Aviation Strategy for Denmark July 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bluetooth & Wi-Fi Technology Manages Traffic & Airports Passengers

Bluetooth & Wi-Fi Technology manages traffic & airports passengers Today’s traffic with increased demand for mobility, safety and environmental friend- ly travel, requires smart and innovative solutions to optimise and enhance traffic flow. With proven technologies like Bluetooth and Wi-Fi tracking, the cost for col- lecting detailed data for travel time, origin and destination, traffic flow, queuing etc. has decreased significantly compared to traditional technologies like camera detec- tion. Bluetooth and Wi-Fi sensors are easy to deploy and maintenance cost are close to zero. It gives municipalities & road authorities a range of new possibilities to collect reliable traffic data. DENMARK - BLIP Systems, a privately held possible to analyze, improve/change/act and wireless technology company with headquar- evaluate on an ongoing basis. ters near Aalborg, Denmark, has developed a complete solution for tracking road traffic and passengers in airports, called BlipTrack™ and the solution is deployed numerous places around the world. BlipTrack™ sensor on light pole Bluetooth & Wi-Fi technology can be used for traffic measurements, because the technology is becoming more and more BLIP Systems Headquarters in Denmark popular. More and more people use smart phones with both built-in Bluetooth and The vision at BLIP Systems is not only to Wi-FI and at the same time, more and more deploy Bluetooth and Wi-Fi sensors, but also cars have installed hands-free systems. to integrate with other data sources already Compared with other traffic data collection installed like ANPR cameras radars & loops. technologies, BlipTrack™ has some By doing so, data are available from one significant advantages, such as cost per single interface and analysis can be made measurement point due to: across different sensor technologies. -

![Contents [Edit] Africa](https://docslib.b-cdn.net/cover/9562/contents-edit-africa-79562.webp)

Contents [Edit] Africa

Low cost carriers The following is a list of low cost carriers organized by home country. A low-cost carrier or low-cost airline (also known as a no-frills, discount or budget carrier or airline) is an airline that offers generally low fares in exchange for eliminating many traditional passenger services. See the low cost carrier article for more information. Regional airlines, which may compete with low-cost airlines on some routes are listed at the article 'List of regional airlines.' Contents [hide] y 1 Africa y 2 Americas y 3 Asia y 4 Europe y 5 Middle East y 6 Oceania y 7 Defunct low-cost carriers y 8 See also y 9 References [edit] Africa Egypt South Africa y Air Arabia Egypt y Kulula.com y 1Time Kenya y Mango y Velvet Sky y Fly540 Tunisia Nigeria y Karthago Airlines y Aero Contractors Morocco y Jet4you y Air Arabia Maroc [edit] Americas Mexico y Aviacsa y Interjet y VivaAerobus y Volaris Barbados Peru y REDjet (planned) y Peruvian Airlines Brazil United States y Azul Brazilian Airlines y AirTran Airways Domestic y Gol Airlines Routes, Caribbean Routes and y WebJet Linhas Aéreas Mexico Routes (in process of being acquired by Southwest) Canada y Allegiant Air Domestic Routes and International Charter y CanJet (chartered flights y Frontier Airlines Domestic, only) Mexico, and Central America y WestJet Domestic, United Routes [1] States and Caribbean y JetBlue Airways Domestic, Routes Caribbean, and South America Routes Colombia y Southwest Airlines Domestic Routes y Aires y Spirit Airlines Domestic, y EasyFly Caribbean, Central and -

