A to Z (428KB)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ANNUAL REPORT 2000 SEGA CORPORATION Year Ended March 31, 2000 CONSOLIDATED FINANCIAL HIGHLIGHTS SEGA Enterprises, Ltd

ANNUAL REPORT 2000 SEGA CORPORATION Year ended March 31, 2000 CONSOLIDATED FINANCIAL HIGHLIGHTS SEGA Enterprises, Ltd. and Consolidated Subsidiaries Years ended March 31, 1998, 1999 and 2000 Thousands of Millions of yen U.S. dollars 1998 1999 2000 2000 For the year: Net sales: Consumer products ........................................................................................................ ¥114,457 ¥084,694 ¥186,189 $1,754,018 Amusement center operations ...................................................................................... 94,521 93,128 79,212 746,227 Amusement machine sales............................................................................................ 122,627 88,372 73,654 693,867 Total ........................................................................................................................... ¥331,605 ¥266,194 ¥339,055 $3,194,112 Cost of sales ...................................................................................................................... ¥270,710 ¥201,819 ¥290,492 $2,736,618 Gross profit ........................................................................................................................ 60,895 64,375 48,563 457,494 Selling, general and administrative expenses .................................................................. 74,862 62,287 88,917 837,654 Operating (loss) income ..................................................................................................... (13,967) 2,088 (40,354) (380,160) Net loss............................................................................................................................. -

Sega Sammy Holdings Inc

2014 summer Contents SEGA SAMMY P 1 Key Points of Financial Results by the Numbers REPORT SEGA SAMMY in 2013 A Message from P 3 Management Segment P 5 Information Looking back with a “Key Person” P9 Review of Activities Launch of pachinko and pachislot game for Bakemonogatari Making of ATLUS.CO.,LTD into a subsidiary P12 Latest News P13 Group Information Business Report for the fiscal Summer year ended March 31, 2014 Edition From April 1, 2013 to March 31, 2014 SEGA SAMMY HOLDINGS INC. Stock Code 6460 010_0324402982606.indd 2 2014/06/13 21:17:31 Key Points of Financial Results by the Numbers FY2014 (Fiscal year ended March 31, 2014) SEGA SAMMY in 2013 Net sales Unit of pachislot machines sold Due to strong sales of mainstay titles in the Pachislot and Pachinko Machine Business and strong performance in the digital areas in the Fiscal year ended billion Consumer Business, both sales and operating income increased March 31, 2013 units year on year significantly. However, due to effects of a delay in the 202,221 ¥378.0 sales schedule for some pachislot titles and the weak perfor- (up 18% year on year) mance of the Amusement Machine Sales Business, net sales and operating income fell short of initial forecasts. The Fiscal year ended Operating income Company recorded extraordinary income of approxi- March 31, 2014 mately ¥15.7 billion due to factors including a gain on 301,575 units sales of investment securities, while an extraordi- nary loss of approximately ¥8.7 billion resulting While the initial forecast was not achieved due to the revision of the sales from factors including a loss on liquidation of schedule for multiple titles including Pachislot SOUTEN-NO-KEN 2, subsidiaries and affiliates from the comple- particularly for the mainstay titles of the Sammy brand such as tion of the liquidation of some of the Pachislot Hokuto No Ken Chapter of Resurrection, Pachislot billion subsidiaries in the U.S. -

