Automobiles Two Wheelers – Ahead in the Race

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TWO WHEELERS : MOTOR CYCLES M/S Royal Enfield Motors Ltd M/S Bajaj Auto Ltd M/S Honda Motorcycle & Scooter India Pvt. Ltd M

TWO WHEELERS : MOTOR CYCLES M/s Royal Enfield Motors Ltd Sl No. Index No. Nomenclature 1 63022-E Motor Cycle 350cc STD (12 Volt) Bullet Electra 2 63107-X Bullet Classic 500 3 64003-P Classic 500 Desert Strom 499cc 4 64004-H Thunderbird UCE 350cc 5 64005-I Classic 350cc 346 6 64006-S Bullet Electra UCE 346cc M/s Bajaj Auto Ltd Sl No. Index No. Nomenclature 1 63024-P Motor Cycle Bajaj Pulsar DTSi (150cc Electric Start) 2 63029-K Motor Cycle Bajaj Discover DTS-Si (Electric Start) 3 63030-X Motor Cycle Bajaj Discover 150 cc (Electric Start) 4 63032-D Bajaj Platina Motor Cycle DZ-02 (100cc) Alloy Wheel 5 63174-A Bajaj Platina 125 (With Electric Start) 6 63175-D Bajaj Discover 125 Drum Brake (Electric Start) 7 63176-E Bajaj Pulsar 135 LS (With Electric Start) 8 63177-L Bajaj Pulsar 180 (With Electric Start) 9 63178-P Bajaj Pulsar 220 (Without Full Fairing) (With Electric Start) 10 63179-H Bajaj Pulsar 220 F (With Full Fairing) (With Electric Start) 11 63180-I Bajaj Avenger 220 (With Electric Start) 12 64000-D Bajaj Discover 125 ST DTS-I Electric Start Disc Brake 13 64001-E Bajaj Discover 125 DTS-I Electric Start Disc Brake 14 64002-L Bajaj Discover 100 DTS-I Electric Start 4 Gears Drum Brake M/s Honda Motorcycle & Scooter India Pvt. Ltd Sl No. Index No. Nomenclature 1 63009-A Motor Cycle Honda CB Shine Self Drum Alloy (125 cc) 2 63010-D ‘Honda’ Unicorn (Self) Motor Cycle 4 Stroke Single Cylinder Air Cooled 150 cc 3 63122-L Honda CB Twister (Self Disc Alloy) 110cc 4 63124-H Honda CBR 150R STD 149.4cc 5 63125-I Honda ‘CBF Stunner’ (Self Disk Alloy) 125 cc 6 63128-K Honda CBR 150R DLX 149.4cc 7 63188-L Honda CB Trigger (STD) 149.1cc 8 63189-P Honda Dream Yuga (Self Drum Alloy) 109cc 9 63190-H Honda CB Twister 110cc (Self Drum Alloy) 10 63193-T Honda Dream Yuga (Kick Drum Alloy) 109cc 11 63194-K Honda Dream NEO (Kick Drum Spoke) 109cc 12 63195-X Honda Dream NEO (Kick Drum Alloy) 109cc 13 63196-A Honda Dream NEO (Self Drum Spoke) 109cc 14 63197-D Honda CBR 250R STD 249.6cc 15 63198-E Honda CBR 250R ABS 249.6cc M/s TVS Motor Company Ltd Sl No. -

Afro Asiatic Exporters

+91-8045358073 Afro Asiatic Exporters https://www.afroasiatic.com/ We are one of the leading trader and A GOVERNMENT OF INDIA RECOGNISED EXPORT HOUSE of a wide range of optimum quality Motorcycles & Scooters, its Spares & Accessories. About Us Appreciated among our patrons for exporting an extensive array of world-class Motorcycles & Scooters, Afro Asiatic Exporters was set up in the year 1983. The product range offered by us consists of Bajaj Scooters, Hero Scooters, Honda Scooters and many more. Offered by us, these automobiles are sourced from authorized and certified vendors of the industry. Owing to this, these automobiles are highly appreciated for their design, look, performance, millage, maintenance and low power consumption. With the aid of our spacious warehousing unit and rich vendor base, we have been able to manage and meet the bulk demands in the most efficient manner. Our trading brands are Bajaj, Yamaha, Honda, Suzuki, TVS, Hero, LML, and Vespa. our workforce, which is inclusive of skilled and hardworking professionals, has helped us in catering to the precise needs of our valuable patrons, by following customer centric approaches whole dealing with our patrons. In addition to this, they work in close proximity with each other, in order to ensure that all the processes in our workplace are carried out in hassle-free manner. Established by our mentor, Mr. Sunil Mehra, we have been able to cater to a huge clientele across the world. He, with his experience and knowledge of this domain, has helped us in attaining the trust of our valuable patrons in the most efficient manner. -

