China Animation Characters Company Limited 華夏動漫形象有限公司 (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 01566)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sega Sammy Holdings Integrated Report 2019

SEGA SAMMY HOLDINGS INTEGRATED REPORT 2019 Challenges & Initiatives Since fiscal year ended March 2018 (fiscal year 2018), the SEGA SAMMY Group has been advancing measures in accordance with the Road to 2020 medium-term management strategy. In fiscal year ended March 2019 (fiscal year 2019), the second year of the strategy, the Group recorded results below initial targets for the second consecutive fiscal year. As for fiscal year ending March 2020 (fiscal year 2020), the strategy’s final fiscal year, we do not expect to reach performance targets, which were an operating income margin of at least 15% and ROA of at least 5%. The aim of INTEGRATED REPORT 2019 is to explain to stakeholders the challenges that emerged while pursuing Road to 2020 and the initiatives we are taking in response. Rapidly and unwaveringly, we will implement initiatives to overcome challenges identified in light of feedback from shareholders, investors, and other stakeholders. INTEGRATED REPORT 2019 1 Introduction Cultural Inheritance Innovative DNA The headquarters of SEGA shortly after its foundation This was the birthplace of milestone innovations. Company credo: “Creation is Life” SEGA A Host of World and Industry Firsts Consistently Innovative In 1960, we brought to market the first made-in-Japan jukebox, SEGA 1000. After entering the home video game console market in the 1980s, The product name was based on an abbreviation of the company’s SEGA remained an innovator. Representative examples of this innova- name at the time: Service Games Japan. Moreover, this is the origin of tiveness include the first domestically produced handheld game the company name “SEGA.” terminal with a color liquid crystal display (LCD) and Dreamcast, which In 1966, the periscope game Periscope became a worldwide hit. -

Sega Sammy Holdings Integrated Report 2019

SEGA SAMMY HOLDINGS INTEGRATED REPORT 2019 Challenges & Initiatives Since fiscal year ended March 2018 (fiscal year 2018), the SEGA SAMMY Group has been advancing measures in accordance with the Road to 2020 medium-term management strategy. In fiscal year ended March 2019 (fiscal year 2019), the second year of the strategy, the Group recorded results below initial targets for the second consecutive fiscal year. As for fiscal year ending March 2020 (fiscal year 2020), the strategy’s final fiscal year, we do not expect to reach performance targets, which were an operating income margin of at least 15% and ROA of at least 5%. The aim of INTEGRATED REPORT 2019 is to explain to stakeholders the challenges that emerged while pursuing Road to 2020 and the initiatives we are taking in response. Rapidly and unwaveringly, we will implement initiatives to overcome challenges identified in light of feedback from shareholders, investors, and other stakeholders. INTEGRATED REPORT 2019 1 Introduction Cultural Inheritance Innovative DNA The headquarters of SEGA shortly after its foundation This was the birthplace of milestone innovations. Company credo: “Creation is Life” SEGA A Host of World and Industry Firsts Consistently Innovative In 1960, we brought to market the first made-in-Japan jukebox, SEGA 1000. After entering the home video game console market in the 1980s, The product name was based on an abbreviation of the company’s SEGA remained an innovator. Representative examples of this innova- name at the time: Service Games Japan. Moreover, this is the origin of tiveness include the first domestically produced handheld game the company name “SEGA.” terminal with a color liquid crystal display (LCD) and Dreamcast, which In 1966, the periscope game Periscope became a worldwide hit. -

