After Gobbling up Motorola, Lenovo Becomes Third-Biggest Smartphone Maker

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

For Immediate Release

For Immediate Release Terrapass scores touchdown with Lyft to Offset Carbon Emissions at University of Michigan Football Games Houston, Texas – October 6, 2017: Terrapass, a member of the Just Energy Group, and a leader in the fight against climate change, has partnered with Lyft, the fastest growing on-demand transportation service in the US, to offset carbon emissions associated with travel for all University of Michigan football games for the 2017/2018 season. Michigan Stadium, located in Ann Arbor, is the largest stadium in the United States and home to the Michigan Wolverines. It’s also the second largest stadium in the world. Patrons travelling to the stadium can play an important part in helping the environment simply by selecting Lyft as their choice of transportation to and from the venue for football games. Every single Lyft ride in Ann Arbor on game day will be balanced with carbon offsets that terrapass will purchase. In fact, terrapass will not only offset travel in Ann Arbor during Michigan football home games, but away games, as well. The carbon offsets will be sourced from a local project, the South Kent Landfill in Byron Center, MI. For the Michigan Wolverine’s first home game, Lyft offset more than 10,000 miles! "We realize that game day can put a large strain on the physical environment of Ann Arbor, and we want to do our part to reduce the impact. Lyft believes in the power of rideshare to not only reduce congestion, but build community. We’re proud to partner with terrapass to help the Ann Arbor community while reinforcing to passengers that it matters how you get there, said Elliot Darvick, General Manager for Lyft in Southeast Michigan. -

Just Energy and Lyft Join Forces on Facebook

Just Energy and Lyft Join Forces on Facebook January 21, 2019 Joint Marketing to Offer Promotional Deals for Houston, Texas Customers HOUSTON, Jan. 21, 2019 (GLOBE NEWSWIRE) -- Just Energy, a leading consumer company focused on essential needs including electricity and natural gas commodities, health and well-being products, and utility conservation, is pleased to announce a new joint marketing partnership with Lyft, whose mission is to improve people's lives with the world's best transportation. Customers can now get free rides along with their energy plan, increasing the benefit and convenience of being a Just Energy customer. Free Nights, Free Rides. Customers that sign up for the promotional Nights Free plan will receive a $50 credit in their Lyft account. With 24 or 36-month term options, Nights Free customers can sleep easy knowing that their energy supply charges incurred between 9pm and 7am will be credited on their bill. With this promotional offer, customers get more of what they want - free usage during the evening hours and the convenience of on-demand rides with Lyft up to $50. “At Just Energy, we believe in creating products and services that make our customers’ lives easier,” says Pat McCullough, Chief Executive Officer at Just Energy. “We are excited to partner with Lyft and provide the added value of free rides when signing up for our Nights Free or Basics promotional plans. This offer embodies our mission of being Trusted Advisors, giving our customers the most in terms of value and convenience.” The promotion is being rolled out in the Houston, Texas market. -

Exploration of the Current State and Directions of Dynamic Ridesharing Joseph J

Montclair State University Montclair State University Digital Commons Theses, Dissertations and Culminating Projects 8-2015 Exploration of the Current State and Directions of Dynamic Ridesharing Joseph J. Di Gianni Montclair State University Follow this and additional works at: https://digitalcommons.montclair.edu/etd Part of the Environmental Sciences Commons Recommended Citation Di Gianni, Joseph J., "Exploration of the Current State and Directions of Dynamic Ridesharing" (2015). Theses, Dissertations and Culminating Projects. 187. https://digitalcommons.montclair.edu/etd/187 This Dissertation is brought to you for free and open access by Montclair State University Digital Commons. It has been accepted for inclusion in Theses, Dissertations and Culminating Projects by an authorized administrator of Montclair State University Digital Commons. For more information, please contact [email protected]. EXPLORATION OF THE CURRENT STATE AND DIRECTIONS OF DYNAMIC RIDESHARING A DISSERTATION Submitted to the Faculty of Montclair State University in partial fulfillment of the requirements for the degree of Doctor of Philosophy by JOSEPH J. DI GIANNI Montclair State University Montclair, NJ 2015 Dissertation Chair: Dr. Rolf Sternberg Copyright © 2015 by Joseph J. Di Gianni. All rights reserved. MONTCLAIR STATE UNIVERSITY THE GRADUATE SCHOOL DISSERTATION APPROVAL We hereby approve the Dissertation EXPLORATION OF THE CURRENT STATE AND DIRECTIONS OF DYNAMIC RIDESHARING of Joseph J. Di Gianni Candidate for the Degree: Doctor ofPhilosophy Dissertation Committee: Department ofEarth and Environmental Studies Dr. RolfSter^eT^ Certified by: Dissertation.Chair Dr. Joan C. Ficke Dr. Gregory Pope Dean ofThe Graduate School Date Dr. Harbans^nsh . Joseph Mirabella ABSTRACT EXPLORATION OF THE CURRENT STATE AND DIRECTIONS OF DYNAMIC RIDSHAREING by Joseph J. -