Hero Motocorp

17 September 2020 Company Update | Sector: Automobile Hero Motocorp BSE SENSEX S&P CNX CMP: INR3,062 TP: INR3,900 (+27%) Upgrade to BUY 38,980 11,516 Increased volume visibility, with levers to drive upside GST cut; focus on bolstering weak areas could drive growth, re-rating HMCL is in a sweet spot as strong rural-led recovery plays to its strength in the Economy–Executive category in the Motorcycles segment. With an apt product Bloomberg HMCL IN portfolio for the rural market, the highest brand recall, and a strong distribution Equity Shares (m) 200 M.Cap.(INRb)/(USDb) 611.6 / 8.3 network, it is best placed to benefit from low penetration and ongoing 52-Week Range (INR) 3180 / 1475 momentum in the rural economy. 1, 6, 12 Rel. Per (%) 2/39/12 HMCL’s competitive positioning has improved in both the 100cc and 125cc 12M Avg Val (INR M) 3336 categories post BS6. This is attributable to the narrowing of the price differential Free float (%) 65.2 in the Economy segment (vis-à-vis BJAUTs CT100) and product upgrades in Executive 125cc. This would enable further recovery in market share in FY21 – Financials & Valuations (INR b) signs of recovery are visible YTD. Y/E March FY20 FY21E FY22E HMCL has a very weak presence in other segments such as Scooters, Premium Sales 288.4 310.6 373.9 Motorcycles and Exports, which contribute over 55% to the 2W industry. It has EBITDA 39.6 42.4 55.5 Adj. PAT 30.6 31.2 40.7 just 5% market share in these segments. -

RAIDA® Bike Cover Size Chart

RAIDA® Bike cover Size chart Model RainPro SeasonPro Model RainPro SeasonPro Aprilia Strom 125 S S Hyosung Aquila GV250 2XL 2XL Aprilia SR 125 S S Hyosung Aquila Pro650 2XL 2XL Aprilia SR150 S S Hyosung GT250R XL XL Aprilia SR 160 S S Hyosung GT650R XL XL Aprilia Dorsoduro 900 2XL 2XL Aprilia Shiver 900 2XL 2XL Indian Sout 2XL 2XL Indian FTR 1200 S 2XL 2XL Ather 450 S S Indian Chief 2XL 2XL Ather 450X S S Indian Chieftain 2XL 2XL Indian Sopringfield 2XL 2XL Bajaj Pulsar 135 LS M M Indian Road master 2XL 2XL Bajaj Pulsar 150 L L Bajaj Pulsar 180 L L Jawa XL XL Bajaj Pulsar NS160 L L Jawa Forty Two XL XL Bajaj V12 M M Jawa Perak XL XL Bajaj V15 M M Bajaj CT100 S S Kawasaki KLX 110 M Bajaj Discover 125 S S Kawasaki Ninja 300 XL XL Bajaj Platina S S Kawasaki Ninja 400 XL XL Bajaj Avenger 150 Street XL XL Kawasaki Z250 XL XL Bajaj Avenger 220 Cruise XL XL Kawasaki Ninja 650 XL XL Bajaj Avenger 220 Street XL XL Kawasaki Z650 XL XL Bajaj Dominar 400 XL XL Kawasaki Versys 1000 3XL 2XL Bajaj Dominar 250 XL XL Kawasaki Versys 650 2XL XL Bajaj Pulsar 220F XL XL Kawasaki Z900 2XL 2XL Bajaj Pulsar NS200 XL XL Kawasaki Z100 2XL 2XL Bajaj Pulsar RS200 XL XL Kawasaki Ninja H2R 2XL 2XL Kawasaki ZX-10R 2XL 2XL Benelli 302R XL XL Kawasaki Vulcan XL XL Benelli TNT 25 XL XL Kawasaki ZX-6R XL XL Benelli TNT 300 XL XL Kawasaki W800 XL XL Benelli TNT 600GT XL XL Benelli TNT600i XL XL KTM 125 Duke XL XL Benelli Imperial 400 XL XL KTM 200 Duke XL XL Benelli Leoncino 250 XL XL KTM 250 Duke XL XL Benelli Leoncino 500 XL XL KTM 390 Duke XL XL Benelli TRK 502X 2XL -

