NSW's Rail Future on the Fast Track

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

New Nsw Rail Timetables Rail and Tram News

AUSTRALASIAN TIMETABLE NEWS No. 268, December 2014 ISSN 1038-3697 RRP $4.95 Published by the Australian Timetable Association www.austta.org.au NEW NSW RAIL TIMETABLES designated as Hamilton Yard (Hamilton Station end) and Sydney area Passenger WTT 15 Nov 2014 Hamilton Sidings (Buffer Stop end). Transport for NSW has published a new Passenger Working Timetable for the Sydney area, version 3.70. Book 2 The following sections of the Working Timetable will be re- Weekends is valid from 15 November, and Book 1 issued with effect from Saturday 3 January 2015: • Weekdays valid from 17 November. There appear to be no Section 7- Central to Hornsby-Berowra (All Routes) significant alterations other than the opening of Shellharbour • Section 8- City to Gosford-Wyong-Morisset- Junction station closing of Dunmore station. A PDF of the Broadmeadow-Hamilton new South Coast line Public timetable can be accessed from • Section 9- Hamilton to Maitland-Dungog/Scone. the Sydney trains website. Cover pages, Explanatory Notes and Section Maps will also be issued. Additionally, amendments to Section 6 will need Sydney area Freight WTT 15 Nov 2014 to be made manually to include updated run numbers and Transport for NSW has published a new Freight Working changes to Sydney Yard working as per Special Train Notice Timetable for the Sydney area, version 3.50. Book 5 0034-2015. The re-issued sections of Books 1 & 2 will be Weekends is valid from 15 November, and Book 4 designated as Version 3.92, and replace the corresponding Weekdays valid from 17 November. There appear to be no sections of Working Timetable 2013, Version 3.31, reprint significant alterations. -

DRIVERS ROUTE KNOWLEDGE DIAGRAMS BANKSTOWN LINE SYDENHAM Effective Date: July 2021

DRIVERS ROUTE KNOWLEDGE DIAGRAMS BANKSTOWN LINE SYDENHAM Effective Date: July 2021 MARRICKVILLE Version: 4.36 DULWICH HILL Explanatory Notes: HURLSTONE PARK Navigate to your area of interest via the station index or by using links created in Adobe bookmarks. CANTERBURY This document is approved for route knowledge only. CAMPSIE Do not use these diagrams for any safety related BELMORE purpose without validating the information against a controlled source or in the field. LAKEMBA Information in these diagrams is uncontrolled. WILEY PARK Please report any updates to [email protected] PUNCHBOWL BANKSTOWN YAGOONA BIRRONG Copyright: Sydney Trains Ownership: Geospatial Services Location: TRIM Record No.D2015/586 BANKSTOWN LINE TO ST PET ERS JOINS MAP IL 04 01 R A 3 4 GRADIENT I 5 SM 602 I L SECTION : SYDENHAM TO REGENTS PARK W 2 AUTO 1 MAP SET : SYDENHAM TO MARRICKVILLE A 6 5.419 KM SYDENHAM Y PAGE: 1 OF 2 P X 4 D 0 UPDATED TO : 12 April 2021 SM 604 IL E GLESSON AV OH E OH 75 5.414 KM X U INFORMATION D N PARK LN X R W SUBURBAN LINES O H Y I A N SM 611 CO X SM 607 I W CONTROLLED FROM : RAIL OPERATIONS CENTRE 1 L S 4 I 5.415 KM A K RD 7 R 20 OH R B PA 5.430 KM R 6 I 3 D RADIO AREA CODE : 004 (SYDENHAM) 7 SM 611 IL E LN 440 IN 1 SM 609 IL G BELMOR HOME E 005 (SYDENHAM) OH 5.412 KM R 5 X 6 X3 X 5 5.418 KM D X X 0 ANY LINE FREIGHT LINE CONTROLLED FROM X4 X SM 613 BOT X 4 7 0 JUNEE NCCS " SYDNEY 1" BOARD 5 4 5.523 KM SM 612 5 0 X 5.525 KM PHONE No. -

