance Standard/Matrix Absence • ESIS Management • Merck • Walgreens • Metropolitan Life Insurance Company ASSOCIATES • Buck • Piper Jordan • Kaiser Permanente • Sera Prognostics • Pacific Resources Benefit Advisors, • Spring Consulting Group LLC • Voya Financial 1901 Harrison Street, Suite 1100 Oakland California 94612 415-222-7280 www.ibiweb.org AFFILIATES • Amazon Disability Leave Services • Heron Therapeutics • CoreHealth Technologies • Inspera Health • Curant Health • Mayo Clinic • EPIC (Edgewood Partners Insurance • Precision for Value Center) • Quantum Health • Erie Insurance Group • Sleepcharge by Nox Health • Evive Health • SWORD Health • Genentech, Inc. • Vida Health • GlaxoSmithKline • Wellthy • Headversity • Health Data & Management Solutions (HDMS) EMPLOYERS • Aleris • 24 Hour Fitness USA, Inc. • -

Usef-I Q2 2021

Units Cost Market Value U.S. EQUITY FUND-I U.S. Equities 88.35% Domestic Common Stocks 10X GENOMICS INC 5,585 868,056 1,093,655 1ST SOURCE CORP 249 9,322 11,569 2U INC 301 10,632 12,543 3D SYSTEMS CORP 128 1,079 5,116 3M CO 11,516 2,040,779 2,287,423 A O SMITH CORP 6,897 407,294 496,998 AARON'S CO INC/THE 472 8,022 15,099 ABBOTT LABORATORIES 24,799 2,007,619 2,874,948 ABBVIE INC 17,604 1,588,697 1,982,915 ABERCROMBIE & FITCH CO 1,021 19,690 47,405 ABIOMED INC 9,158 2,800,138 2,858,303 ABM INDUSTRIES INC 1,126 40,076 49,938 ACACIA RESEARCH CORP 1,223 7,498 8,267 ACADEMY SPORTS & OUTDOORS INC 1,036 35,982 42,725 ACADIA HEALTHCARE CO INC 2,181 67,154 136,858 ACADIA REALTY TRUST 1,390 24,572 30,524 ACCO BRANDS CORP 1,709 11,329 14,749 ACI WORLDWIDE INC 6,138 169,838 227,965 ACTIVISION BLIZZARD INC 13,175 839,968 1,257,422 ACUITY BRANDS INC 1,404 132,535 262,590 ACUSHNET HOLDINGS CORP 466 15,677 23,020 ADAPTHEALTH CORP 1,320 39,475 36,181 ADAPTIVE BIOTECHNOLOGIES CORP 18,687 644,897 763,551 ADDUS HOMECARE CORP 148 13,034 12,912 ADOBE INC 5,047 1,447,216 2,955,725 ADT INC 3,049 22,268 32,899 ADTALEM GLOBAL EDUCATION INC 846 31,161 30,151 ADTRAN INC 892 10,257 18,420 ADVANCE AUTO PARTS INC 216 34,544 44,310 ADVANCED DRAINAGE SYSTEMS INC 12,295 298,154 1,433,228 ADVANCED MICRO DEVICES INC 14,280 895,664 1,341,320 ADVANSIX INC 674 15,459 20,126 ADVANTAGE SOLUTIONS INC 1,279 14,497 13,800 ADVERUM BIOTECHNOLOGIES INC 1,840 7,030 6,440 AECOM 5,145 227,453 325,781 AEGLEA BIOTHERAPEUTICS INC 287 1,770 1,998 AEMETIS INC 498 6,023 5,563 AERSALE CORP -

Add Presentation Title

State of Wisconsin Deferred Compensation Plan Investment Performance and Expense Ratio Review Performance as of December 31, 2019 Bill Thornton Investment Director, Great-West Investments 303-737-1514 [email protected] FOR FINANCIAL PROFESSIONAL USE ONLY. Table of Contents 1) Executive Summary 2) Target Date Summary 3) Expense Ratio Information 4) Fund Analysis 5) Capital Markets Overview 6) Appendix FOR FINANCIAL PROFESSIONAL USE ONLY. 2 Executive Summary Wisconsin Deferred Compensation Program – Asset Class Coverage Core "Doers" Stable Value/ Large Cap Large Cap Large Cap Global/ Fixed Income Mid Cap Small Cap Money Market Value Core Growth International FDIC Bank Option, BlackRock US Debt American Beacon Vanguard Fidelity Contrafund BlackRock Mid Cap BlackRock Russell American Funds Vanguard Treasury Index, Federated US Bridgeway Large Cap Institutional 500 Commingled Pool, Equity Index, T.Rowe 2000 Index, DFA US Europacific Growth, Money Market, Gov Securities, Value Trust Index Calvert U.S. Core Price Instl Mid-Cap Micro Cap Blackrock EAFE Stable Value Fund Vanguard Long-Term Large Cap Resp Idx Equity Equity Index Investment Grade, Dodge & Cox Income Asset Allocation "Delegators" Balanced/Lifestyle/Lifecycle Managed Accounts Vanguard Target Retirement Trusts, Vanguard Wellington Professional Management Program - Ibbotson Specialty "Sophisticates" Brokerage Other Company Stock Schwab This graph is intended to show generally the anticipated relationship between various asset classes and the corresponding funds within each asset class available through your plan. Please note this is not intended to predict an actual level of return or risk for these funds. The historical returns and risk for these funds may vary significantly from the linear relationship represented above. -

Investment Holdings As of June 30, 2019

Investment Holdings As of June 30, 2019 Montana Board of Investments | Portfolio as of June 30, 2019 Transparency of the Montana Investment Holdings The Montana Board of Investment’s holdings file is a comprehensive listing of all manager funds, separately managed and commingled, and aggregated security positions. Securities are organized across common categories: Pension Pool, Asset Class, Manager Fund, Aggregated Individual Holdings, and Non-Pension Pools. Market values shown are in U.S. dollars. The market values shown in this document are for the individual investment holdings only and do not include any information on accounts for receivables or payables. Aggregated Individual Holdings represent securities held at our custodian bank and individual commingled accounts. The Investment Holdings Report is unaudited and may be subject to change. The audited Unified Investment Program Financial Statements, prepared on a June 30th fiscal year-end basis, will be made available once the Legislative Audit Division issues the Audit Opinion. Once issued, the Legislative Audit Division will have the Audit Opinion available online at https://www.leg.mt.gov/publications/audit/agency-search-report and the complete audited financial statements will also be available on the Board’s website http://investmentmt.com/AnnualReportsAudits. Additional information can be found at www.investmentmt.com Montana Board of Investments | Portfolio as of June 30, 2019 2 Table of Contents Consolidated Asset Pension Pool (CAPP) 4 CAPP - Domestic Equities 5 CAPP - International