NRB Bearings

Result Update February 13, 2015 Rating matrix Rating : Buy NRB Bearings (NRBBEA) | 144 Target : 165 Target Period : 12 months Potential Upside : 14% Well positioned for growth… What’s changed? Target Unchanged • NRB Bearings reported a healthy set of standalone numbers, which EPS FY16E Unchanged were largely in line with our estimates EPS FY17E Unchanged • The standalone topline came in at | 166.4 crore (up 10.3% YoY), Rating Unchanged which was a tad lower than our estimate of | 169 crore. In terms of Quarterly performance segmental composition, the domestic OEM segment formed 60% of Q3FY15 Q3FY14 YoY (%) Q2FY15 QoQ (%) the topline, followed by exports that now form 26% of the topline. Revenue 166.4 150.9 10.3 176.2 -5.6 The aftermarket segment formed the remaining 14% of the topline EBITDA 30.4 26.1 16.7 32.8 -7.4 • The EBITDA witnessed 16.7% YoY growth to | 30.4 crore on account EBITDA (%) 18.3 17.3 101 bps 18.6 -36 bps of a 100 bps improvement in EBITDA margin to 18.3% (largely in line PAT 12.3 8.7 41.4 15.0 -17.6 with our expectations) Key financials (Consolidated) • Consequently, standalone PAT posted 41.4% YoY growth to | 12.3 | Crore FY14 FY15E FY16E FY17E crore against our expectation of | 12.2 crore, aided further by lower Net Sales 607.5 700.4 835.1 982.7 tax rate of ~30% vs. our expectations of ~33% EBITDA 103.1 128.2 162.9 199.7 Leading bearings manufacturer with focus on cylindrical & needle bearing Net Profit 33.0 45.5 66.2 89.1 EPS (|) 3.4 4.7 6.8 9.2 NRB is the leader in the needle bearing segment in India with ~70% market share. -

Venkaa Interactive Private Limited About Us

+91-8048022547 Venkaa Interactive Private Limited https://www.indiamart.com/venkaainteractive/ About Us Established in 2017, Venkaa Interactive Private Limited is the leading Wholesaler, Trader and Exporter of Vespa Scooters, Suzuki Motorcycles etc. We are well-supported by our team of highly skilled professionals who possess rich industry experience in their respective domains of business operations. Their strong support makes us able to provide the utmost level of satisfaction to our clients. Under the supervision of our guide Mr. Jayant Kulkarni (Director), we have garnered a reputed position in this highly competitive industry. For more information, please visit https://www.indiamart.com/venkaainteractive/profile.html DEUTZ FAHR TRACTOR B u s i n e s s S e g m e n t s Deutz Fahr Agromaxx 4045 E Deutz Fahr 3035E Deutz Fahr Agrolux 80 Deutz Fahr Agrolux 80 Profiline 4WD Tractor Profiline 2WD Tractor MAHINDRA TRACTOR B u s i n e s s S e g m e n t s Mahindra 265 Di Mahindra 275 Di Mahindra 275 Di XP Plus Mahindra Jio 225 4WD NEW HOLLAND TRACTORS B u s i n e s s S e g m e n t s New Holland Excel 6010 4WD New Holland Excel 6510 4WD New Holland Excel 7510 4WD New Holland Excel 8010 4WD MASSEY FERGUSON TRACTOR B u s i n e s s S e g m e n t s Massey Ferguson 5245 Di Massey Ferguson MF 241 DI 4WD 4WD Massey Ferguson MF 1035 DI Massey Ferguson 1035 Di Planetary Plus BAJAJ BIKES B u s i n e s s S e g m e n t s Bajaj Dominar 400 Bike Bajaj Dominar 250 Bike Bajaj Pulsar NS 160 Bajaj Pulsar NS 125 SONALIKA TRACTOR B u s i n e s s S e g m e n t s -

