Final Merger Notice

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Radio Multiplex Licence Variation Request Form This Form Should Be

Radio Multiplex Licence Variation Request Form This form should be used for any request to vary a local or national radio multiplex licence, e.g: replacing one programme or data service with another adding a programme or data service removing a programme or data service changing the Format description of a programme service changing a programme service from stereo to mono changing a programme service's bit-rate Please complete all relevant parts of this form. You should submit one form per multiplex licence, but you should complete as many versions of Part 3 of this form as required (one per change). Before completing this form, applicants are strongly advised to read our published guidance on radio multiplex licence variations, which can be found at: http://licensing.ofcom.org.uk/radio-broadcast-licensing/digital-radio/radio-mux-changes Part 1 – Details of multiplex licence Radio multiplex licence: North Yorkshire Licensee: Muxco North Yorkshire Limited Contact name: Gregory Watson Date of request: 13th October 2016 Part 2 – Summary of multiplex line-up before and after proposed change(s) Existing line-up of programme services Proposed line-up of programme services Service name, short- Bit-rate Service Service name, short- Bit- Service form description and (kbps/ mode form description and rate mode hours of broadcast data hours of broadcast (kbps/ rate) data rate) Minster FM 128/F JS Minster FM 128/F JS Stray FM 128/F JS Stray FM 128/F JS BBC Radio Yorkshire 128/F JS BBC Radio Yorkshire 128/F JS Yorkshire Coast Radio 128/F JS Yorkshire -

Anti-Stress Garden Coming to RHS Chelsea Flower Show

Spring 2019 News from the University of Surrey for Guildford residents SURREY.AC.UK UNIVERSITYOFSURREY @ UNIOFSURREYCPE Page 4 - Surrey graduate Page 7 - Could your car Page 10 - Iain Sinclair, Page 11 - Shrek workshop meets Michelle Obama park itself? Writer-in-Residence supports local group Guildford Residents’ Survey 2019 The University is calling on residents of Guildford to take part in our fifth annual residents’ survey. Since its launch in 2015, the Guildford Residents’ Survey has provided the Right: an artist’s impression of the garden design University with Main image: the garden will feature irises, flowers celebrated valuable insight, for their wellbeing properties. Credit: Getty Images feedback and ideas to build greater links with our home town. Last year, more than Anti-stress garden coming to 1,300 local residents took part, with many entering the annual RHS Chelsea Flower Show prize draw to win The University has partnered with Silent Pool Gin to present an anti-stress garden at the one of five £100 RHS Chelsea Flower Show, transporting visitors to the Surrey Hills using scents and sounds. cash prizes. We want to hear The exciting collaboration with Albury-based He will be using sensors to detect and from you – to gin brand Silent Pool, acclaimed Surrey-based capture changing electrical signals directly complete the survey garden designer David Neale and Dutch from the plants, enabling the garden to visit: surrey.ac.uk/ horticultural pioneers Plant-e will explore govern and interact with the soundscape. guildfordsurvey plant technologies that encourage wellbeing. Professor Murphy said: “This truly exciting The survey closes Through their combined expertise, the team collaboration brings to life the hidden power on 1 July 2019. -

