Smart Networks and Services Version 30 June 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rte Guide Tv Listings Ten

Rte guide tv listings ten Continue For the radio station RTS, watch Radio RTS 1. RTE1 redirects here. For sister service channel, see Irish television station This article needs additional quotes to check. Please help improve this article by adding quotes to reliable sources. Non-sources of materials can be challenged and removed. Найти источники: РТЗ Один - новости газеты книги ученый JSTOR (March 2020) (Learn how and when to remove this template message) RTÉ One / RTÉ a hAonCountryIrelandBroadcast areaIreland & Northern IrelandWorldwide (online)SloganFuel Your Imagination Stay at home (during the Covid 19 pandemic)HeadquartersDonnybrook, DublinProgrammingLanguage(s)EnglishIrishIrish Sign LanguagePicture format1080i 16:9 (HDTV) (2013–) 576i 16:9 (SDTV) (2005–) 576i 4:3 (SDTV) (1961–2005)Timeshift serviceRTÉ One +1OwnershipOwnerRaidió Teilifís ÉireannKey peopleGeorge Dixon(Channel Controller)Sister channelsRTÉ2RTÉ News NowRTÉjrTRTÉHistoryLaunched31 December 1961Former namesTelefís Éireann (1961–1966) RTÉ (1966–1978) RTÉ 1 (1978–1995)LinksWebsitewww.rte.ie/tv/rteone.htmlAvailabilityTerrestrialSaorviewChannel 1 (HD)Channel 11 (+1)Freeview (Northern Ireland only)Channel 52CableVirgin Media IrelandChannel 101Channel 107 (+1)Channel 135 (HD)Virgin Media UK (Northern Ireland only)Channel 875SatelliteSaorsatChannel 1 (HD)Channel 11 (+1)Sky IrelandChannel 101 (SD/HD)Channel 201 (+1)Channel 801 (SD)Sky UK (Northern Ireland only)Channel 161IPTVEir TVChannel 101Channel 107 (+1)Channel 115 (HD)Streaming mediaVirgin TV AnywhereWatch liveAer TVWatch live (Ireland only)RTÉ PlayerWatch live (Ireland Only / Worldwide - depending on rights) RT'One (Irish : RTH hAon) is the main television channel of the Irish state broadcaster, Raidi'teilif's Siranne (RTW), and it is the most popular and most popular television channel in Ireland. It was launched as Telefes Siranne on December 31, 1961, it was renamed RTH in 1966, and it was renamed RTS 1 after the launch of RTW 2 in 1978. -

Master in International Marketing in a Digital Environment Agreement

MASTER IN INTERNATIONAL MARKETING IN A DIGITAL ENVIRONMENT AGREEMENT between IQS School of Management – Universitat Ramon LLull Via Augusta 390, 08017 Barcelona, Spain And FU JEN Catholic University No. 510, Zhongzheng Rd., Xinzhuang Dist. New Taipei City 24205, Taiwan IQS School of Management – Universitat Ramon Llull (herein referred to as IQS SM) and, Fu Jen Catholic University (herein referred to as Fu Jen) agree to the following terms. 1 Terms: I. Purpose The purpose of this agreement is to establish the possibility for FU JEN students to complete their second master year at IQS SM and to complete the Master in International Marketing in a Digital Environment at IQS SM (University Ramon Llull). According to this agreement, a maximum of 4 FU JEN students can apply to spend: One year at the IQS SM to take 60 ECTS during the entire academic year. Upon completion of all credits, FU JEN students will earn the official diploma Master in International Marketing in a Digital Environment (see the program courses in the appendix 1). II. Selection of Students FU JEN will screen applications from its student body. The Master is aimed at university graduates in the economy, business, marketing, management and tourism fields. Applicants that come from a different Social Sciences fields or with a different academic background, such as Engineering, will be asked to enrol to the following complementary training courses: Marketing Principles and Strategies (6 ECTS) and Accounting for Decision Making (3 ECTS). Other applicants that come from Advertising and Public Relations field will be asked to enrol to the following complementary training course: Accounting for Decision Making (3 ECTS). -

