Dallas/Ft.Worth Office Market Report Third Quarter 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

World Class Capital Group & Colliers International 717Harwood.Com

717 Harwood is both Energy Star and LEED Gold certified REPRESENTED BY Colliers International +1 214 692 1100 David N. Quisenberry +1 214 217 1226 [email protected] John Conger +1 972 759 7850 [email protected] Lindsay Wolcott +1 214 217 1243 [email protected] PRESENTED BY World Class Capital Group 401 Congress Avenue & Colliers International 33rd Floor Austin, TX 78701 512.327.3300 colliers.com/texas wccapitalgroup.com 717harwood.com THE ART OF BUSINESS THE HEART OF DALLAS THE ART OF BUSINESS THE HEART OF DALLAS WI-FI POWERED COMMUNITY WORKSPACE REDESIGNED LOBBY a renovation that sparks innovation AND STREETSCAPE 717 Harwood features streamlined, tech-savvy, tenant focused services, in order to meet the needs of a 21st century tenant. WI-FI POWERED modern COMMUNITY WORKSPACE ACCESS TO MULTIPLE FIBER PROVIDERS CONTEMPORARY FURNITURE AND CURATED ARTWORK ON DISPLAY DUAL BACK-UP POWER FROM SEPARATE SUBSTITUTIONS RENOVATED LOBBY MODERN WORKING SPACE PRIVATE MEETING ROOMS WI-FI POWERED COMMUNITY WORKSPACE REDESIGNED LOBBY a renovation that sparks innovation AND STREETSCAPE 717 Harwood features streamlined, tech-savvy, tenant focused services, in order to meet the needs of a 21st century tenant. WI-FI POWERED modern COMMUNITY WORKSPACE ACCESS TO MULTIPLE FIBER PROVIDERS CONTEMPORARY FURNITURE AND CURATED ARTWORK ON DISPLAY DUAL BACK-UP POWER FROM SEPARATE SUBSTITUTIONS RENOVATED LOBBY MODERN WORKING SPACE PRIVATE MEETING ROOMS ONE BLOCK FROM DART AND LIGHT RAIL STATION (SERVICE TO ALL LINES) 24/7 MANNED AND MONITORED -

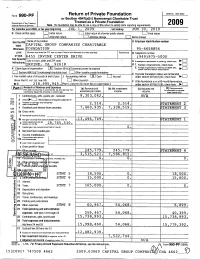

Form 990-PF Return of Private Foundation Or Section 4947(A)(1) Nonexempt Charitable Trust

OMB No 1545-0052 Form 990-PF Return of Private Foundation or Section 4947(a)(1) Nonexempt Charitable Trust Department of the Treasury Treated as a Private. Foundation Internal Revenue Service Note. The foundation may be able to use a copy of this return to satisfy state reporting requirements 2 00 9 For calendar year 2009 , or tax year beginning JUL 1, 2009 , and ending JUN 30 , 2010 G Check all that apply 0 Initial return initial return of a former public charity Final return 0 Amended return 0 Address change LI Name change Use the IRS Name of foundation A Employer identification number label. CAPITAL GROUP COMPANIES CHARITABLE Otherwise , F OUNDATION 95-4658856 print Number and street (or P O box number if mail is not delivered to street address) Room/suite B Telephone number ortype . 6455-IRVINE CENTER DRIVE ( 949 ) 975-5000 See Specific ^ City or town, state, and ZIP code C exemption ► Instructions . If application is pending, check here IRVINE , CA 92618 0 1. Foreign organizations, check here 2. Foreign organizations meeting the 85% test, ► H Check typea of organization Section 501(c)(3) exempt private foundation check here and attach computation Section 4947 (a )( 1 ) nonexem pt charitable trust 0 Other taxable p rivate foundation E If private foun dation status was terminated I Fair market value of all assets at end of year J Accounting method OX Cash LI Accrual under section 507(b)(1)(A), check here ► ll, (c), (from Part co! line 16) 0 Other (specify) F If the foundation is in a 60-month termination ► $ 218 , 995 , 94 5 . -

