Hspa Gsm- Umts

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Gsma Lança Iniciativas De Serviços Móveis Com O Governo E As Operadoras Brasileiras

GSMA LANÇA INICIATIVAS DE SERVIÇOS MÓVEIS COM O GOVERNO E AS OPERADORAS BRASILEIRAS 25 de fevereiro de 2014, Barcelona: A GSMA anunciou hoje várias iniciativas para melhorar o alcance e a escala dos serviços móveis no Brasil, em benefício de seus cidadãos e empresas. Paulo Bernardo, ministro das Comunicações do Brasil, e Anne Bouverot, diretora geral da GSMA, assinaram um acordo sob o qual a GSMA e o Governo brasileiro vão trabalhar juntos para acelerar a adoção da banda larga móvel e a entrega de novos serviços móveis no Brasil. Além disso, a GSMA e todas as operadoras de celular do Brasil – Algar Telecom, Claro, Nextel, Oi, Sercomtel, TIM Brasil e Vivo – anunciaram sua colaboração para proporcionar aos usuários experiências móveis mais convenientes e seguras, por meio de um conjunto de iniciativas que abordam questões como spam por SMS, roubo de aparelhos e proteção à criança. “Com aproximadamente 115 milhões de assinantes exclusivos e 277 milhões de conexões móveis, o Brasil é o maior mercado móvel na América Latina,” afirmou Anne Bouverot, diretora geral, GSMA. “Trabalhando em conjunto com o governo do Brasil e as operadoras móveis do país, continuaremos a expandir o alcance das redes e serviços móveis no Brasil, e a garantir que todos os clientes possam desfrutar dos benefícios de um ambiente mais confiável e protegido.” GSMA e Memorando de Entendimento com o Brasil A GSMA e o Ministério das Comunicações vão abordar uma série de áreas principais para acelerar a adoção de redes de banda larga móvel e serviços em todo o país. A GSMA vai oferecer sua experiência global e facilitar o diálogo em áreas como comunicações máquina a máquina (M2M), mHealth e mEducation, entre outras. -

Prospecto-Preliminar-Gvt.Pdf

Prospecto Preliminar de Oferta Pública de Distribuição Primária de Ações Ordinárias de Emissão da GVT (Holding) S.A. ospecto Preliminar está sujeito a a sujeito está Preliminar ospecto GVT (HOLDING) S.A. Companhia Aberta de Capital Autorizado - CVM nº 02011-7 CNPJ nº 03.420.904/0001-64 - NIRE nº 41300071331 Rua Lourenço Pinto, nº 299, 4º andar, Curitiba, PR Código ISIN BRGVTTACNOR8 52.000.000 Ações Valor da Distribuição: R$[●] odo de distribuição. No contexto desta Oferta (conforme definido abaixo), estima-se que o Preço por Ação (conforme definido abaixo) estará situado entre R$11,00 e R$16,00, ressalvado, no entanto, que o Preço por Ação poderá, eventualmente, ser fixado fora dessa faixa indicativa. nifestou a seu respeito. O presente Pr A GVT (Holding) S.A. (“Companhia”) está realizando uma oferta pública primária de 52.000.000 ações ordinárias (“Oferta”), todas nominativas, escriturais, sem valor nominal (“Ações”), a ser realizada na República Federativa do Brasil (“Brasil”), sob a coordenação do Banco de Investimentos Credit Suisse (Brasil) S.A. (“Coordenador Líder”) e do Banco UBS Pactual S.A. (“UBS Pactual” e, em conjunto com o Coordenador Líder “Coordenadores”), com esforços de colocação no exterior a serem realizados por Credit Suisse Securities (USA) LLC, UBS Securities LLC, ABN AMRO Inc. e J.P. Morgan Securities, Inc. A Oferta e o aumento de capital com a emissão das Ações foram aprovados por deliberação do Conselho de Administração da Companhia, em reunião realizada em 12 de janeiro de 2007, conforme ata a ser publicada no Diário Oficial do Estado do Paraná e nos jornais “Gazeta do Povo” de Curitiba e “Valor Econômico”, edição nacional. -

