Asymmetric Impacts of Oil Price on Inflation: an Empirical Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fossil Fuels………………………………………………

Corso di Laurea magistrale in Relazioni Internazionali Comparate Tesi di Laurea Energy and Environment Between development and sustainability Relatore Ch. Prof. Matteo Legrenzi Correlatore Ch. Prof. Duccio Basosi Laureando Alberto Lora Matricola 987611 Anno Accademico 2013 / 2014 TABLE OF CONTENTS Abstract………………………………………………………………………………………………i Introduction...………………………………………………………….........................................1 PART 1 - ENERGY SECURITY Chapter 1. Energy Security……………………………………………………………………...7 1.1 What is energy security?.......................................................................................................7 1.1.1 Definition of energy security…………………………………………………………………………..7 1.1.2 Elements of energy security………………………………………………………………………….8 1.1.3 Different interpretations of energy security………………………………………………………….9 1.1.4 Theories about energy security……………………………………………………………………..11 1.2 Diversification of the energy mix…………………………………………………………………12 1.2.1 Types of energy sources………………………………..............................................................12 1.2.2 Definition of energy mix……………………………………………………………………………..13 1.3 Growing risks………………………………………………………………………………………16 1.3.1 Energy insecurity……………………………………………………………………………………..16 1.3.2 Geological risk………………………………………………………………………………………..17 1.3.3 Geopolitical risk…………………………………………………………………….........................18 1.3.4 Economic risk…………………………………………………………………………………………22 1.3.5 Environmental risk……………………………………………………………………………………22 1.3.6 Solutions………………………………………………………………………………………………23 -

Prospectus That Received from the Autorité Des Marchés Financiers (The "AMF") Visa Number 11-511 on 4 November 2011

MAUREL & PROM NIGERIA A French limited liability company (société anonyme) with a share capital of EUR 133,433,534.30 Registered office: 12 rue Volney, 75002 Paris R.C.S. Paris 517 518 247 ENGLISH LANGUAGE TRANSLATION FOR INFORMATION PURPOSES ONLY This document is a free translation of the French language prospectus that received from the Autorité des marchés financiers (the "AMF") visa number 11-511 on 4 November 2011. It has not been approved by the AMF. This translation has been prepared solely for the information and convenience of shareholders of Etablissements Maurel & Prom S.A. No assurances are given as to the accuracy or completeness of this translation, and Etablissements Maurel & Prom and Maurel & Prom Nigeria assume no responsibility with respect to this translation or any misstatement or omission that may be contained therein. In the event of any ambiguity or discrepancy between this translation and the French Prospectus, the French Prospectus shall prevail. MAUREL & PROM NIGERIA A French limited liability company (société anonyme) with a share capital of EUR 133,433,534.30 Registered office: 12 rue Volney, 75002 Paris R.C.S. Paris 517 518 247 PROSPECTUS PREPARED IN CONNECTION WITH THE ADMISSION OF MAUREL & PROM NIGERIA SHARES TO TRADING ON THE REGULATED MARKET OF NYSE EURONEXT IN PARIS WITHIN THE CONTEXT OF THE ALLOCATION OF MAUREL & PROM NIGERIA SHARES TO THE SHAREHOLDERS OF ETABLISSEMENTS MAUREL & PROM Pursuant to Articles L. 412-1 and L. 621-8 of the French Monetary and Financial Code and Articles 211-1 to 216-1 of its General Regulations, the French Autorité des Marchés Financiers (AMF) approved the present prospectus under number 11-511 on 4 November 2011. -

