Annual Turkish M&A Review 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Günlük Bülten S&P 500 Brent Petrol USD Endeks %0.36 -%0.75 %0.17

Türkiye | Piyasalar 26 Ocak 2021 Salı Günlük Bülten S&P 500 Brent Petrol USD Endeks %0.36 -%0.75 %0.17 Ekonomik Veriler Açıklanacak Veriler Saat Piyasa Yorumu: İngiltere İşsizlik Oranı 10:00 Amerika Tüketici Güveni 18:00 TSİ Bu sabah BIST100’de aşağı yönlü bir açılış bekliyoruz. Küresel piyasalardaki negatif seyir devam ederken, hisse senetlerinde satışların Hisse Senedi Piyasası devam ettiğini görüyoruz. Zayıf bankacılık ve havacılık hisse senetlerinin performansı endekse karşı genel duyarlılığı etkiliyor. 50,000 1,580 48,000 1,570 Bu sabah negatif açılış ve sonrasında 1510 – 1550 arasında işlem 46,000 1,560 aktivitesi bekliyoruz. 44,000 1,550 42,000 1,540 40,000 1,530 38,000 1,520 Bugünün Haberleri: 36,000 1,510 34,000 1,500 15-Oca 18-Oca 19-Oca 20-Oca 21-Oca 22-Oca 25-Oca Piyasa Gelişmesi İşlem Hacmi, TRY mln BIST 100 . Reel kesim güveninde düşüş Bono Piyasası . Ocak ayı - Kapasite Kullanım Oranı 60.0 13.6 13.5 50.0 Hisse Senetleri 13.5 40.0 13.4 13.4 . ARCLK; 4Ç20 sonuçları beklentilerin oldukça üzerinde geldi / 30.0 13.3 20.0 13.3 olumlu 13.2 10.0 13.2 0.0 13.1 . PETKM; Etilen-nafta spread’i yeniden 650 USD'ye yöneldi / olumlu 15-Oca 18-Oca 19-Oca 20-Oca 21-Oca 22-Oca 25-Oca . GUBRF; 2020 yılı faaliyetleri hakkında bilgilendirme / pozitif İşlem Hacmi, TRY mln Türkiye 2030 Endeksler, para piyasaları ve emtia . BAGFS; %200 bedelli sermaye artırımı / nötr Kapanış Önceki 1 Gün 1 Ay Yıl Baş. BIST100 1,540 1,542 -0.1% 8.0% 4.3% . -

1 Ocak 2021 Itibariyle Şirketlerin Katilim Endeksi

1 OCAK 2021 İTİBARİYLE ŞİRKETLERİN KATILIM ENDEKSİ KRİTERLERİNE UYGUNLUK DURUMU & ARINDIRMA ORANLARI Faaliyet alanı, grubu ve pazarı uygun olmayan şirketlerin finansal kriterleri hesaplanmamaktadır. Faizli krediler / (piyasa değeri ya da aktif toplamdan büyük olanı) < %33 kriterini geçemeyen şirketlerin diğer finansal kriterleri hesaplanmamaktadır. Faiz Getirili Nakit/(piyasa değeri ya da aktif toplamdan büyük olanı)<%33 kriterini geçemeyen şirketlerin diğer finansal kriterleri hesaplanmamaktadır. Toplam Faizli Uygunsuz Krediler / Piyasa (Nakit+Menkul Uygun Olmayan Sıra Hisse Kodu Hisse Adı Gerekçe Değeri veya Aktif (< Kıymet)/Piyasa Değeri Faaliyetlerden Gelir / %33) veya Aktif (<%33) Toplam Gelir (< %5) 1 BIMAS Bim Mağazalar Uygun 0,0% 0,0% 0,2% 2 EREGL Ereğli Demir Çelik Uygun 14,4% 25,3% 2,7% 3 ASELS Aselsan Uygun 9,6% 5,5% 1,5% 4 THYAO Türk Hava Yolları Uygun 18,3% 4,6% 4,3% 5 CCOLA Coca Cola İçecek Uygun 29,5% 18,4% 1,8% 6 GUBRF Gübre Fabrik. Uygun 22,7% 11,5% 0,3% 7 BERA Bera Holding Uygun 26,3% 0,0% 0,5% 8 TKFEN Tekfen Holding Uygun 14,0% 15,6% 1,2% 9 OYAKC Oyak Çimento Uygun 9,7% 6,2% -22,6% 10 PGSUS Pegasus Uygun 7,5% 12,4% 2,6% 11 EGEEN Ege Endüstri Uygun 4,3% 22,0% 2,1% 12 TTRAK Türk Traktör Uygun 30,7% 32,9% 2,3% 13 MAVI Mavi Giyim Uygun 30,2% 22,6% 1,5% 14 LOGO Logo Yazılım Uygun 7,6% 7,9% 2,8% 15 KARTN Kartonsan Uygun 0,0% 7,4% 1,8% 16 SELEC Selçuk Ecza Deposu Uygun 0,6% 10,6% 0,7% 17 ISDMR İskenderun Demir Çelik Uygun 4,9% 0,2% 1,3% 18 RTALB RTA Laboratuvarları Uygun 1,5% 0,1% 2,8% 19 CEMAS Çemaş Döküm Uygun 0,3% 17,9% -