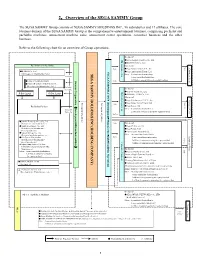

2.Overview of the SEGA SAMMY Group

2.Overview of the SEGA SAMMY Group The SEGA SAMMY Group consists of SEGA SAMMY HOLDINGS INC., 96 subsidiaries and 17 affiliates. The core business domain of the SEGA SAMMY Group is the comprehensive entertainment business, comprising pachislot and pachinko machines, amusement machine sales, amusement center operations, consumer business and the other business. Refer to the following chart for an overview of Group operations. 《In Japan》 AM machine sales machine AM ●SEGA Logistics Service Co., Ltd. ●DARTSLIVE Co., Ltd. Pachislot and Pachinko 《Overseas》 Sale Customers (DevelopmentCORPORATION SEGA Sale ●Sega Amusements U.S.A., Inc. ●RODEO Co., Ltd. ●Sega Amusements Europe Ltd. (Development・Manufacture・Sale ) SEGA SAMMY HOLDINGS INC.(HOLDING COMPANY) Other : 2 consolidated subusidiary Pachislot ・ 1 non-consolidatd subsidiary Users Sammy CorporationSammy 1 affiliated company using the equity method ●GINZA CORPORATION Sale ●GINZAHANBAI CORPORATION ・ ・ (Development Manufacture Sale ) Pachislot 《In Japan》 Pachinko center operationAM ●OASYS PARK Co., Ltd. Sales Agent Sales Agent ●SEGA Bee LINK Co., Ltd. 《Overseas》 ●Sega Entertainment U.S.A., Inc. Customers Service Management guidanceManagement guidanceManagement ●Sega Amusements Taiwan Ltd. ( Sale Pachinko Parlors ●Sega Korea, Ltd. Development ・ Pachislot Other : 6 consolidated subsidiaries Users Pachinko 2 affiliated companies using the equity method Service ・ Manufacture ●Sammy Rental Services Co., Ltd. (Rental lease and maintenance) ・ Sale 《Overseas》 Manufacture ●Shuko Electronics Co., Ltd. ●Sega of America, Inc. (Development・Manufacture・ ●Sega Europe Ltd. Sale of peripherals) ●The Creative Assembly Ltd. ●Sammy Design Co., Ltd. ・ Other : 16 consolidated subsidiaries (Design of pachinko parlors, etc.) Customers Sale ● Sale 2 non-consolidatd subsidiaries H-I System Corporation Service (Development・Manufacture・ ・ ・ 2 affiliated companies using the equity method Sale Consumer businessConsumer Operation) Facilities Sale of peripherals) 4 affiliated companies non-using the equity method △Japan Setup Service Co., Ltd. -

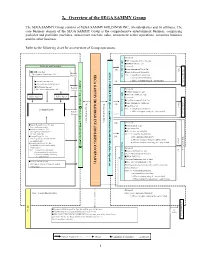

2.Overview of the SEGA SAMMY Group

2.Overview of the SEGA SAMMY Group The SEGA SAMMY Group consists of SEGA SAMMY HOLDINGS INC., 86 subsidiaries and 16 affiliates. The core business domain of the SEGA SAMMY Group is the comprehensive entertainment business, comprising pachislot and pachinko machines, amusement machine sales, amusement center operations, consumer business and the other business. Refer to the following chart for an overview of Group operations. 《In Japan》 AM machine sales ●SEGA Logistics Service Co., Ltd. ● DARTSLIVE Co., Ltd. Pachislot and Pachinko 《Overseas》 Sale Customers SEGA CORPORATION (Development CORPORATION SEGA Sale ●Sega Amusements U.S.A., Inc. ●RODEO Co., Ltd. ●Sega Amusements Europe Ltd. (Development・Manufacture・Sale ) SEGA SAMMY HOLDINGS INC.(HOLDINGCOMPANY) Pachislot Other : 2 consolidated subusidiary ・ 1 non-consolidatd subsidiary Users Sammy Corporation 1 affiliated company using the equity method ●GINZA CORPORATION Sale ●GINZAHANBAI CORPORATION ●TAIYO ELEC Co.,Ltd. Pachislot (Development・Manufacture・Sale ) 《In Japan》 Pachinko operation AM center ●OASYS PARK Co., Ltd. ●SEGA Bee LINK Co., Ltd. Sales Agent Sales Agent 《Overseas》 ●Sega Entertainment U.S.A., Inc. Customers Service Management guidance Management guidance ●Sega Amusements Taiwan Ltd. ( Sale ●Sega Korea Ltd. Development ・ Pachinko Parlors Other : 5 consolidated subsidiaries Users Pachislot 2 affiliated companies using the equity method Pachinko Service ・ Manufacture ・ Sale 《Overseas》 Manufacture ●Sammy Rental Services Co., Ltd. ●Sega of America, Inc. (Lease and maintenance) ●Sega Europe Ltd. ●Sammy Systems Co., Ltd. (Development・Manufacture・ ●The Creative Assembly Ltd. Sale of peripherals) ・ Other : 18 consolidated subsidiaries Customers Sale ●Sammy Design Co., Ltd. Sale 2 non-consolidatd subsidiaries (Planning, design, construction of) Service ・ ・ 2 affiliated companies using the equity method pachinko parlors.) Sale Consumer business Facilities Operation) △Japan Setup Service Co., Ltd. -