QUARTERLY SUMMARY of RADIO LISTENING Survey Period Ending 20Th December 2015

QUARTERLY SUMMARY OF RADIO LISTENING Survey Period Ending 20th December 2015 PART 1 - UNITED KINGDOM (INCLUDING CHANNEL ISLANDS AND ISLE OF MAN) Adults aged 15 and over: population 53,575,000 Survey Weekly Reach Average Hours Total Hours Share in Period '000 % per head per listener '000 TSA % All Radio Q 48237 90 18.9 21.0 1013438 100.0 All BBC Radio Q 34947 65 10.1 15.5 541794 53.5 All BBC Radio 15-44 Q 14656 58 5.9 10.1 148396 38.7 All BBC Radio 45+ Q 20291 72 13.9 19.4 393398 62.4 All BBC Network Radio1 Q 32125 60 8.7 14.6 467524 46.1 BBC Local Radio Q 8558 16 1.4 8.7 74270 7.3 All Commercial Radio Q 35111 66 8.3 12.7 446584 44.1 All Commercial Radio 15-44 Q 18313 72 8.8 12.2 222861 58.1 All Commercial Radio 45+ Q 16798 59 7.9 13.3 223723 35.5 All National Commercial1 Q 18298 34 2.8 8.1 147660 14.6 All Local Commercial (National TSA) Q 27126 51 5.6 11.0 298924 29.5 Other Radio Q 3966 7 0.5 6.3 25059 2.5 Source: RAJAR/Ipsos MORI/RSMB 1 See note on back cover. For survey periods and other definitions please see back cover. Embargoed until 00.01 am Enquiries to: RAJAR, 6th floor, 55 New Oxford St, London WC1A 1BS 4th February 2016 Telephone: 020 7395 0630 Facsimile: 020 7395 0631 e mail: [email protected] Internet: www.rajar.co.uk ©Rajar 2016. -

We've Come a Long Way!

Spotlight The halow project’s magazine Issue 1 in June 2008 with the appointment of Project Director, We’ve come a Yvonne Hignell - by November of that year, Yvonne had produced a business plan, halow had moved into an office in Quarry Street, Guildford and held an official launch party. long way! In January of 2009, a dedicated social activities group was established for halow young people. By March of the same Over seven years since halow was formed, we bring year halow had secured its first tranche of much needed supporters new and old a sense of just where halow has come funding from Surrey Short Breaks and by June, funding was from, where it is now, and where the Guildford-based charity obtained from the LDD Fund (Learning Disability Development) is heading... to set up the Building Futures Programme and the charity’s first The inspiration for halow came from Harriet, Amber, Laura, website was launched. That summer also saw the first major Oliver and William. Their parents, all friends, came together at activity, with 36 young people and volunteers attending the the beginning of 2006 concerned with the prospect for their WOMAD festival in Malmesbury, Wiltshire. children’s future and others like them. Passionate that these In September 2009, the Building Futures Programme young people should lead positive and happy lives, near their commenced, shortly followed in October with the registration own friends and families in Surrey, the parents established the of halow care, a social enterprise, which runs alongside the halow project. halow project. Through this, our Buddy service was launched The first major turning point in the charity’s growth story was for our young people. -

Pioneering Tool to Manage Media Industry's Digital Carbon Footprint 13 January 2020

Pioneering tool to manage media industry's digital carbon footprint 13 January 2020 industry understand and manage the carbon impact of digital media. Mapping the carbon footprint of digital services like advertising, publishing and broadcasting is difficult because the underlying technological systems are hugely complex and constantly shifting. Media content passes through content delivery networks, data centres, web infrastructure and user devices, to name just a few, with each element of the delivery chain having different owners. With climate change high on the agenda, DIMPACT The online tool with help media industry manage its will allow participating companies to understand digital carbon footprint. Credit: Pixabay/ University of their 'downstream' carbon impacts, right through to Bristol the end-user. This, in turn, will enable more informed decision-making to reduce the overall carbon footprint of digital services. A collaboration between computer scientists at the University of Bristol and nine major media "We know that more and more of our interactions companies, including ITV and BBC, will help the happen online, and screens play an ever more media industry understand and manage the important role in our lives. We can say with significant carbon impacts of digital content. absolute certainty that the digital economy will continue to grow. What we don't know is how those The 12-month collaboration, facilitated by modes of digital consumption translate into carbon sustainability experts, Carnstone, will see impacts and where the 'hotspots' reside. DIMPACT University of Bristol researchers working with will change that," said Christian Toennesen, Senior sustainability and technology teams at the BBC, Partner at Carnstone and DIMPACT's initiator and Dentsu Aegis Network, Informa, ITV, Pearson, product manager. -

