Full Text (PDF)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2 | 12 Stamper the Magazine for High-Performance Punching Technology

2 | 12 Stamper The magazine for high-performance punching technology See you at EuroBLECH Innovative solutions BRUDERER precision for China 2012 from KLEINER GmbH BRUDERER will be presenting its newly- The company from Pforzheim in Germany Using a BSTA 1600-117, BBV 450 feed and ARKU peripheral developed BPG 22 planetary gearbox at supplies demanding customers with inno- devices, Shanghai Mint – a subsidiary of the state-run EuroBLECH. This technology enables the vative solutions and products while relying China Bank Note Printing and Minting Corporation (CBPM) high-performance BSTA 510 punching press on stamping technology from BRUDERER’s – stamps blanks for Chinese coins. The BRUDERER punch- to also be used for testing and running in high-performance punching presses. ing press is set up to ensure the ultimate in precision and tools. increased production levels. page 2 page 3 pages 4-5 Issue 02/2012 Issue 02/2012 editorial Looking forward to the euroBLeCH 2012 KLeINER GmBH – thinking in terms of solutions With the stamping world assembling at the Innovation, ultra-modern technologies and highly-motivated expert employees are the recipe for the EuroBLECH in Hanover from 23 – 27 October 2012, healthy growth that KLEINER GmbH company has continually achieved. Part of this success is also down to this will give the BRUDERER stand the opportunity strategic partnerships with customers and suppliers, and since the early 1990s, the Pforzheim-based com- to showcase the new BPG 22 planetary gearbox. pany in Germany has been relying for its stamping technology and toolmaking on Swiss-made BRUDERER The switchable gear can be adjusted by hand punching presses. -

Annual Report 2020 Central Bank of the Republic of China (Taiwan)

Annual Report 2020 Central Bank of the Republic of China (Taiwan) Taipei, Taiwan Republic of China Foreword Chin-Long Yang, Governor Looking back on 2020, it started with an outbreak of the coronavirus COVID-19 that quickly spread out and wreaked havoc on the global economy and world trade. Hampered by the resulting demand weakness both at home and abroad, Taiwan's economic growth slowed to 0.35% in the second quarter, the lowest since the second quarter of 2016. However, the pace picked up further and further in the latter half of the year amid economic reopening overseas and the introduction of consumption stimulus policies domestically. The annual growth rate of GDP reached 5.09% in the fourth quarter, the highest since the second quarter of 2011. For the year as a whole, the economy expanded by 3.11%, also higher than the past two years. Similarly, domestic inflation was affected by the pandemic as softer international demand for raw materials dragged down energy prices and hospitality services (such as travel and hotels) launched promotional price cuts. The annual growth rate of CPI dropped to -0.23%, the lowest since 2016, while that of the core CPI (excluding fruit, vegetables, and energy) fell to 0.35%, a record low unseen for more than a decade. Faced with the unusual challenges posed by pandemic-induced impacts on the economy and the labor market, the Bank reduced the policy rates by 25 basis points and rolled out a special accommodation facility worth NT$200 billion to help SMEs obtain funding in March, followed by an expansion of the facility to NT$300 billion in September. -

Protocol Amending the Agreement on Government Procurement

PROTOCOL AMENDING THE AGREEMENT ON GOVERNMENT PROCUREMENT PROTOCOLE PORTANT AMENDEMENT DE L'ACCORD SUR LES MARCHÉS PUBLICS PROTOCOLO POR EL QUE SE MODIFICA EL ACUERDO SOBRE CONTRATACIÓN PÚBLICA WORLD TRADE ORGANIZATION ORGANISATION MONDIALE DU COMMERCE ORGANIZACIÓN MUNDIAL DEL COMERCIO Geneva 30 March 2012 - 1 - PROTOCOL AMENDING THE AGREEMENT ON GOVERNMENT PROCUREMENT The Parties to the Agreement on Government Procurement, done at Marrakesh on 15 April 1994, (hereinafter referred to as "the 1994 Agreement"), Having undertaken further negotiations pursuant to Article XXIV:7(b) and (c) of the 1994 Agreement; Hereby agree as follows: 1. The Preamble, Articles I through XXIV, and Appendices to the 1994 Agreement shall be deleted and replaced by the provisions as set forth in the Annex hereto. 2. This Protocol shall be open for acceptance by the Parties to the 1994 Agreement. 3. This Protocol shall enter into force for those Parties to the 1994 Agreement that have deposited their respective instruments of acceptance of this Protocol, on the 30th day following such deposit by two thirds of the Parties to the 1994 Agreement. Thereafter this Protocol shall enter into force for each Party to the 1994 Agreement which has deposited its instrument of acceptance of this Protocol, on the 30th day following the date of such deposit. 4. This Protocol shall be deposited with the Director-General of the WTO, who shall promptly furnish to each Party to the 1994 Agreement a certified true copy of this Protocol, and a notification of each acceptance thereof. 5. This Protocol shall be registered in accordance with the provisions of Article 102 of the Charter of the United Nations. -