Dallas-Fort Worth Guide

FACULTY: SEDEF DOGANER, PhD STUDENTS: MICHAEL BRADEN MICHAEL LOCKWOOD LEVI SANCIUC hE/sZ^/dzK&dy^^EEdKE/K COLLEGE OF ARCHITECTURE ARCHITOURISM CONTENTS CHAPTER 1 p. 04 /ŶƚƌŽĚƵĐƟŽŶ CHAPTER 2 p. 11 The Architourist City: Dallas / Ft. Worth History 2.1.1 Importance 2.1.2 DFW Economy Related to Tourism 2.1.3 &t^ƚĂƟƐƟĐƐZĞůĂƚĞĚƚŽdŽƵƌŝƐŵϮ͘ϭ͘ϰ dƌĂŶƐĨŽƌŵĂƟŽŶŽĨ^ŝƚĞƐZĞůĂƚĞĚƚŽdŽƵƌŝƐŵϮ͘ϭ͘ϱ DFW Current Problems 2.1.6 The Architourist 2.2.1 Importance of Architourism 2.2.2 DFW Economy 2.2.3 &t^ƚĂƟƐƟĐƐZĞůĂƚĞĚƚŽdŽƵƌŝƐŵϮ͘Ϯ͘ϰ &tdŽƵƌŝƐƚWƌŽĮůĞƐϮ͘Ϯ͘ϱ &tƌĐŚŝƚŽƵƌŝƐƚ^ŝƚĞϮ͘Ϯ͘ϲ CHAPTER 3 p. 27 Analysis of Tourism in DFW CHAPTER 4 p. 87 Architourist Guide to DFW ARCHITOURISM CHAPTER 1 IntroducƟ on Introduc on: The focus of this analysis is to look at the eff ects of Architourism in the Dallas/Ft Worth area. What kind of culture if any has been created by Architourism and is it authen c or inauthen c. What kinds of developments have occurred there recently and what has this done to boost or change the local community. In the 2010 census the city of Dallas saw less than a one percent increase in its total popula on while Ft Worth increased by more than 38%. Did Architourism play a role in this? If so, what? Our analysis will begin with researching the demographics of the local users and types of tourists, their income level, race, educa on and loca on of residency. We will also include looking into the histories of selected sites with respect to their economies, culture, tourist ac vi es, and rela onship to the built environment. -

Q4 2017 Office Brief.Indd

The Lee Offi ce Brief 1 LEE OVERVIEW 2 NATIONAL OVERVIEW 2017 3 KEY MARKET SNAPSHOTS 4 SIGNIFICANT TRANSACTIONS Q4 5 NATIONWIDE LEE OFFICES 1 CANADA THE POWER OF THE LEE NETWORK THE LEE ADVANTAGE LEE & ASSOCIATES IS A COMMERCIAL REAL EAST WEST MIDWEST ESTATE BROKERAGE, MANAGEMENT AND APPRAISAL SERVICES FIRM. ESTABLISHED IN 1979, LEE & ASSOCIATES HAS GROWN ITS SOUTH SERVICE PLATFORM TO INCLUDE OFFICES IN THE UNITED STATES AND CANADA. Every Lee SOUTH & Associates offi ce delivers world class service to WEST an array of regional, national and international clients--from small businesses and local investors SERVING OUR CLIENTS to major corporate users and institutional THROUGHOUT THE U.S. AND investors. Our professionals combine the latest CANADA technology, resources and market intelligence ARIZONA with their experience, expertise and commitment BRITISH COLUMBIA to superior service to optimize your results. CALIFORNIA COLORADO INDUSTRY 1 FLORIDA SPONSORSHIPS & MARKET LEADER GEORGIA ORGANIZATIONS SPECIALIZING IN MARKET INTELLIGENCE IDAHO 2 ILLINOIS RELEVANT WORK INDIANA SEASONED PROFESSIONALS WITH RELEVANT MARYLAND TRANSACTION EXPERIENCE MICHIGAN 3 MINNESOTA WE SAVE YOU TIME MISSOURI CREATIVE PROBLEM SOLVING SKILL SETS NEVADA NEW JERSEY 4 ABILITY TO UNDERSTAND NEW YORK EFFECTIVE CLIENT COMMUNICATION OHIO PENNSYLVANIA 5 INTEGRITY SOUTH CAROLINA SHAPES OUR CULTURE & TEXAS DEFINES THE CHARACTER WASHINGTON WISCONSIN AFFILIATE INTERNATIONAL RELATIONSHIP 62% $11.6 billion 900 ▶ AUSTRIA ▶ NETHERLANDS ▶ BELGIUM ▶ POLAND ▶ FRANCE ▶ POLAND increase -