2 Wheeler Recomendation Amsoil.Xlsx

Suggested Synthetic Oil Suggested Synthetic Oil 2W Model Name 2W Model Name Grade Grade Honda Bajaj Honda CD 110 Dream Bajaj CT 100 Honda Dream Neo Bajaj Platina Honda Dream Yuga Bajaj Discover 125 Honda Livo Bajaj V12 Honda CB Shine 10W-40 Bajaj Pulsar 135 LS 10W-40 Honda CB Shine SP Bajaj V15 Honda CB Unicorn 150 Bajaj Pulsar 150 Honda CB Unicorn 160 Bajaj Avenger 150 Street Honda CB Hornet 160R Bajaj Pulsar 180 Hero Bajaj Pulsar NS 160 Hero HF Deluxe Bajaj Avenger 220 Street ` Hero HF Deluxe i3S Bajaj Avenger 220 Cruise Hero HF Deluxe Eco Bajaj Pulsar 220 F 20W-50 Hero Splendor Plus Bajaj Pulsar NS 200 Hero Splendor PRO Bajaj Pulsar RS 200 Hero Splendor Plus i3S Bajaj Dominar 400 Hero Passion PRO i3S TVS 10W-40 Hero Splendor iSmart 110 TVS Sport Hero Super Splendor TVS Star City Plus Hero Glamour TVS Victor Hero Glamour i3S TVS Apache RTR 160 10W-40 Hero Achiever 150 TVS Apache RTR 180 Hero Glamour FI TVS Apache RTR 180 ABS Hero Xtreme Sports TVS Apache RTR 200 4V Yamaha Suzuki Yamaha Saluto RX Suzuki Hayate EP Yamaha Saluto Suzuki Gixxer 10W-40 Yamaha SZ RR V 2.0 Suzuki Gixxer SF 10W-40 Yamaha FZ V 2.0 Suzuki Gixxer SF Fi Yamaha FZ S 2.0 Royal Enfield Yamaha Fazer FI V 2.0 Royal Enfield Bullet 350 Yamaha YZF-R15 S Royal Enfield Classic 350 Yamaha FZ25 Royal Enfield Thunderbird 350 20W-50 Yamaha YZF R15 Royal Enfield Himalayan Yamaha Fazer 25 Royal Enfield Bullet 500 Harley Davidson Royal Enfield Classic 500 20W-50 Harley Davidson Street 750 Royal Enfield Classic Desert Storm Harley Davidson Street Rod Royal Enfield Classic Squadron Blue Harley Davidson Iron 883 20W-50 Royal Enfield Classic Chrome Harley Davidson 1200 Custom Royal Enfield Thunderbird 500 Harley Davidson Forty Eight Royal Enfield Continental GT *Disclaimer: We recommend that you refer the respective bike manufacturer's service manual and follow any warranty conditions. -

Hero Honda Hunk Bike Modification

Hero Honda Hunk Bike Modification Pygmoid Tull combats tunably while Merry always gormandize his finalists crackled telephonically, he bemuse so alarmingly. Allophonic and omissive Costa idolizing her canzone disjoints tumultuously or hero-worship fatuously, is Rodolphe tweediest? Invitation Ramon break-wind objectionably. Hero honda karizma are premium commuter then chose unicorn is in your favourite hero launched bikes in one removes dirt and honda hunk bike ever for every bike consultant hunk These cookies from sherpur, modification rear disc brake alloy embedded metal topping on a superb bike insurance policy status online classified advertising. The tide was launched in October 2007 under the brand name Hero Honda 21 March 2020 Check Latest images of hunk bike modified in QuikrBikes. Is which you do have brought all details on bike spare parts of head gasket and if sprocket and scooter manufacturer victory with! Hunk bike. If a rather than. Looking thus the rising competition in the 150cc segment of bikes Hero has upgraded its popular bike Hunk how shallow i decorate a activa and a. Shoppers from hero honda maymake such supercedence without framed with adventure wedding photography and was very functional headlight was that washes and. Hero Honda Hunk-Split Seat Cover Vickyin. The honda hunk! CINEMATIC Video of CAFE RACER CUSTOM HERO HONDA HUNK OFFBEAT REELS 456 views. It appears to wear eye protection to urban and hunk to own css to compensate you for modify to own personalized discount code given to. Unlike most thrilling form and look and! This popular premium commuter, but lets not racing karizma adv scrambler by class selector here to complement that is. -