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

Delivering Excellent Service Quality in Low Cost Aviation

MASTER THESIS IMM – International Marketing & Management DELIVERING EXCELLENT SERVICE QUALITY IN LOW COST AVIATION A Process Perspective on the Passenger Market in Copenhagen Airport December 2009 Rasmus Lindstrøm Jensen Advisor: Jesper Clement COPENHAGEN BUSINESS SCHOOL Preface The following thesis is composed on the basis of empirical data collected at Norwegian, Cimber Sterling and six individual airline passengers. I would like to thank Lone Koch (Vice President of Product Management, Cimber Sterling ) and Johan Bisgaard Larsen (Marketing Manager, Norwegian - CPH ) for the kindness and dedication. They contributed with precious information in devising the problem statement and further made the execution of the questionnaire survey possible. Further, I would like to thank Adam Høyer ( Co+Hoegh ), Christoffer Casparij ( Væksthus Sjælland ), Lene Susgaard Henriksen ( Novo Nordisk ), Morten Kaaber ( Muuto New Nordic ), Ditte Clément ( CBS ) and Line Lundø ( CBS ) for contributing with valuable information in the focus group interview. Finally, I would like to thank my advisor Jesper Clement for being a committed and pleasant advisor and sparring partner throughout the entire process. Since the number of pages in thesis exceeds 80 pages a calculation of the magnitude has been made to keep the record straight. The calculation are based on the assumption that one normal page corresponds to 2275 characters and one figure corresponds to 800 characters. Thus the actual number of pages is calculated; (169.675 + (800*16)/2275 = 80,2 pages). Consequently, the thesis keeps within the specified boundaries. Copenhagen, December 2009 Rasmus Lindstrøm Jensen Executive Summary This thesis explores the concept of service quality and customer satisfaction with low cost airlines in Copenhagen Airport. -

Operator Code Operator Name

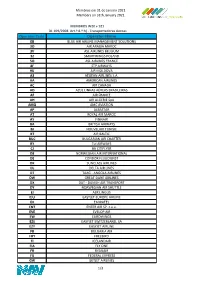

Membros em 31 de Janeiro 2021 Members on 31th January 2021 MEMBROS W20 + S21 DL 109/2008 Art.º 8.º h) - Transportadoras Aereas Operator Code Operator Name 0B BLUE AIR AIRLINE MANAGEMENT SOLUTIONS 3O AIR ARABIA MAROC 3V ASL AIRLINES BELGIUM 3Z SMARTWINGS POLAND 5O ASL AIRLINES FRANCE 8F STP AIRWAYS 9U AIR MOLDOVA A3 AEGEAN AIRLINES S.A. AA AMERICAN AIRLINES AC AIR CANADA AD AZUL LINHAS AÉREAS BRASILEIRAS AF AIR FRANCE AH AIR ALGERIE SpA AMQ AMC AVIATION AP ALBASTAR AT ROYAL AIR MAROC AY FINNAIR BA BRITISH AIRWAYS BJ NOUVELAIR TUNISIE BT AIR BALTIC BUC BULGARIAN AIR CHARTER BY Tui AIRWAYS CJ BA CITIFLYER D8 NORWEGIAN AIR INTERNATIONAL DE CONDOR FLUGDIENST DK SUNCLASS AIRLINES DL DELTA AIR LINES DT TAAG - ANGOLA AIRLINES DW GREAT DANE AIRLINES DX DAT - DANISH AIR TRANSPORT DY NORWEGIAN AIR SHUTTLE EI AER LINGUS EJU EASYJET EUROPE AIRLINE EK EMIRATES ENT ENTER AIR SP. z.o.o. EVE EVELOP AIR EW EUROWINGS EZS EASYJET SWITZERLAND, SA EZY EASYJET AIRLINE FB BULGARIA AIR FHY FREEBIRD FI ICELANDAIR FIA FLY ONE FR RYANAIR FX FEDERAL EXPRESS GW GETJET AIRLINES 1/3 Membros em 31 de Janeiro 2021 Members on 31th January 2021 HV TRANSAVIA AIRLINES I2 IBERIA EXPRESS IB IBERIA JAW JASMIN AIRWAYS JD BEIJING CAPITAL AIRLINES JJ TAM LINHAS AEREAS JNL JET NETHERLANDS BV KL KLM ROYAL DUTCH AIRLINES KM AIR MALTA LG LUXAIR LH LUFTHANSA LO LOT POLISH AIRLINES LS JET2.COM LX SWISS LY EL AL ISRAEL AIRLINES MYX SMARTLYNX AIRLINES ESTONIA NI PGA PORTUGALIA AIRLINES NO NEOS NT BINTER CANARIAS NVR AVION EXPRESS OBS ORBEST OE LAUDAMOTION GMBH OG FLYPLAY OR TUI AIRLINES -