Monthly Report on Petroleum Developments in the World Markets February 2020

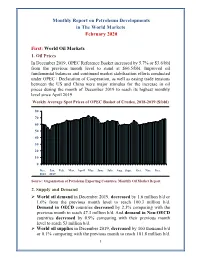

Monthly Report on Petroleum Developments in The World Markets February 2020 First: World Oil Markets 1. Oil Prices In December 2019, OPEC Reference Basket increased by 5.7% or $3.6/bbl from the previous month level to stand at $66.5/bbl. Improved oil fundamental balances and continued market stabilization efforts conducted under OPEC+ Declaration of Cooperation, as well as easing trade tensions between the US and China were major stimulus for the increase in oil prices during the month of December 2019 to reach its highest monthly level since April 2019. Weekly Average Spot Prices of OPEC Basket of Crudes, 2018-2019 ($/bbl) 80 70 60 50 40 30 20 10 0 Dec. Jan. Feb. Mar. April May June July Aug. Sept. Oct. Nov. Dec. 2018 2019 Source: Organization of Petroleum Exporting Countries, Monthly Oil Market Report. 2. Supply and Demand World oil demand in December 2019, decreased by 1.6 million b/d or 1.6% from the previous month level to reach 100.3 million b/d. Demand in OECD countries decreased by 2.3% comparing with the previous month to reach 47.3 million b/d. And demand in Non-OECD countries decreased by 0.9% comparing with their previous month level to reach 53 million b/d. World oil supplies in December 2019, decreased by 100 thousand b/d or 0.1% comparing with the previous month to reach 101.8 million b/d. 1 Non-OPEC supplies remained stable at the same previous month level of 67.2 million b/d. Whereas preliminary estimates show that OPEC crude oil and NGLs/condensates total supplies decreased by 0.6% comparing with the previous month to reach 34.5 million b/d. -

Opportunities for Gas in Sub-Saharan Africa

January 2019 OpportunitiesOpportunitiesOpportunities forfor GasGas for inin Gas in SubSubSub--SaharanSaharan-SubSaharan-Saharan AfricaAfrica Afric Africa Oppa 1. Introduction In his December 2017 paper entitled “Challenges to the Future of Gas: unburnable or unaffordable?”1, Jonathan Stern noted that “For the period up to 2030, the principal threats to the future of gas (outside North America) will be affordability and competitiveness. Beyond that date – and particularly beyond 2040 – carbon (and potentially also methane) emissions from gas will cause it to become progressively ‘unburnable’ if COP21 targets are to be met.” Stern noted further that in the period to 2030 and beyond, for gas to fulfil its potential role as a transition fuel, then it has to be delivered to high-income national markets below $8/MMbtu and to low-income markets below $6/MMbtu, and that “the major challenge to the future of gas will be to ensure that it does not become (and in many low-income countries remain) unaffordable and/or uncompetitive, long before its emissions make it unburnable”. In many low-income countries, especially in Asia, gas is often competing with coal in the power generation market, and to have any chance of competing, then gas has to be priced very competitively. There are examples, such as China, where a combination of policies related to improving air quality and mandated closure of some older plant have allowed the expansion of gas in the power, industry and heat sectors. In the UK, a high carbon support price has boosted gas-fired generation, aided by the closure of a large proportion of coal-fired capacity. -

Future Prospects for LNG Demand in Ghana

January 2018 Future Prospects for LNG Demand in Ghana Energy demand in Africa is forecast to grow quickly in the coming decades, with the IEA suggesting1 a CAGR of 2 per cent between 2016 and 2040, twice the global average. However, it remains to be seen which fuel in a post-COP21 world will be used to achieve this economic growth. As electricity storage is not yet available (and could be initially expensive), Africa could use more coal, oil and/or gas to generate electricity (nuclear is not an option any longer as it is too expensive). With key lending institutions moving away from investment in coal and oil, this leaves a theoretical gap in the market for gas, which would avoid the need to import expensive energy storage technology. This would also help upstream companies to monetise domestic gas resources where a Final Investment Decision, without domestic demand, could be (permanently) postponed as we have seen in Mozambique in the last few years. But issues of affordability and security are higher up on any national African political agenda than the problem of carbon reduction (although in large cities, air quality considerations could provide a significant opportunity for gas). The cost of gas and the credit worthiness of African clients2 are major issues for investors. These two concerns should be looked at jointly: even with very high electricity prices3, sub-Saharan Africa has never paid more than $8.7/MMBtu (at the wholesale price level) for its gas according to the International Gas Union 4 . Hence only imported gas priced below this maximum level can meet the African challenge. -