Cable Tv Scrolling Software Free Download

Cable tv scrolling software free download Movies; Songs Playing randomly and sequence; Religious Video(Bhajan); YouTube Live Streaming and Video Play; Serial Daily Sop Episode. Cable TV Software for broadcasting of TV Channel with various Locations like Internet TV, IPTV, and Cable Operator LCO for Local TV Channel, MSO Multi. Download Scrolling Software For Cable Tv - best software for Windows. Cable Player: Cable Player is a Entry Level digital video player for cable TV operators. A/V Broadcast System for Cable TV is a professional and reliable digital video broadcast software designed for cable TV operators. With A/V Scrolling & Animated Ad: displays ad crawlers at the any position of the screen. visit on web - contact No. + Cable TV Software, Media On Air software, Tv. It's a free all-in-one application for all of your entertainment needs. Search and download over songs directly to your PC, or listen over+ radio & TV Scrolling & Animated Ad: displays ad crawlers at the any position of the screen. Cable Player is a Entry Level digital video player for cable TV operators. Built-in titler with Easy-to-create scrolls and special effects like. Top/Bottom Scrolling Ad, Visual Ad, Live/Recorded Shows, slot booking. tv, tv advertising job description, local cable tv advertising software free download, tv. You want cable tv player software or broadcasting software for TV possibility for using as digital signage software along with smooth scrolls or ad scrolling from. Mx player cable tv software free download found at. TV Channel Automation Playout software - For Cable TV Channel RTF Scrolling in Titler. -

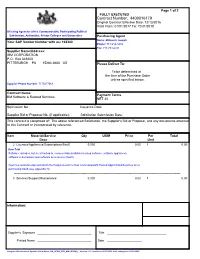

Contract Number: 4400016179

Page 1 of 2 FULLY EXECUTED Contract Number: 4400016179 Original Contract Effective Date: 12/13/2016 Valid From: 01/01/2017 To: 12/31/2018 All using Agencies of the Commonwealth, Participating Political Subdivision, Authorities, Private Colleges and Universities Purchasing Agent Name: Millovich Joseph Your SAP Vendor Number with us: 102380 Phone: 717-214-3434 Fax: 717-783-6241 Supplier Name/Address: IBM CORPORATION P.O. Box 643600 PITTSBURGH PA 15264-3600 US Please Deliver To: To be determined at the time of the Purchase Order unless specified below. Supplier Phone Number: 7175477069 Contract Name: Payment Terms IBM Software & Related Services NET 30 Solicitation No.: Issuance Date: Supplier Bid or Proposal No. (if applicable): Solicitation Submission Date: This contract is comprised of: The above referenced Solicitation, the Supplier's Bid or Proposal, and any documents attached to this Contract or incorporated by reference. Item Material/Service Qty UOM Price Per Total Desc Unit 2 Licenses/Appliances/Subscriptions/SaaS 0.000 0.00 1 0.00 Item Text Software: includes, but is not limited to, commercially available licensed software, software appliances, software subscriptions and software as a service (SaaS). Agencies must develop and attach the Requirements for Non-Commonwealth Hosted Applications/Services when purchasing SaaS (see Appendix H). -------------------------------------------------------------------------------------------------------------------------------------------------------- 3 Services/Support/Maintenance 0.000 0.00 -

Sky Italia 1 Sky Italia

Sky Italia 1 Sky Italia Sky Italia S.r.l. Nazione Italia Tipologia Società a responsabilità limitata Fondazione 31 luglio 2003 Fondata da Rupert Murdoch Sede principale Milano, Roma Gruppo News Corporation Persone chiave • James Murdoch: Presidente • Andrea Zappia: Amministratore Delegato • Andrea Scrosati: Vicepresidente Settore Media Prodotti Pay TV [1] Fatturato 2,740 miliardi di € (2010) [1] Risultato operativo 176 milioni di € (2010) [2] Utile netto 439 milioni di € (2009) Dipendenti 5000 (2011) Slogan Liberi di... [3] Sito web www.sky.it Sky Italia S.r.l. è la piattaforma televisiva digitale italiana del gruppo News Corporation, nata il 31 Luglio 2003 dall’operazione di concentrazione che ha coinvolto le due precedenti piattaforme Stream TV e Telepiù. Sky svolge la propria attività nel settore delle Pay TV via satellite, offrendo ai propri abbonati una serie di servizi, anche interattivi, accessibili previa installazione di una parabola satellitare, mediante un ricevitore di decodifica del segnale ed una smart card, abilitata alla visione dei contenuti diffusi da Sky. Sky viene diffusa agli utenti via satellite dalla flotta di satelliti Hot Bird posizionata a 13° est (i satelliti normalmente utilizzati per i servizi televisivi destinati all'Italia) e via cavo con le piattaforme televisive commerciali IPTV: TV di Fastweb, IPTV di Telecom Italia e Infostrada TV. Sky Italia 2 Storia • 2003 • Marzo: la Commissione europea autorizza la fusione tra TELE+ e Stream, da cui nasce Sky Italia. • Luglio: il 31 luglio Sky Italia inizia ufficialmente a trasmettere. • 2004 • Aprile: Sky abbandona il sistema di codifica SECA per passare all'NDS, gestito da News Corporation. -