Gazl Çecek Sektörü Ve Gazoz Pazar Ndaki KOB Ler Çin Ni Pazarlamas Na Bir Örnek Doç

YÖNET M VE EKONOM Y l:2005 Cilt:12 Say :2 Celal Bayar Üniversitesi . .B.F. MAN SA Gazl çecek Sektörü ve Gazoz Pazar ndaki KOB ler çin Ni Pazarlamas na Bir Örnek Doç. Dr. Canan AY Celal Bayar Üniversitesi, BF, letme Bölümü, MAN SA Ara . Gör. Sinan NARDALI Celal Bayar Üniversitesi, Uygulamal Bilimler Yüksek Okulu, MAN SA Ara . Gör. Burak KARTAL Celal Bayar Üniversitesi, BF, letme Bölümü, MAN SA ÖZET Küçük ve Orta Ölçekli letmeler (KOB ) belki de çok az say da sektörde, me rubat sektöründeki kadar zor durumdad r. Bunun temel nedeni sektörlerindeki dev say labilecek birkaç firman n pazar n büyük ço unlu unu ve kontrolü elinde tutmas ve sektörün rekabetçi yap s n n, bilinen genel sorunlar nedeniyle KOB lerin hareket yetene ini k s tlamas d r. Bu çal ma ile gazoz pazar nda bölgesel olarak mücadele veren bir KOB nin ni pazarlamas n nas l uygulayabilece i gösterilmeye çal lm t r. Anahtar Kelimeler: Gazl içecekler, Ni pazarlamas , KOB . A Sample of The Appl cat on of Niche Marketing by SMEs In The Soda and Carbonated Beverages Market ABSTRACT Small and Medium-Sized Enterprises (SME) rarely find themselves in distress like the ones do in carbonated beverages market. The reasons for that may be the market dominance of a few gigantic firms in terms of control and market share, and the disability of resource-limited SMEs in responding to market needs due to the competitive structure of the industry. In this paper we try to show how a local soda pop company can better deal with the challenges in its market through niche marketing. -

