02 Editorial Information 03 Commentary a Shared

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fossil Fuels………………………………………………

Corso di Laurea magistrale in Relazioni Internazionali Comparate Tesi di Laurea Energy and Environment Between development and sustainability Relatore Ch. Prof. Matteo Legrenzi Correlatore Ch. Prof. Duccio Basosi Laureando Alberto Lora Matricola 987611 Anno Accademico 2013 / 2014 TABLE OF CONTENTS Abstract………………………………………………………………………………………………i Introduction...………………………………………………………….........................................1 PART 1 - ENERGY SECURITY Chapter 1. Energy Security……………………………………………………………………...7 1.1 What is energy security?.......................................................................................................7 1.1.1 Definition of energy security…………………………………………………………………………..7 1.1.2 Elements of energy security………………………………………………………………………….8 1.1.3 Different interpretations of energy security………………………………………………………….9 1.1.4 Theories about energy security……………………………………………………………………..11 1.2 Diversification of the energy mix…………………………………………………………………12 1.2.1 Types of energy sources………………………………..............................................................12 1.2.2 Definition of energy mix……………………………………………………………………………..13 1.3 Growing risks………………………………………………………………………………………16 1.3.1 Energy insecurity……………………………………………………………………………………..16 1.3.2 Geological risk………………………………………………………………………………………..17 1.3.3 Geopolitical risk…………………………………………………………………….........................18 1.3.4 Economic risk…………………………………………………………………………………………22 1.3.5 Environmental risk……………………………………………………………………………………22 1.3.6 Solutions………………………………………………………………………………………………23 -

Monthly Report on Petroleum Developments in the World Markets February 2020

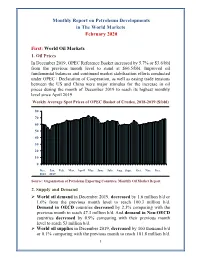

Monthly Report on Petroleum Developments in The World Markets February 2020 First: World Oil Markets 1. Oil Prices In December 2019, OPEC Reference Basket increased by 5.7% or $3.6/bbl from the previous month level to stand at $66.5/bbl. Improved oil fundamental balances and continued market stabilization efforts conducted under OPEC+ Declaration of Cooperation, as well as easing trade tensions between the US and China were major stimulus for the increase in oil prices during the month of December 2019 to reach its highest monthly level since April 2019. Weekly Average Spot Prices of OPEC Basket of Crudes, 2018-2019 ($/bbl) 80 70 60 50 40 30 20 10 0 Dec. Jan. Feb. Mar. April May June July Aug. Sept. Oct. Nov. Dec. 2018 2019 Source: Organization of Petroleum Exporting Countries, Monthly Oil Market Report. 2. Supply and Demand World oil demand in December 2019, decreased by 1.6 million b/d or 1.6% from the previous month level to reach 100.3 million b/d. Demand in OECD countries decreased by 2.3% comparing with the previous month to reach 47.3 million b/d. And demand in Non-OECD countries decreased by 0.9% comparing with their previous month level to reach 53 million b/d. World oil supplies in December 2019, decreased by 100 thousand b/d or 0.1% comparing with the previous month to reach 101.8 million b/d. 1 Non-OPEC supplies remained stable at the same previous month level of 67.2 million b/d. Whereas preliminary estimates show that OPEC crude oil and NGLs/condensates total supplies decreased by 0.6% comparing with the previous month to reach 34.5 million b/d. -