Chapter 1. the Dependence of Profitability on Industry Structure

01-4702-Conklin.qxd 5/10/2005 5:48 PM Page 1 1 THE DEPENDENCE OF PROFITABILITY ON INDUSTRY STRUCTURE he cases in this chapter illustrate the ways that microeconomic forces and industry structure influence management decisions. Determining the prices to be charged T and quantities to be produced requires that management understand customer, supplier, and competitor strategies, and these market realities vary among countries. Conceptual frameworks used in analyzing industry structure include Michael Porter’s (1979) “five forces model,” through which each industry can be analyzed from the perspective of the rivalry among existing competitors, the threat of new entrants, the bar- gaining power of buyers, the threat of substitutes, and the bargaining power of suppliers. A sixth force, the impacts of complementors, can be added to this model. Elements of microeconomic theory and game theory are analytical tools that help in the examination of how a change in price will affect sales volumes and hence revenue, costs, and profits. Industry structures may differ significantly from one country to another, and these differences may provide a rationale for international investment. In particular, interna- tional investment can enable a firm to increase its profitability by shifting from a market where it has no significant competitive advantage to a market where its activities are unique. Strong competitors can limit expansion opportunities in a firm’s home country, whereas the firm may benefit from a monopoly position if it invests in a foreign market. Differences in industry structures among countries can result from any of the environ- mental forces: for example, levels of economic development, types of political regulations, preferences of consumers, or stages of technologies. -

How Theme Park Rides Adapted the Shooting Gallery

How Theme Park Rides Adapted the Shooting Gallery Bobby Schweizer Texas Tech University Lubbock, Texas United States [email protected] Keywords Shooting galleries, theme parks, midways, arcades, media archeology EXTENDED ABSTRACT In 1998, Walt Disney Imagineering unveiled a new ride for Tomorrowland in the Magic Kingdom park in Orlando, Florida—one that introduced a new form of interactivity previously unseen in their parks. Buzz Lightyear Space Ranger Spin was a hybrid attraction: part dark ride, part shooting gallery. Riders boarded Omnimover vehicles armed with two blaster guns mounted to the dashboard that could be aimed with a limited range of motion to defeat the Emperor Zurg. An LCD screen tallied the score as passengers spun their vehicles to position themselves to shoot at “Z” marked targets throughout the blacklight neon ride. With the creation of this attraction and, most recently the opening of the Star Wars Millennium Falcon: Smuggler’s Run, the dark ride has seemingly adopted the values of videogame interactivity. Yet, while a comparison to videogames seems obvious, this transition did not happen overnight and was, in fact, part of a long tradition of target shooting forms of play. The shooting gallery has always been a perennial entertainment form seen in fairs, carnivals, and amusement parks across the globe (Adams 1991). Emerging out of military and marksmanship traditions, these games emulate the practice of real target shooting in which a marksman stands at one end of a booth or range while shooting pellets at stationary or moving targets (Tucker and Tucker 2014). Played for prizes or bragging right, the simple act of aiming and pulling a trigger has undergone technological adaptations to automate the process, place it into new venues, and create new feedback loops that construct new player experiences intended for social interaction. -