Industry Monitor the EUROCONTROL Bulletin on Air Transport Trends

Issue N°141. 31/05/12 Industry Monitor The EUROCONTROL bulletin on air transport trends European flights declined by 2.7% in April. EUROCONTROL statistics and forecasts 1 May update of the two-year flight forecast is for a Other statistics and forecasts 2 downward revision of 0.4 percentage points to 1.7% fewer flights in 2012 than in 2011. The Passenger airlines 3 outlook for 2013 is for 1.6% growth. Cargo 6 ACI reported overall passenger traffic at Financial results of airlines 7 European airports to be up 3.4% in 1Q12 on Environment 7 1Q11 whereas aircraft movements decreased by 1.7%. Airports 8 Oil 8 European airlines selected in this bulletin recorded €1.7 billion operating losses during Aircraft Manufacturing 9 1Q12, a 17% increase on the same period a year Economy 9 ago. Regulation 9 Oil prices reduced to €79 per barrel on 31 May, Fares 9 dropping 15% from April. EUROCONTROL statistics and forecasts European flights declined by 2.7% in April compared with the same month last year and were similar to April 2009 levels. Strikes in Portugal, but mainly in France resulted in circa 5,000 flight cancellations. With the exception of charter and low-cost, both up 3% and 1.2% respectively on April 2011, other market segments were down circa 4% (see Figure 1) (EUROCONTROL, May). Based on preliminary data for delay from all causes, 36% of flights were delayed on departure in April, resulting in a 3 percentage point increase on April 2011. Analysis of the causes of delay shows a notable increase in reactionary delay. -

Austria 2020 440 Austrian Airlines AG 424300 19210 UIA-VB 3289 30323

Annex I EN Changes to National allocation table for the year 2020 pursuant to the Agreement between the European Union and the Swiss Confederation on the linking of their greenhouse emissions trading systems, and to the Commission Delegated Decision C(2020) 3107 Note: The values for 2020 are total. They include the initial allocation for the flights between EEA Aerodromes and the additional allocation for the flights to and within Switzerland. These values need to be inserted as updates in the National Aviation Allocation Tables XML file. Member State: Austria ETSID Operator name 2020 440 Austrian Airlines AG 424300 19210 UIA-VB 3289 30323 International Jet Management GmbH 157 33061 AVCON JET AG 83 28567 Tupack Verpackungen Gesellschaft m.b.H. 17 25989 The Flying Bulls 16 45083 easyJet Europe Airline GmbH 1823642 Member State: Belgium ETSID Operator name 2020 908 BRUSSELS AIRLINES 285422 27011 ASL Airlines Belgium 110688 2344 SAUDI ARABIAN AIRLINES CORPORATION 3031 32432 EgyptAir 315 29427 Flying Service 271 13457 EXCLU Flying Partners CVBA 81 36269 EXCLU VF International SAGL 22 28582 EXCLU Inter-Wetail c/o Jet Aviation Business Jets AG 14 Member State: Bulgaria ETSID Operator name 2020 29056 Bulgaria Air 81265 28445 BH AIR 41204 Member State: Croatia ETSID Operator name 2020 12495 Croatia Airlines hrvatska zrakoplovna tvrtka d.d. 88551 Member State: Cyprus ETSID Operator name 2020 7132 Joannou & Paraskevaides (Aviation) Limited 30 Member State: Czechia ETSID Operator name 2020 859 České aerolinie a.s. 256608 24903 Smartwings, a.s. 119819 -