Weekly Notice

1 weekly notice Monday, 28 December 2020 Sunday, 03 January 2021 Safeworking information, including Weekly Notices and SAFE Notices, is available on the RailSafe website. By accessing Weekly Notices and SAFE Notices online, you will receive safety information more quickly. Weekly Notices remain on the RailSafe website for two years; Permanent and Temporary SAFE Notices remain online as long as they are current. Anyone needing back issues of Weekly Notices and SAFE Notices should contact the Network Rules unit. If you are outside Sydney Trains, you can reach the RailSafe website via the following address: www.railsafe.org.au Other Safeworking documents, such as Network Rules, Network Procedures, Network Local Appendices, Safeworking Policies, SafeTracks flyers, and contractor information are also available online. Director Safety and Standards Sydney Trains Continued on next page 1 weekly notice CONTENTS PUBLICATION DEADLINES AND SUBMISSION OF ARTICLES 4 CAMPBELLTOWN SIGNAL BOX AND SOUTH WEST MAINTENANCE TERRITORY – TRIAL OF NON-LOCAL POSSESSION AUTHORITY TRACK ACCESS PRE-APPROVAL PROCESS 5 MERRYLANDS RATIONALISATION - STAGE 2 REMOVALS (DIAGRAM) 7 HAND OVER MAINTENANCE RESPONSIBILITY OF AUTOMATIC SELECTIVE DOOR OPERATION (ASDO) INFRASTRUCTURE ASSETS TO SYDNEY TRAINS FOR THE AREA CENTRAL TO NEWCASTLE INTERCHANGE VIA NORTH STRATHFIELD 8 NORTH SYDNEY - SPEED SIGN INSTALLATION 9 STATUS OF TOM NOTICES 10 STATUS OF PERMANENT SAFE NOTICES 11 STATUS OF NETWORK MANUALS AND FORMS 12 DISTRIBUTION OFFICERS 14 WN 1 — 28 December 2020 3 weekly notice PUBLICATION DEADLINES AND SUBMISSION OF ARTICLES Dates of the next four Weekly Notices and deadlines for articles are: Weekly Notice For Week Deadline 2 04/01/2021 – 10/01/2021 08/12/2020 3 11/01/2021 – 17/01/2021 15/12/2020 4 18/01/2021 – 24/01/2021 22/12/2020 5 25/01/2021 – 31/01/2021 29/12/2020 To meet printing and distributing schedules, articles for a Weekly Notice must be received by its deadline. -