The Advertiser's Perspective on Advertising Agency

THE ADVERTISER’S PERSPECTIVE ON ADVERTISING AGENCY-CLIENT RELATIONSHIPS: A SURVEY OF LEADING ADVERTISERS IN TURKEY TANSES YASEMİN GÜLSOY Submitted to the Graduate School of Social Sciences in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Contemporary Management IŞIK UNIVERSITY 2006 ii THE ADVERTISER’S PERSPECTIVE ON ADVERTISING AGENCY- CLIENT RELATIONSHIPS: A SURVEY OF LEADING ADVERTISERS IN TURKEY Abstract This dissertation focuses on the relationship between advertisers and their advertising agencies, in an effort to understand what drives advertiser’s satisfaction in this relationship which can have considerable impact on the business success of both parties. The research develops a model of relationship satisfaction positioned within the conceptual framework of Wackman, Salmon & Salmon (1986/87). This conceptual framework has been extended with additional variables to account for the complexities of the agency-client relationship in the Turkish advertising industry today. A survey of Turkey’s largest advertisers was conducted, using the face-to-face interview method. Factor analysis and regression analysis (of factor-scores) were then used to test the proposed framework. All of the dimensions of the model were found to significantly influence the advertiser’s satisfaction with the agency. The results suggest that advertisers principally value the agency’s creativity and the relationship with the agency. Compatibility, agency’s cost-consciousness, service breadth, leadership capability, and perceived contribution to advertiser’s sales, market share, and brand targets were also found to be important for satisfaction. Other significant predictors are people- related attributes, strategic input, trust, cooperativeness, and prestige and full-service capability. The empirical findings are consistent with the theory and confirm the importance of relationship attributes in advertiser’s satisfaction. -

2016 Annual Report & Sustainability Report

2016 ANNUAL REPORT & SUSTAINABILITY REPORT BOYNER RETAIL AND TEXTILE INVESTMENTS BOYNER RETAIL AND TEXTILE INVESTMENTS www.boynerperakende.com www.boynergrup.com 2 2016 ANNUAL REPORT & SUSTAINABILITY REPORT 3 CONTENTS 05 10 29 69 106 121 137 FROM THE MANAGEMENT BOYNER GROUP BOYNER RETAIL AND SUSTAINABILITY CORPORATE AGENDA FOR THE INDEPENDENT TEXTILE INVESTMENTS REPORT GOVERNANCE ORDINARY GENERAL AUDITOR’S REPORT ON 06 12 CO. INC. and PRINCIPLES ASSEMBLY MEETING ANNUAL REPORT Message from the CEO and Our History 71 ITS COMPANIES COMPLIANCE REPORT FOR 2016 Chairman of the Board Sustainability 141 14 30 Management and our 117 122 INDEPENDENT 09 Our 2016 Awards Partnership Structure Stakeholders RISK MANAGEMENT AND Resumes and AUDITOR’S REPORT Members of the Board of 15 INTERNAL AUDIT Statements of & FINANCIAL Directors 33 73 Our Values Independent Members STATEMENTS Boyner Büyük Our Working Ecosystem 118 for Ordinary General 16 Mağazacılık A.Ş. DONATIONS AND GRANTS 83 Assembly Meeting for Our Working 43 Anti-Corruption 118 2016 Environment Beymen Mağazacılık CAPITAL MARKET 84 130 18 A.Ş. INSTRUMENTS ISSUED Our Environmental Dividend Distribution Our Strategies and IN 2016 51 Awareness Proposal and Statement Projects in 2016 AY Marka Mağazacılık 119 for 2016 - WEPUBLIC 90 A.Ş. LEGAL DISCLOSURES - Hopi Our Value Chain 132 - All Line Retail 61 Remuneration Policy 95 Altınyıldız Tekstil ve for Board Members and Our Contribution to Konfeksiyon A.Ş. Senior Executives Society 136 Dividend Distribution Policy FROM THE MANAGEMENT 05 6 2016 ANNUAL REPORT & SUSTAINABILITY REPORT 7 By making a very important investment in 2016, we enabled Boyner not be restricted and purchases will be realized with nominal value. -