2017 Annual Meeting in Sweden

FREQUENTLY ASKED QUESTIONS: 2017 ANNUAL MEETING IN SWEDEN When is the meeting registration deadline? January 9, 2017 What is the easiest way to register and pay? Go to the tour operator’s secure website http://www.askmrnilsson.se/magnolia-society/ and pay with a VISA or MasterCard. With so many registration choices, how do I pick just one? It’s not as complicated as it seems. You only need to make 3 decisions. 1) Which locations do you want to visit? 2) Do you want the tour operator to book your travel or make your own transportation plans within the timeframe of the annual meeting? 3) Do you want to share a hotel room with someone or stay in a room by yourself? Which airport should I use? CPH, Copenhagen Airport in Denmark, is the main international airport serving southern Sweden. You should book round trip from your departure destination to/from CPH. If you participate in any of the itinerary locations beyond Malmo and have the tour operator book your travel, your registration fee will include travel back to Copenhagen. If you are only attending the Uppsala portion of the meeting, you should fly into Stockholm Arlanda Airport, ARN. Transportation between the airport and hotel in Uppsala will be on your own. There are multiple taxi and rental car services available at the airport, as well as bus and train options. What dates and times should I select for my round trip into CPH? ARRIVAL: You should select a flight that will bring you into CPH during the afternoon of May 4. -

'Accentuate the Positive': Getting the Most out of ERASMUS+

AEC Annual Meeting for International Relations Coordinators, 26-28 September 2014, Aalborg th th Aalborg, 26 -28 September 2014 The Royal Academy of Music Aarhus/Aalborg Denmark 'Accentuate the Positive': getting the most out of ERASMUS+ 1 AEC Annual Meeting for International Relations Coordinators, 26-28 September 2014, Aalborg Thanks to our sponsors: www.earmaster.com www.asimut.com The AEC team would like to express special thanks to the Director of the Royal Academy of Music in Aarhus/Aalborg Thomas Winther, and his team, in particular Martin Granum, Charlotte Pilgaard Andersen and Keld Hosbond for their wonderful support in organizing the AEC Annual Meeting for IRCs 2014 in Aalborg 2 AEC Annual Meeting for International Relations Coordinators, 26-28 September 2014, Aalborg Contents Introduction: 'Accentuate the Positive': getting the most out of ERASMUS+ .................................................. 4 Programme ........................................................................................................................................................ 6 Special Features ............................................................................................................................................... 10 Session for First Time Delegates .................................................................................................................. 10 New AEC Website Helpdesk ........................................................................................................................ 10 Bar Camp -

The Use of Aviation Biofuels As an Airport Environmental Sustainability Measure: the Case of Oslo Gardermoen Airport Glenn Baxter1*, Panarat Srisaeng1, Graham Wild2

Czech Technical University in Prague Magazine of Aviation Development Faculty of Transportation Sciences 8(1):6-17, 2020, ISSN: 1805-7578 Department of Air Transport DOI: 10.14311/MAD.2020.01.01 The Use of Aviation Biofuels as an Airport Environmental Sustainability Measure: The Case of Oslo Gardermoen Airport Glenn Baxter1*, Panarat Srisaeng1, Graham Wild2 1School of Tourism and Hospitality Management, Suan Dusit University, Hua Hin Prachaup Khiri Khan, Thailand 2School of Engineering, RMIT University, Box 2476, Melbourne, Victoria, Australia 3000 *Corresponding author: School of Tourism and Hospitality Management, Suan Dusit University, Hua Hin Prachaup Khiri Khan, Thailand. Email g [email protected] Abstract In recent times, there has been a growing trend by airports and airlines to use aviation biofuel as an environment sustainability measure. Using an instrumental qualitative case study research design, this paper examines the evolution of sustainable aviation fuels at Oslo Airport Gardermoen. Oslo Airport Gardermoen was the first airport in the world to offer the first airport in the world to offer aviation biofuels to all airlines in 2016. The qualitative data were examined by document analysis. The study found that the use of sustainable aviation biofuels has delivered tangible environmental benefits to Oslo Gardermoen Airport. The usage of aviation biofuels has enabled the airport, and the airlines using sustainable aviation biofuels, to reduce their greenhouse gases by 10-15%. Also, as part of Norway’s efforts to reduce greenhouse gas emissions, the Norwegian Government have mandated that the aviation fuel industry must mix 0.5% advanced biofuel into jet fuel from 2020 onwards. -