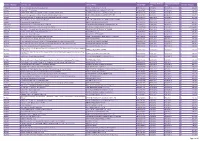

2012 Contracts (PDF, 498.96

Contract Awarded Contract Expiration Contract Number Contract Title Vendor Name VendorABN Contract Amount Date Date CW22831 V Line - Miscellaneous Services Agreement V/LINE PASSENGER PTY LTD 29087425269 1/01/2012 31/12/2012 $ 422,290 AL5913 Labour Hire - Test Analyst HCI PROFESSIONAL SERVICES PTY LTD 52108307955 5/01/2012 27/06/2016 $ 334,710 AL6212 General Solid Waste For Disposal Contract For Spent Railway Spoil COMPACTION & SOIL TESTING SERVICES PTY LTD 44106976738 6/01/2012 31/05/2013 $ 179,559 AL6696 Concrete Or Aggregates Or Stone Products Manufacturing Services BORAL RESOURCES (COUNTRY) PTY LTD 51000187002 9/01/2012 30/05/2013 $ 148,872 AL7090 Maintenance Works For Outdoor Advertising Billboards At Seven Locations SFS 22703705163 10/01/2012 21/05/2012 $ 217,100 AL7099 Oracle Software License Update And Support. ORACLE CORPORATION AUSTRALIA PTY LIMITED 80003074468 10/01/2012 23/01/2012 $ 1,293,796 AL8049 Procurement Of Legal Services HENRY DAVIS YORK LAWYERS 94516079651 12/01/2012 16/01/2012 $ 282,939 CW21625 Supply And Implement Waratah Train Set Qa Db INTEGRUM MANAGEMENT SYSTEMS PTY LTD 73125273494 13/01/2012 30/06/2016 $ 542,551 CW34115 Supply Of On-Board Catering Services For Nsw Trains APEX PACIFIC SERVICES PTY. LTD. 16102856440 14/01/2012 15/07/2016 $ 25,682,400 CW34571 Nsw Trains - Country Regional Network (Crn) Access Agreement CRN COUNTRY REGIONAL NETWORK 61009252653 15/01/2012 14/01/2015 $ 3,700,000 BL0124 Climate Change Vulnerability Assessment Fees ADVISIAN PTY LTD 50098008818 16/01/2012 26/07/2012 $ 149,285 BL0358 Labour Hire - Project Manager PROVINCIAL PERSONNEL 11002921468 16/01/2012 19/09/2013 $ 237,827 BL1229 Asset Taggingaffix Railcorp Supplied Barcode Label ADNET TECHNOLOGY AUSTRALIA PTY LIMITED 52071304213 18/01/2012 29/03/2012 $ 186,816 BL1343 Greta & Branxton Footbridge Balustrade Upgrade RKR ENGINEERING 74052053031 18/01/2012 5/07/2012 $ 198,000 BL1218 Planned Bus Services From Central To Wollongong/Dapto On 4 And 5 February 2012. -

Digital Starting Blocks: the Sydney Metro Experience Samantha Mcwilliam1, Damien Cutcliffe2 1&2WSP, Sydney, AUSTRALIA Corresponding Author: [email protected]

Digital starting blocks: The Sydney Metro experience Samantha McWilliam1, Damien Cutcliffe2 1&2WSP, Sydney, AUSTRALIA Corresponding Author: [email protected] SUMMARY Sydney Metro is currently Australia’s biggest public transport project. Stage 1 and 2 of this new standalone railway will ultimately deliver 31 metro stations and more than 66 kilometres of new metro rail, revolutionising the way Australia’s biggest city travels. Once it is extended into the central business district (CBD) and beyond in 2024, metro rail will run from Sydney’s booming North West region under Sydney Harbour, through new underground stations in the CBD and beyond to the south west. Sydney Metro City and Southwest (Stage 2) features twin 15.5km tunnels along with 7 new underground stations between Chatswood and Sydenham. The line is extended beyond Sydenham with an upgrade of the existing Sydney Trains heavy rail line to Bankstown. The adoption of a digital engineering approach on the Sydney Metro City and Southwest project resulted in an unprecedented level of collaboration and engagement between designers, clients and stakeholders. The use of tools such as WSP’s bespoke web based GIS spatial data portal Sitemap allowed geographically mapped data to be made securely available to all stakeholders involved on the project, enabling the team to work off a common data set while simultaneously controlling/restricting access to sensitive data. Over the course of the project this portal was enhanced to act as a gateway to all other digital content developed for such as live digital design models, virtual reality and augmented reality content. This portal was the prototype for what is now called ‘WSP Create’. -