China's Dependence Upon Oil Supply: Part 1

PART 1 1 CHINA’S DEPENDENCE UPON OIL SUPPLY PART 1 of 3 SERIALIZED STUDY BY – CAPT David L.O. Hayward Australian Army Reserve (Retd.) First published as an RUSI Defence Research Paper & republished as a SAGE International Special Study with the kind permission of CAPT David L.O. Hayward 2012 PART 1 2 “War which has undergone the changes of modern technology and the market system will be launched even more in atypical forms. In other words, while we are seeing a relative reduction in military violence, at the same time we definitely are seeing an increase in political, economic, and technological violence. However, regardless of the form the violence takes, war is war, and a change in the external appearance does not keep any war from abiding by the principles of war.” The above quote is from the book Unrestricted Warfare jointly written by two People’s Liberation Army (PLA) Colonels, namely Qaio Liang and Wang Xiangsui. The book was published in Beijing in early 1999. In the twelve years since it was unveiled to the West, the work has largely been dismissed as unlikely wishful thinking on the part of the authors. The book is not representative of PLA military philosophy or official policy. As recently as 2008, discussions held at the Pentagon in strategic-level war games were dismissive of Chinese capability and intent in the cyber realm. Source: US Navy Institute Blog, Annapolis, Maryland: March 2010 2012 PART 1 3 UNCLASSIFIED CHINA’S DEPENDENCE UPON OIL SUPPLY” By CAPT David L.O. Hayward (Rtd), former IT consultant in the oil industry. -

Iraq's Oil Sector

June 14, 2014 ISSUE BRIEF: IRAQ’S OIL SECTOR BACKGROUND Oil prices rise on Iraq turmoil Oil markets have reacted strongly to the turmoil in Iraq, the world’s seventh largest oil producer, in recent weeks. International Brent oil prices hit 9-month highs over $113 a barrel on June 13 following the takeover by the Islamic State of Iraq and Syria (ISIS) of Mosul in the north as well as some regions further south with just a few thousand fighters. ISIS has targeted strategic oil operations in the past, attacking and shutting the Kirkuk-Ceyhan pipeline. In Syria, the group holds the Raqqa oil field. POTENTIAL GROWTH The OPEC nation is expected to be largest contributor to global oil supplies through 2035 Iraq’s potential to increase oil production in the coming decades is seen by analysts as a key component to global growth. The IEA's 2013 World Energy Outlook forecasts Iraqi crude and NGL production to ramp up to 5.8 million b/d by 2020 and to 7.9 million b/d by 2035 in the base case scenario, making it the single largest contributor to global oil supply growth through 2035. Iraq produced roughly 3.4 million b/d in May, according to the IEA. The IEA’s medium-term outlook forecasts Iraqi production could reach 4.8 million b/d by 2018. OIL RESERVES Vast reserves are among the cheapest to develop and produce in the world Iraq has the world's fifth largest proven oil reserves, with estimates ranging between 141 billion and 150 billion barrels. -

Crude Oil Price Movements

OPEC Monthly Oil Market Report 11 July 2018 Feature article: Oil Market Outlook for 2019 Oil market highlights iii Feature article v Crude oil price movements 1 Commodity markets 8 World economy 11 World oil demand 31 World oil supply 44 Product markets and refinery operations 63 Tanker market 71 Oil trade 76 Stock movements 81 Balance of supply and demand 87 Organization of the Petroleum Exporting Countries Helferstorferstrasse 17, A-1010 Vienna, Austria E-mail: prid(at)opec.org Website: www.opec.org Welcome to the Republic of the Congo Welcome to the Republic of the Congo as the 15th OPEC Member The 174th Meeting of the Conference approved the request from the Republic of the Congo to join the Organization of the Petroleum Exporting Countries (OPEC), with immediate effect from 22nd June 2018. In line with this development, data for the Republic of the Congo is now included within the OPEC grouping. As a result, the figures for OPEC crude production, demand for OPEC crude and non-OPEC supply as well as the OPEC Reference Basket have been adjusted to reflect this change. For comparative purposes, related historical data has also been revised. OPEC Monthly Oil Market Report – July 2018 i Welcome the Republic of Congo ii OPEC Monthly Oil Market Report – July 2018 Oil Market Highlights Oil Market Highlights Crude Oil Price Movements The OPEC Reference Basket (ORB) eased by 1.2% month-on-month (m-o-m) in June to average $73.22/b. The ORB ended 1H18 higher at $68.43/b, up more than 36% since the start of the year. -