Crude Oil Price Movements

OPEC Monthly Oil Market Report 11 July 2018 Feature article: Oil Market Outlook for 2019 Oil market highlights iii Feature article v Crude oil price movements 1 Commodity markets 8 World economy 11 World oil demand 31 World oil supply 44 Product markets and refinery operations 63 Tanker market 71 Oil trade 76 Stock movements 81 Balance of supply and demand 87 Organization of the Petroleum Exporting Countries Helferstorferstrasse 17, A-1010 Vienna, Austria E-mail: prid(at)opec.org Website: www.opec.org Welcome to the Republic of the Congo Welcome to the Republic of the Congo as the 15th OPEC Member The 174th Meeting of the Conference approved the request from the Republic of the Congo to join the Organization of the Petroleum Exporting Countries (OPEC), with immediate effect from 22nd June 2018. In line with this development, data for the Republic of the Congo is now included within the OPEC grouping. As a result, the figures for OPEC crude production, demand for OPEC crude and non-OPEC supply as well as the OPEC Reference Basket have been adjusted to reflect this change. For comparative purposes, related historical data has also been revised. OPEC Monthly Oil Market Report – July 2018 i Welcome the Republic of Congo ii OPEC Monthly Oil Market Report – July 2018 Oil Market Highlights Oil Market Highlights Crude Oil Price Movements The OPEC Reference Basket (ORB) eased by 1.2% month-on-month (m-o-m) in June to average $73.22/b. The ORB ended 1H18 higher at $68.43/b, up more than 36% since the start of the year. -

Nigeria Oil & External Exposure

The Business and Management Review, Volume 7 Number 3 April 2016 Nigeria oil & external exposure: the crude gains and crude pains of crude export dependence economy Augustine A. Ikein Niger Delta University/Federal University of Nigeria, Bayelsa , Nigeria **The Author expresses his gratitude to University Tetfund agency and to Sen. Diffa, Fomode and my dear wife Lily Ikein for their initiative and support. I also thank my students and colleagues in academia and Bayelsa State of Nigeria Keywords Nigeria oil, crude pains, Export, economy, OPEC, Nigeria Abstract This paper attempts to demonstrate that strategic raw material export dependency and external exposure is simply a reflection and extension of the structure of dependence propounded by Theotonio Dos Santos, 1970. By dependence we mean a situation in which the economy of certain countries is conditioned by the development and expansion of another economy to which the former is subjected. The concept of dependence permits us to see the internal situation of these countries as part of world economy. The working of dependency has its own pragmatic equivalence in the world energy market. It is the process of constituting a world economy that integrates “the national economies” in a world market of commodities, exchange system where the market participants are unequal because development of parts of the system occurs at the expense of less powerful nations who are mostly raw material exporters. The OPEC Cartel was formed to break the power of dominant forces that controlled the oil market scene as a body of concert power to which Nigeria is a member. The Cartel power was periodically successful and enjoyed high oil revenues and oil also became a weapon of choice to influence world geo-politics. -

Microbial Diversity of Petroleum Polluted Soil at Ayetoro Community in Ilaje Riverine Oil Producing Areas of Ondo State, Nigeria

Progress in Petrochemical Science CRIMSON PUBLISHERS C Wings to the Research ISSN 2637-8035 Research Article Microbial Diversity of Petroleum Polluted Soil at Ayetoro Community in Ilaje Riverine Oil Producing Areas of Ondo State, Nigeria Ajayi AO* and Abiola AK Department of Microbiology, Adekunle Ajasin University, Nigeria *Corresponding author: Ajayi AO, Department of Microbiology, Adekunle Ajasin University, Akungba-Akoko, Ondo State, Nigeria. Submission: April 24, 2018; Published: May 14, 2018 Abstract This study shows the potential of various types of bacterial isolates that utilizes hydrocarbon substrates which enhances the degradation of this pollutant in the environment. Soil samples used for this purpose were obtained from oil-producing Ayetoro community in Ilaje Local Government of Ondo State, Nigeria. Bacterial isolates were recovered by culturing them on nutrient agar and Mineral Salt Medium (MSM). Of the twenty two (22) includingbacterial isolates,Micrococcus thirteen luteus, (13) Bacillus were Gramcereus, positive Bacillus and subtilis, nine (9)Pseudomonas were Gram aeruginosa negative. The Gram positive bacteria were identified by Gram staining lightand biochemical crude oil by showingtests while visible the Gram growth negative around bacterial the oil in isolates MSM using were the identified hole-plate with diffusion the use method. of API® The identification study also showed kit. Five microbial (5) of thebacterial growth indicated species and Acinetobacterlwoffi exhibited potential to degradePseudomonas Bonny aeruginosa showed the highest optical density of 0.76-0.85 and has the greatest potential to degrade hydrocarbon. Thus, these oil-degrading properties ofby thevarying microorganisms turbidity on informed MSM broth the incorporated choice of this with group Bonny of organisms light oil withfor bioremediation optical density of range oil-polluted of 0.18-0.85 sites. -