INSTITUTE of TRANSPORT and LOGISTICS STUDIES WORKING

WORKING PAPER ITLS-WP-19-05 Collaboration as a service (CaaS) to fully integrate public transportation – lessons from long distance travel to reimagine Mobility as a Service By Rico Merkert, James Bushell and Matthew Beck Institute of Transport and Logistics Studies (ITLS), The University of Sydney Business School, Australia March 2019 ISSN 1832-570X INSTITUTE of TRANSPORT and LOGISTICS STUDIES The Australian Key Centre in Transport and Logistics Management The University of Sydney Established under the Australian Research Council’s Key Centre Program. NUMBER: Working Paper ITLS-WP-19-05 TITLE: Collaboration as a service (CaaS) to fully integrate public transportation – lessons from long distance travel to reimagine Mobility as a Service Integrated mobility aims to improve multimodal integration to ABSTRACT: make public transport an attractive alternative to private transport. This paper critically reviews extant literature and current public transport governance frameworks of both macro and micro transport operators. Our aim is to extent the concept of Mobility-as-a-Service (MaaS), a proposed coordination mechanism for public transport that in our view is yet to prove its commercial viability and general acceptance. Drawing from the airline experience, we propose that smart ticketing systems, providing Software-as-a-Service (SaaS) can be extended with governance and operational processes that enhance their ability to facilitate Collaboration-as-a-Service (CaaS) to offer a reimagined MaaS 2.0 = CaaS + SaaS. Rather than using the traditional MaaS broker, CaaS incorporates operators more fully and utilises their commercial self-interest to deliver commercially viable and attractive integrated public transport solutions to consumers. This would also facilitate more collaboration of private sector operators into public transport with potentially new opportunities for taxi/rideshare/bikeshare operators and cross geographical transport providers (i.e. -

Temporary Exemptions to the Australian Human Rights Commission

Temporary Exemptions to the Australian Human Rights Commission Disability Standards for Accessible Public Transport Disability (Access to Premises – Buildings) Standards) September 2019 | Version: 1 Contents 1 Introduction ............................................................................................................. 3 2 Key achievements ................................................................................................... 4 3 Temporary exemptions from the Transport Standards and Premises Standards ..... 5 3.1 Part 2.1 Access paths – unhindered passage (H2.2) .................................. 5 3.2 Part 2.1 Access paths – unhindered passage (H2.2) .................................. 6 3.3 Part 2.4 Access paths – minimum obstructed width (H2.2) ......................... 7 3.4 Part 2.6 Access paths – conveyances ........................................................ 7 3.5 Part 4.2 Passing areas – two-way access paths and aerobridges (H2.2) .... 8 3.6 Part 5.1 Resting points – when resting points must be provided ................. 8 3.7 Part 6.4 Slope of external boarding ramps .................................................. 9 3.8 Part 8.2 Boarding – when boarding devices must be provided.................. 10 3.9 Part 11.2 Handrails and grabrails – handrails to be provided on access paths (H2.4) ....................................................................................................... 11 3.10 Part 15.3 Toilets – unisex accessible toilets – ferries and accessible rail cars 11 3.11 Part 15.4 Toilets -

Sydney Trains Corporate Plan 2016-2017

Transport Sydney Trains 2016-2017 Corporate Plan 2 Sydney Trains Corporate Plan 2016-17 Contents Sydney Trains – key statistics 4 Chief Executive’s message 5 Legislative context 7 Strategic alignment 8 Safety 9 Customer, accessibility and travel 10 People 11 Business 12 Assets 13 Environment and the community 14 Sydney Trains Corporate Plan 2016-17 3 Sydney Trains – key statistics • Customer satisfaction: 90%, up from 88% in our last survey • Passenger journeys per weekday: 1 million • Annual patronage: 307 million (for 12 months to 31 December 2015) • Timetabled trips per typical weekday: 2,961 • Stations: 178 (includes four on the Airport Line) • Fleet: 2,191 electric and diesel cars (includes 574 NSW TrainLink fleet) • Number of passengers one eight-car train can carry: 1,000 plus • Capitalised value of a new Waratah train: $30 million • Length of total track maintained: 1,643km (includes NSW TrainLink area) • Length of electrified track (bounded by Emu Plains, Berowra, Waterfall and Macarthur): 961km • Length of overhead wiring maintained: 1,576km (includes NSW TrainLink) • CCTV cameras maintained: more than 10,000 • Total cost of operations: $2.7 billion • Value of assets under Sydney Trains management: $35 billion • Workforce head count: approximately 10,000 (as at May 2016) 4 Sydney Trains Corporate Plan 2016-17 Chief Executive’s message I want to share with you Sydney Trains’ priorities for the 2016-2017 financial year. Sydney Trains was established on 1 July 2013 and is the operator, maintainer and deliverer of choice for rail services across Sydney. This includes 178 stations, 961kms of electrified track and signals, and 2,191 electric and diesel cars, among them 574 NSW TrainLink cars. -