UPC Platform Publisher Title Price Available 730865001347

UPC Platform Publisher Title Price Available 730865001347 PlayStation 3 Atlus 3D Dot Game Heroes PS3 $16.00 52 722674110402 PlayStation 3 Namco Bandai Ace Combat: Assault Horizon PS3 $21.00 2 Other 853490002678 PlayStation 3 Air Conflicts: Secret Wars PS3 $14.00 37 Publishers 014633098587 PlayStation 3 Electronic Arts Alice: Madness Returns PS3 $16.50 60 Aliens Colonial Marines 010086690682 PlayStation 3 Sega $47.50 100+ (Portuguese) PS3 Aliens Colonial Marines (Spanish) 010086690675 PlayStation 3 Sega $47.50 100+ PS3 Aliens Colonial Marines Collector's 010086690637 PlayStation 3 Sega $76.00 9 Edition PS3 010086690170 PlayStation 3 Sega Aliens Colonial Marines PS3 $50.00 92 010086690194 PlayStation 3 Sega Alpha Protocol PS3 $14.00 14 047875843479 PlayStation 3 Activision Amazing Spider-Man PS3 $39.00 100+ 010086690545 PlayStation 3 Sega Anarchy Reigns PS3 $24.00 100+ 722674110525 PlayStation 3 Namco Bandai Armored Core V PS3 $23.00 100+ 014633157147 PlayStation 3 Electronic Arts Army of Two: The 40th Day PS3 $16.00 61 008888345343 PlayStation 3 Ubisoft Assassin's Creed II PS3 $15.00 100+ Assassin's Creed III Limited Edition 008888397717 PlayStation 3 Ubisoft $116.00 4 PS3 008888347231 PlayStation 3 Ubisoft Assassin's Creed III PS3 $47.50 100+ 008888343394 PlayStation 3 Ubisoft Assassin's Creed PS3 $14.00 100+ 008888346258 PlayStation 3 Ubisoft Assassin's Creed: Brotherhood PS3 $16.00 100+ 008888356844 PlayStation 3 Ubisoft Assassin's Creed: Revelations PS3 $22.50 100+ 013388340446 PlayStation 3 Capcom Asura's Wrath PS3 $16.00 55 008888345435 -

Video Game Archive: Nintendo 64

Video Game Archive: Nintendo 64 An Interactive Qualifying Project submitted to the Faculty of WORCESTER POLYTECHNIC INSTITUTE in partial fulfilment of the requirements for the degree of Bachelor of Science by James R. McAleese Janelle Knight Edward Matava Matthew Hurlbut-Coke Date: 22nd March 2021 Report Submitted to: Professor Dean O’Donnell Worcester Polytechnic Institute This report represents work of one or more WPI undergraduate students submitted to the faculty as evidence of a degree requirement. WPI routinely publishes these reports on its web site without editorial or peer review. Abstract This project was an attempt to expand and document the Gordon Library’s Video Game Archive more specifically, the Nintendo 64 (N64) collection. We made the N64 and related accessories and games more accessible to the WPI community and created an exhibition on The History of 3D Games and Twitch Plays Paper Mario, featuring the N64. 2 Table of Contents Abstract…………………………………………………………………………………………………… 2 Table of Contents…………………………………………………………………………………………. 3 Table of Figures……………………………………………………………………………………………5 Acknowledgements……………………………………………………………………………………….. 7 Executive Summary………………………………………………………………………………………. 8 1-Introduction…………………………………………………………………………………………….. 9 2-Background………………………………………………………………………………………… . 11 2.1 - A Brief of History of Nintendo Co., Ltd. Prior to the Release of the N64 in 1996:……………. 11 2.2 - The Console and its Competitors:………………………………………………………………. 16 Development of the Console……………………………………………………………………...16 -

Sega Sammy Holdings Integrated Report 2019

SEGA SAMMY HOLDINGS INTEGRATED REPORT 2019 Challenges & Initiatives Since fiscal year ended March 2018 (fiscal year 2018), the SEGA SAMMY Group has been advancing measures in accordance with the Road to 2020 medium-term management strategy. In fiscal year ended March 2019 (fiscal year 2019), the second year of the strategy, the Group recorded results below initial targets for the second consecutive fiscal year. As for fiscal year ending March 2020 (fiscal year 2020), the strategy’s final fiscal year, we do not expect to reach performance targets, which were an operating income margin of at least 15% and ROA of at least 5%. The aim of INTEGRATED REPORT 2019 is to explain to stakeholders the challenges that emerged while pursuing Road to 2020 and the initiatives we are taking in response. Rapidly and unwaveringly, we will implement initiatives to overcome challenges identified in light of feedback from shareholders, investors, and other stakeholders. INTEGRATED REPORT 2019 1 Introduction Cultural Inheritance Innovative DNA The headquarters of SEGA shortly after its foundation This was the birthplace of milestone innovations. Company credo: “Creation is Life” SEGA A Host of World and Industry Firsts Consistently Innovative In 1960, we brought to market the first made-in-Japan jukebox, SEGA 1000. After entering the home video game console market in the 1980s, The product name was based on an abbreviation of the company’s SEGA remained an innovator. Representative examples of this innova- name at the time: Service Games Japan. Moreover, this is the origin of tiveness include the first domestically produced handheld game the company name “SEGA.” terminal with a color liquid crystal display (LCD) and Dreamcast, which In 1966, the periscope game Periscope became a worldwide hit. -