The Effect of School Closure On

Public Gaming: eSport and Event Marketing in the Experience Economy by Michael Borowy B.A., University of British Columbia, 2008 Thesis Submitted in Partial Fulfillment of the Requirements for the Degree of Master of Arts in the School of Communication Faculty of Communication, Art, and Technology Michael Borowy 2012 SIMON FRASER UNIVERSITY Summer 2012 All rights reserved. However, in accordance with the Copyright Act of Canada, this work may be reproduced, without authorization, under the conditions for “Fair Dealing.” Therefore, limited reproduction of this work for the purposes of private study, research, criticism, review and news reporting is likely to be in accordance with the law, particularly if cited appropriately. Approval Name: Michael Borowy Degree: Master of Arts (Communication) Title of Thesis: Public Gaming: eSport and Event Marketing in the Experience Economy Examining Committee: Chair: David Murphy, Senior Lecturer Dr. Stephen Kline Senior Supervisor Professor Dr. Dal Yong Jin Supervisor Associate Professor Dr. Richard Smith Internal Examiner Professor Date Defended/Approved: July 06, 2012 ii Partial Copyright Licence iii STATEMENT OF ETHICS APPROVAL The author, whose name appears on the title page of this work, has obtained, for the research described in this work, either: (a) Human research ethics approval from the Simon Fraser University Office of Research Ethics, or (b) Advance approval of the animal care protocol from the University Animal Care Committee of Simon Fraser University; or has conducted the research (c) as a co-investigator, collaborator or research assistant in a research project approved in advance, or (d) as a member of a course approved in advance for minimal risk human research, by the Office of Research Ethics. -

Sega Sammy Group Csr Report 2 0

SEGA SAMMY GROUP CSR REPORT 2016 REPORT CSR GROUP SAMMY SEGA ©SEGA ©Sammy ©TMS ©DARTSLIVE Co., Ltd. Group Overview The SEGA SAMMY Group has been providing creative entertainment to customers of all ages in Japan and over- seas as a versatile entertainment company group engaged in a wide range of business areas. Pachislot and Pachinko Machines Business Machines Pachinko and Pachislot Major Business Line Net sales*1 Development, production and sales of pachislot 133.4 billion yen and pachinko machines Major Group Companies Ratio of consolidated Sammy Corporation, GINZA Corporation, net sales TAIYO ELEC Co., Ltd., Japan Multimedia Services Corporation, RODEO Co., Ltd. (and 14 other % 38.2 companies) Entertainment ContentsBusiness Major Business Line Development and sales of packaged games and amusement machines, with digital games at the core; development and operation of amusement centers; Fiscal 2016 Results 2016 Fiscal *1 planning, production and sales of animation films; Net sales and development, production and sales of toys 199.7billion yen Major Group Companies SEGA Holdings Co., Ltd., ATLUS CO., LTD., *2 Ratio of consolidated Sammy Networks Co., Ltd. , net sales SEGA Interactive Co., Ltd., SEGA ENTERTAINMENT CO., Ltd, % SEGA Games Co., Ltd., SEGA TOYS CO., LTD., 57.1 SEGA LOGISTICS SERVICE CO., LTD, SEGA SAMMY CREATION INC., DARTSLIVE Co., Ltd., TMS ENTERTAINMENT Co., Ltd., MARZA ANIMATION PLANET INC. (and 20 other companies in Japan and 44 overseas) Resort Business Resort Major Business Line Net sales*1 Integrated resorts and development and operation 16.4billion yen of other resort facilities, hotels and theme parks Major Group Companies Ratio of consolidated ON-U INC., SEGA SAMMY GOLF ENTERTAINMENT net sales INC., SEGA LIVE CREATION Inc., PHOENIX RESORT CO., LTD. -