Download Valuing Radio

Valuing Radio How commercial radio contributes to the UK A report by the All-Party Parliamentary Group on Commercial Radio The data within Valuing Radio is largely drawn from a 2018 survey of Radiocentre members. It is supplemented by additional research which is sourced individually. Contents 01 Introduction 03 Overview and recommendations 05 The public value of commercial radio • News and information • Economic value • Charity and community 21 Commercial radio people 27 Future of radio Introduction The APPG on Commercial Radio helps provide this important industry with a voice in parliament. With record audiences and more ways to listen than ever before, the impact of the industry should not be underestimated. While the challenges facing the sector have changed over the years, the steadfast commitment of stations to provide public value content every day remains. This new report, the first of its kind produced by the APPG, showcases the rich public value content that commercial radio provides to listeners for free. Valuing Radio explores the impact made by stations up and down the country, over and above the music and entertainment output that audiences expect. It looks particularly at radio’s role in providing news and information, the sector’s significant support for both charitable fundraising and education, in addition to work to improve diversity within the industry. Alongside this important public value content is a significant economic contribution to local economies across the UK. For the first time we have analysis on the impact of local advertising and the return on investment (ROI) that this generates for particular nations and regions of the UK. -

Pocketbook for You, in Any Print Style: Including Updated and Filtered Data, However You Want It

Hello Since 1994, Media UK - www.mediauk.com - has contained a full media directory. We now contain media news from over 50 sources, RAJAR and playlist information, the industry's widest selection of radio jobs, and much more - and it's all free. From our directory, we're proud to be able to produce a new edition of the Radio Pocket Book. We've based this on the Radio Authority version that was available when we launched 17 years ago. We hope you find it useful. Enjoy this return of an old favourite: and set mediauk.com on your browser favourites list. James Cridland Managing Director Media UK First published in Great Britain in September 2011 Copyright © 1994-2011 Not At All Bad Ltd. All Rights Reserved. mediauk.com/terms This edition produced October 18, 2011 Set in Book Antiqua Printed on dead trees Published by Not At All Bad Ltd (t/a Media UK) Registered in England, No 6312072 Registered Office (not for correspondence): 96a Curtain Road, London EC2A 3AA 020 7100 1811 [email protected] @mediauk www.mediauk.com Foreword In 1975, when I was 13, I wrote to the IBA to ask for a copy of their latest publication grandly titled Transmitting stations: a Pocket Guide. The year before I had listened with excitement to the launch of our local commercial station, Liverpool's Radio City, and wanted to find out what other stations I might be able to pick up. In those days the Guide covered TV as well as radio, which could only manage to fill two pages – but then there were only 19 “ILR” stations. -

Monthly Business & Tech-Enabled Services Sector Summary Report

BUSINESS AND TECH-ENABLED SERVICES SECTOR REPORT March 2018 1 BUSINESS & TECH-ENABLED SERVICES DEAL DASHBOARD $94.4 Billion 788 M&A Volume YTD M&A Transactions YTD Quarterly M&A Volume ($Bn) and Deal Count Select M&A Transactions 100 $94.4 Announced Date Acquirer Target EV ($MM) 80 3/29/2018 NA 60 $48.5 $45.1 $45.5 $37.1 3/29/2018 NA 40 $31.1 $24.6 $27.4 $26.9 $19.1 $19.2 $21.7 Volume ($Bn) Volume $14.9 20 3/28/2018 $4,000 (Sig. M inority Stake) 0 3/26/2018 NA Q1 '15Q2 '15Q3 '15Q4 '15Q1 '16Q2 '16Q3 '16Q4 '16Q1 '17Q2 '17Q3 '17Q4 '17Q1 '18 (Investment) 1200 3/21/2018 NA 966 944 964 995 986 1000 901 929 917 875 894 797 788 788 800 3/21/2018 NA 600 3/19/2018 $1,180 Deal Count Deal 400 200 3/15/2018 $383 0 Q1 '15Q2 '15Q3 '15Q4 '15Q1 '16Q2 '16Q3 '16Q4 '16Q1 '17Q2 '17Q3 '17Q4 '17Q1 '18 3/15/2018 NA (1) Last 12 Months Business & Tech-Enabled Services Performance vs. S&P 500 3/14/2018 NA (Investment) 125.0% 3/13/2018 $205 120.0% 115.0% 3/13/2018 NA 110.0% 105.0% 3/12/2018 $108 100.0% 3/6/2018 $564 95.0% 90.0% 3/5/2018 NA Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 Business & Tech-Enabled Services S&P 500 3/1/2018 NA (Investment) Notes: 2 Source: Capital IQ and PitchBook. -