Hisse Senedi Veri Bankasi

Günlük Haftalık Aylık 3 Aylık 12 Aylık Yılbaşına Göre 22.04.2021 21.04.2021 15.04.2021 22.03.2021 22.01.2021 22.04.2020 31.12.2020 22 Nisan 2021 HİSSE SENEDİ VERİ BANKASI ENDEKSLER KAPANIŞ P E R F O R M A N S TL US $ Günlük (TL) 1 Hafta (TL/US$) 1 Ay (TL/US$) 3 Ay (TL/US$) YBB (TL/US$) 1 Yıl (TL/US$) BIST-100 1,345.2 162.7 %1.10 -%4.4 -%6.9 -%2.5 -%6.8 -%12.8 -%22.0 -%8.9 -%18.3 %37.0 %15.5 BIST-30 1,412.7 170.8 %1.12 -%3.6 -%6.1 -%1.4 -%5.8 -%14.4 -%23.4 -%13.7 -%22.5 %22.0 %2.8 Mali 1,253.1 151.5 %0.82 -%6.3 -%8.7 -%9.5 -%13.5 -%23.0 -%31.1 -%19.9 -%28.2 %18.2 -%0.4 Sanayi 2,475.9 299.4 %1.65 -%5.3 -%7.7 %0.4 -%4.0 -%3.1 -%13.3 %5.8 -%5.1 %99.0 %67.8 Hizmetler 1,082.1 130.9 %1.35 -%5.5 -%7.9 -%2.5 -%6.8 -%12.7 -%21.9 -%9.3 -%18.6 %28.2 %8.0 Banka 1,086.5 131.4 %0.85 -%4.1 -%6.6 -%9.9 -%13.9 -%28.3 -%35.8 -%30.3 -%37.4 -%9.0 -%23.3 XU100_Getiri 2,350.8 284.3 %1.10 -%4.44 -%6.9 -%0.7 -%5.1 -%11.2 -%20.5 -%7.0 -%16.6 %40.8 %18.7 PİY. -

34 Küresel Markalarin Yerel Stratejileri Ve Advergame

İpek Sucu; Küresel Markaların Yerel Stratejileri ve Advergame Uygulamaları Karşısında Yerel Markaların Rekabet Durumu KÜRESEL MARKALARIN YEREL STRATEJİLERİ VE ADVERGAME UYGULAMALARI KARŞISINDA YEREL MARKALARIN REKABET DURUMU Öğr. Gör. Dr. İpek Sucu* Özet Günümüzde küresel markaların pazarlama stratejilerini küyerelleşme (glocalization) bazında yerel özelliklere nüfuz etmeleri, yekürelleşme (loglobalization) stratejilerini uygulamayan rakip yerel markaların rekabet olanaklarını azaltmaktadır. Küresel markaların küyerel stratejilerin yanında reklam-oyun (advergame) uygulamalarına da ağırlık vermeleri tüketici kitlelerinin küyerel markaları daha fazla talep etmesine teşvik etmektedir. Bu çalışmada küresel markaların küyerel stratejileri ve advergame uygulamaları karşısında yerel markaların ne tür stratejiler uyguladıklarının, uyguladıkları bu stratejiler ile küresel markalar karşısında ne derece rekabet edebildiklerinin ve rekabet olanaklarını arttırabilmek için neler yapılabileceğinin örneklendirilerek değerlendirilmesi amaçlanmaktadır. Bu bağlamda örnek olarak “Coca Cola” ve “Kristal Kola” ile “Nestle” ve “Halk” markaları literatür araştırması kapsamında karşılaştırılarak ele alınacaktır. Anahtar Kelimeler: Küreselleşme, Küyerelleşme, Yeküreselleşme, Advergame, Rekabet. LOCAL STRATEGIES OF GLOBAL BRANDS AND THE COMPETITION OF LOCAL BRANDS IN THE FACE OF ADVERGAME APPLICATIONS Abstract Today, the influence of marketing strategies of global brands into local features on the basis of glocalization decreases the competition possibilities of -