Play It Again SEGA CORPORATION Annual Report 2004

SEGA CORPORATION Annual Report 2004 play it again www.sega.co.jp SEGA CORPORATION 2-12 Haneda 1-chome, Ohta-ku, Tokyo 144-8531, Japan Tel: +81-3-5736-7111 Printed in Japan © SEGA the © SEGA excitem Contents Consolidated Financial Highlights 2 A Message from the Management 3 New Holding Company 6 Review of Operations 10 Results of Financial Reform 14 Financial Section 16 Board of Directors and Auditors 44 Corporate Data 45 Principal Overseas Subsidiaries 45 Cautionary Statements This annual report contains forecasts of business results, statements regarding business plans and other forward-looking statements. These statements are based on management’s assumptions regarding the economic environment and the Company’s operating environment as of the date of publication and involve various risks and uncertainties. Actual business results may differ materially from forecasts herein. © SEGA, 2003, 2004 ent company, SEGA CORPORATION was established in 1951 and incorporated in 1960. Three pillars support SEGA’s all- round entertainment business – Amusement Machine Sales, Amusement Center Operations, and Consumer Business – which operates in markets the world over. Our core competence lies in our ability to develop a diverse range of products in those three business segments. Consequently, SEGA has debuted an array of first-ever products. By offering a steady flow of such leading-edge goods, the Company has consistently led markets. Thanks to those extensive software assets, SEGA has become one of only a handful of blue-chip game manufacturers recognized by game players worldwide. This annual report contains forecasts of business results, statements regarding business plans and other forward-looking statements. -

January 29, 2021 (Translation) Dear Sirs Or Madams, Name of Company

January 29, 2021 (Translation) Dear Sirs or Madams, Name of Company: SEGA SAMMY HOLDINGS INC. Name of Representative: Haruki Satomi, President and Group COO (Representative Director) (Code No. 6460, Tokyo Stock Exchange 1st Section) Further Inquiry: Yoichi Owaki, Senior Vice President, Executive Officer Managing Director of Finance & Accounting Division (TEL: 03-6864-2400) Notice of Changes of Representative Directors’ Title and Change of Directors and Executive Officers SEGA SAMMY HOLDINGS INC. (the “Company”) hereby notifies that it resolved at its Board of Directors meeting, held on today to implement changes to the title of representative directors of the Company and changes in Directors and Executive Officers of the Company and the Company’s major subsidiaries, SEGA CORPORATION and Sammy Corporation as described below: Description SEGA SAMMY HOLDINGS INC. 1.Changes in Representative Directors’ Title New Title Name Former Title Chairman, Chairman and Group CEO, Hajime Satomi Representative Director Representative Director President and Group CEO, President and Group COO, Haruki Satomi Representative Director Representative Director 2. Management System of the Company as of April 1, 2021 Name Title Hajime Satomi Chairman, Representative Director Haruki Satomi President and Group CEO, Representative Director Naoya Tsurumi Senior Executive Vice President, Director of the Board Koichi Fukazawa Senior Executive Vice President and Group CFO, Director of the Board Hideo Yoshizawa Senior Vice President, Director of the Board Takeshi Natsuno -

Company Vendor ID (Decimal Format) (AVL) Ditest Fahrzeugdiagnose Gmbh 4621 @Pos.Com 3765 0XF8 Limited 10737 1MORE INC