Lllllllllllllllllllllllllllillllllllllllllilllllllllllllllll

lllllllllllllllllllllllllllIllllllllllllllIllllllllllllllllllllIlllllllllll USOO5221083A United States Patent [19] [11] Patent Number: 5,221,083 Dote [45] Date of Patent: Jun. 22, 1993 [54] MEDAL GAME MACHINE OTHER PUBLICATIONS [75] Inventor: Singo Dote, Tokyo, Japan Stephen D. Bristow, The History of Video Games, [73] Assignee: Sega Enterprises, Ltd., Tokyo, Japan IEEE Tranactions on Consumer Electronics, Feb. [21] Appl. No.: 593,696 1977, pp. 58-68. Ed Edelson, Popular Science, 3-D optical blender, [22] Filed: Oct. 5, 1990 Nov. 1983, pp. 98-99. [30] Foreign Application Priority Data Primary Examiner-V. Millin Oct. 17, 1989 [JP] Japan ................................ .. l-27l025 Assistant Examiner—-Steven B. Wong Attorney, Agent, or Firm-Price, Gess & Ubell [51] 1111. (:1.5 .............................................. .. A63F 1/00 [52] us. 01. ........................... .. 273/85 CP; 273/85 G; [57] ABSTRACT ' ‘ 273/D1G. 28; 353/37 A medal game machine adapted to use a multiplicity of [58] Field of Search ...... .. 273/85 CP, 85 o, DIG. 28, medals and to apportion them to the player who bet 273/161, 138 A, 313, 316, 355, 358; 353/28, 30, 37, 74, 77, 94; 248/917-924 medals and won in a game. The machine comprises an enclosure having an open central portion on its front [56] References Cited side, a display unit mounted in the center of the head U.S. PATENT DOCUMENTS portion of the enclosure, a ?at half mirror located below the display unit, a georama forming a back 3,790,172 2/1974 Nakamura ......................... 1. 273/313 4,189,l45 2/1980 Stubben et a1. .. 272/DIG 28 ground, illuminators equipped with dimmers for illumi 4,265,449 5/1981 Reineretal. -

MEDIA CONTACT: Aram Jabbari Atlus U.S.A., Inc

MEDIA CONTACT: Aram Jabbari Atlus U.S.A., Inc. FOR IMMEDIATE 949-788-0455 (x102) RELEASE [email protected] ATLUS U.S.A., INC. ANNOUNCES SHIN MEGAMI TENSEI®: PERSONA 3™ WEBSITE LAUNCH! Locked away in the human psyche is power beyond imagination... IRVINE, CALIFORNIA — JULY 10th, 2007 — Atlus U.S.A., Inc., a leading publisher of interactive entertainment, today announced the launch of the official website for Shin Megami Tensei: Persona 3! Enormously successful in Japan, P3 is the newest RPG from the publisher of the acclaimed Shin Megami Tensei series. After eight long years of anticipation, fans have very little left to wait. Shin Megami Tensei: Persona 3 is set to ship on July 24, 2007, exclusively for the PlayStation®2 computer entertainment system. Every copy is a deluxe edition with a 52-page color art book and soundtrack CD! Shin Megami Tensei: Persona 3 has been rated “M” for Mature by the ESRB for Blood, Language, Partial Nudity, and Violence. About Shin Megami Tensei: Persona 3: In Persona 3, you’ll assume the role of a high school student, orphaned as a young boy, who’s recently transferred to Gekkoukan High School on Port Island. Shortly after his arrival, he is attacked by creatures of the night known as Shadows. The assault awakens his Persona, Orpheus, from the depths of his subconscious, enabling him to defeat the terrifying foes. He soon discovers that he shares this special ability with other students at his new school. From them, he learns of the Dark Hour, a hidden time that exists between one day and the next, swarming with Shadows. -