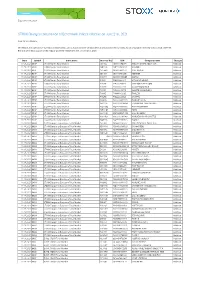

STOXX Changes Composition of Benchmark Indices Effective on June 21St, 2021

Zug, June 11th, 2021 STOXX Changes composition of Benchmark Indices effective on June 21st, 2021 Dear Sir and Madam, STOXX Ltd., the operator of Qontigo’s index business and a global provider of innovative and tradable index concepts, today announced the new composition of STOXX Benchmark Indices as part of the regular quarterly review effective on June 21st, 2021 Date Symbol Index name Internal Key ISIN Company name Changes 11.06.2021 BDXP STOXX Nordic Total Market SE10V2 SE0001174970 MILLICOM INTL.CELU. SDR Addition 11.06.2021 BDXP STOXX Nordic Total Market NO112F NO0010823131 KAHOOT! Addition 11.06.2021 BDXP STOXX Nordic Total Market SE10W3 SE0015483276 CINT GROUP Addition 11.06.2021 BDXP STOXX Nordic Total Market SE10X4 SE0015671995 HEMNET Addition 11.06.2021 BDXP STOXX Nordic Total Market DK3011 DK0060497295 MATAS Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10JH FI4000480215 SITOWISE GROUP Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10HF FI4000049812 VERKKOKAUPPA COM Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10FD FI0009001127 ALANDSBANKEN B Addition 11.06.2021 BDXP STOXX Nordic Total Market FI6036 FI4000048418 AHLSTROM-MUNKSJO Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10IG FI4000062195 TAALERI Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10GE FI4000029905 SCANFIL Addition 11.06.2021 BDXP STOXX Nordic Total Market NO90I2 NO0010861115 NORSKE SKOG Addition 11.06.2021 BDXP STOXX Nordic Total Market NO111E NO0010029804 SPAREBANK 1 HELGELAND Addition 11.06.2021 BDXP STOXX Nordic Total Market NO113G NO0010886625 AKER BIOMARINE Addition 11.06.2021 BDXP STOXX Nordic Total Market NO114H NO0010936792 FROY Addition 11.06.2021 BDXP STOXX Nordic Total Market NO110D BMG9156K1018 2020 BULKERS Addition 11.06.2021 BDXP STOXX Nordic Total Market NO10R3 NO0010196140 NORWEGIAN AIR SHUTTLE Addition 11.06.2021 BDXP STOXX Nordic Total Market NO809S NO0010792625 FJORD1 Deletion 11.06.2021 BKXA STOXX Europe ex Eurozone Total Market SE10V2 SE0001174970 MILLICOM INTL.CELU. -

Günlük Bülten S&P 500 Brent Petrol USD Endeks -%0.29 %0.38 %0.49

Türkiye | Piyasalar 20 Mayıs 2021 Perşembe Günlük Bülten S&P 500 Brent Petrol USD Endeks -%0.29 %0.38 %0.49 Ekonomik Veriler Açıklanacak Veriler Saat Piyasa Yorumu: - - TSİ Bu sabah BIST100’de yatay/negatif yönlü bir açılış bekliyoruz. Hisse Senedi Piyasası Geçtiğimiz günlerde bankacılık hisse senetlerinde güçlü performans olduğu gözlemlenirken bazı sanayi hisselerinden bankacılık hisselerine 35,000 1,470 geçişlerin önümüzdeki günlerde devam edeceğini tahmin ediyoruz. 30,000 1,460 25,000 Bu sabah yatay/negatif açılış ve sonrasında 1450 – 1470 arasında işlem 1,450 20,000 aktivitesi bekliyoruz. 1,440 15,000 1,430 10,000 5,000 1,420 Bugünün Haberleri: 0 1,410 06-May 07-May 10-May 11-May 12-May 17-May 18-May İşlem Hacmi, TRY mln BIST 100 Ekonomik Veriler . Saat 15:30 – Amerika, İşsizlik haklarından yararlanma başvuruları Bono Piyasası . Saat 15:30 – Amerika, Philadelphia Fed istihdam (May) 60.0 18.3 50.0 18.2 18.2 . Saat 17:30 – Türkiye, Merkezi hükümet borç stoku (Nis) 40.0 18.1 30.0 18.1 20.0 18.0 10.0 18.0 0.0 17.9 06-May 07-May 10-May 11-May 12-May 17-May 18-May İşlem Hacmi, TRY mln Türkiye 2030 Endeksler, para piyasaları ve emtia Kapanış Önceki 1 Gün 1 Ay Yıl Baş. BIST100 1,460 1,454 0.4% 6.0% -1.2% İşlem Hacmi, TL mln 24,080 21,610 11.4% 3.4% -34.1% Turkey 2030 (13.11.2030) 18.17% 18.23% -6 bps 20 bps 526 bps Turkey 2030 6.31% 6.26% 5 bps 2 bps 94 bps TCMB karışık fonlama mlyt 19.00% 19.00% 0 bps 0 bps 197 bps USD/TRY 8.41 8.36 0.7% 3.9% 13.1% EUR/TRY 10.25 10.21 0.3% 5.1% 12.9% Sepet (50/50) 9.33 9.29 0.5% 4.5% 13.0% DOW 33,896 34,061 -0.5% -0.5% 10.7% S&P500 4,116 4,128 -0.3% -1.1% 9.6% FTSE 6,950 7,034 -1.2% -0.7% 7.6% MSCI EM 1,328 1,333 -0.4% -1.6% 2.8% MSCI EE 178.69 181.25 -1.4% 6.3% 9.8% Shanghai SE Comp 3,511 3,529 -0.5% 1.0% 1.1% Nikkei 28,044 28,407 -1.3% -5.5% 2.2% Petrol (Brent) 66.92 66.66 0.4% 30.0% 30.0% Altın 1,870 1,869 0.0% 5.5% -1.5% En Çok Yükselen & Düşenler Hisse Kodu Son Kapanış Gün Değ. -