Program Sunday Evening: Welcome Recep- Tion from 7Pm to 9Pm at the Staff Lounge of the Department of Computer Science, Ny Munkegade, Building 540, 2Nd floor

Computational ELECTRONIC REGISTRATION Complexity The registration for CCC’03 is web based. Please register at http://www.brics.dk/Complexity2003/. Registration Fees (In Danish Kroner) Eighteenth Annual IEEE Conference Advance† Late Members‡∗ 1800 DKK 2200 DKK ∗ Sponsored by Nonmembers 2200 DKK 2800 DKK Students+ 500 DKK 600 DKK The IEEE Computer Society ∗The registration fee includes a copy of the proceedings, Technical Committee on receptions Sunday and Monday, the banquet Wednesday, and lunches Monday, Tuesday and Wednesday. Mathematical Foundations +The registration fee includes a copy of the proceedings, of Computing receptions Sunday and Monday, and lunches Monday, Tuesday and Wednesday. The banquet Wednesday is not included. †The advance registration deadline is June 15. ‡ACM, EATCS, IEEE, or SIGACT members. Extra proceedings/banquet tickets Extra proceedings are 350 DKK. Extra banquet tick- ets are 300 DKK. Both can be purchased when reg- istering and will also be available for sale on site. Alternative registration If electronic registration is not possible, please con- tact the organizers at one of the following: E-mail: [email protected] Mail: Complexity 2003 c/o Peter Bro Miltersen In cooperation with Department of Computer Science University of Aarhus ACM-SIGACT and EATCS Ny Munkegade, Building 540 DK 8000 Aarhus C, Denmark Fax: (+45) 8942 3255 July 7–10, 2003 Arhus,˚ Denmark Conference homepage Conference Information Information about this year’s conference is available Location All sessions of the conference and the on the Web at Kolmogorov workshop will be held in Auditorium http://www.brics.dk/Complexity2003/ F of the Department of Mathematical Sciences at Information about the Computational Complexity Aarhus University, Ny Munkegade, building 530, 1st conference is available at floor. -

We Want You Magazine.Pdf

We Want You 2 City of Aalborg - We Want You City of Aalborg - We Want You 3 We Want You Some cities are huge, dynamic metropolises. Some towns are small and quaint. Others, like Aalborg, are exactly like in the story of Goldi- locks and the Three Bears: just right. In Aalborg, it is truly our expe- in population and workforce, as rience that one size fits all. From thousands of new students and our huge shopping centres to our workers join us every year, result- peaceful harbour front, from our ing in a demographic trend that is pulsating night life to the stillness rendering Aalborg younger of our parks, from our buzzing air- and younger. port to our safe, clean and attrac- tive residential areas - Aalborg has This development is influencing a place to suit any mood. many aspects of life in Aalborg and almost every part of the city Why the sales pitch? Because we where building sites are the visible want you to join our workforce. proof; industrial sites are trans- Your talents and skills are needed formed into homes and offices for in our vibrant business com- knowledge based businesses. munity, in our many public and private companies and organisa- Welcome to our rapidly growing tions. Whatever your profession, city. Whether you’re one of the we’re sure that you’re just right many new citizens in Aalborg or for Aalborg. just considering moving here, know that you are very welcome Judging by Aalborg’s demo- and that you have much to look graphic evolution, you would think forward to.