Steel Matters Issue 8

ISSUE 8 SteelMatters February 2021 Your community magazine WHAT’S INSIDE SAFE WORKING Mass Covid-19 testing at 3 Port Talbot site CLEAN-up at MORFA Beach 5 Steel Heroes to beach heroes Ca ‘I lOVE IT WHEN A PLAN COMES TOGETHER’ FAMILY POVERTY The focus on ‘first events’, such as despatches out of each UK site, passed the test The Cold Truth appeal is back with a 2021 twist 7 Director Strategic Business the UK and mainland Europe would be What’s more, we kept all our promises to separation is just as relevant to the Development Deirdre Fox may not significantly less. our customers.” inwards supply of materials and services see herself as John “Hannibal” Smith, “However, until the deal was done Deirdre added: “The teams have also that allow us to operate.” but she may well see all those people at the end of December, the issue of been dealing with external factors such as Of course, the Brexit separation is who worked so hard to prepare for and trading measures was still one that availability of transport and the efficiency far from over, as Deirdre explained: execute Tata Steel’s Brexit plans, to be could make a massive difference to our of third party systems and so on. “There will continue to be issues to akin to the A-Team. customers and their supply chains. “There remain challenges on these resolve across the water in the next 12 While it may not be accurate to “Our own focus in the first week of fronts, especially following the pre- to 24 months as industries align their describe the transition between 2020 January was on testing ‘first events’, Christmas Covid-19-related blockages product qualifications and so on, but and 2021 as totally seamless, for Tata such as the first despatch out of each of and now availability of transport as I’m delighted that the team’s hard work, Steel and its customers it went as well as our UK sites and the first transfers from volumes start to ramp up in all sectors of professionalism and attention-to-detail is anyone might have expected. -

Consultation: Bauer Radio Stations in the North of England

Bauer Radio stations in the north of England Request to create a new approved area CONSULTATION: Publication date: 25 September 2020 Closing date for responses: 23 October 2020 Contents Section 1. Overview 1 2. Details and background information 2 3. Consideration of the request 5 Annex A1. Responding to this consultation 6 A2. Ofcom’s consultation principles 8 A3. Consultation coversheet 9 A4. Consultation questions 10 A5. Bauer’s approved area request 11 Bauer Radio stations in the north of England – request to create a new approved area 1. Overview Most local analogue commercial radio stations are required to produce a certain number of hours of locally-made programming. Under legislation passed in 2010, these stations are not only able to broadcast their locally-made hours from within their licence area, but may instead broadcast from studios that are based within a larger area approved by Ofcom. These wider areas are known as ‘approved areas’. Stations can also share their local hours of programming with other stations located in the same approved area. Ofcom has approved an area for every local radio licence in the UK, to give stations more flexibility in their broadcasting arrangements. However, a licensee can ask Ofcom to approve a bespoke area, since the statutory framework allows for an approved area in relation to each local analogue service. What we are consulting on – in brief Bauer Radio has asked Ofcom to approve the creation of a new bespoke approved area in the north of England which would include the Northallerton licence, currently part of the North East of England Ofcom approved area, in a new approved area alongside 16 FM licences held by Bauer which are currently in the Yorkshire & Lincolnshire Ofcom approved area. -