Scotch Whisky, They Often Refer to A

Catalogue Family Overview Styles About the Font LL Catalogue is a contemporary a rising demand for novels and ‘news’, update of a 19th century serif font of these fonts emerged as symptom of Catalogue Light Scottish origin. Initially copied from a new culture of mass education and an old edition of Gulliver’s Travels by entertainment. designers M/M (Paris) in 2002, and In our digital age, the particularities Catalogue Light Italic first used for their redesign of French of such historical letterforms appear Vogue, it has since been redrawn both odd and unusually beautiful. To from scratch and expanded, following capture the original matrices, we had Catalogue Regular research into its origins and history. new hot metal types moulded, and The typeface originated from our resultant prints provided the basis Alexander Phemister’s 1858 de- for a digital redrawing that honoured Catalogue Italic sign for renowned foundry Miller & the imperfections and oddities of the Richard, with offices in Edinburgh and metal original. London. The technical possibilities We also added small caps, a Catalogue Bold and restrictions of the time deter- generous selection of special glyphs mined the conspicuously upright and, finally, a bold and a light cut to and bold verticals of the letters as the family, to make it more versatile. Catalogue Bold Italic well as their almost clunky serifs. Like its historical predecessors, LL The extremely straight and robust Catalogue is a jobbing font for large typeface allowed for an accelerated amounts of text. It is ideally suited for printing process, more economical uses between 8 and 16 pt, provid- production, and more efficient mass ing both excellent readability and a distribution in the age of Manchester distinctive character. -