Interior Ago/Oct

editorial na de las características más importantes de nuestra Empresa es el impacto que ésta tiene en los más diversos ámbitos de la comunidad, pues además de las actividades propias del negocio, realiza acciones que promueven beneficios para los mexicanos, convirtiéndose así en un ejemplo a seguir por las diferentes compañías e instituciones de U nuestro país y del mundo. Por ello, la reciente apertura del Centro de Tecnología Telmex cobra gran relevancia, ya que además de ser un espacio en el que los visitantes conocen lo que ofrece nuestra Empresa y la tecnología de punta que poseemos, pueden interactuar con los productos y servicios que permiten a las personas transformar sus actividades cotidianas, estrechando el contacto humano, incrementando su productividad, mejorando su forma de hacer negocios y haciendo su vida más fácil. Otro importante impacto comunitario se da en el plano de la calidad, pues ésta no sólo beneficia a nuestros Clientes, sino a todo aquel con quien establezcamos relaciones de negocios; en este sentido destaca el esfuerzo conjunto del equipo LADA para darle a Telmex la primera Certificación ISO 9001/2000 Multisitio a nivel mundial, como un merecido reconocimiento a la calidad de sus áreas, procesos y servicios. Con ello, nuestros Clientes pueden tener la seguridad de que cuentan con el mejor servicio de larga distancia del mundo. Asimismo debemos recordar el beneficio ambiental y, para muestra, basta el botón más representativo y reconocido de la Empresa: el COAE Telmex, el comité que ha hecho del ahorro de energía el reflejo de nuestros más altos valores e ideales en beneficio de las generaciones futuras. -

Madam Prosecutor: Elisa María A. CARRIÓ, on My Own Behalf

Madam Prosecutor: Elisa María A. CARRIÓ, on my own behalf, National Deputy domiciled at my public office located at Riobamba 25, office 708 (Attached to the 2nd Chamber of Deputies of the Nation), in this Federal Capital, in case No. 3559/2015, I come before the representative of the Public Prosecutor’s Office and respectfully state as follows: I. PURPOSE: I enclose the following information on the occasion of submitting my witness statement on today’s date, which I believe will be of use in clarifying the events being investigated in the present case. II. IRAN’S INTELLIGENCE WAR AND THE THREE ATTACKS PERPETRATED AGAINST ARGENTINA. Iran has launched an intelligence war in the struggle it is waging against its regional enemies who do not belong to the Shiite crescent (Israel and Saudi Arabia), which it is perpetrating utilizing two major groups: the traditional Iranian grouping on the one hand and that composed of terrorist organizations such as the Lebanese Hezbollah group on the other; this intelligence is gathered via mosques and is characterized by the perpetration of terrorist attacks as a means of attacking its enemies (The regime of the ayatollah). The attacks carried out by the second group, to which Mahmoud Ahmadinejad and Mohsen Rabbani, among others, have belonged are perpetrated wherever in the world that favorable conditions exist to carry them out through lack of vigilance, the availability of local connections, etc. [Islamic] Jihad, which means resistance or guerrilla warfare, was founded with Iranian assistance in Beirut. This intelligence war prompted the first ever attack on Argentine soil, against the Israeli Embassy in Buenos Aires. -

Ready Awarded It to Operators by the End of 2016, Whereas Mexico Has Already Allocated 90 Mhz of That Band to Those in Charge of Deploying the Shared Network

TABLE OF CONTENTS TABLE OF CONTENTS ............................................................................................................ 2 EXECUTIVE SUMMARY ........................................................................................................... 3 INTRODUCTION ...................................................................................................................... 6 ITU MOBILE SPECTRUM SUGGESTIONS .............................................................................. 8 ITU RECOMMENDATIONS: SPECTRUM ALLOCATION FOR THE DEVELOPMENT OF IMT AND IMT-ADVANCED TECHNOLOGIES .............................................................................. 9 LATIN AMERICA SPECTRUM OVERVIEW ............................................................................ 10 FUTURE OF THE RADIO SPECTRUM IN LATIN AMERICA ................................................... 12 CHALLENGES TO AWARD THE RADIO SPECTRUM ............................................................ 15 CONCLUSION ........................................................................................................................ 16 APPENDIX A: LATIN AMERICA MARKETS PROFILES ......................................................... 18 ARGENTINA ....................................................................................................................... 18 BOLIVIA ............................................................................................................................. 18 BRAZIL .............................................................................................................................. -