Sega Sammy Holdings Integrated Report 2019

SEGA SAMMY HOLDINGS INTEGRATED REPORT 2019 Challenges & Initiatives Since fiscal year ended March 2018 (fiscal year 2018), the SEGA SAMMY Group has been advancing measures in accordance with the Road to 2020 medium-term management strategy. In fiscal year ended March 2019 (fiscal year 2019), the second year of the strategy, the Group recorded results below initial targets for the second consecutive fiscal year. As for fiscal year ending March 2020 (fiscal year 2020), the strategy’s final fiscal year, we do not expect to reach performance targets, which were an operating income margin of at least 15% and ROA of at least 5%. The aim of INTEGRATED REPORT 2019 is to explain to stakeholders the challenges that emerged while pursuing Road to 2020 and the initiatives we are taking in response. Rapidly and unwaveringly, we will implement initiatives to overcome challenges identified in light of feedback from shareholders, investors, and other stakeholders. INTEGRATED REPORT 2019 1 Introduction Cultural Inheritance Innovative DNA The headquarters of SEGA shortly after its foundation This was the birthplace of milestone innovations. Company credo: “Creation is Life” SEGA A Host of World and Industry Firsts Consistently Innovative In 1960, we brought to market the first made-in-Japan jukebox, SEGA 1000. After entering the home video game console market in the 1980s, The product name was based on an abbreviation of the company’s SEGA remained an innovator. Representative examples of this innova- name at the time: Service Games Japan. Moreover, this is the origin of tiveness include the first domestically produced handheld game the company name “SEGA.” terminal with a color liquid crystal display (LCD) and Dreamcast, which In 1966, the periscope game Periscope became a worldwide hit. -

Domain Analysis for a Video Game Metadata Schema: Issues and Challenges

Domain Analysis for a Video Game Metadata Schema: Issues and Challenges Jin Ha Lee*, Joseph T. Tennis, Rachel Ivy Clarke Information School, University of Washington Mary Gates Hall, Ste 370, Seattle, WA 98195 {jinhalee, jtennis, raclarke}@uw.edu Abstract. As interest in video games increases, so does the need for intelligent access to them. However, traditional organization systems and standards fall short. Through domain analysis and cataloging real-world examples while attempting to develop a formal metadata schema for video games, we encountered challenges in description. Inconsistent, vague, and subjective sources of information for genre, release date, feature, region, language, developer and publisher information confirm the imporatnce of developing a standardized description model for video games. 1 Introduction Recent years demonstrate an immense surge of interest in video games. 72% of American households play video games, and industry analysts expect the global gam- ing market to reach $91 billion by 2015 (GIA, 2009). Video games are also increas- ingly of interest in scholarly and educational communities. Studies across various scholarly disciplines aim to examine the roles of games in society and interactions around games and players (Winget, 2011). Games are also of interest to the education community for use as learning tools and technologies (Gee, 2003). Thus we can assert that video games are entrenched in our economic, cultural, and academic systems. As games become embedded in our culture, providing intelligent access to them becomes increasingly important. Effectiveness of information access is a direct result of the design efforts put into the organization of that information (Svenonius, 2000). Consumers, manufacturers, scholars and educators all need meaningful ways of or- ganizing video game collections for access. -