STOXX EASTERN EUROPE 300 Selection List

STOXX EASTERN EUROPE 300 Last Updated: 20210802 ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) Rank (FINAL)Rank (PREVIOUS) RU0009024277 B59SNS8 LKOH.MM EV020 LUKOIL RU RUB Large 50.2 1 1 RU0007661625 B59L4L7 GAZP.MM EV019 GAZPROM RU RUB Large 39.4 2 2 RU0009029540 4767981 SBER.MM EV023 SBERBANK RU RUB Large 36.3 3 3 RU000A0DKVS5 B59HPK1 NVTK.MM B058LB NOVATEK RU RUB Large 35.3 4 4 RU0007288411 B5B1TX2 GMKN.MM EV022 MMC NORILSK NICKEL RU RUB Large 20 5 5 RU0008926258 B5BHQP1 SNGS.MM EV014 SURGUTNEFTEGAS RU RUB Large 13.4 6 6 HU0000061726 7320154 OTPB.BU 732015 OTP BANK HU HUF Large 10.8 7 7 RU0009033591 B59BXN2 TATN.MM EV015 TATNEFT RU RUB Large 8.7 8 8 RU000A0J2Q06 B59SS16 ROSN.MM EV021 ROSNEFT RU RUB Large 7.8 9 9 PLPKO0000016 B03NGS5 PKO.WA B03NGS PKO BANK PL PLN Large 7.3 10 10 RU000A0JKQU8 B59GLW2 MGNT.MM EV050 MAGNIT RU RUB Large 6.3 11 11 RU000A0JP7J7 B59Q6G1 PIKK.MM EV007 PIK SHB RU RUB Large 5.9 12 14 PLKGHM000017 5263251 KGH.WA 526325 KGHM PL PLN Large 5.8 13 12 LU2237380790 BMBQDF6 ALEP.WA PL00OY ALLEGRO.EU PL PLN Large 5.6 14 13 RU000A0JNAA8 B57R0L9 PLZL.MM EV010 POLYUS RU RUB Large 5.2 15 16 PLPKN0000018 5810066 PKN.WA 581006 PKNORLEN PL PLN Large 5 16 15 PLPZU0000011 B63DG21 PZU.WA PL001B PZU GROUP PL PLN Large 4.7 17 18 RU0007252813 B6QPBP2 ALRS.MM RU501R ALROSA RU RUB Large 4.6 18 17 RU0009046510 B5B9C59 CHMF.MM EV013 SEVERSTAL RU RUB Large 4 19 21 CZ0005112300 5624030 CEZP.PR 562403 CEZ CZ CZK Large 3.8 20 19 RU0009046452 B59FPC7 NLMK.MM EV009 NLMK RU RUB Large 3.7 21 25 PLPEKAO00016 5473113 -

“Kapt›Rmasayd›N›Z!”

Türk k›z›n› sokak ortas›nda öldüresiye dövdüler Elin k›r›ls›n dazlak kafa Haberin devam› S.5’de “Kapt›rmasayd›n›z!” Say› 36 / Tem-A¤ust 2003 / Kostenlos ‹nan›lmaz ama gerçek Türkiye’den Avusturya’ya 240 otobüs TEMSA adl› Türk flirketi Nieder- österreich Eyaleti’nin Posta kuru- munun ihalesini bile¤inin hakk› ile kazanarak 240 adet otobüs satt›. 50 adet teslim edildi. Geri kalan› dört y›l içinde teslim edilecek. Haberin devam› sayfa 32’de Baflbakan Tayyip Erdo¤an, “faizsiz kazanç” vadi ile yurt d›fl›nda çal›flan Türklerin al›n WIENSTROM ile emin ellerde teri tassaruflar›n› toplayan sözde holdinglerin ma¤durlar›na Viyana'da “kapt›rma- sayd›n›z!” dedi. Millenium City ‹fl Merkezi toplant› salonunda Viyana’da yaflayan Türkler ile bir araya gelen Erdo¤an, “Türkiye'de bundan sonra haks›zl›k ve yolsuz- luk olmayacak. Tüyü bitmemifl yetimlerin hakk›n› yemeyecek ve yedirtmeye- ce¤iz” dedi. Erdo¤an'›n bu sözü üzerine, bir vatandafl, faizsiz kazanç sözü vererek holdinglerin kendilerinden ald›klar› alin teri paralar› geri vermedi¤ini belirterek, "Hol- WIENSTROM’da dinglere kapt›rd›¤›m›z paralar› da kurtar›n. Onlara da yedirtmeyin" diye seslenin- derhal daha ce, Erdo¤an, "Çok hatalar›n›z var. Bu holdinglere para verirken kime sordunuz? uygun elektrik. Kapt›rmasayd›n›z!" fleklinde cevap verdi. Erdo¤an’›n konuflmas› Türkiye seninle gurur duyuyor sözleri ile yer yer kesildi. Yorum ve haberler sayfa 2,3 ve 4’te Sayfa 2 BAÞ YAZI Sayý 36 Baþyazý HoldingZEDELER Baþbakan Erdoðan’dan yardým bekliyor! Birol KILIÇ Avusturya’da baþta YÝMPAÞ ruz.