Dallas-Fort Worth Office Market 4Q 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2019 Uptown Demographic Study

Uptown Dallas Prepared for Uptown Dallas, Inc. Market Study December 2019 Metrostudy-Dallas/Ft. Worth 1255 West 15th Street, Suite 240 Plano, TX 75075 Phone: 214.869.4916 Email: [email protected] Web: www.metrostudy.com Table of Contents Profile 3 – 8 Economic/Demographic 7 – 11 Employment 12 – 14 Real Estate 15 – 21 Transportation 22 – 24 Uptown Data 25 – 28 Uptown Residents 29 – 37 UPTOWN DALLAS, INC. CUSTOM STUDY Page 2 Profile Uptown Dallas 1993 Development in Uptown began in the 1980s with residential and commercial growth. As the neighborhood began to take shape, developers and residents alike saw an opportunity to enhance the area. Through consensus with the City of Dallas, Uptown Dallas, Inc. was formed in 1993 to scale, maintain and further improve the neighborhood. Uptown Dallas, Inc. celebrated 25 years in 2018. 591.8 Acres Stretching just under one square mile, or 591.8 acres, Uptown is a diverse and dense neighborhood. The community includes numerous residential options, reputable companies, schools and a variety of retail and dining options. 58.1 Acres Uptown has 19 square feet of greenspace per person totaling 58.1 acres. Open space includes Griggs Park which is 8 acres and Greenwood Cemetery, Calvary, Temple Emanuel, Anita Phelps Park and Freedman’s Memorial comprise 44 acres. Katy Trail, a 3.5-mile, privately funded trail system built on an old railroad line defines Uptown’s western border. Additionally, there are 53.5 acres of greenspace bordering Uptown including the award-winning Klyde Warren Park. 4.6 Miles Founded in 1983 with the intent of returning heritage streetcars to the streets of Uptown, the McKinney Avenue Transit Authority successfully accomplished that goal in July of 1989. -

March-1-2018-Dallas-Houston-Free

FREE RENT APARTMENT SPECIALS for DALLAS - Weekly LIST - As of 3/1/2018 100% Free Housing Service for Graduating Professionals locating to Dallas - Houston - Austin - SA Start Your Free Real Time Daily Search here! http://www.homebaseservices.com/1monthfree/ Year Property Special! Starting 1B Starting 2B Area of Town Built Aura on McKinney 1 month free! $1,497 $1,497 2016 D10-UptownNorth Cityplace Heights 2 months free! $1,412 $1,879 2013 D10-UptownNorth Flats at The Sawyer 2 months free! 2006 D10-UptownNorth $1,000 off 1st Gallery at Turtle Creek $1,244 $1,996 2014 D10-UptownNorth month! Lofts at The Sawyer 2 months free! 2006 D10-UptownNorth $750 off 1st Monaco on the Trail $1,469 $2,566 2009 D10-UptownNorth month! Oakwood Dallas 1 month free! 2003 D10-UptownNorth Uptown One Oak Grove 2 months free! $1,700 $2,825 2016 D10-UptownNorth $1,000 off 1st Radius at Turtle Creek $1,365 $1,750 2001 D10-UptownNorth month! The Lennox at West 2 months free! $1,300 $1,807 1999 D10-UptownNorth Village Uptown at Cole Park 6 weeks free! 2016 D10-UptownNorth 28TwentyEight 1 month free! 2017 D11-UptownSouth $1,000 off 1st Avenue on Fairmount 2015 D11-UptownSouth month! 1 month free Brady $1,865 $3,424 2016 D11-UptownSouth on 1 bed! Cantabria at Turtle $1000 off 1st $1,425 $1,930 2014 D11-UptownSouth Creek month! 1.5 month Miro $1,499 $2,199 2016 D11-UptownSouth free! $500 off .5 Post Gallery $5,000 1999 D11-UptownSouth month! Post Heights 1 month free! $1,185 $1,550 1997 D11-UptownSouth $500 off 1st Post Vintage $1,145 $1,420 1995 D11-UptownSouth month! -