Global Pay TV Fragments

Global pay TV fragments The top 503 pay TV operators will reach 853 million subscribers from the 1.02 billion global total by 2026. The top 50 operators accounted for 64% of the world’s pay TV subscribers by end-2020, with this proportion dropping to 62% by 2026. Pay TV subscribers by operator ranking (million) 1200 1000 143 165 38 45 800 74 80 102 102 600 224 215 400 200 423 412 0 2020 2026 Top 10 11-50 51-100 101-200 201+ Excluded from report The top 50 will lose 20 million subscribers over the next five years. However, operators beyond the top 100 will gain subscribers over the same period. Simon Murray, Principal Analyst at Digital TV Research, said: “Most industries consolidate as they mature. The pay TV sector is doing the opposite – fragmenting. Most of the subscriber growth will take place in developing countries where operators are not controlled by larger corporations.” By end-2020, 13 operators had more than 10 million pay TV subscribers. China and India will continue to dominate the top pay TV operator rankings, partly as their subscriber bases climb but also due to the US operators losing subscribers. Between 2020 and 2026, 307 of the 503 operators (61%) will gain subscribers, with 13 showing no change and 183 losing subscribers (36%). In 2020, 28 pay TV operators earned more than $1 billion in revenues, but this will drop to 24 operators by 2026. The Global Pay TV Operator Forecasts report covers 503 operators with 726 platforms [132 digital cable, 116 analog cable, 279 satellite, 142 IPTV and 57 DTT] across 135 countries. -

European SME Expertise in 5G and Beyond COMPANY PROFILES

This material has been designed and printed with support from the Full5G project and the NetWorld2020 SME Working Group. The Full5G Project has received funding by the European Commission’s Horizon 2020 Programme under the grant agreement number: 856777. European The European Commission support for the production of this publication does not constitute endorsement of the contents which reflects the views only of the authors, and the Commission SME Expertise cannot be held responsible for any use which may be made of the information contained therein. The NetWorld2020 SME Working Group and the NetWorld2020 in 5G and Beyond European Technology Platform cannot be held responsible for the information provided by the SMEs and for the quality of their potential contribution. More information at www.networld2020.eu/sme-support Co-funded by the Horizon 2020 programme of the European Union Co-funded by the Horizon 2020 programme of the European Union SME MEMBERS Citypassenger France INTEGRASYS Spain INTERINNOV France Martel GmbH Switzerland Nextworks s.r.l. Italy USEFUL LINKS Oledcomm France QUOBIS NETWORKS Spain Satelio IOT Services Spain Find the SME you need Seven Solutions S.L. Spain www.networld2020.eu/find-the-sme-you-need/ NetWorld2020 SME support www.networld2020.eu/sme-support NetWorld2020 European Technology Platform www.networld2020.eu 5G Public-Private Partnership www.5g-ppp.eu This document is released in June 2020 by the NetWorld2020 SME Working Group, with support from the Full5G project, from the NetWorld2020 European Technology Platform, and from the 5G Infrastructure Association. JACQUES MAGEN NICOLA CIULLI interinnov Nextworks Chair of the Vice-chair of the SME Working Group SME Working Group EDITORIAL I can hardly believe that this June 2020 edition of the “SME I am very happy to join our SME WG Chair, Jacques Magen, in brochure” is already the 4th annual edition. -