Painting the Future

Stanford eCorner Painting the Future Ann Miura-Ko, Floodgate 26-08-2020 URL: https://ecorner.stanford.edu/in-brief/painting-the-future/ Stanford Management Science and Engineering lecturer and Floodgate founding partner Ann Miura-Ko explains why she made a crucial early investment in Zimride, which later became Lyft. Founders John Zimmer and Logan Green, she recalls, were able to paint a compelling vision of the future in which better transportation options would enable more efficient communities. Transcript - Back in, I think it was 2010 00:00:07,700 is when John and Logan came to pitch Floodgate on what was originally called Zimride.. And Zimride was a platform that enabled carpooling for corporations, as well as universities.. And the vision of the world that they actually painted, actually describes a lot of what Lyft does today.. And so this is sort of a good example of mission-driven founders who really believe in a vision of the future, and how that transcends different products.. So the message that John and Logan came to Floodgate with in the early days, was look, we believe actually transportation is about to change.. The fact that we have social networks now, and people can be connected to one another digitally actually implies something really fundamentally different.. And when transportation changes, actually the world changes.. And they demonstrated this in just the United States alone, if you look at the fabric of society, you would have canals, you would have railways, and then you would have highways.. And if you just look at the map of where cities developed, it was very true that waterways, railways, and highways were actually the ways in which cities were created. -

Spring 2019 Mu Chapter of Sigma Pi Fraternity

the MUSE SPRING 2019 Mu Chapter of Sigma Pi Fraternity TOP LEFT: Slater Goodman ’18 (far right) and Sigma Pi seniors at the senior lacrosse tailgate in spring 2018, hosted by Jarett Wait ’80. TOP RIGHT (L–R): (front) Steve Bergh ’79, Jolene Kraker (Cornell ’77), Sandy Kraker ’74, Landon Budenholzer ’19, Sam Barnum www.sigmapicornell.org ’19; (back) Pete Wright ’77, Jim Franz ’77, Mark Sullivan ’77, Alec Jautz ’22, Ari Perlmutter ’19, Jack D’Agostino ’19. MIDDLE: holiday party (L–R): Sam Barnum ’19, Ian Atkinson ’20, Cameron Peterson ’20, Jet Hardie ’21. BOttOM: fall formal 2018. Please Support DINING and LEARNING for the 21ST CENTURY KITCHEN AND DINING FACILITIES UPDATE CAMPAIGN AND PROJECT HIGHLIGHTS: By Steve Pirozzi ’80 ✚ More than $521,000 has been raised out of the $650,000 project goal ✚ Mu Chapter’s Educational Foundation has committed a $60,000 The Dining and Learning (D&L) project is now at the grant toward the project stage where the final punch-list items are being identified, ✚ More than 200 alumni have already contributed discussed, and addressed. There was an unexpected delay, ✚ 100% of undergraduates have already contributed caused by a mistake in the manufacture of the new dining ✚ Construction was completed in summer 2018 room exit door, so that the door needed to be re-manufac- ✚ Building and renovation work includes upgrades to all kitchen and tured. Once all details are finalized and the pending work is meal-service equipment, the new Adolphus “Dolly” C. Hailstork Din- completed, we will negotiate final costs and make final pay- ing Room, and the new Learning Commons ments to the contractors. -