Market Insights Dallas/Fort Worth 4Q 2020 - OFFICE

Market Insights Dallas/Fort Worth 4Q 2020 - OFFICE Bradford Commercial Real Estate Services 3100 McKinnon Street, Suite 400 Dallas, Texas 75201 DALLAS-FORT WORTH OFFICE MARKET INSIGHTS 4Q2019 Table of Contents BRADFORD DALLAS-FORT WORTH OFFICE TEAM 1 DALLAS - FORT WORTH OVERALL MARKET INSIGHT 2 SUBMARKET EXPERTISE • Central Expressway • Dallas CBD • Fort Worth CBD 3 • Far North Dallas • White Rock/East Dallas • Las Colinas • LBJ Freeway • Mid Cities • Preston Center • Stemmons • Richardson/Plano • Uptown-Turtle Creek The information contained herein was obtained from CoStar; however, Bradford Companies makes no guarantees, warranties, or representation as to the completeness or accuracy thereof. The presentation of this property is submitted subject to errors, omissions, change of price or conditions prior to sale or lease or withdrawal without notice. 1 DFW OFFICE COVERAGE BinformedOFFICE MARKET EXPERTS Melanie Hughes Richmond Collinsworth Erik Blais Jared Laake Senior Vice President First Vice President Vice President Vice President 972.776.7046 972.776.7041 817.921.8179 972.776.7045 Dallas Dallas Fort Worth Dallas Susan Singer, CCIM Paul Richter Shane Benner Executive Vice President Vice President Vice President Brokerage Services 972.776.7036 817.921.8174 972.776.7043 Dallas Fort Worth Dallas • Bradford Corporate Office • Bradford Field Offices Bret Cooper Elizabeth Robertson Kyle Espie Market Director Market Director Senior Associate 972.776.7035 972.776.7199 972.776.7070 Dallas Dallas Dallas 2 3 Existing Inventory Vacancy Delivered -

World Class Capital Group & Colliers International 717Harwood.Com

717 Harwood is both Energy Star and LEED Gold certified REPRESENTED BY Colliers International +1 214 692 1100 David N. Quisenberry +1 214 217 1226 [email protected] John Conger +1 972 759 7850 [email protected] Lindsay Wolcott +1 214 217 1243 [email protected] PRESENTED BY World Class Capital Group 401 Congress Avenue & Colliers International 33rd Floor Austin, TX 78701 512.327.3300 colliers.com/texas wccapitalgroup.com 717harwood.com THE ART OF BUSINESS THE HEART OF DALLAS THE ART OF BUSINESS THE HEART OF DALLAS WI-FI POWERED COMMUNITY WORKSPACE REDESIGNED LOBBY a renovation that sparks innovation AND STREETSCAPE 717 Harwood features streamlined, tech-savvy, tenant focused services, in order to meet the needs of a 21st century tenant. WI-FI POWERED modern COMMUNITY WORKSPACE ACCESS TO MULTIPLE FIBER PROVIDERS CONTEMPORARY FURNITURE AND CURATED ARTWORK ON DISPLAY DUAL BACK-UP POWER FROM SEPARATE SUBSTITUTIONS RENOVATED LOBBY MODERN WORKING SPACE PRIVATE MEETING ROOMS WI-FI POWERED COMMUNITY WORKSPACE REDESIGNED LOBBY a renovation that sparks innovation AND STREETSCAPE 717 Harwood features streamlined, tech-savvy, tenant focused services, in order to meet the needs of a 21st century tenant. WI-FI POWERED modern COMMUNITY WORKSPACE ACCESS TO MULTIPLE FIBER PROVIDERS CONTEMPORARY FURNITURE AND CURATED ARTWORK ON DISPLAY DUAL BACK-UP POWER FROM SEPARATE SUBSTITUTIONS RENOVATED LOBBY MODERN WORKING SPACE PRIVATE MEETING ROOMS ONE BLOCK FROM DART AND LIGHT RAIL STATION (SERVICE TO ALL LINES) 24/7 MANNED AND MONITORED -