Zerohack Zer0pwn Youranonnews Yevgeniy Anikin Yes Men

Zerohack Zer0Pwn YourAnonNews Yevgeniy Anikin Yes Men YamaTough Xtreme x-Leader xenu xen0nymous www.oem.com.mx www.nytimes.com/pages/world/asia/index.html www.informador.com.mx www.futuregov.asia www.cronica.com.mx www.asiapacificsecuritymagazine.com Worm Wolfy Withdrawal* WillyFoReal Wikileaks IRC 88.80.16.13/9999 IRC Channel WikiLeaks WiiSpellWhy whitekidney Wells Fargo weed WallRoad w0rmware Vulnerability Vladislav Khorokhorin Visa Inc. Virus Virgin Islands "Viewpointe Archive Services, LLC" Versability Verizon Venezuela Vegas Vatican City USB US Trust US Bankcorp Uruguay Uran0n unusedcrayon United Kingdom UnicormCr3w unfittoprint unelected.org UndisclosedAnon Ukraine UGNazi ua_musti_1905 U.S. Bankcorp TYLER Turkey trosec113 Trojan Horse Trojan Trivette TriCk Tribalzer0 Transnistria transaction Traitor traffic court Tradecraft Trade Secrets "Total System Services, Inc." Topiary Top Secret Tom Stracener TibitXimer Thumb Drive Thomson Reuters TheWikiBoat thepeoplescause the_infecti0n The Unknowns The UnderTaker The Syrian electronic army The Jokerhack Thailand ThaCosmo th3j35t3r testeux1 TEST Telecomix TehWongZ Teddy Bigglesworth TeaMp0isoN TeamHav0k Team Ghost Shell Team Digi7al tdl4 taxes TARP tango down Tampa Tammy Shapiro Taiwan Tabu T0x1c t0wN T.A.R.P. Syrian Electronic Army syndiv Symantec Corporation Switzerland Swingers Club SWIFT Sweden Swan SwaggSec Swagg Security "SunGard Data Systems, Inc." Stuxnet Stringer Streamroller Stole* Sterlok SteelAnne st0rm SQLi Spyware Spying Spydevilz Spy Camera Sposed Spook Spoofing Splendide -

1 Norbert's Homepage

Norbert's Homepage - 11/2016 1 Die Wochenübersicht Nr. 11/2016, vom Freitag, den 01. Juli 2016, nach christlicher Zeitrechnung Autor: Norbert Schlammer Neuigkeiten: Yamal 401, 90 Grad Ost: Rossiya 1 Tver mit Radio Tver rechts zum TV-Ton, auf 3,924 GHz, lz, mit 2,850 und 3/4, Pid's 512/4112, codieren in Biss. Im Gazprom Space Systems HD Digitalpaket, auf 11,092 GHz, h, mit 30,000 und 3/4, in MPEG-4/HD DVB S-2 8PSK, wurde Domashniy Magazin abgeschaltet. Von den 21 TV und sieben Radios, senden 16 TV und alle Radios, offen. Auch auf 11,265 GHz, h, mit denselben Empfangsparametern ist Domashniy Magazin nicht mehr auf Sendung. 13 TV und sieben Radios kommen uncodiert herein, fünf TV-Kanäle codieren in Biss. Auf 11,535 GHz, v, mit 2,645 und 1/2, in MPEG-2/DVB S-2 8PSK, ist nur noch Vestnik Nadyma, Pid's 222/223, auf Sendung - offen. OGRTK Yamal, Region 1, wurde abgeschaltet. Neu sind im Spacecom Space Systems SD Digitalpaket auf dem Nordicbeam, auf 12,718 GHz, v, mit 27,500 und 3/4, Ren TV International und NTW +4h, Pid's 207/307, bzw. 4907/4908. Alle sechs TV- Kanäle kommen unverschlüsselt herein. Horizons 2, 84,9 Grad Ost: Im Orion-Express HD Paket auf dem Westrusslandbeam, auf 11,840 GHz, h, mit 28,800 und 2/3, in MPEG-4/HD DVB S-2 8PSK, ersetzte NTW +2h, Pid's 1807/2807, wie alle 14 TV-Programme in Conax, Irdeto 3 und Quintic codiert, NTW +3h. -

Telecomunicazioni

====== TELECOMUNICAZIONI ================== Telefonia, Internet, TV: notizie, consigli e testimonianze per tutelare i propri diritti e capire cosa si muove in un mondo in continua mutazione Edito da ADUC, Associazione per i Diritti degli Utenti e Consumatori. Redazione: Via Cavour 68, 50129 Firenze Tel: 055.290606 (ore 15-18, da lun. a ven.) Fax: 055.2302452 URL: http://tlc.aduc.it A cura di Domenico Murrone NON DARE PER SCONTATA LA NOSTRA ESISTENZA! Senza il sostegno economico di persone come te non saremmo in grado di informarti. Se ci ritieni utili, sostienici con una donazione http://www.aduc.it/info/sostienici.php ------------------------------------------- Il numero integrale è scaricabile a questi indirizzi in formato TXT o PDF: http://tlc.aduc.it/generale/files/file/newsletter/Tlc-2010-12.txt http://tlc.aduc.it/generale/files/file/newsletter/Tlc-2010-12.pdf ------------------------------------------- Archivio dal 09-09-2010 al 15-09-2010 2010-12 ARTICOLI - Le istituzioni secondo il Televideo Rai: catasto e vescovi, sì! Napolitano, Berlusconi, Fini e Schifani, no! http://tlc.aduc.it/articolo/istituzioni+secondo+televideo+rai+catasto+vescovi_18106.php - Software Windows preinstallato sul PC. Corte Appello conferma motivazioni Aduc per il rimborso. Analisi http://tlc.aduc.it/articolo/software+windows+preinstallato+sul+pc+corte+appello_18122.php COMUNICATI - Easy download. L'Antitrust estende l'indagine sul sito che fa pagare ciò che è gratis http://tlc.aduc.it/comunicato/easy+download+antitrust+estende+indagine+sul+sito_18108.php - Rimborso Windows preinstallato sul pc. Le ragioni della vittoria dell'Aduc. Verso la class action http://tlc.aduc.it/comunicato/rimborso+windows+preinstallato+sul+pc+ragioni+della_18128.php - Piano banda larga. -