Information Economy Report 2009 Trends and Outlook in Turbulent Times

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT Information Economy Report 2009 Trends and Outlook in Turbulent Times New York and Geneva, 2009 ii Information Economy Report 2009 NOTE Within the UNCTAD Division on Technology and Logistics, the ICT Analysis Section carries out policy-oriented analytical work on the development implications of information and communication technologies (ICTs). It is responsible for the preparation of the Information Economy Report. The ICT Analysis Section promotes inter- national dialogue on issues related to ICTs for development and contributes to building developing countries’ capacities to measure the information economy, as well as to design and implement relevant policies and legal frameworks. In this report, the terms country/economy refer, as appropriate, to territories or areas. The designations employed and the presentation of the material do not imply the expression of any opinion whatsoever on the part of the Secretariat of the United Nations concerning the legal status of any country, territory, city or area or of its authori- ties, or concerning the delimitation of its frontiers or boundaries. In addition, the designations of country groups are intended solely for statistical or analytical convenience and do not necessarily express a judgement about the stage of development reached by a particular country or area in the development process. The major country groupings used in this report follow the classification of the United Nations Statistical Office. These are: Developed countries: the member countries of the Organization for Economic Cooperation and Development (OECD) (other than Mexico, the Republic of Korea and Turkey), plus the new European Union member countries that are not OECD members (Bulgaria, Cyprus, Estonia, Latvia, Lithuania, Malta, Romania and Slovenia), plus Andorra, Israel, Liechtenstein, Monaco and San Marino. -

Global Rich Communication Services (RCS) Market Analysis and Forecast (2013 – 2018)

IndustryARC Global Rich Communication Services (RCS) Market Analysis and Forecast (2013 – 2018) VAS and VoLTE Main Features of Growing MNO Deployability Strategies IndustryARC | 1 TABLE OF CONTENTS 1. Global Rich Communication Services – Market Overview 2. Executive Summary 3. Global Rich Communication Services – Market Landscape 3.1. Market Share Analysis 3.2. Comparative Analysis 3.2.1. Product Benchmarking 3.2.2. End user profiling 3.2.3. Patent Analysis 3.2.4. Top 5 Financials Analysis 4. Global Rich Communication Services – Market Forces 4.1. Market Drivers 4.2. Market Constraints 4.3. Market Challenges 4.4. Attractiveness of the Rich Communication Services Industry 4.4.1. Power of Suppliers 4.4.2. Power of Customers 4.4.3. Threat of New entrants 4.4.4. Threat of Substitution 4.4.5. Degree of Competition 5. Global Rich Communication Services Market – Strategic Analysis 5.1. Value Chain Analysis 5.2. Pricing Analysis 5.3. Opportunities Analysis IndustryARC | 2 5.4. Product/Market Life Cycle Analysis 5.5. Suppliers and Distributors 5.6. Business Model 5.6.1. B2C 5.6.2. B2B 5.6.3. B2B2x 6. Rich Communication Services Market by Applications 6.1. Mobile Commerce 6.2. Cloud Storage/Access 6.3. LTE Direct 6.4. Rich Calls and Messaging 6.5. Video 6.6. Enterprise 6.7. Others 6.7.1. Social 6.7.2. VAS 7. Rich Communication Services Market by Solution Types 7.1. Unified Messaging 7.2. Web Conferencing 7.3. VoIP 7.4. Online Storage 7.5. File Transfer/Content Sharing 7.6. -

Informe Estadístico Soy Usuario Enero-Marzo 2019 Informe Estadístico Soy Usuario Enero-Marzo 2019