19/20 Interim Report 2 Reg No

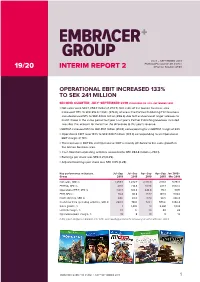

JULY – SEPTEMBER 2019 EMBRACER GROUP AB (PUBL) 19/20 INTERIM REPORT 2 REG NO. 556582-6558 OPERATIONAL EBIT INCREASED 133% TO SEK 241 MILLION SECOND QUARTER, JULY–SEPTEMBER 2019 (COMPARED TO JULY–SEPTEMBER 2018) > Net sales were SEK 1,259.7 million (1,272.7). Net sales of the Games business area increased 117% to SEK 816.0 million (376.0), whereas the Partner Publishing/Film business area decreased 51% to SEK 443.6 million (896.6) due to the absence of larger releases to match those in the same period last year. Last year’s Partner Publishing revenues included two titles that account for more than the difference to this year’s revenue. > EBITDA increased 95% to SEK 418.1 million (214.8), corresponding to an EBITDA margin of 33%. > Operational EBIT rose 133% to SEK 240.7 million (103.4) corresponding to an Operational EBIT margin of 19%. > The increase in EBITDA and Operational EBIT is mainly attributed to the sales growth in the Games business area. > Cash flow from operating activities amounted to SEK 284.8 million (–740.1). > Earnings per share was SEK 0.21 (0.25). > Adjusted earnings per share was SEK 0.65 (0.28). Key performance indicators, Jul–Sep Jul–Sep Apr–Sep Apr–Sep Jan 2018– Group 2019 2018 2019 2018 Mar 2019 Net sales, SEK m 1,259.7 1,272.7 2,401.8 2,110.1 5,754.1 EBITDA, SEK m 418.1 214.8 807.6 421.7 1,592.6 Operational EBIT, SEK m 240.7 103.4 444.8 173.1 897.1 EBIT, SEK m 76.4 90.8 157.7 143.3 574.6 Profit after tax, SEK m 64.6 65.0 117.4 98.5 396.8 Cash flow from operating activities, SEK m 284.8 –740.1 723.1 –575.6 1,356.4 Sales growth, % –1 1,403 14 2,281 1,034 EBITDA margin, % 33 17 34 20 28 Operational EBIT margin, % 19 8 19 8 16 In this report, all figures in brackets refer to the corresponding period of the previous year, unless otherwise stated. -

Chapter 1. the Dependence of Profitability on Industry Structure

01-4702-Conklin.qxd 5/10/2005 5:48 PM Page 1 1 THE DEPENDENCE OF PROFITABILITY ON INDUSTRY STRUCTURE he cases in this chapter illustrate the ways that microeconomic forces and industry structure influence management decisions. Determining the prices to be charged T and quantities to be produced requires that management understand customer, supplier, and competitor strategies, and these market realities vary among countries. Conceptual frameworks used in analyzing industry structure include Michael Porter’s (1979) “five forces model,” through which each industry can be analyzed from the perspective of the rivalry among existing competitors, the threat of new entrants, the bar- gaining power of buyers, the threat of substitutes, and the bargaining power of suppliers. A sixth force, the impacts of complementors, can be added to this model. Elements of microeconomic theory and game theory are analytical tools that help in the examination of how a change in price will affect sales volumes and hence revenue, costs, and profits. Industry structures may differ significantly from one country to another, and these differences may provide a rationale for international investment. In particular, interna- tional investment can enable a firm to increase its profitability by shifting from a market where it has no significant competitive advantage to a market where its activities are unique. Strong competitors can limit expansion opportunities in a firm’s home country, whereas the firm may benefit from a monopoly position if it invests in a foreign market. Differences in industry structures among countries can result from any of the environ- mental forces: for example, levels of economic development, types of political regulations, preferences of consumers, or stages of technologies. -

Card, Board, Or Roulette Games; Indoor Games Using

A63F CARD, BOARD, OR ROULETTE GAMES; INDOOR GAMES USING SMALL MOVING PLAYING BODIES; MISCELLANEOUS GAMES (data-processing equipment characterised by a specific application for game playing G06F 17/00, G06F 19/00; [N: coin-freed apparatus for games G07F 17/32 ]) Definition statement This subclass/group covers: • Games including card games, board games, roulette games, indoor games using small moving playing bodies, e.g. pinball games, miscellaneous games, e.g. puzzle games. • Video games, i.e. games using an electronically generated display having two or more dimensions, e.g. on a television screen, showing representations related to the game. References relevant to classification in this subclass This subclass/group does not cover: Casino chips A44C 21/00 Sport games A63B Bowling games, games of pins, A63D billiards Video games, online or networked A63F 13/00 video games Guns (laser guns, water guns, etc.), F41A,F41B,F41C, F41J, F42B targets, darts Vending machines G07F Data-processing equipment G06F 17/00 characterised by a specific application for game playing Casino gaming machines, slot G07F 17/32 machines, medal game machines, coin pushers, online or networked gaming systems Educational games, i.e. games G09B 1 having educative or pedagogical purpose Informative references Attention is drawn to the following places, which may be of interest for search: Animal toys A01K 15/025 Nursery furniture A47D Household or table equipment A47G Toys A63H Robots B25J Cards in general (trading cards, B42D postcards, etc.) Ornamental bodies B44C