Marston's Off Trade Beer Report 2019/20

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

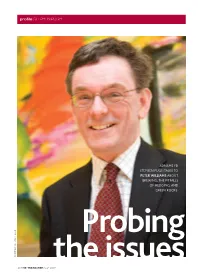

Profile STEPHEN PUGH ADNAMS

PHOTOGRAPHER: ROGER HARRIS 20 profile THE TREASURER STEPHEN PUGH MAY 2007 MAY the issues Probing STEPHEN PETER WILLIAMS BREWING, THE PITFALLS OF HEDGING, AND OF HEDGING, PUGH GREEN R ADNAMS FD T ALKS ABOUT OOF T O S. profile STEPHEN PUGH tephen Pugh has been restructurings, gearing up and Finance Director at A taste of Adnams securitising debt and heavily Adnams for three and a leveraging their pub estate. A traditional brewer of classic English beer, Adnams has been in business half years. He joined the Inevitably, this has been partly for more than 130 years. With a turnover of £45m a year, based in the Scompany as a result of lunch with driven by private equity-type coastal resort of Southwold in Suffolk, the company owns around 80 pubs, a former colleague who told Pugh interest with, for instance, he had seen his next job mostly in East Anglia, as well as a couple of hotels in Southwold. A regional property tycoon Robert Tchenguiz advertised in The Financial Times. brewer, Adnams also has a long-established and thriving wine business, stalking Mitchells & Butlers. And Although he wasn’t looking to and recently opened a handful of cellar and kitchen stores. within the industry itself there is move, at 35 miles away the With more than 300 employees, Adnams has an important presence in hot discussion about whether or company was nearer Pugh’s the local economy. Finance Director Stephen Pugh says: “We are well when some brewers will turn Ipswich home. thought of in the local community and we work hard to ensure that view themselves into real estate “I wasn’t looking to move but I remains the case.” investment trusts (REITS). -

Brewers Toast the Return of Real Ale - FT.Com Page 1 of 1

Brewers toast the return of real ale - FT.com Page 1 of 1 FINANCIAL TIMES September 4,20128:10 pm Brewers toast the return of real ale By Christopher Thompson On a weekday evening at the Rake in London's Borough Market the assembled drinkers - a mix of hipsters and suited local businessmen - are not supping Foster's, Stella Artois or any of the other mass market lager brands. Since opening in 2006, the Rake has only sold craft beers, of which it offers 130 different types. Despite typically charging more than £4 for a pint or a bottle, co-owner Richard Dinwoodie, 45, says the pub has registered year-on-year sales growth since it opened. "Our popularity is on the back of the foodie revolution, where people are more interested in taste ... we've also seen big growth in supplying restaurants and hotels, [some of whom] have beer menus and even a beer sommelier," he says. The Rake's success reflects a broader movement of beer drinkers towards cask ale and craft beers as Britain's overall beer market declines. In 2011 total beer sales were £17bn, of which ale accounted for £3.7bn, according to the British Beer and Pub Association. Last month Heineken, the maker of the eponymous lager and Kronenbourg brand, reported a fall in volumes in western Europe, including the UK, in the first half of 2012. It follows a long decline in UK lager sales, which have fallen by more than a fifth over the past five years. In contrast, cask ales sales have declined at less than half that rate, with many companies even registering sales increases. -