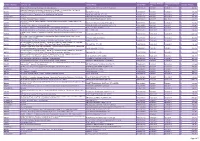

2017 Contracts (PDF, 335.48

Contract Awarded Contract Expiration Contract Number Contract Title Vendor Name VendorABN Contract Amount Date Date EA6922 Bridge Refurbishment @ Shoalhaven Rd Kiama Msa 2615 ABERGELDIE CONTRACTORS PTY LIMITED 47004533519 3/01/2017 18/09/2017 $ 268,694 Additional Analysis On Infrastructure Requirements To Mitigate The Loss Of Mmc, Ttu Phase 2, EA7011 Potential Benefits From An (Description Truncated, Refer To Ariba) ADVISIAN PTY LTD 50098008818 4/01/2017 13/06/2017 $ 191,750 EA7059 Crew62810 - We28 - Transmission Line Modifications And Removal JOHN HOLLAND RAIL PTY LTD 61009252653 4/01/2017 23/02/2018 $ 939,731 ST00EA7059 Services CRN COUNTRY REGIONAL NETWORK 61009252653 4/01/2017 23/02/2018 $ 401,080 EA7508 1 X Track Technical Trainer 12 Months SWETHA INTERNATIONAL P/L (RCTI) 13067280433 9/01/2017 9/02/2018 $ 263,873 168027Ar - Technical Change Manager - Electrical Isolations Improvement Program- Labour Hire EA7503 Engagement MANTECH INTERNATIONAL SYSTEMS PL 74003393155 9/01/2017 19/09/2017 $ 155,306 EA7504 Variation To Msa 1051, We18 Hornsby Refurbs AFFECTIVE SERVICES AUSTRALIA PTY LTD 64093395558 9/01/2017 1/02/2017 $ 471,097 EA7633 167939Wh - Extension 1: Technical Specialist Control Systems, Neil Dsouza AURECON AUSTRALASIA PTY LTD 54005139873 10/01/2017 5/07/2018 $ 662,310 EA8019 168562Mb - First Extension Tmp Engineering Analyst, Tmp Backlog Management Project KELLY SERVICES 45010806523 12/01/2017 9/11/2017 $ 409,609 Eraring Culvert Extension - Extension Of Culvert At Eraring On The Main North Line As Per Project EA7957 Order. JOHN HOLLAND PTY LTD 11004282268 12/01/2017 22/09/2017 $ 1,365,120 167814Aa - There Is A Requirement For An Additional Senior Business Analyst (Cims) For Rail EA8444 Operations Centre Program. -

Drivers Route Knowledge Diagrams North Shore Line

DRKD DRIVERS ROUTE KNOWLEDGE DIAGRAMS NORTH SHORE LINE CENTRAL Effective Date: August 2021 TOWN HALL Version: 5.55 WYNYARD Explanatory Notes: MILSONS POINT Navigate to your area of interest via the station index NORTH SYDNEY or by using links created in Adobe bookmarks. This document is approved for route knowledge only. WAVERTON Do not use these diagrams for any safety related WOLLSTONECRAFT purpose without validating the information against a controlled source or in the field. ST LEONARDS Information in these diagrams is uncontrolled. ARTARMON Please report any updates to [email protected] CHATSWOOD ROSEVILLE LINDFIELD KILLARA GORDON PYMBLE TURRAMURRA WARRAWEE WAHROONGA WAITARA HORNSBY Copyright: Sydney Trains Ownership: Geospatial Services, Enterprise Asset Systems Location: TRIM Record No.D2015/569 NORTH SHORE LINE 01 TO AIRPORT LINE TOREDFERN JOINS MAP NSR 02 JOINS MAP MS 01 6 R 6 5 2 2 O 2 3 2 45 6 T A 3 C I 8 D 3 N I PONR PONR PONR 3 O 3 H O SYDNEY TERMINAL 3 8 H "K" 8 U "K" D 8 5 7 1 O P U W P I L U N L SY 381 S S Y 383 L L SY 387 SR S Y 385 IL P O A I HOME HOME HOME HOME L I W C L E L 0.182 KM A 0.180 KM 0.181 KM 0.182 KM L A A D N L I A 10 2 1 RR W O 15 3 3 L W 3 WN 8 8 A 13 11 T 14 6 PONR PONR PONR PONR A A 0 2 4 R R 12 R 7 R L L 8 O 5 R O 9 A O P I A SY 367 SY 365 SH C C L A A DCO HOME HOME O A L N L CENTRAL C 5.692 KM 0.154 KM A W 16 23 21 17 UP L O 20 D D 19 18 PONR S PONR 22 O U W B N U S R R U O B B T A U A N C R R I OH R O D H 6 B D D A 7 N A N N - I I I 3 PL N O N 3 8 SO 8 W 7 A C 7 R 7 9 0 KM 0 Y3 5 Y3 -