Inventory - July 2017 Office-Dfw

INVENTORY - JULY 2017 OFFICE-DFW PINNACLE TOWER LAKESLAKESIDE AT BENT SQUARE TREE THE BUTLER CENTER PREMIER PLACE 5005 Lyndon B Johnson 1740012377 Dallas Merit PkwyDrive 2231 Butler Street 5910 N Central Expwy. Dallas, TX Dallas, TX Dallas, TX Dallas, TX Office | Sublease | 6,612 SF Office | Sublease | 24,244 SF Office/Medical | Lease | 9,630 SF Office | Sublease | 8,005 SF $24.00/SF + E $17.00/SF Full Service Rate Negotiable $25.50/SF + E Available in 30 Days Suite 300 Great DFW Medical District Site Class A Office Space Class A Office Furniture Available Available Immediately 16th Floor with Excellent Views Great Building Amenities Recently Refurbished Parking Ratio 3/1000 Three Private Offices Lease Expires: 2/28/2021 Lease Expires: 6/30/2020 Workroom & Break room Jim Buddrus | 214.365.2791 Reception Area & IT Storage Closet Duke Biggers | 214.365.2784 Alan Thomas | 214.365.2737 3/1000 Parking Ratio Lease Expires: 4/30/2019 Ben Goldthorpe | 214.365.2716 Bruce Hecht | 214.365.2712 THREE LINCOLN CENTRE 717 HARWOOD 4455 LBJ LAKESTOLLWAY AT BENT TOWERS TREE 5430 LBJ Freeway 717 N Harwood St 4455 LBJ Freeway 1577017400 N Dallas Dallas Parkway Pkwy Dallas, TX Dallas, TX Dallas, TX Dallas, TX Office | Sublease | up to 20,073 SF Office | Sublease | 6,523 SF Office | Sublease | 21,153 SF Office | Sublease | 6,000 SF Below Market Rate $16.00/SF MG $10.00/SF + E $19.50/SF + E Suite 1500: 9,964 RSF Class A Office Space Available in 30 Days Available Immediately Suite 1580: 4,353 RSF Available Immediately Furniture Available, Negotiable Elevator -

The Art of Business the Heart of Dallas

717 Harwood is both Energy Star and LEED Gold certified REPRESENTED BY Colliers International +1 214 692 1100 David N. Quisenberry +1 214 217 1226 [email protected] John Conger +1 972 759 7850 [email protected] Lindsay Wolcott +1 214 217 1243 [email protected] PRESENTED BY World Class Capital Group 401 Congress Avenue & Colliers International 33rd Floor Austin, TX 78701 512.327.3300 colliers.com/texas wccapitalgroup.com 717harwood.com THE ART OF BUSINESS THE HEART OF DALLAS THE ART OF BUSINESS THE HEART OF DALLAS WI-FI POWERED COMMUNITY WORKSPACE REDESIGNED LOBBY a renovation that sparks innovation AND STREETSCAPE 717 Harwood features streamlined, tech-savvy, tenant focused services, in order to meet the needs of a 21st century tenant. WI-FI POWERED modern COMMUNITY WORKSPACE ACCESS TO MULTIPLE FIBER PROVIDERS CONTEMPORARY FURNITURE AND CURATED ARTWORK ON DISPLAY DUAL BACK-UP POWER FROM SEPARATE SUBSTITUTIONS RENOVATED LOBBY MODERN WORKING SPACE PRIVATE MEETING ROOMS WI-FI POWERED COMMUNITY WORKSPACE REDESIGNED LOBBY a renovation that sparks innovation AND STREETSCAPE 717 Harwood features streamlined, tech-savvy, tenant focused services, in order to meet the needs of a 21st century tenant. WI-FI POWERED modern COMMUNITY WORKSPACE ACCESS TO MULTIPLE FIBER PROVIDERS CONTEMPORARY FURNITURE AND CURATED ARTWORK ON DISPLAY DUAL BACK-UP POWER FROM SEPARATE SUBSTITUTIONS RENOVATED LOBBY MODERN WORKING SPACE PRIVATE MEETING ROOMS ONE BLOCK FROM DART AND LIGHT RAIL STATION (SERVICE TO ALL LINES) 24/7 MANNED AND MONITORED -