Declaration of Salvatore J. Graziano in Support of (I) Lead Plaintiff's Motion

4:14-cv-11191-LVP-MKM Doc # 102 Filed 03/09/16 Pg 1 of 64 Pg ID 3552 UNITED STATES DISTRICT COURT EASTERN DISTRICT OF MICHIGAN SOUTHERN DIVISION NEW YORK STATE TEACHERS’ Civil Case No. 4:14-cv-11191 RETIREMENT SYSTEM, Individually and on Behalf of All Other Persons Honorable Linda V. Parker Similarly Situated, Plaintiff, v. GENERAL MOTORS COMPANY, DANIEL F. AKERSON, NICHOLAS S. CYPRUS, CHRISTOPHER P. LIDDELL, DANIEL AMMANN, CHARLES K. STEVENS, III, MARY T. BARRA, THOMAS S. TIMKO, and GAY KENT Defendants. DECLARATION OF SALVATORE J. GRAZIANO IN SUPPORT OF (I) LEAD PLAINTIFF’S MOTION FOR FINAL APPROVAL OF SETTLEMENT AND PLAN OF ALLOCATION, AND (II) LEAD COUNSEL’S MOTION FOR AN AWARD OF ATTORNEYS’ FEES AND REIMBURSEMENT OF LITIGATION EXPENSES 4:14-cv-11191-LVP-MKM Doc # 102 Filed 03/09/16 Pg 2 of 64 Pg ID 3553 TABLE OF CONTENTS I. INTRODUCTION ........................................................................................... 1 II. PROSECUTION OF THE ACTION ............................................................... 5 A. Background ........................................................................................... 5 B. The Preparation And Filing Of The Complaint .................................... 7 C. Defendants’ Motion To Dismiss And Lead Plaintiff’s Opposition ...........................................................................................15 D. Additional Lead Plaintiff Briefing ......................................................20 E. Lead Plaintiff’s Successful Motion For Partial Modification Of The -

Consolidated Class Action Complaint

1 Thomas L. Laughlin, IV (pro hac vice) Jonathan M. Zimmerman (pro hac vice) 2 SCOTT+SCOTT ATTORNEYS AT LAW LLP The Helmsley Building 3 230 Park Avenue, 17th Floor New York, NY 10169 4 Telephone: 212/223-6444 212/223-6334 (fax) 5 [email protected] [email protected] 6 John T. Jasnoch (CA 281605) 7 SCOTT+SCOTT ATTORNEYS AT LAW LLP 600 W. Broadway, Suite 3300 8 San Diego, CA 92101 Telephone: 619-233-4565 9 Facsimile: 619-233-0508 [email protected] 10 James I. Jaconette (CA 179565) 11 ROBBINS GELLER RUDMAN & DOWD LLP 665 West Broadway, Suite 1900 12 San Diego, CA 92101-8498 Telephone: 619-231-1058 13 Facsimile: 619-231-7423 [email protected] 14 Co-Lead Counsel for Plaintiffs and the Class 15 [Additional counsel on signature page.] 16 17 SUPERIOR COURT OF THE STATE OF CALIFORNIA 18 COUNTY OF SAN FRANCISCO 19 Lead Case No. CGC-19-575293 20 IN RE LYFT, INC., SECURITIES LITIGATION CLASS ACTION 21 CORRECTED CONSOLIDATED 22 CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE SECURITIES 23 ACT OF 1933 This Document Relates To: 24 ALL ACTIONS JURY TRIAL DEMANDED 25 26 27 28 CORRECTED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF THE SECURITIES ACT OF 1933 1 Plaintiffs Brian Hinson, Frederic Lande, Wesley Clapper, Narendra Gupta, Liang Xue, Nathaniel 2 Pyron, Mary McCloskey, Palm Bay Police & Firefighters’ Pension Fund and Greater Pennsylvania 3 Carpenters’ Pension Fund (collectively, “Plaintiffs”), individually and on behalf of all others similarly 4 situated, by Plaintiffs’ undersigned attorneys, allege the following based upon personal knowledge, as to 5 Plaintiffs and Plaintiffs’ own acts, and upon information and belief, as to all other matters, based on the 6 investigation conducted by and through Plaintiffs’ attorneys, which included, among other things, a 7 review of U.S. -

Exploration of the Current State and Directions in the Emerging Field of Dynamic Ridesharing Platforms