Classic Cocktails Gin Cocktails Vodka Cocktails

CLASSIC COCKTAILS VODKA COCKTAILS SPIRITS PORN STAR MARTINI Absolut vanilla, Passoa, Passion Fruit THE LIVERPOOL, Liverpool vodka, infused blackberries, VODKAS served with a shot of Adnams Prosecco on the side £10.75 lemon wedges, Fevertree lemon tonic £11.60 Absolut flavours £3.70 JJ Whitley £3.70 STRAWBERRY & PASSION FRUIT MARTINI Absolut vodka, RAZBERI FIZZ, Stoli Razberi, lime wedges, cherries, fevertree Absolut blue £3.50 Rhubarb strawberry puree, passion fruit, lime, apple juice £9.75 lemonade - it’s sooo tasty! £10.10 Adnams £4.30 Liverpool £5.00 ESPRESSO MARTINI Espresso, Kahlua, Absolut vanilla BLACK COW VODKA, (made from milk) cinnamon, vanilla, Belvedere £5.00 Stoli Razberi £4.30 vodka, coffee beans £9.50 lime, lime wedges, fevertree soda £12.60 Black Cow £5.50 Wybrorowa £3.60 FRENCH MARTINI Absolut vanilla vodka, Chambord, ADNAMS EAST COAST, Adnams east coast vodka, mint Grey Goose £5.65 pineapple juice £9 leaves, cucumber, Fevertree lemonade £10.60 BAKEWELL TART Amaretto, Chambord, cranberry juice RHUBARB TWIST, JJ Whitley rhubarb vodka, lemon , GIN £8.75 Fevertree lemonade £9.60 Adnams £4.30 Ely Gin Company £4.45 BULL INN KISS Amaretto, Strawberry Liqueur, Prosecco ORANGE SPLASH, Absolut mandarin, fresh orange slices, Bombay £3.45 Edgerton Pink £5.50 £8.75 Fevertree lemonade £9.10 Hendricks £4.30 Edgerton Blue £5.50 GINGERBREAD DAIQUIRI Havana club rum, gingerbread, CITRON CHILLER, Absolut citron, lemon, lime, orange, Pinkster £5.30 The Botanist £5.35 lime £8.50 Fevertree lemon tonic £9.10 Saffron gin £4.90 Mombassa £5.25 -

GUEST ALE Exmoor Brewery, Somerset

BRAINS THE REV JAMES ORIGINAL 4.5% ABV KELHAM ISLAND PALE RIDER 5.2% ABV Brains Brewery, Cardiff. Est. 1882 Kelham Island Brewery, South Yorkshire. Est. 1990 ALL ALES AVAILABLE ON This mahogany-coloured beer is rich and well balanced, with a mellow, This golden-coloured, award-winning beer is brewed using a blend of the finest malts malty flavour which unexpectedly gives way to a clean, refreshing finish. and American hops, resulting in a fresh citrus nose, ample hints of fruit and a smooth, Hops: Challenger, Fuggles Allergens: barley (GLUTEN) refreshing juicy malt character. THE WETHERSPOON APP real ales Hops: Cascade, Citra, Columbus, Willamette Allergens: barley (GLUTEN), wheat (GLUTEN) EXMOOR GOLD 4.5% ABV THEAKSTON OLD PECULIER 5.6% ABV GUEST ALE Exmoor Brewery, Somerset. Est. 1980 This classic golden ale has a juicy malt aroma, with hints of citrus hops Theakston Brewery, North Yorkshire. Est. 1827 and vanilla, while the subtle malt sweetness in its flavour leads to a refreshing, This dark ruby beer is one of the world’s classic beers. It has a rich, full-bodied flavour, bittersweet finish of citrus, toffee and vanilla. with subtle cherry and rich fruit overtones, plus a smooth, lasting finish. available Hops: Challenger, Fuggles, Target Allergens: barley (GLUTEN), wheat (GLUTEN) Hops: Celeia, Challenger, Fuggles, Goldings Allergens: barley (GLUTEN) MORLAND OLD SPECKLED HEN 4.5% ABV MARSTON’S OLD EMPIRE IPA 5.7% ABV TASTING Greene King Brewery, Suffolk. Est. 1799 Marston’s Brewery, Staffordshire. Est. 1834 This amber-coloured beer has a superb fruity aroma, with its warming malt and toffee This golden beer is brewed in the style of a traditional IPA, with plenty of crisp citrus hop all year character balanced by fruity notes and a subtle bitterness, leading to a refreshing, dry finish. -