SINO-JAPANESE TRADE in the EARLY TOKUGAWA PERIOD By

SINO-JAPANESE TRADE IN THE EARLY TOKUGAWA PERIOD KANGO, COPPER, AND SHINPAI by YUN TANG B.A., Jilin University, 1982 M.A., Jilin University, 1985 A THESIS SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTERS OF ARTS in THE FACULTY OF GRADUATE STUDIES (Department of History) We accept this thesis as conforming to the required standard THE UNIVERSITY OF BRITISH COLUMBIA April 1995 ©Yun Tang, 1995 In presenting this thesis in partial fulfilment of the requirements for an advanced degree at the University of British Columbia, I agree that the Library shall make it freely available for reference and study. I further agree that permission for extensive copying of this thesis for scholarly purposes may be granted by the head of my department or by his or her representatives. It is understood that copying or publication of this thesis for financial gain shall not be allowed without my written permission. Department of The University of British Columbia Vancouver, Canada Date AoriLny?. ,MC DE-6 (2/88) ABSTRACT This thesis surveys Sino-Japanese relations in the early Tokugawa period with a specific focus on transactions in the major commodity--copper--between the two countries. The main purpose of the research is to investigate the bilateral contact in the early Tokugawa, the evolution of the copper trade, the political events involved with the trade, and to reexamine the significance of sakoku (seclusion) policy of Japan from a Chinese perspective. This thesis first explores the efforts of the shogunate from 1600 to 1625 towards reopening the kango or tally trade with China which had been suspended in the previous Muromachi period. -

Session B 1174

Islamic Coins All Arabic legends are somewhat stylized, with many misspellings and peculiarities. This is likely a Christian imitation, before the commencement of Christian Arabic dinars under Alfonso VIII in Session B 1174. The additional circle of beads around the obverse center is unique to this variety. Begins at 14:00 PDT on Thursday, May 19, 2016 Islamic Coins 406. IDRISID: ‘Abd al-Wahab, ca. 790s, AE fals (3.60g), Tahirt, ND, Spain & North Africa A-N430, the precise service of ‘Abd al-Wahab is unknown, but the relationship to the Idrisids is likely, light porosity, VF, RRR $200 - 300 Tahirt is the modern Tiaret in Algeria. A few examples of this type were found together with a few Abbasid fulus of Walila, as Lot 383 in this auction. 401. UMAYYAD OF SPAIN: ‘Abd al-Rahman I, 756-788, AR dirham (2.68g), al-Andalus, AH153, A-339, choice VF $100 - 120 407. AGHLABID: Ibrahim II, 874-902, AV dinar (4.18g), NM, AH268, A-447, al-’Ush-102, scarce variety for this year, citing the official Balâghi below obverse field, VF $240 - 300 408. AGHLABID: Ibrahim II, 874-902, AV dinar (4.20g), NM, AH281, 402. UMAYYAD OF SPAIN: ‘Abd al-Rahman I, 756-788, AR dirham A-447, well-centered, bold VF-EF $300 - 350 (2.65g), al-Andalus, AH165, A-339, superb strike, choice EF-AU $150 - 200 409. MIDRARID: al-Shakir, 933-958, AV dinar (4.13g), NM [Sijilmasa], AH337, A-453, lightly crinkled, VF-EF $300 - 350 403. UMAYYAD OF SPAIN: Hisham I, 788-796, AR dirham (2.62g), al-Andalus, AH175, A-340, small scratch on reverse, strong VF, R $130 - 170 410. -