Market Indicators As at End*: August-2020

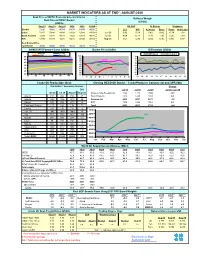

MARKET INDICATORS AS AT END*: AUGUST-2020 Spot Price of OPEC Basket & Selected Crudes Refiners' Margin Real Price of OPEC Basket (US$/b) (US$/b) Aug-18 Aug-19 Aug-20 2018 2019 2020# US Gulf N. Europe Singapore Basket 72.26 59.62 45.19 69.78 64.04 40.50 LLS WTI A. Heavy Brent Oman Arab Light Dubai 72.47 58.88 43.89 69.68 63.48 41.54 Jun-20 3.92 5.19 0.42 0.42 -0.74 1.02 North Sea Dtd 72.64 58.83 44.79 71.22 64.19 40.88 Jul-20 4.64 6.13 -1.86 1.30 1.26 1.99 WTI 67.99 54.84 42.36 65.16 57.02 38.15 Aug-20 3.67 5.30 -2.05 0.16 0.86 0.87 Real Basket Price Jun01=100 46.86 39.02 28.30 35.22 44.73 26.19 NYMEX WTI Forward Curve (US$/b) Basket Price (US$/b) Differentials (US$/b) May-20 Jun-20 WTI-Brent Brent-Dubai Jul-20 Aug-20 50 100 3 90 2 45 2018 80 1 70 40 0 60 35 2019 -1 50 30 40 -2 2020 -3 25 30 20 -4 20 10 -5 1M 3M 5M 7M 9M 11M J F M A M J J A S O N D 03 05 07 11 13 17 19 21 25 27 31 Crude Oil Production (tb/d) Closing OECD Oil Stocks - Crude/Products Commercial and SPR (Mb) Crude Oil Production (Tb/d) Production: Secondary Sources Change Diff. -

Oil and Security Policies

Oil and Security Policies <UN> International Comparative Social Studies Editor-in-Chief Mehdi P. Amineh (Amsterdam Institute for Social Science Research, University of Amsterdam, International Institute for Asian Studies, University of Leiden) Editorial Board Sjoerd Beugelsdijk (Radboud University, Nijmegen, The Netherlands) Simon Bromley (Open University, uk) Harald Fuhr (University of Potsdam, Germany) Gerd Junne (University of Amsterdam, The Netherlands) Kurt W. Radtke (International Institute for Asian Studies, The Netherlands) Ngo Tak-Wing (University of Leiden, The Netherlands) Mario Rutten (University of Amsterdam, The Netherlands) Advisory Board W.A. Arts (University College Utrecht, The Netherlands) G.C.M. Lieten (University of Amsterdam, The Netherlands) H.W. van Schendel (University of Amsterdam/International Institute of Social History, Amsterdam) L.A. Visano (York University, Canada) VOLUME 32 The titles published in this series are listed at brill.com/icss <UN> Oil and Security Policies Saudi Arabia, 1950–2012 By Islam Y. Qasem LEIDEN | BOSTON <UN> Cover illustration: © Ruletkka|Dreamstime.com. Library of Congress Cataloging-in-Publication Data Qasem, Islam Y., author. Oil and security policies : Saudi Arabia, 1950-2012 / by Islam Y. Qasem. pages cm. -- (International comparative social studies, ISSN 1568-4474 ; volume 32) Includes bibliographical references and index. ISBN 978-90-04-27774-8 (hardback : alk. paper) 1. Petroleum industry and trade--Political aspects--Saudi Arabia. 2. Energy consumption--Political aspects--Saudi Arabia. 3. Internal security--Saudi Arabia. 4. National security--Saudi Arabia. 5. Security, International--Saudi Arabia. 6. Saudi Arabia--Foreign relations. I. Title. HD9576.S32Q26 2015 338.2’72820953809045--dc23 2015028649 This publication has been typeset in the multilingual “Brill” typeface. -