English and Welsh Whisky Trail

WHISKY TRAIL DESTINATIONS Dunstanburgh Castle 1 ABER FALLS DISTILLERY Llanfairfechan 10 DARTMOOR WHISKY DISTILLERY Newton Abbot ENGLISH AND Aber Falls Distillery sits at the foot of the famous Aber Falls waterfall. Previously a slate Production of Dartmoor Whisky began in 2016, after a group of whisky enthusiasts visited WELSH WHISKY works in the 19th century, a margarine factory during the world wars, and more recently a Islay in Scotland and came back determined to make whisky in Devon. The climate, soil, drinks wholesaler depot, the distillery has been lovingly restored. Dartmoor spring water and sea breeze are all ideal for producing whisky. TRAIL Address: Station Road, Abergwyngregyn, North Wales, LL33 0LB Address: The Town Hall, Bovey Tracey, Devon TQ13 9AA Web: www.aberfallsdistillery.com Web: www.dartmoorwhiskydistillery.co.uk Durham Cathedral Open: 12 noon - 4pm Thursday to Sunday. Open: Open 7 days a week, with tours starting at 11am and 3pm. The Lake District 2 ADNAMS COPPER HOUSE DISTILLERY Southwold 11 DURHAM DISTILLERY Durham 11 10 1616 Best-known as a brewer of beer in the coastal town of Southwold in Suffolk, Adnams Founded in 2014, Durham Distillery initially produced Durham Gin, and will be producing produce award-winning spirits using locally-sourced grains that are found in their beers, in the North-East’s first single malt whisky in late-2018 when the move to a new state-of- the Copper House Distillery, which opened in 2010. the-art distillery in Durham city centre is complete. Address: The Sole Bay Brewery, Southwold, Suffolk, IP18 6JW Addresses: 2F & 2G Riverside Industrial Estate, Langley Park, Durham DH7 9TT. -

Ipswich Town V Wycombe Wanderers Tuesday 26

IPSWICH TOWN V WYCOMBE WANDERERS TUESDAY 26 NOVEMBER 2019, KICK OFF 19:45 INFORMATION FOR AWAY FANS Information in this guide is correct as at 25 November. Welcome to Ipswich! This is a short guide, designed to answer the kind of questions that we often get from visiting fans, and provide the information that we find useful when we’re travelling away ourselves. For any further information, or if you have any feedback on our guide, please contact Elizabeth Edwards, Supporter Liaison Officer, on [email protected] or 07968 876504 or via Twitter on @ITFC_SLO. IPSWICH TOWN FOOTBALL CLUB Address: Ipswich Town Football Club, Portman Road, Ipswich, IP12DA Website: www.itfc.co.uk Club Telephone Number: 01473 400 500 Ticket Office Number: 03330 05 05 03 Supporter Liaison Officer: Elizabeth Edwards, [email protected], 07968 876504, @ITFC_SLO Disability Liaison Officer: Lee Smith, [email protected] 01473 400556 Customer Services: [email protected] Twitter: @IpswichTown IF YOU HAVE AN HOUR OR TWO PRE-MATCH IN IPSWICH The stadium is just a short, 5-10 minute, walk to the town centre, with shops, cafes and restaurants. The waterfront area is around a 15-minute walk from the ground, with a yachting marina and a range of cafes and restaurants. Note that the designated away pub is the Station Hotel (details below). Many pubs and bars in the town centre are strictly home fans only (more info below), whilst others are more relaxed – this does vary from match to match though. A number of pubs around the town will welcome small numbers of away fans, especially those looking for a chat and a quiet pint. -

2015 BJCP Beer Style Guidelines

BEER JUDGE CERTIFICATION PROGRAM 2015 STYLE GUIDELINES Beer Style Guidelines Copyright © 2015, BJCP, Inc. The BJCP grants the right to make copies for use in BJCP-sanctioned competitions or for educational/judge training purposes. All other rights reserved. Updates available at www.bjcp.org. Edited by Gordon Strong with Kristen England Past Guideline Analysis: Don Blake, Agatha Feltus, Tom Fitzpatrick, Mark Linsner, Jamil Zainasheff New Style Contributions: Drew Beechum, Craig Belanger, Dibbs Harting, Antony Hayes, Ben Jankowski, Andew Korty, Larry Nadeau, William Shawn Scott, Ron Smith, Lachlan Strong, Peter Symons, Michael Tonsmeire, Mike Winnie, Tony Wheeler Review and Commentary: Ray Daniels, Roger Deschner, Rick Garvin, Jan Grmela, Bob Hall, Stan Hieronymus, Marek Mahut, Ron Pattinson, Steve Piatz, Evan Rail, Nathan Smith,Petra and Michal Vřes Final Review: Brian Eichhorn, Agatha Feltus, Dennis Mitchell, Michael Wilcox TABLE OF CONTENTS 5B. Kölsch ...................................................................... 8 INTRODUCTION TO THE 2015 GUIDELINES............................. IV 5C. German Helles Exportbier ...................................... 9 Styles and Categories .................................................... iv 5D. German Pils ............................................................ 9 Naming of Styles and Categories ................................. iv Using the Style Guidelines ............................................ v 6. AMBER MALTY EUROPEAN LAGER .................................... 10 Format of a -