Asymmetric Impacts of Oil Price on Inflation: an Empirical Study

energies Article Asymmetric Impacts of Oil Price on Inflation: An Empirical Study of African OPEC Member Countries Umar Bala 1,2 and Lee Chin 2,* 1 Department of Economics, Faculty of Management and Social Sciences, Bauchi State University, P.M.B. 65 Gadau, Nigeria; [email protected] 2 Department of Economics, Faculty of Economics and Management, Universiti Putra Malaysia, 43400 UPM Serdang, Selangor Darul Ehsan, Malaysia * Correspondence: [email protected]; Tel.: +60-603-8946-7769 Received: 14 August 2018; Accepted: 26 October 2018; Published: 2 November 2018 Abstract: This study investigates the asymmetric impacts of oil price changes on inflation in Algeria, Angola, Libya, and Nigeria. Three different kinds of oil price data were applied in this study: the actual spot oil price of individual countries, the OPEC reference basket oil price, and an average of the Brent, WTI, and Dubai oil price. Autoregressive distributed lag (ARDL) dynamic panels were used to estimate the short- and long-term impacts. Also, we partitioned the oil price into positive and negative changes to capture asymmetric impacts and found that both the positive and negative oil price changes positively influenced inflation. However, the impact was found to be more significant when the oil prices dropped. We also found that the money supply, the exchange rate, and the gross domestic product (GDP) are positively related to inflation, while food production is negatively related to inflation. Accordingly, policy-makers should be cautious when formulating policies between the positive and negative changes in oil prices, as it was shown that inflation increased when the oil price dropped. -

A Legal Analysis of Production Sharing Contract Arrangements in the Nigerian Petroleum Industry

Journal of Energy Technologies and Policy www.iiste.org ISSN 2224-3232 (Paper) ISSN 2225-0573 (Online) Vol.5, No.8, 2015 A Legal Analysis of Production Sharing Contract Arrangements in the Nigerian Petroleum Industry Dr. Taiwo Adebola Ogunleye Department of Business Law, Faculty of Law, Obafemi Awolowo University, Ile-Ife. Nigeria, Abstract Production sharing contract (PSC) is an arrangement used in the upstream sector for the exploration and development of petroleum resources. Several oil producing countries, particularly the developing ones have adopted it as a contract for the exploration and development of their oil and gas resources. Nigeria has adopted it for the exploration and development of the offshore and inland basin. This paper examined the concept and general basic features of PSC. It went further to look at the PSC arrangements in Nigeria and observed that there are various models of PSC executed in Nigeria and identified the significant differences in each one. In addition, it reviewed the Deep Offshore and Inland Basin Production Sharing Contracts Act, 1999 which gave legislative backing to the fiscal terms granted by the Government to certain PSC models. It evaluated the various models of PSC executed in Nigeria and ascertained the shortcomings in them. Keywords: production sharing contract, different models of production sharing contract in Nigeria 1. Introduction Production Sharing Contract (PSC) is a distinct petroleum arrangement that has been adopted by many developing countries in the exploration and production of their petroleum resources as it guarantees the sovereign right of the state over these resources and meets their economic desires by providing capital and technology for their production. -

Law on Pollution and Debris from Oil and Gas Drilling and Production Operations Offshore Nova Scotia