Creative Space. Artfully Executed

DOWNTOWN DALLAS TEXAS Creative Space. Artfully Executed Top of Building Signage Available 717Harwood aims to elevate the workday by providing a space that is both inspiring and uniquely Dallas. The 34-story, 844,326 square foot, Class A office tower features an all-glass exterior facade, a completely refreshed modern street presence and a premier second floor coworking space, all within steps of the largest Arts District in the United States and multiple award winning green spaces, restaurants and cultural attractions. With its top-tier on-site and surround- ing amenities, some of the biggest blocks available in Dallas CBD and prominent top of building signage available, your company can make its home—and its mark—on the Dallas skyline. 2 Steps to the Arts District and the best of Downtown Dallas 717 Harwood is on the doorstep of the Klyde Warren Park is a 5.2 acre green Tenants can walk one block south largest arts district in the United States, space that provides a (literal) bridge to catch the Dart Rail--the largest home to the Meyerson Symphony between Downtown and Uptown lightrail system in the US, giving them Center, Dallas Museum of Art, Nasher Dallas. Constructed on top of Wooddall rail access to virtually anywhere in the Sculpture Center, Winspear Opera Rodgers Expressway, it features public Metroplex House, and more performance space and award-winning eateries 3 Open, Inviting Lobby Make your day your way A place to stretch your legs. And your mind. One of the top office trends for 2019 will be more enhancements to the work environment to cultivate creativity and engagement. -

2100 ROSS AVE. 2Nd Generation Restaurant DALLAS, TEXAS PEARL ST

2100 ROSS AVE. 2nd Generation Restaurant DALLAS, TEXAS PEARL ST. AND ROSS AVE. COLIN BEAMS TRAMMELL HANCOCK LEASING | TENANT REPRESENTATION | LAND | INVESTMENT SALES | PROPERTY MANAGEMENT 8235 DOUGLAS AVE, SUITE 720 DALLAS, TEXAS 75225 VENTUREDFW.COM 214.378.1212 2100 ROSS AVE. DEMOGRAPHICS 1 MILE 3 MILE TRAFFIC COUNTS 2015 EST POPULATION 25,906 158,850 PEARL ST. 26,074 VPD (NCTCOG 2009) 2015 EST DAYTIME POPULATION 145,953 286,114 ROSS AVE. 12,104 VPD (NCTCOG 2002) 2015 EST AVG HH INCOME $92,635 $75,832 WOODALL ROGERS 178,074 VPD (NCTCOG 2013) 8235 DOUGLAS AVE, SUITE 720 DALLAS, TEXAS 75225 VENTUREDFW.COM 214.378.1212 HIGHLIGHTS • 2100 Ross – 33 Story Office Tower, 3200 SF of 2nd Generation Restaurant space FOR LEASE. • Klyde Warren Park. • The Spire – master-planned, mixed use development. • 2000 Ross – 26 story Residential/Hotel development site adding 2000 parking spaces to downtown Dallas. • One Arts Plaza – 500,000 SF of office, residential, and retail. 2nd and 3rd phases coming soon. • One Dallas Center -30-story office and residential tower, $40 million redevelopment in 2013. • Flora Lofts – Residential Tower with Artist Housing and street-level retail. • Museum Tower – residential tower. • Chase Tower – 55 story office tower. • Belo Mansion – Historic site in Downtown Dallas, proposed park adajcent. • Hall Arts - KPMG Plaza: 500,000 SF office and delivered Fall 2015, 72% leased. 30-story condo complex and additional office high-rise coming soon. • Myerson Symphony Center. • Winspear Opera House. • Nasher Sculpture Center. • Dallas Museum of Art. • Trammell Crow Center – 50 story office tower, home to Crow Collection of Asian Art. -