Vendor ID Company (Decimal Format) (AVL) DiTEST Fahrzeugdiagnose GmbH 4621 @pos.com 3765 0XF8 Limited 10737 1MORE INC. 12048 360fly, Inc. 11161 3C TEK CORP. 9397 3D Imaging & Simulations Corp. (3DISC) 11190 3D Systems Corporation 10632 3DRUDDER 11770 3eYamaichi Electronics Co., Ltd. 8709 3M Cogent, Inc. 7717 3M Scott 8463 3T B.V. 11721 4iiii Innovations Inc. 10009 4Links Limited 10728 4MOD Technology 10244 64seconds, Inc. 12215 77 Elektronika Kft. 11175 89 North, Inc. 12070 Shenzhen 8Bitdo Tech Co., Ltd. 11720 90meter Solutions, Inc. 12086 A‐FOUR TECH CO., LTD. 2522 A‐One Co., Ltd. 10116 A‐Tec Subsystem, Inc. 2164 A‐VEKT K.K. 11459 A. Eberle GmbH & Co. KG 6910 a.tron3d GmbH 9965 A&T Corporation 11849 Aaronia AG 12146 abatec group AG 10371 ABB India Limited 11250 ABILITY ENTERPRISE CO., LTD. 5145 Abionic SA 12412 AbleNet Inc. 8262 Ableton AG 10626 ABOV Semiconductor Co., Ltd. 6697 Absolute USA 10972 AcBel Polytech Inc. 12335 Access Network Technology Limited 10568 ACCUCOMM, INC. 10219 Accumetrics Associates, Inc. 10392 Accusys, Inc. 5055 Ace Karaoke Corp. 8799 ACELLA 8758 Acer, Inc. 1282 Aces Electronics Co., Ltd. 7347 Aclima Inc. 10273 ACON, Advanced‐Connectek, Inc. 1314 Acoustic Arc Technology Holding Limited 12353 ACR Braendli & Voegeli AG 11152 Acromag Inc. 9855 Acroname Inc. 9471 Action Industries (M) SDN BHD 11715 Action Star Technology Co., Ltd. 2101 Actions Microelectronics Co., Ltd. 7649 Actions Semiconductor Co., Ltd. 4310 Active Mind Technology 10505 Qorvo, Inc 11744 Activision 5168 Acute Technology Inc. 10876 Adam Tech 5437 Adapt‐IP Company 10990 Adaptertek Technology Co., Ltd. 11329 ADATA Technology Co., Ltd. -

Notice of the 14Th Ordinary General Meeting of Shareholders to Be Held on June 22, 2018

[English Translation of Convocation Notice Originally Issued in the Japanese Language] 【Note】This document has been translated from the Japanese original for reference purposes only. In the event of any discrepancy between this translated document and the Japanese original, the original shall prevail. The Company assumes no responsibility for this translation or for direct, indirect or any other forms of damages arising from the translation. Securities Code: 6460 May 31, 2018 Haruki Satomi President (Representative Director) SEGA SAMMY HOLDINGS INC. Shiodome Sumitomo Building, 1-9-2 Higashi Shimbashi, Minato-ku, Tokyo, Japan Dear Shareholders: Notice of the 14th Ordinary General Meeting of Shareholders to be held on June 22, 2018 You are cordially invited to attend the 14th Ordinary General Meeting of Shareholders of SEGA SAMMY HOLDINGS INC. (the “Company”) to be held at Ho-Oh-No-Ma (Main Hall), 2F, Tokyo Prince Hotel, 3-3-1 Shiba-koen, Minato-ku, Tokyo, 105-8560, Japan on Friday, June 22, 2018 at 10:00 a.m. for the purposes listed below. If you are unable to attend the meeting in person, you may exercise your voting rights by either mail (in writing) or via the Internet. Therefore, please review the attached Reference Documents for General Meeting of Shareholders, and kindly exercise your voting rights before 6:00 p.m., Japan Standard Time, on Thursday, June 21, 2018. Details of the Meeting 1. Date and time: Friday, June 22, 2018 at 10:00 a.m. (Reception commences at 9:00 a.m.) 2. Venue: Ho-Oh-No-Ma (Main Hall), 2F, Tokyo Prince Hotel 3-3-1 Shiba-koen, Minato-ku, Tokyo, 105-8560, Japan 3.