INFORME ESTADÍSTICO SOY USUARIO ENERO-MARZO 2019 INFORME ESTADÍSTICO SOY USUARIO ENERO-MARZO 2019 ÍNDICE Introducción ...................3 Datos generales .............5 Servicios Móviles ..........10 Servicios Fijos .............14 Conclusiones ...............18 INICIO INTRODUCCIÓN DATOS GENERALES SERVICIOS MÓVILES SERVICIOS FIJOS CONLUSIONES 2 INFORME ESTADÍSTICO SOY USUARIO ENERO-MARZO 2019 El sistema Soy Usuario es resultado del Convenio de Colaboración suscrito entre el IFT y la Procuraduría Federal del Consumidor (PROFECO) en el año 2014 y renovado el 20 de septiembre de 2016, con la finalidad de fortalecer los mecanismos de atención e intercam- bio de información en beneficio de los usuarios de telecomunicaciones. Se trata de una herramienta de fácil uso a través de Internet que permite un mayor acercamiento entre los prestadores de servicios de telecomunicaciones y sus clientes, así como entre los usuarios de estos servicios y las autoridades, ya que privilegia el proceso de pre conciliación. La plataforma obtuvo el reconocimiento de Buenas Prácticas 2016 por parte de la organi- zación internacional Regulatel. Además, fue galardonada con el premio WSIS Champion otorgado por la Unión Internacional de Telecomunicaciones en el marco de la Cumbre Mundial sobre la Sociedad de la Información 2017. La información estadística que se presenta, contempla el número de inconformidades in- gresadas del 1 de enero al 31 de marzo de 2019 y tiene la finalidad de dar a conocer el comportamiento de las empresas y la atención que brindan a los usuarios que ingresan inconformidades a través de la plataforma. Entre la información relevante que se puede consultar, se encuentran los Estados de la Repú- blica con mayor número de inconformidades; el tipo de problemáticas reportadas; el número de folios canalizados a PROFECO; el número de inconformidades asesoradas por la PROFE- INTRODUCCIÓN CO; así como el ranking de atención tanto para servicios móviles como fijos. -

Estrategias Comerciales Incorporada a La Secretaría De Educación Pública Rvoe 20122890

ECEE MAESTRÍA EN ESTRATEGIAS COMERCIALES INCORPORADA A LA SECRETARÍA DE EDUCACIÓN PÚBLICA RVOE 20122890 TESIS “Estrategia de Comercialización para los Servicios de Contenidos Móviles en México” QUE PARA OBTENER EL GRADO ACADÉMICO DE: MAESTRA EN ESTRATEGIAS COMERCIALES PRESENTA: Natalia Rebeca Valencia García DIRECTOR: Dr. Sergio Garcilazo Lagunes Ciudad de México, 2017. 1 Contenido ÍNDICE DE TABLAS, FIGURAS Y GRÁFICAS ................................................... 6 RESUMEN .............................................................................................................. 7 INTRODUCCIÓN .................................................................................................... 8 Capítulo 1. MARCO TÉORICO Y CONCEPTAL ................................................... 11 1.1. Marketing de servicios .............................................................................. 11 1.2 La oferta de telefonía móvil como servicio. ............................................... 12 1.2.1 Oferta Pospago ......................................................................................... 12 1.2.2 Oferta Prepago ......................................................................................... 12 1.2.3. Servicios Adicionales ............................................................................... 13 1.2.3.1 Servicios de Contenidos Móviles ........................................................... 13 1.2.3.1.1 Tipos de servicios de contenidos ........................................................ 14 -

Latin America Pay TV Decelerates

Latin America pay TV decelerates Although the economic recession waned somewhat in 2017, the Latin American pay TV sector was still affected. According to the eighth edition of the Latin America Pay TV Forecasts report, the number of pay TV subscribers was flat year-on-year. Fewer than 5 million additional pay TV subscribers are expected between 2017 and 2023 – bringing the total to almost 76 million. Pay TV penetration will not climb beyond the current 44% of TV households. Latin America pay TV subscribers by country (000) 80,000 70,000 60,000 50,000 40,000 30,000 20,000 10,000 0 2017 2018 2023 Others 18,552 18,953 20,808 Colombia 5,557 5,691 6,161 Argentina 9,253 9,388 9,599 Brazil 18,181 17,839 19,656 Mexico 19,417 19,283 19,560 Source: Digital TV Research Ltd Simon Murray, Principal Analyst at Digital TV Research, said: “Given its continuing economic and social problems, Brazil lost 1 million pay TV subscribers between 2015 and 2017. Its peak year of 2014 will not be bettered until 2023.” Murray continued: “Mexico recorded impressive growth in 2016, but its pay TV subscriber count fell in 2017. It will continue to decline until a slow recovery starts in 2020. The 2023 total will be just under the 2016 peak. However, it’s not all bad news as Claro and Telefonica will enter Argentina and Mexico, although this is likely to involve OTT.” Mexico overtook Brazil in 2016 to become Latin America’s largest pay TV market, despite Brazil having twice as many TV households as Mexico. -

Processo Nº 53500.010080/2019-55 Interessado: Algar Telecom S/A, ALGAR CELULAR S.A., Algar Multimídia S/A, Brasil Telecom Comunicação Multimídia Ltda