The Brewing Industry

Strategy for the Historic Industrial Environment The Brewing Industry A report by the Brewery History Society for English Heritage February 2010 Front cover: Detail of stained glass window in the Millennium Brewhouse, Shepherd Neame Brewery, Faversham, Kent. Design, showing elements of the brewing process, by Keith and Judy Hill of Staplehurst. Strategy for the Historic Industrial Environment The Brewing Industry A report by the Brewery History Society for English Heritage February 2010 Text by Lynn Pearson Brewery History Society, 102 Ayelands, New Ash Green, Longfield, Kent DA3 8JW www.breweryhistory.com Foreword The Brewery History Society (BHS) was founded in 1972 to promote research into all aspects of the brewing industry, to encourage the interchange of information about breweries and brewing, and to collect photographic and other archive information about brewery history. The Society publishes a Newsletter and a quarterly journal Brewery History, which first appeared in 1972. It has also published a national directory and a series of county-wide surveys of historic breweries; the Society’s archive is held by Birmingham Central Library. Further details of BHS activities may be found at <http://www.breweryhistory.com>. The ongoing threat to the historic fabric of the English brewing industry was discussed at the conference From Grain to Glass, organised jointly by English Heritage (EH), the BHS and the Association for Industrial Archaeology (AIA), which took place at Swindon on 13 June 2003; the joint BHS and Victorian Society study day From Hop to Hostelry: the brewing and licensed trades 1837 -1914 (Young’s Ram Brewery, Wandsworth, 25 February 2006); and during the AIA Ironbridge Working Weekend (Coalbrookdale, 29 April 2006). -

The Olde English Pub & Pantry

THE OLDE ENGLISH PUB & PANTRY S U N D A Y B R U N C H S O U P S & S A L A D S FRENCH ONION SOUP ENGLISH GARDEN SALAD Caramelized onions, beef jus, Fresh greens, tomatoes, carrots, croutons, Gruyère cheese, served with English cucumber, radish, hardboiled a toasted roll $8 egg, walnuts, honey mustard vinaigrette $16 TOMATO BISQUE Rich bisque, parmesan crisps, garlic SPINACH AND APPLE SALAD toast $8 Local spinach, apples, candied walnuts, pickled onions, balsamic vinaigrette $15 S a l a d a d d o n s : C h i c k e n B r e a s t $ 4 , S a l m o n C a k e $ 8 , S h r i m p $ 8 , T o f u $ 7 S T A R T E R S GREEK YOGURT PARFAIT CIDER DONUT HOLES Greek yogurt, honey, seasonal fruit $9 Fried house-made donut holes rolled in sugar $9 DANISHES Assorted pastries, selection rotating SAUSAGE ROLLS weekly $6 Seasoned sausage wrapped in puff pastry, pub mustard $11 DIPPING FRIES Garlic truffle salt seasoned fries, Pub ENGLISH SALMON CAKES Mustard, Malted Ranch, Chipotle Aioli, Faroe Island salmon, potatoes, dill, Garlic Aioli $10 mustard, scallions, small salad, honey mustard vinaigrette $17 B R U N C H FULL ENGLISH BREAKFAST Two sunny side eggs, baked beans, sausage, toast, mushrooms, roasted tomatoes $15 BERRY FRENCH TOAST MORNING GYRO Sourdough French toast, berry Gyro meat, scrambled eggs, tzatziki, compote, whipped cream, homefries, lettuce, tomatoes, red onions, and fresh fruit $14 homefries $15 STEAK AND EGGS THE PUB BREAKFAST PLATE Two eggs (of your choice), two steak Two eggs, chips, gravy, bangers, toast medallions, caramelized onions, $14 -