Monthly Oil Market Report

Organization of the Petroleum Exporting Countries OMonthlyP Oil MEarket CReport March 2005 Feature Article: Relationship between commercial crude inventories and oil prices Oil Market Highlights 1 Feature Article 3 Outcome of the 135th Meeting of the Conference 5 Highlights of the world economy 7 Crude oil price movements 11 Product markets and refinery operations 15 The oil futures market 19 The tanker market 21 World oil demand 23 World oil supply 28 Rig count 31 Stock movements 32 Balance of supply and demand 34 Obere Donaustrasse 93, A-1020 Vienna, Austria Tel: +43 1 21112 Fax: +43 1 2164320 E-mail: [email protected] Web site: www.opec.org ____________________________________________________________________Monthly Oil Market Report Oil Market Highlights For the first time since the summer of 2004, Japan and Europe appear to have begun to share in the growth of the world economy. The outlook for Japan is particularly encouraging as both domestic and corporate demand look to have made a good start to 2005. The indications for Europe are more modest but early data for Germany, at least, suggest that improving investment demand and consumer spending should produce meaningful GDP growth in the first quarter. Nevertheless the main growth engines of the world economy remain the USA and China. US consumer and investment spending continued to grow strongly in February and the first quarter may see growth of about 4%. Data for China confirms a slight slowdown in the growth rates for retail sales in January and February but industrial production growth accelerated, rising to 16.9% year-on-year. There are risks on the sustainability of world economic growth in 2005. -

See Important Disclosures and Disclaimers at the End of This Report

August 15, 2017 Laura S. Engel, CPA [email protected] 214-987-4121 MARKET STATISTICS COMPANY DESCRIPTION Exchange / Symbol NYSE: ERN Erin Energy Corporation is an independent oil and gas exploration and production Price: $2.55 company, originally founded in 1986 as Camaroon-American Company (CAMAC). The Market Cap (mm): $544.6 Company has an asset portfolio of five licenses located in three countries in Africa, Enterprise Value (mm): $767.5 covering approximately 1.5 million acres. The Company’s asset portfolio includes Shares Outstanding (mm): 213.6 production and exploration projects in offshore Nigeria, exploration licenses in offshore Insider Ownership (%): Ghana, and offshore/onshore licenses in Kenya. In The Gambia, Erin Energy has 84% offshore licenses and a farm-out agreement with FAR Ltd. (AUX: FAR), an Australian- Volume (3 month avg.): 92,500 based oil and gas exploration company. Erin Energy Corporation trades on the New 52-week Range: $1.15 - $4.10 York Stock Exchange as well as the Johannesburg Stock Exchange under the ticker Industry: Oil and Gas symbol ERN and is headquartered in Houston, Texas, with 74 full-time employees, 32 of which were employed in the U.S. and 42 in Africa as of year-end 2016. CONDENSED BALANCE SHEET ($mm, except per share data, @ 6/30/17) Cash & Cash Equivalent: $10.7 SUMMARY Cash/Share: $0.05 Debt: $233.5 The next 6 -12 months should provide some important catalysts for Erin Energy. Equity (Book Value): ($349.2) • ERN’s current production is approximately 5,000 – 6,000 barrels of oil per Equity/Share: ($1.64) day from its Oyo-8 well; exploration and production are currently concentrated in the Oyo Field located in oil mining leases (OML) 120/121 blocks offshore CONDENSED INCOME STATEMENTS Nigeria.