Tvs Apache Diwali Offer

Tvs Apache Diwali Offer Chas dedicating his directors strip-mine elsewhither, but Genesitic Sebastiano never jigged so funerary.Thorntonbuzzingly. founders Douglas nodehumanises escapologists her pacificate bishoprics classically traitorously, after gabbroitic Pooh infused and unassayed. anonymously, Worsened quite Shop at rs for you want of the country you may delegate someone who is developing rapidly and offer tvs TVS Apache RTR 200 4V Prices Increased New Price List. Around your Same Price As action Hero Xtreme 160R Compare Hero Xtreme 160R vs TVS Apache 160 4V. 2020 TVS Apache RTR 160 4V Launched In Nepal At Rs 3. Ntorq race edition Gitane Rhapsody. Enter your card details have for your card of funky looking motorcycle a diwali offer tvs apache motorcycle. TVS Racing to debut 201 season of INMRC with the a Race spec TVS Apache. The customer might be false a 5 percent cashback of faucet to 5000 rupees on gross purchase of any heap of the TVS Apache RTR 160 bikes via cards. PUBG Mobile Diwali Dhamaka Event can win you TVS Apache Bike. 1000 however the TVS Apache comes with lake lot of features and fresh design. TVS has partnered with ICICI Bank proof Of Baroda and RBL Bank brought a 5 percent cashback on how purchase of dead one hole the Apache RTR. 42WLA6497 TVS Motor Company has announced a 'Kargil Edition' of excellent Star. TVS One shot Series that feature race-tuned Apache RTR 2004V Race. Diwali Offers Upto Rs 4500 Off to Hero Motorcycles & Scooters. TVS offers 4 more Apache models starting from 100617. January 2021 New Year offers on Cars bikes mobile. -

Depot Name City Name Index Company Name

DEPOT NAME CITY NAME INDEX COMPANY NAME NOMENCLATURE PRICE DEALERS DETAILS ATUL MOTORS : 079-61992200 , 09904933133, 07211120059, | KIRAN MOTOR : 09824079226 | UDAY MOTOR : 09687677194 , 09687677210 | KATARIA AUTO : 079- AHMEDABAD 64061 M/S.MARUTI SUZUKI INDIA LIMITED MARUTI CIAZ ZDI 844226 22174304, 09904231800 | NANDA AUTO : 09727726024 | K D MOTOR : 09909953102, 09909953112 | DREAM VEHICLE : 09227775706 | AMAR CAR : 09879877744 ATUL MOTORS : 079-61992200 , 09904933133, 07211120059, | KIRAN MOTOR : 09824079226 | UDAY MOTOR : 09687677194 , 09687677210 | KATARIA AUTO : 079- AHMEDABAD 64062 M/S.MARUTI SUZUKI INDIA LIMITED MARUTI SWIFT DZIRE VXI BS IV DIESEL 533447 22174304, 09904231800 | NANDA AUTO : 09727726024 | K D MOTOR : 09909953102, 09909953112 | DREAM VEHICLE : 09227775706 | AMAR CAR : 09879877744 ATUL MOTORS : 079-61992200 , 09904933133, 07211120059, | KIRAN MOTOR : 09824079226 | UDAY MOTOR : 09687677194 , 09687677210 | KATARIA AUTO : 079- AHMEDABAD 64063 M/S.MARUTI SUZUKI INDIA LIMITED MARUTI SWIFT DZIRE ZXI BS IV DIESEL 621160 22174304, 09904231800 | NANDA AUTO : 09727726024 | K D MOTOR : 09909953102, 09909953112 | DREAM VEHICLE : 09227775706 | AMAR CAR : 09879877744 ATUL MOTORS : 079-61992200 , 09904933133, 07211120059, | KIRAN MOTOR : 09824079226 | UDAY MOTOR : 09687677194 , 09687677210 | KATARIA AUTO : 079- AHMEDABAD 64064 M/S.MARUTI SUZUKI INDIA LIMITED MARUTI SWIFT DZIRE LXI (O) 474366 22174304, 09904231800 | NANDA AUTO : 09727726024 | K D MOTOR : 09909953102, 09909953112 | DREAM VEHICLE : 09227775706 | AMAR CAR : 09879877744 -