13/06/2019 2301 Página 1 de 1 Imprimir Boletim de Serviço Eletrônico em 13/06/2019 AGÊNCIA NACIONAL DE TELECOMUNICAÇÕES DESPACHO DECISÓRIO Nº 3/2019/RCTS/SRC Processo nº 53500.010080/2019-55 Interessado: Algar Telecom S/A, ALGAR CELULAR S.A., Algar Multimídia S/A, Brasil Telecom Comunicação Multimídia Ltda. (02.041.460/0001-93), OI S.A. - EM RECUPERAÇÃO JUDICIAL, OI MÓVEL S.A. - EM RECUPERAÇÃO JUDICIAL, Telemar Norte Leste S.A., Claro S.A., TELMEX DO BRASIL S/A, Embratel TVsat Telecomunicações S.A., Empresa Brasileira de Telecomunicações S.A. (Embratel), Nextel Telecomunicações Ltda., Sercomtel Participações S.A., Sercomtel S.A. - Telecomunicações, Telefônica Brasil S.A., TIM S.A., Sky Serviços de Banda Larga Ltda. A SUPERINTENDENTE DE RELAÇÕES COM CONSUMIDORES DA AGÊNCIA NACIONAL DE TELECOMUNICAÇÕES, no uso de suas atribuições legais e regulamentares, em especial a disposta no art. 160, I e IV, do Regimento Interno da ANATEL, aprovado pela Resolução nº 612, de 29 de abril de 2013, considerando: - as razões e justificativas constantes do Informe nº 49/2019/RCTS/SRC (4265244), e - a conveniência e oportunidade da proposta de implementação de mecanismo nacional e centralizado para o registro de intenções de bloqueio dos consumidores para que não recebam ligações de telemarketing, apresentada pelos Interessados em correspondências protocoladas nos autos dos processos nº 53500.012093/2019-69 (Grupo Oi), 53500.012094/2019-11 (Grupo Algar), 53500.012095/2019-58 (Grupo Claro), 53500.012098/2019-91 (Nextel), 53500.012100/2019-22 (Grupo Sercomtel), 53500.012102/2019-11 (Sky), 53500.012103/2019-66 (Grupo Tim), 53500.012104/2019-19 (Grupo Telefônica), DECIDE, com fundamento nos arts. -

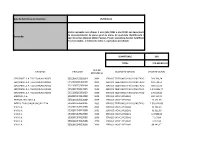

Data De Referência Do Relatório: 05/06/2012 Demanda

Data de Referência do Relatório: 05/06/2012 Multas aplicadas nos últimos 3 anos (abr/2009 a abr/2012) em decorrência de descumprimento de plano geral de metas de qualidade identificando o Demanda: tipo de serviço (Serviço Móvel Pessoal, TV por assinatura, Serviço Telefônico Fixo Comutado), o motivo da multa e a operadora penalizada. QUANTIDADE 190 TOTAL 275.429.825,32 ANO DE ENTIDADE PROCESSO DESCRIÇÃO SERVIÇO VALOR APLICADO REFERÊNCIA SERCOMTEL S.A. TELECOMUNICACOES 535160049302004 2009 SERVICO TELEFONICO FIXO COMUTADO 519.399,24 SERCOMTEL S.A. TELECOMUNICACOES 535000238592008 2009 SERVICO TELEFONICO FIXO COMUTADO 878.744,51 SERCOMTEL S.A. TELECOMUNICACOES 535160075292004 2009 SERVICO TELEFONICO FIXO COMUTADO 489.531,50 SERCOMTEL S.A. TELECOMUNICACOES 535000139942005 2009 SERVICO TELEFONICO FIXO COMUTADO 1.240.985,77 SERCOMTEL S.A. TELECOMUNICACOES 535160016202003 2009 SERVICO TELEFONICO FIXO COMUTADO 476.625,50 AMERICEL S.A. 535000134932008 2009 SERVIÇO MOVEL PESSOAL 485.313,33 TELEMIG CELULAR S.A 535000134912008 2009 SERVIÇO MOVEL PESSOAL 17.451,69 INTELIG TELECOMUNICACOES LTDA 535000152642005 2009 SERVICO TELEFONICO FIXO COMUTADO 1.820.426,88 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 34.556,34 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 35.315,00 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 147.886,96 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 7.117,84 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 3.312,94 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 88.443,17 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 65.424,78 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 51.447,53 VIVO S.A.