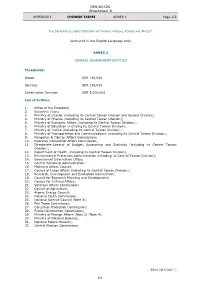

GPA/W/326 Attachment K K1

GPA/W/326 Attachment K APPENDIX I CHINESE TAIPEI ANNEX 1 Page 1/2 THE SEPARATE CUSTOMS TERRITORY OF TAIWAN, PENGHU, KINMEN AND MATSU* (Authentic in the English Language only) ANNEX 1 CENTRAL GOVERNMENT ENTITIES Thresholds: Goods SDR 130,000 Services SDR 130,000 Construction Services SDR 5,000,000 List of Entities: 1. Office of the President; 2. Executive Yuan; 3. Ministry of Interior (including its Central Taiwan Division and Second Division); 4. Ministry of Finance (including its Central Taiwan Division); 5. Ministry of Economic Affairs (including its Central Taiwan Division); 6. Ministry of Education (including its Central Taiwan Division); 7. Ministry of Justice (including its Central Taiwan Division); 8. Ministry of Transportation and Communications (including its Central Taiwan Division); 9. Mongolian & Tibetan Affairs Commission; 10. Overseas Compatriot Affairs Commission; 11. Directorate-General of Budget, Accounting and Statistics (including its Central Taiwan Division); 12. Department of Health (including its Central Taiwan Division); 13. Environmental Protection Administration (including its Central Taiwan Division); 14. Government Information Office; 15. Central Personnel Administration; 16. Mainland Affairs Council; 17. Council of Labor Affairs (including its Central Taiwan Division); 18. Research, Development and Evaluation Commission; 19. Council for Economic Planning and Development; 20. Council for Cultural Affairs; 21. Veterans Affairs Commission; 22. Council of Agriculture; 23. Atomic Energy Council; 24. National Youth Commission; 25. National Science Council (Note 3); 26. Fair Trade Commission; 27. Consumer Protection Commission; 28. Public Construction Commission; 29. Ministry of Foreign Affairs (Note 2) (Note 4); 30. Ministry of National Defense; 31. National Palace Museum; 32. Central Election Commission. … 2014 (WT/Let/…) K1 GPA/W/326 Attachment K APPENDIX I CHINESE TAIPEI ANNEX 1 Page 2/2 * In English only. -

Arms of Chinese Empire Provinces of China

Modern Dime Size Silver Coins of the World CHINA ====================================================================== ====================================================================== CHINA,Empire and Republic ====================================================================== Provinces of China China Mints striking Modern Silver Dime Size Coins ====================================================================== MINT (1) PROVINCE (2) REFERENCE (3) ANKING ANHWEI Y-42 CANTON KWANGTUNG Y-195, Y-200, Y-422, Y-425 CHANGSHA HUNAN Y-115 CHANGTU SZECHUAN Y-235, Y-240, Y-453 FOOCHOW FUKIEN Y-103, Y-326, Y-339, Y-380, Y-382, Y-388, Y-390 HANGCHOW CHEHKIANG Y-52, Y-371 KIRIN KIRIN (4) Y-180, Y-180A, Y-180C MUKDEN FENGTIEN (4) Y-84, Y-209 NANKING KIANGNAN (5) Y-142, Y-142A, Y-146 NANNING KWANGSI Y-414 (6) TAIPEH TAIWAN Y-247 TIENTSIN (7) CHIHLI (HOPEI) Y-12, Y-28, Y-62, Y-70, Y-334 WUCHANG HUPEH Y-124, Y-129 YUNNANFU YUNNAN Y-255 ====================================================================== (1) Mints which struck the 10 cents size only. FOOTNOTE: Since the middle of the thirteenth century China was (2) Other provinces: Shantung, Kweichow, Shansi, twice conquered by the foreigner; the Mongols in 1260 and the Shensi and Kansu. Manchus in 1644. The Manchus gave a stability and permanence (3) Modern World Coins, 11 Edition, R.S.Yeoman to the government. The head of the state was the Emperor, the (4) Manchuria, know as the Three Eastern Provinces: Sovereign by Divine right, the Son of Heaven. He was the Father Fengtien, Kirin and Heilungkiang (Since 1928 Jehol of the Nation. Succession passed in the male line to the Emperor’s was made a fourth Province). ablest rather than oldest son, not excluding the offspring of con- (5) A Region consisting of Kiangsu, Anhwei, Kiangsi. -