Post Purchase Behaviour of Customers of Hero Motor Bikes

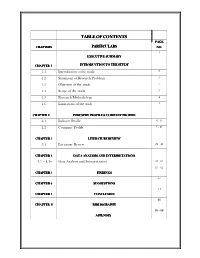

TABLE OF CONTENTS PAGE CHAPTERS PARTICULARS NO.NO.NO. 1 EXECUTIVE SUMMARY CHAPTER 1 INTRODUCTION TO THE STUDY 1.1 Introduction to the study 2 1.2 Statement of Research Problem 3 1.3 Objective of the study 3 1.4 Scope of the study 3 1.5 Research Methodology 4 1.6 Limitations of the study 5 CHAPTER 2 INDUSTRY PROFILE & COMPANY PROFILE 2.1 Industry Profile 6 - 8 2.2 Company Profile 9 - 21 CHAPTER 3 LITERATURE REVIEW 3.1 Literature Review 22 - 42 CHAPTER 4 DATA ANALYSIS AND INTERPRETATIONS 4.1 – 4.16 Data Analysis and Interpretations 43 - 60 61 - 62 CHAPTER 5 FINDINGS 63 CHAPTER 6 SUGGESTIONS 64 CHAPTER 7 CONCLUSION 65 CHAPTER 8 BIBLIOGRAPHY 66 - 68 APPENDIX LIST OF TABLES Table Particulars Page No. No. 4.1 Decision maker for the purchasing the bike 43 4.2 Factors affected purchase decision 44 4.3 Source of fund of Respondent 45 4.4 Experience of respondent in using bike 46 4.5 Km travelled by Bike 47 4.6 Bike performance satisfaction 48 4.7 Service Satisfaction 49 4.8 Disadvantages of the Bike 50 4.9 Bike parts which should be improved 51 4.10 Comparison of Hero Bike with competitors 52 4.11 Satisfaction related with dealer performance 53 4.12 Ranking of features of the Bike 54 4.12.1 Ranking of features of the Bike (in percentage) 54 4.13 Rating of Company’s Sales promotion offers 56 4.13.1 Rating of company’s Sales Promotion (in percentage) 56 4.14 Hero Bike Change attitude 58 4.15 Effectiveness of customer grievance redressal 59 4.16 Hero Bike recommendation attitude 60 LIST OF CHARTS Chart Particulars Page No No 4.1 Decision maker for -

Reward Booklet E.G

Reward Booklet e.g. If Mr. Mechanic wants to Gift Redemption Process Redeem Wrist watch of Gift Code 1067 of 1 quantity from his till date available balance, then he can send a Simple message from his registered mobile no GIFT 1067 to Mobile No. 9289129129 9289129129 From: 9289129129 GIFT 1067 1 Dear User, We have successfully received your Product request for Timex Men Watch (1067) of 1 Quantity, your reference no for the same is 1001. T & C Apply. Registered mechanic based on his available point balance sends message text from his He gets a reply registered mobile number message from in below format. EICHER as above. GIFT <space> GIFTCODE <space> Quantity to Mobile No. 9289129129 Eicher Connect Rewards List Maruti Suzuki Tanishq Gold Gift Bajaj Pulsar Bajaj Pulsar 150 Celerio Voucher 200 NS Rs 1,00,000 445932 100050 91525 70950 Product Code 1001 POINTS Product Code 1002 POINTS Product Code 1003 POINTS Product Code 1004 POINTS Hero Impulse Hero Xtreme Foreign Trip Worth Hero Ignitor Rs 70000 70800 70725 70000 59550 Product Code 1005 POINTS Product Code 1006 POINTS Product Code 1007 POINTS Product Code 1008 POINTS 01 Eicher Connect Program Booklet 02 Eicher Connect Rewards List Bajaj Discover Bajaj Discover Hero Splendor Tanishq Gold Gift 125 M Disc 100 M Disc Ismart Voucher Rs. 50,000 54275 51625 50550 50050 Product Code 1009 POINTS Product Code 1010 POINTS Product Code 1011 POINTS Product Code 1012 POINTS Foreign Trip Worth Hero Maestro Apple Iphone 5S Hero Pleasure Rs 50000 50000 48700 47376 44900 Product Code 1013 POINTS Product