Erasmus Policy Statement (Overall Strategy)

Erasmus Policy Statement (Overall Strategy) Institution's international (EU and non-EU) strategy. In a world increasingly globalized, interconnected in real time and with important migration flows, it is very important that a professional knows, communicates, works and lives with people belonging to different cultures, sometimes very different from his own. For this reason, it is essential that in his formative stage, at home, or outside, the student interact with people who come from other parts of the world and, without abandoning his roots, values and beliefs, is open to them. Obviously, to speak other languages is important, especially English. However, speak other languages is necessary, but not sufficient. What matters is to be open-minded and wishing to understand the diversity and learn from it. Aware of its relevance, the University Ramon Llull (URL) gives a great importance to the international dimension with the goal of offering to our students the possibility to end up being good professionals able to do their job inside and outside their country, regardless of the sector. To make it possible, our centres have many agreements with foreign universities in all continents with which they exchange students, develop joint programs, conduct research or make benchmark. Being the Ramon Llull University (URL) a federation of schools, we harmonize the overall strategy with the one of each URL member. The main goal is to give to our community (students, professors, staff…) the opportunity to have a truly international experience. To select a university partner, we look at several aspects like, for example, their prestige, the disciplines they offer, the level of the demand of our community to develop exchanges or projects with them; where they are located, for geographical balance and security reasons; the structure of their programs or their research lines. -

Cop 2012 X Offset

2009 Relazione annuale 2012 sull’attività svolta e sui programmi di lavoro www.agcom.it Relazione annuale sull’attività svolta e sui programmi di lavoro 2012 2.2. Il settore dei media Nel 2011, il settore complessivo dei media (comprensivo sia della pubblicità sia dei ricavi derivanti da offerte a pagamento) ha fatto registrare, in termini nominali, una sostanziale stabilità (+0,5%, che equivale a una contrazione in termini reali di oltre due punti percentuali), dopo la contrazione registrata nel 2009 (-6%) e la ripresa del 2010 (+5%). Questo dato rappresenta il risultato di due dinamiche opposte: da un lato, i media tradizionali (televisione tradizionale, stampa e radio) hanno registrato un calo, dall’altro si è assistito alla crescita dei nuovi media digitali, in particolare legati al mondo internet 2.0. Il 2011 ha visto, quindi, l’affermarsi di forme di accesso alla rete e di fruizione dei contenuti on line non più legate strettamente al computer, ma fruibi- li attraverso device di maggiore appeal per il pubblico italiano, come gli smartphone, i tablet e le connected tv. Il grafico successivo illustra l’evoluzione del settore dei media, in termini di risor- se, dal 2008 al 2011, offrendo significative indicazioni circa i recenti mutamenti nel peso dei diversi mezzi (Figura 2.17). Figura 2.17. Evoluzione delle risorse dei mezzi di comunicazione (milioni di euro) 18.000 Tot. 17.631 Tot. 16.651 Tot. 17.456 Tot. 17.540 Internet 16.000 978 1.026 1.323 1.767 Periodici 3.937 3.292 3.409 Quotidiani 3.274 14.000 Radio 12.000 TV a pagamento 3.252 3.047 2.954 2.896 TV gratuita 10.000 715 697 746 708 8.000 2.901 3.170 3.406 3.415 6.000 5.849 5.420 5.619 5.479 4.000 2.000 0 2008 2009 2010 2011 (*) Per il 2011, il valore riportato nella Figura rappresenta una stima dell’Autorità.