A Silver Transformation: Chinese Monetary Integration in Times of Political Disintegration During 1898–1933* Debin Ma and Liuyan Zhao

Economic History Working Papers No: 283 A Silver Transformation: Chinese Monetary Integration in Times of Political Disintegration during 1898-1933 Debin Ma and Liuyan Zhao LSE July 2018 Economic History Department, London School of Economics and Political Science, Houghton Street, London, WC2A 2AE, London, UK. T: +44 (0) 20 7955 7084. F: +44 (0) 20 7955 7730 A Silver Transformation: Chinese Monetary Integration in Times of Political Disintegration during 1898–1933* Debin Ma and Liuyan Zhao JEL Classification: E42, F15, N25 Key Words: Silver standard, Silver Point Arbitrage, Market Integration Abstract: This paper provides the first systematic econometric study on the evolution of Chinese silver exchange and monetary regimes during 1898–1933. Using high quality data sets of monthly and daily prices of silver dollars, we apply the threshold autoregressive models to estimate the silver points between Shanghai and other seventeen cities in Northern and Central China. We find a dramatic improvement in monetary integration from the 1910s, consolidated throughout the 1920s and 1930s to rival the global standard. We supplement our analysis with new data sets on volumes and costs of silver flows and with an in-depth historical narrative. Our paper revaluates the efficiency of the silver regime and China’s economic performance in the Republican era. 1. Introduction Whether the 1842 Sino-British Opium War and the forced opening of Qing China to Western imperialism and global trade marked the beginning of a century of Chinese humiliation or era of awakening to modernity may be a matter of perspectives. But the era of 1898–1933, covered in this study, saw China’s best and worst of times, straddling several sub-periods of a tumultuous era in modern Chinese history. -

Shanghai's Wartime Emergency Money

SHANGHAI'S WARTIME EMERGENCY MONEY John E. Sandrock This is the story of a little known aspect of China's wartime history and an oft neglected area of numismatics. The setting for our tale is the city of Shanghai and the time 1939. Dire things are about to happen, but before we can fully appreciate and understand them, a refresher course in Chinese currency might prove useful. For centuries the currency of China had consisted of a jumble of bank notes and coins issued by every conceivable authority - government, provincial and private. Most issues circulated only within limited areas (the province of issue) or, in the case of native banks, circulation was limited to the locale of the town or city of issue. On the lower end of the scale, notes of the myriad pawn shops and money- lenders were heavily discounted when presented only a few blocks away or were refused altogether! Many of these issues had little if any financial backing in the form of reserves - most depended solely on the reputation of the person printing and circulating the notes. This chaotic situation permitted the circulation side by side of notes and coins denominated in cash, cents, ch'uan, coppers, fen, and chiao much to the consternation of foreigners and to the detriment of commerce. Silver Dollars Steps had been taken in 1890 to modernize China's currency system which led to the introduction of the first steam operated press at Canton in Kwangtung province. The mint's initial task was to strike Chinese silver dollars to replace the tremendously popular Mexican dollars which had been imported into China to facilitate trade. -

THE STATE of CHINA's CITIES the STATE of CHINA's CITIES Global Action&China Practice:Together for a Better Future