Middle States Geographer, 2014, 47: 68-78 EXPLORATION OF THE CURRENT STATE AND DIRECTIONS IN THE EMERGING FIELD OF DYNAMIC RIDESHARING PLATFORMS Joseph J. Di Gianni Department of Earth and Environmental Studies Montclair State University Montclair, NJ 07043 ABSTRACT: Automobility has advanced since the postwar decline of public transportation and its near universal replacement by single-occupant vehicles (SOVs) throughout much of the developed economies. Even so- called “transit friendly” economies of the Global South have seen shifts in their modes of transportation to systems that are predominantly SOV-based (Cervero, 2013). Intensive infrastructure expansion within emerging economies indicates that the SOV is being adopted at a rate similar to the developed economies of one hundred years ago. In Henry Ford's quote “With mobility comes freedom and progress” mobility becomes universally interpreted as “automobility”. Grave concern is linked to the continuation of the SOV model and its consequences for an environment taxed by an ever-expanding transportation sector. A paradigm shift, however, in the SOV-driven model, has been detected coming not from transportation but the different domains of information and communication technologies (ICT). This review examined the current state and direction of dynamic ridesharing (DRS), an emerging technology driven by recent innovations in ICT over the last two decades (Siddiqi & Buliung, 2013). DRS matches drivers and riders in real-time using Internet and mobile technology, and are single- occurrence events organized on short notice (Amey, Attanucci, & Mishalani, 2011). We conclude with a case study of DRS from its roots in San Francisco, CA. The city provides a present-day template for emerging themes when DRS is introduced into the present-day urban transportation system. -

Oke Hauptmann Defense Loses 3 Skirmishes at Today's

T MONDAT, FEBSUAKT 4,1988. IIWILTB V, manrlfratnr Etmtbts ifrrald THE WEATHER W E R A O B DAILY CIRCULATIOM Forecast of 1). S. Weather Burnaa. The Ulspah group -of the Wes The Sewing Circle o f Mona Tpres Princess and was given th* nams, In the Carnival Queen contast, con for the 'month of Jonnary, 1686 Hartford OLVER RHYTHM ORCH. leyan Guild will meet tomorrow eve auxiliary, will omit Its meeting plan "Rad Wing," and Jackie May was gratulated the Qiieen, Miss Alice ned for this week. POUCE COURT 2 6 5 COUPLES DANCE crowned with s Warrior headdress Brasauskis, during the Indian pag ning at 7:30 with Mrs. T. B. Kehler Snow this afternoon and early to '■il Tlinndar. Ffbniary 7th of 67 Cambridge street. Work will and given the name, “Red Eagle.” eant. 5 , 4 5 9 night; Wedneeday fair and slightly The Ancient Order Of United Just one arrest was made in Man Jrand March Skaters and guests were present TLeJWHALECo School St. Ree be on salting peanuts. chester over the week-eno. That AT CARNIVAL BALL Chairman Lawrence Converse from Meriden, Hartford, Spring- Member of ifie Audit colder. j Workmen will hold a brief business was Frederick J. Wilhelm of Elling Door Priw. meeting tonight at 8 o'clock In the and his daughter, Mias JuUa Ck>n- field, Holyoke, Cnilcopee and New Boreon et Clrculatlmia Mrs. J. M. Williams of Hudson ton, for driving an automobile while verse led the grand march of 12S York. • • • a e o M M to r ibmi and wwnM. -

02/13/19 Farm Direction Van Trump

Tim Francisco <[email protected]> GOOD MORNING: 02/13/19 Farm Direction Van Trump Report 1 message The Van Trump Report <reply@vantrumpreportemail.com> Wed, Feb 13, 2019 at 7:08 AM ReplyTo: Jordan <replyfed4167277640478314_HTML362509461000034501@vantrumpreportemail.com> To: [email protected] "We generate fears while we sit. We over come them by action. Fear is nature's way of warning us to get busy." Dr. Henry Link 1822, Ashley Advertises for WEDNESDAY, FEBRUARY 13, 2019 Western Fur Trappers Printable Copy or Audio Version Missouri Lieutenant Governor William Ashley places an Morning Summary: Stocks are slightly higher this morning as bulls remain optimistic advertisement in the Missouri about two nearby hurdles perhaps being cleared. Leaders in Washington seem to have Gazette and Public Advisor seeking 100 reached a budget compromise that will help avoid another government shutdown. There “enterprising young men” to engage in fur has also been more optimistic headlines circulating regarding Chinese trade. Headlines trading on the Upper Missouri. A Virginia were circulating yesterday that President Trump was “open” to letting the March 1 native, Ashley had moved to Missouri just Chinese trade deadline slide if the two countries are close to a deal by then. Technically, after President Thomas Jefferson the bulls are also extremely excited to see the S&P 500 move back above its 200day concluded the Louisiana Purchase from moving average and post a new twomonth high. Keep in mind, the last time the S&P France, which made the region American 500 closed back above the 200DMA was on December 3rd. -