Schulich School of Law, Dalhousie University Schulich Law Scholars LLM Theses Theses and Dissertations 1998 Law on Pollution and Debris from Oil and Gas Drilling and Production Operations Offshore Nova Scotia Boris B. De Jonge Follow this and additional works at: https://digitalcommons.schulichlaw.dal.ca/llm_theses Part of the Administrative Law Commons, Environmental Law Commons, Law of the Sea Commons, and the Oil, Gas, and Mineral Law Commons LAW ON POLLUTION AND DEBRIS FROM OIL AND CAS DRILLING AND PRODUCTION OPERATIONS OFFSHORE NOVA SCOTIA by Bons B. de Jonge Submitted in partial fùlfillment of the requirements for the degree of Master of Laws Dalhousie Law School Halifax, Nova Scotia December 1998 Copyright O Boris B. de Jonge, 1998 National Library Bibliothèque nationale 1*1 ofCanada du Canada Acquisitions and Acquisitions et Bibliographie Services seiuices bibliographiques 395 Wellington Street 395. rue Wellington OttawaON K1A ON4 OaawaOcu KlAW canada canada The author has granted a non- L'auteur a accordé une licence non exclusive licence allowing the exclusive permettant à la National Library of Canada to Bibliothèque nationale du Canada de reproduce, loan, distribute or sell reproduire, prêter, distribuer ou copies of this thesis in microform, vendre des copies de cette thèse sous paper or electronic formats. la forme de microfiche/film, de reproduction sur papier ou sur format électronique. The author retains ownership of the L'auteur conserve la propriété du copyright in this thesis. Neither the droit d'auteur qui protège cette thèse. thesis nor substantial extracts fiom it Ni la thèse ni des extraits substantiels may be printed or otherwise de celle-ci ne doivent être imprimés reproduced without the author's ou autrement reproduits sans son permission. -

2005/06 Annual Service Plan Report National Library of Canada Cataloguing in Publication Data British Columbia

Ministry of Energy, Mines and Petroleum Resources 2005/06 Annual Service Plan Report National Library of Canada Cataloguing in Publication Data British Columbia. Ministry of Energy, Mines and Petroleum Resources. Annual service plan report. — 2005/06 – Annual. Continues: British Columbia. Ministry of Energy and Mines. Annual service plan report. ISSN 1705-9275. ISSN 1911-0162 = Annual service plan report (British Columbia. Ministry of Energy, Mines and Petroleum Resources) 1. British Columbia. Ministry of Energy, Mines and Petroleum Resources – Periodicals. 2. Mines and mineral resources – British Columbia – Periodicals. 3. Mineral industries – Government policy – British Columbia – Periodicals. 4. Petroleum industry and trade – Government policy – British Columbia – Periodicals. I. Title. II. Title: Ministry of Energy, Mines and Petroleum Resources ... annual service plan report. TN27.B7B74 354.4’0971105 C2006-960091-0 For more information on the British Columbia Ministry of Energy, Mines and Petroleum Resources, contact: Ministry of Energy, Mines and Petroleum Resources PO BOX 9319 STN PROV GOVT VICTORIA BC V8W 9N3 or visit our website at http://www.gov.bc.ca/em/ Published by the Ministry of Energy, Mines and Petroleum Resources Ministry of Energy, Mines and Petroleum Resources Message from the Minister and Accountability Statement Energy, mining and petroleum resources drive British Columbia’s dynamic and modern economy. B.C. is experiencing renewed development of these important resource sectors within our thriving economy. B.C.’s real GDP grew by a solid 3.5 per cent in 2005, slightly faster than the 3.4 per cent growth rate forecast in the September Budget Update. This growth ranks B.C. first in Canada in per capita job creation in 2005. -

Market Indicators As at End*: August-2020

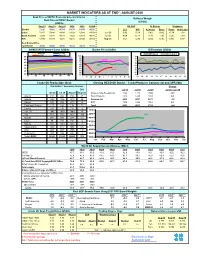

MARKET INDICATORS AS AT END*: AUGUST-2020 Spot Price of OPEC Basket & Selected Crudes Refiners' Margin Real Price of OPEC Basket (US$/b) (US$/b) Aug-18 Aug-19 Aug-20 2018 2019 2020# US Gulf N. Europe Singapore Basket 72.26 59.62 45.19 69.78 64.04 40.50 LLS WTI A. Heavy Brent Oman Arab Light Dubai 72.47 58.88 43.89 69.68 63.48 41.54 Jun-20 3.92 5.19 0.42 0.42 -0.74 1.02 North Sea Dtd 72.64 58.83 44.79 71.22 64.19 40.88 Jul-20 4.64 6.13 -1.86 1.30 1.26 1.99 WTI 67.99 54.84 42.36 65.16 57.02 38.15 Aug-20 3.67 5.30 -2.05 0.16 0.86 0.87 Real Basket Price Jun01=100 46.86 39.02 28.30 35.22 44.73 26.19 NYMEX WTI Forward Curve (US$/b) Basket Price (US$/b) Differentials (US$/b) May-20 Jun-20 WTI-Brent Brent-Dubai Jul-20 Aug-20 50 100 3 90 2 45 2018 80 1 70 40 0 60 35 2019 -1 50 30 40 -2 2020 -3 25 30 20 -4 20 10 -5 1M 3M 5M 7M 9M 11M J F M A M J J A S O N D 03 05 07 11 13 17 19 21 25 27 31 Crude Oil Production (tb/d) Closing OECD Oil Stocks - Crude/Products Commercial and SPR (Mb) Crude Oil Production (Tb/d) Production: Secondary Sources Change Diff. -