Lessislow ALCOHOL & GLUTEN FREE BEERS

Less More!LOWis ALCOHOL & GLUTEN FREE BEERS THE ORIGINAL SMALL BEER Back in the 1700's when drinking water could be fatal, small beer was a staple of British daily life. Enjoyed in work places and schools across the country, it was traditionally brewed between 0.5%-2.8% ABV. In a world where consumers are looking for a low alcohol product, Small Beer is a perfect alternative maximising the flavour with no loss of quality, drawing on the past for recipe inspiration. ORIGINAL SMALL BEER Low Alcohol & Low LAGER SMA001 24x35cl | 2.1% | £40.31 There can be no dispute over the demand for low or non-alcoholic drinks ORIGINAL SMALL BEER Gluten Free Beers DARK LAGER these days. Whether it’s a short-term abstinence, or a lifestyle choice, every bar Alcohol SMA002 in the trade needs to tackle the subject. 24x35cl | 1.0% | £42.36 It seems beer and ciders are leading the way in terms of choice and experimentation — the craft beer revolution has certainly produced brewers with expert skills who are embracing this issue with the same curiosity and creativity as standard alcoholic lines. The results are getting better and better and for the consumer it means not only an end to the potential stigma of not drinking socially, but wider choice and taste ranges. •Did In the UKyou an alcohol-free know... drink must be 0.05% ABV or below. The future certainly looks bright for this category with annual growth of these • Any beer produced outside of the UK products making it worth every brewer’s while to explore what’s possible, but inside Europe can be classed as alcohol free if under 0.5% ABV. -

Pints of View the Bi -Monthly Publication for Every Discerning Drinker December/January 2010 Circulation 8000 No

www.hertsale.org.uk www.watfordcamra.org.uk www.heb-camra.org.uk www.camranorthherts.org.uk HERTFORDSHIRE’S Pints of View The bi -monthly publication for every discerning drinker December/January 2010 Circulation 8000 No. 238 Our seasonal pub above for this edition is the Chequers in Barley (near Royston). This Greene King pub serves IPA and Abbot , with Old Speckled Hen also being available over Xmas and New Year. Home cooked food is also served. More on page 25 Also in this issue: The Woodman The Third Annual The Liberty Hops to it Bucks the Trend Sawbridgeworth Beer Festival 1 Pub Sector 'ties' Cleared by OFT he Office of Fair Trading (OFT) says it has pubs, said that the beer tie had, for decades, found no evidence that ties between pub "provided a low cost of entry to the pub industry Tcompanies and landlords are harming for committed, entrepreneurial licensees who are competition in the pub sector. unable to afford to buy a pub of their own". Its inquiry followed a super-complaint from the BBC News 22 October 2009 Campaign for Real Ed Says: Obviously Ale (CAMRA) over the enquiry team so-called "beer ties" were completely - landlords having hoodwinked by the to buy beer from brewers and pub pub owners. companies’ submissions. If you buy a lease or The OFT said there was "generally effective" tenancy there is no security attached, and the competition between pubs. terms such as rent are reviewed (usually upwards). CAMRA said it would now be urging Business You only have to look at cases such as those Secretary Lord Mandelson to overturn the OFT's recently highlighted in Pints of View ; where decision. -

Oxford Drinker Issue 74

Issue 75 August/Sept 2012 (PleFasertaeke ea copy, read it and pass it on) the Oxford Drinker Thursday 11th October Saturday 13th October See Page 12 The free newsletter of the Also Including the Oxford Branch of CAMRA White Horse Branch of CAMRA www.oxfordcamra.org.uk www.whitehorsecamra.org.uk August/September 2012 The Oxford Drinker is the newsletter of Contents Oxford and White Horse branches of Pub News........................................................ 4 CAMRA, The Campaign for Real Ale. Abingdon Pub News........................................5 5000 copies are distributed free of charge to pubs Brewery News................................................. 6 and other locations across the branch area; May Rural Mini Bus Trip ................................. 8 including Oxford, Abingdon, Witney, Faringdon, Oxford Pubs, News & Views..........................10 Eynsham, Kidlington, Bampton and Wantage. Wild West Rural Mini Bus Survey.................. 11 This newsletter is also available electronically in 15th Oxford Beer Festival 2012.....................12 PDF format at www.oxfordcamra.org.uk/drinker Oxford Brewers Taste & Swap.......................14 Valuable contributions to this edition have been Oxford CAMRA Branch AGM........................ 15 made by Matt Bullock, Neil Hoggarth, Richard Oxford CAMRA Branch Diary........................ 16 Queralt, John Mackie, Dave Richardson, Dave Notes from Branch Meetings.........................16 Cogdell, David Hill and others. Beer Festival Diary........................................ 17 The next issue will be published in October 2012. White Horse Branch Diary.............................18 White Horse Branch Information................... 18 Deadline for the next issue is Wantage Beer Festival.................................. 19 Monday 10th September 2012. Five go mad in Wadworthshire...................... 20 To advertise, contact Johanne Green on Pub Walk 7 Newbridge to Standlake...........23 07766‑663215 or send an email to Meet the Brewer Lymestone Brewery........