Lyft's Rapid Surge in the Rideshare Sector

VC20033 Lyft’s Rapid Surge in the Rideshare Sector Joseph Conde University of the Incarnate Word Ryan Lunsford, Ph.D. University of the Incarnate Word VC20033 Abstract Lyft is a rideshare company that has successfully provided convenient and cost-effective transportation services for 22.9 million people across the United States (Iqbal, 2020). The company was established in the Summer of 2012 and by 2019, Lyft increased both the total number of customers and the crucial rides per customer metric leading to a valuation of nearly $24 billion (Madrigal, 2019). The rise began in 2017 when Lyft began increasing its earnings rapidly after pitfalls from its primary competitor, Uber, which had several ethical and legal scandals that received intense media coverage (Carson, 2017). In the subsequent months, Lyft realized a 130% rise in the number of rides from the previous year and launched service in 160 new cities, increasing Lyft’s percentage of market share to 48% (Kerr, 2018). Lyft’s competitive advantage relative to its rivals includes maintaining a transparent, trustworthy reputation, resolving customer and employee concerns quickly and equitably, and providing a safe ride experience that enables riders to conveniently and affordably enjoy their transportation service (Srivastava, 2016). Lyft prioritizes both the relationships that it has with its employees and the industry-leading rates that it charges per ride (Oswald & Revilla, 2020). The company has emphasized improvements to Lyft services by concentrating on customer data analytics, implementing rideshare capabilities to minimize fees, and providing customers a monthly membership subscription that is expected to generate eight times as much revenue in the next 12 years (Forbes, 2018). -

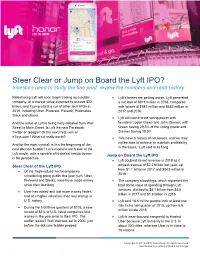

Steer Clear Or Jump on Board the Lyft IPO? Investors Need to Study the Fine Print, Review the Numbers and Read History

Steer Clear or Jump on Board the Lyft IPO? Investors need to study the fine print, review the numbers and read history Ridesharing Lyft will soon begin trading as a public • Lyft’s losses are getting worse: Lyft generated company, at a market value expected to exceed $22 a net loss of $911 million in 2018, compared billion, and it jump-starts a run of other tech IPOs in with losses of $687 million and $683 million in 2019, including Uber, Pinterest, Palantir, Postmates, 2017 and 2016 Slack and others. • Lyft will concentrate voting power with And the value of Lyft is being hotly debated from Wall founders Logan Green and John Zimmer, with Street to Main Street. Is Lyft the next Facebook, Green having 29.3% of the voting power and Twitter or Google? Or the next Pets.com or Zimmer having 19.5% eToys.com? What’s it really worth? • “We have a history of net losses, and we may not be able to achieve or maintain profitability And for the most cynical: is this the beginning of the in the future,” Lyft said in its filing next dot.com bubble? Let’s examine each side of the Lyft model, with a sprinkle of historical trends thrown Jump on Board the Lyft IPO in for perspective: • Lyft doubled its net revenue in 2018 as it Steer Clear of the Lyft IPO posted revenue of $2.2 billion last year, up from $1.1 billion in 2017 and $343 million in • Of the “high-valued” tech-companies 2016 considering going public this year (Lyft, Uber, Pinterest and Slack), none have made money • The company’s bookings, which represent the since their founding total dollar value of spending through Lyft services, climbed to $8.1 billion from $4.6 • Uber has raised and lost more money faster, billion in 2017 and $1.9 billion in 2016 and at a higher valuation, than any startup in U.S.