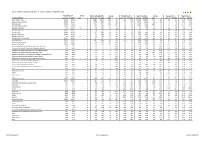

Hallett Arendt Rajar Topline Results - Wave 3 2019/Last Published Data

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 3 2019/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share STATION/GROUP Last Pub W3 2019 000's % Last Pub W3 2019 000's % Last Pub W3 2019 Last Pub W3 2019 000's % Last Pub W3 2019 Last Pub W3 2019 Bauer Radio - Total 55032 55032 0 0% 18083 18371 288 2% 33% 33% 156216 158995 2779 2% 8.6 8.7 15.3% 15.9% Absolute Radio Network 55032 55032 0 0% 4743 4921 178 4% 9% 9% 35474 35522 48 0% 7.5 7.2 3.5% 3.6% Absolute Radio 55032 55032 0 0% 2151 2447 296 14% 4% 4% 16402 17626 1224 7% 7.6 7.2 1.6% 1.8% Absolute Radio (London) 12260 12260 0 0% 729 821 92 13% 6% 7% 4279 4370 91 2% 5.9 5.3 2.1% 2.2% Absolute Radio 60s n/p 55032 n/a n/a n/p 125 n/a n/a n/p *% n/p 298 n/a n/a n/p 2.4 n/p *% Absolute Radio 70s 55032 55032 0 0% 206 208 2 1% *% *% 699 712 13 2% 3.4 3.4 0.1% 0.1% Absolute 80s 55032 55032 0 0% 1779 1824 45 3% 3% 3% 9294 9435 141 2% 5.2 5.2 0.9% 1.0% Absolute Radio 90s 55032 55032 0 0% 907 856 -51 -6% 2% 2% 4008 3661 -347 -9% 4.4 4.3 0.4% 0.4% Absolute Radio 00s n/p 55032 n/a n/a n/p 209 n/a n/a n/p *% n/p 540 n/a n/a n/p 2.6 n/p 0.1% Absolute Radio Classic Rock 55032 55032 0 0% 741 721 -20 -3% 1% 1% 3438 3703 265 8% 4.6 5.1 0.3% 0.4% Hits Radio Brand 55032 55032 0 0% 6491 6684 193 3% 12% 12% 53184 54489 1305 2% 8.2 8.2 5.2% 5.5% Greatest Hits Network 55032 55032 0 0% 1103 1209 106 10% 2% 2% 8070 8435 365 5% 7.3 7.0 0.8% 0.8% Greatest Hits Radio 55032 55032 0 0% 715 818 103 14% 1% 1% 5281 5870 589 11% 7.4 7.2 0.5% -

TRAVEL PRESENTER Reading Live Travel Bulletins Every Fifteen Minutes

I am the industrious worker that does not resort to the bare minimum. With a strong voice and equally strong work ethic I am a great addition to any broadcasting team. I am imaginative and creative, I work with my listener in mind and with a “can do” mentality I am determined to go the extra mile to help out. I have the knowledge and passion - all I need is the opportunity to impress! TRAVEL PRESENTER BBC RADIO NORFOLK | JAN 2014 - PRESENT | NORWICH Reading live travel bulletins every fifteen minutes throughout the morning, quickly adapting to new information and reporting issues live as they happen. ● Utilising a range of sources - cameras, callers, travel companies and Twitter to create accurate and engaging reports. ● Manning the local Twitter travel service (@BBCNrfkTravel) while updating it coherently and responding to queries. PHOTOGRAPHER & HEART ANGEL HEART EAST ANGLIA | JUN 2011 - PRESENT | NORWICH A senior member of a busy promotions team assistant managing events, mentoring and training new staff and looking after the station’s collateral. ● Driving brand awareness, approaching members of the public and helping to prepare sold promotions. BROADCASTING ● Event photographer taking brand-friendly, managing online PRESENTING galleries and working on a very quick turnaround. PRODUCING RADIO STATION MANAGER AUDIO PRODUCTION ESSEX INTERNATIONAL JAMBOREE | JAN 2015 - PRESENT | MUSIC PLAYLISTING MARKETING & BRANDING Managing a week’s RSL at the biggest Scout & Guide Jamboree in the United Kingdom in August 2016. PROMTIONS ● Recruiting and leading a team of radio staff to help plan and VOICEOVER prepare for broadcast to 12’000 participants. DJING ● Responsible for the scheduling of the station, liaising with other PHOTOGRAPHY event departments and managing pre-recorded content.