THE STATE OF CHINA'S CITIES THE STATE THE STATE OF CHINA'S CITIES Global Action&China Practice:Together for a Better Future 2018/2019 Global Action&China Practice :Together for a Better Future Global Action&China Practice:Together for a Better Future 2018 2019 (35378)定价:108.00元 城市规划﹒城市设计(P20) 正式方案1.indd 2 2020/7/31 10:03:47 2018/2019 The State of China's Cities Global Action & China Practice: Together for a Better Future 审图号:GS(2020)2613号 图书在版编目(CIP)数据 中国城市状况报告 2018/2019: 全球行动与中国实践 :共创人类 美好未来 =The State of China’s Cities 2018/2019 Global Action & China Practice: Together for a Better Future :英文/ 国际欧亚科学院中国科学 中心,中国市长协会,中国城市规划学会编著 . —北京 : 中国建筑工 业出版社,2020.1 ISBN 978-7-112-24814-8 Ⅰ.①中… Ⅱ.①国… Ⅲ. ①城市建设—研究报告—中国— 2018-2019—英文 Ⅳ. ① TU984.2 中国版本图书馆CIP数据核字(2020)第022550号 The State of China's Cities 2018/2019 Global Action & China Practice: Together for a Better Future EDITED BY China Science Center of International Eurasian Academy of Sciences China Association of Mayors Urban Planning Society of China * 中国建筑工业出版社出版、发行(北京海淀三里河路9号) 各地新华书店、建筑书店经销 北京雅盈中佳图文设计公司制版 印刷厂印刷 * 开本: 787×1092毫米 1/16 印张: 字数: 千字 年 月第 1 版 年 月第 1 次印刷 定价: 108.00元 ISBN 978-7-112-24814-8 (35378) 版权所有 翻印必究 如有印装质量问题,可寄本社退换 ( 邮政编码 100037) EDITED BY China Science Center of International Eurasian Academy of Sciences China Association of Mayors Urban Planning Society of China 35378 The State of China's Cities (2018-2019).indd 9 2020/9/15 下午4:10 Foreword I City is the common home of human beings, and bright future of the city needs our creation together. -

Annual Report 2017 Central Bank of the Republic of China (Taiwan)

Annual Report 2017 Central Bank of the Republic of China (Taiwan) Taipei, Taiwan Republic of China Foreword Chin-Long Yang, Governor 2017 was a year of a steady global economic recovery and commodity price upswings, which combined to drive Taiwan's exports expansion as domestic consumer spending maintained moderate growth. Against this backdrop, Taiwan's economy grew at a faster pace of 2.86%, the highest annual growth rate in three years. Meanwhile, inflation was mild as NT dollar appreciation helped alleviate imported inflationary pressures and a weather-induced higher base effect held down food prices. Compared to the previous year, the consumer price index (CPI) rose by 0.62% and the core CPI (excluding vegetables, fruit, and energy prices) went up by 1.04%. While formulating this year's monetary policy, we have noted that the global economic outlook remains uncertain, the domestic economy is posting moderate growth, and the output gap is still negative. In addition, current inflationary pressures are subdued and inflation expectations are well anchored. Compared to several major economies, Taiwan's real interest rate also stands at an appropriate level. Based on these assessments, the Bank has held the policy rates unchanged during thecourseofyear2017,keepingmoneyand credit conditions adequate and accommodative to foster economic growth. We also conducted open market operations to adjust liquidity in the banking system. For the year as whole, bank credit and M2 increased by 4.79% and 3.75% year on year, indicating that market liquidity was sufficient to support economic activity. The Bank is dedicated to policy transparency. We recognize that ever-changing economic and financial conditions around the world have amplified public expectations for greater transparency at the central bank. -

Studies in Applied Economics

SAE./No.102/May 2018 Studies in Applied Economics INFLATION IN EASTERN CHINA DURING THE SECOND SINO-JAPANESE WAR Michell Li Johns Hopkins Institute for Applied Economics, Global Health, and Study of Business Enterprise Subsequently published in KSP Journals, December 2019 Inflation in Eastern China during the Second Sino-Japanese War By Michell Li Copyright 2017 by Michell Li. This work may be reproduced provided that no fee is charged and the original source is properly cited. About the Series The Studies in Applied Economics series is under the general direction of Professor Steve H. Hanke, Co-Director of The Johns Hopkins Institute for Applied Economics, Global Health and the Study of Business Enterprise ([email protected]). The authors are mainly students at The Johns Hopkins University in Baltimore. About the Author Michell Li ([email protected]) is a sophomore at The Johns Hopkins University in Baltimore pursuing a double major in International Studies and Economics. She wrote this paper as an undergraduate researcher at the Institute for Applied Economics, Global Health, and the Study of Business Enterprise in Fall 2017. She will graduate in May 2020. Abstract Although the history of the Japanese invasion of China is well-known and well-taught in China, the history of the currency war between China and Japan during the time is far less known. From 1937-1945, China and Japan engaged in not only a military war but also a "currency war." Japan, in an attempt to generate funds for the war from the war itself and to overthrow the Chinese government, attacked China's currency, the fabi (meaning “legal tender”), by printing counterfeit fabi notes and establishing “puppet” banks in China to issue mass amounts of puppet currencies to displace the fabi.