End of the Concessionary Regime: Oil and American Power in Iraq, 1958‐1972

THE END OF THE CONCESSIONARY REGIME: OIL AND AMERICAN POWER IN IRAQ, 1958‐1972 A DISSERTATION SUBMITTED TO THE DEPARTMENT OF HISTORY AND THE COMMITTEE ON GRADUATE STUDIES OF STANFORD UNIVERSITY IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PHILOSOPHY Brandon Wolfe‐Hunnicutt March 2011 © 2011 by Brandon Roy Wolfe-Hunnicutt. All Rights Reserved. Re-distributed by Stanford University under license with the author. This work is licensed under a Creative Commons Attribution- Noncommercial 3.0 United States License. http://creativecommons.org/licenses/by-nc/3.0/us/ This dissertation is online at: http://purl.stanford.edu/tm772zz7352 ii I certify that I have read this dissertation and that, in my opinion, it is fully adequate in scope and quality as a dissertation for the degree of Doctor of Philosophy. Joel Beinin, Primary Adviser I certify that I have read this dissertation and that, in my opinion, it is fully adequate in scope and quality as a dissertation for the degree of Doctor of Philosophy. Barton Bernstein I certify that I have read this dissertation and that, in my opinion, it is fully adequate in scope and quality as a dissertation for the degree of Doctor of Philosophy. Gordon Chang I certify that I have read this dissertation and that, in my opinion, it is fully adequate in scope and quality as a dissertation for the degree of Doctor of Philosophy. Robert Vitalis Approved for the Stanford University Committee on Graduate Studies. Patricia J. Gumport, Vice Provost Graduate Education This signature page was generated electronically upon submission of this dissertation in electronic format. -

China in the Transition to a Low-Carbon Economony

EAST-WEST CENTER WORKING PAPERS Economics Series No. 109, February 2010 China in the Transition to a Low-Carbon Economy ZhongXiang Zhang WORKING PAPERS WORKING The East-West Center promotes better relations and understanding among the people and nations of the United States, Asia, and the Pacific through coopera- tive study, research, and dialogue. Established by the U.S. Congress in 1960, the Center serves as a resource for information and analysis on critical issues of com- mon concern, bringing people together to exchange views, build expertise, and develop policy options. The Center’s 21-acre Honolulu campus, adjacent to the University of Hawai‘i at Mānoa, is located midway between Asia and the U.S. mainland and features research, residential, and international conference facilities. The Center’s Washington, D.C., office focuses on preparing the United States for an era of growing Asia Pacific prominence. The Center is an independent, public, nonprofit organi zation with funding from the U.S. government, and additional support provided by private agencies, individuals, foundations, corporations, and governments in the region. East-West Center Working Papers are circulated for comment and to inform interested colleagues about work in progress at the Center. For more information about the Center or to order publications, contact: Publication Sales Office East-West Center 1601 East-West Road Honolulu, Hawai‘i 96848-1601 Telephone: 808.944.7145 Facsimile: 808.944.7376 Email: [email protected] Website: EastWestCenter.org EAST-WEST CENTER WORKING PAPERS Economics Series No. 109, February 2010 China in the Transition to a Low-Carbon Economy ZhongXiang Zhang ZhongXiang Zhang is a Senior Fellow at the East-West Center.