Market Insights Dallas/Fort Worth 2Q 2020 - OFFICE

Market Insights Dallas/Fort Worth 2Q 2020 - OFFICE Bradford Commercial Real Estate Services 3100 McKinnon Street, Suite 400 Dallas, Texas 75201 DALLAS-FORT WORTH OFFICE MARKET INSIGHTS 4Q2019 Table of Contents BRADFORD DALLAS-FORT WORTH OFFICE TEAM 1 DALLAS - FORT WORTH OVERALL MARKET INSIGHT 2 SUBMARKET EXPERTISE • Central Expressway • Dallas CBD • East Dallas 3 • Far North Dallas • Fort Worth CBD • Las Colinas • LBJ Freeway • Mid Cities • Preston Center • Richardson Plano • Stemmons • Uptown-Turtle Creek The information contained herein was obtained from CoStar; however, Bradford Companies makes no guarantees, warranties, or representation as to the completeness or accuracy thereof. The presentation of this property is submitted subject to errors, omissions, change of price or conditions prior to sale or lease or withdrawal without notice. 1 DFW OFFICE COVERAGE OFFICE MARKET EXPERTS • Bradford Corporate Office • Bradford Field Offices 2 BinformedOFFICE MARKET EXPERTS Melanie Hughes Richmond Collinsworth Erik Blais Jared Laake Senior Vice President First Vice President Vice President Vice President 972.776.7046 972.776.7041 817.921.8179 972.776.7045 Dallas Dallas Fort Worth Dallas Susan Singer, CCIM Paul Richter Shane Benner Executive Vice President Vice President Vice President Brokerage Services 972.776.7036 817.921.8174 972.776.7043 Dallas Fort Worth Dallas Bret Cooper Elizabeth Robertson Kyle Espie Market Director Market Director Senior Associate 972.776.7035 972.776.7199 972.776.7070 Dallas Dallas Dallas 3 CENTRAL EXPRESSWAY OFFICE -

Documentation of Public Meeting

Documentation of Public Meeting Project Location Hays County Ranch-to-Market 150 CSJ: 0805-04-028; 0016-17-013 Project Limits From I-35 to Ranch-to-Market 150 West of Kyle Meeting Location Wallace Middle School (Cafeteria) 1302 W. Center Street, Kyle, TX 78640 Meeting Date and Time August 2, 2018 from 4:00 p.m. to 7:00 p.m. Translation Services Spanish and ASL translation available at meeting Presenters N/A Elected/Public Officials in Attendance Commissioner Mark Jones, Hays County, Precinct 2 Commissioner Ray Whisenant, Hays County, Precinct 4 Total Number of Attendees (approx.) 172 Total Number of Commenters 34 Contents A. Comment/response matrix.……………………………………………….2 B. Notices..…………………………………………………………………….10 C. Sign-in sheets.……………………………………………………………..118 D. Comments received……………………………………………………….126 E. Figures.……………………………………………………………………..194 F. Description of modifications resulting from public meeting…………...207 A. Comment/Response Matrix 2 Commenter Commenter Name Date Received Source Comment Comment Topic Response Number 1 Evangelina Chapa 8/2/2018 Comment Card We are concerned about County road tax. What is the percentage breakdown increase on taxes for individual Impact to taxes Funding for construction has not yet been identified at this point and can potentially household. Since this is proposing to be planned next to a school, is the Southern connection being connected to Connection to I-35 come from multiple sources (state, federal, and local partnerships). service lane via Opal or is it going to angle towards the Yarrington road bridge. Is there going to be modification to current Yarrington Bridge to facilitate on fly over connection to IH 35 North and South.