Save T3 Bankstown Line Future Transport Survey

Save T3 Bankstown Line Future Transport Survey Rail west of Bankstown in 2024 T3 Bankstown Line: Lidcombe to Bankstown shuttle Transport for NSW is planning for future rail and bus services for the West of Bankstown area including a number of potential new transit corridors. Following a successful local residents' campaign against the closure of train stations in the West of Bankstown area, Transport for NSW has announced the reinstatement of the former Inner West Line's City to Liverpool via Regents Park train service in 2024. A number of changes to the existing T3 Bankstown Line have been announced for 2024 including the removal of all direct trains to City from Birrong and Yagoona as well as the removal of direct trains between Bankstown and Liverpool. Transport for NSW has also indicated that the Lidcombe to Bankstown shuttle service (for Birrong and Yagoona) will likely be superseded in future with a new transport corridor between Parramatta and Kogarah via Bankstown. The NSW Government has not confirmed its indicative route for the new Parramatta to Kogarah corridor beyond indicating that a potential connection to existing services will be established in the West of Bankstown area before reaching the Bankstown Interchange. Canterbury-Bankstown Council is advocating for the new corridor to service Chullora (new station east of Yagoona) while Cumberland Council has earmarked the new corridor to meet existing services at Chester Hill. Transport for NSW has announced that the extension of Sydney Metro Southwest from Bankstown to Liverpool is temporarily paused with other transport options such as rapid bus or trackless trams being considered as an alternative to rail services for the West of Bankstown area. -

Cityrail Performance Update

Sydney Trains Performance Update Comparison with International Benchmarking Groups [2018 data] • Membership of international benchmarking groups allows Sydney Trains to compare its performance to international peers and, through sharing best practices, identify opportunities for improvement. • Sydney Trains belongs to the International Suburban Railway Benchmarking Group (ISBeRG), which comprises 14 suburban railways. Typically, these railways link the suburbs to the CBD, with longer lines and larger networks than metros, but with fewer, longer, passenger journeys. Sydney Trains joined this group in 2011. • Sydney Trains is also a member of the ‘Nova’ group, which is part of the wider ‘Community of Metros’. The Community of Metros consists of: o ‘CoMET’, a group of 20 of the world’s largest metros. Its constituents typically have more than 500 million passenger journeys per annum. o ‘Nova’ is a group of 22 small to medium-sized metros, typically with fewer than 500 million passenger journeys per annum. Sydney Trains joined the Nova benchmarking group in September 2007. • Benchmarking between the members of the various groups is undertaken annually. This document provides a provisional update of selected charts from Sydney Trains’ previously published report and shows results for the calendar years 2014 to 2018. To preserve confidentiality of other members’ data, Sydney Trains’ performance is compared to the: o average of all ISBeRG Members o average of all CoMET Members o average of all Nova Members o individual ISBeRG members, on an anonymised basis • In some cases there are changes to previously published figures due to revision of data. Comparison to averages may disguise some significant ‘highs’ and ‘lows’ in performance: individual results within each group may vary significantly.