Texas Public Schools and Charters, Directory, November 2016

Texas Public Schools and Charters, Directory, November 2016 Tax rate 2015-16 Appraised Mailing address Cnty.-dist. Sch. County and district enroll- valuation (in Main- County, district, region, school and phone number number no. superintendents, principals Grades ment $ thousands) tenance Bond 001 ANDERSON COUNTY 001 CAYUGA ISD 07 P O BOX 427 001-902 DR RICK WEBB 570 270,576 .104 .000 CAYUGA 75832-0427 PHONE - (903) 928-2102 FAX - (903) 928-2646 REGULAR INSTRUCTIONAL CAYUGA H S (903) 928-2294 ext:012 001 RUSSELL HOLDEN 9-12 188 CAYUGA MIDDLE (903) 928-2699 ext:4001 041 SHERRI MCINNIS 6-8 120 CAYUGA EL (903) 928-2295 103 TRACIE CAMPBELL EE-5 262 ELKHART ISD 07 301 E PARKER ST 001-903 DR RAYMOND DESPAIN, JR 1244 262,857 .117 .019 ELKHART 75839-9701 PHONE - (903) 764-2952 FAX - (903) 764-2466 REGULAR INSTRUCTIONAL ELKHART H S (903) 764-5161 001 JASON IVES 9-12 368 ELKHART MIDDLE (903) 764-2459 041 JAMES MAYS, JR 6-8 299 ELKHART EL (903) 764-2979 101 TANA HERRING EE-2 332 ELKHART INT (903) 764-8535 102 GREGORY HERRING 3-5 245 DAEP INSTRUCTIONAL ELKHART DAEP 002 KG-12 0 FRANKSTON ISD 07 P O BOX 428 001-904 JOHN ALLEN 842 248,392 .117 .040 FRANKSTON 75763-0428 PHONE - (903) 876-2556 FAX - (903) 876-4558 REGULAR INSTRUCTIONAL FRANKSTON H S (903) 876-3219 001 DONNY LEE 9-12 231 FRANKSTON MIDDLE (903) 876-2215 041 MELISSA MCINTIRE 6-8 175 FRANKSTON EL (903) 876-2214 102 MELISSA MCINTIRE EE-5 436 NECHES ISD 07 P O BOX 310 001-906 RANDY SNIDER 383 104,058 .104 .029 NECHES 75779-0310 PHONE - (903) 584-3311 FAX - (903) 584-3686 REGULAR INSTRUCTIONAL -

Austin-Ranch-Offices-May-2015.Pdf

AUSTINRANCH.COM THE OFFICES OF AUSTIN RANCH OVERVIEW AUSTIN RANCH 1700 ACRES OF NATURAL BEAUTY AND ROLLING VISTAS 700 ACRES OF CORPORATE CAMPUS -HOME TO OVER 10 MILLION SF OF CORPORATE AND REGIONAL HEADQUARTERS SERENE HILL COUNTRY ENVIRONMENT IN HEART OF FASTEST GROWING PART OF DFW DFW’S EPICENTER FOR HEADQUARTERS DEVELOPMENT -LOCATED IN THE COLONY, LEWISVILLE, & CARROLTON — ADJACENT TO LEGACY, FRISCO, & PLANO -ECONOMIC DEVELOPMENT INCENTIVES IN A PRO-BUSINESS ENVIRONMENT RAPIDLY GROWING SKILLED LABOR FORCE OF 2 MILLION IN THE REGION EXCELLENT ACCESS TO DNT, SH 121, I-35, & PGBT WITH GREAT INGRESS / EGRESS INTEGRATE BUILD TO SUIT EPICENTER FOR ARCHITECTURAL DESIGN QUALITY BILLINGSLEY COMPANY IS KNOWN FOR WITH NATURE OFFICE CAMPUS HQ DEVELOPMENT 1 2 121 THE OFFICES OF AUSTIN RANCH FRISCO WITHIN A 20-MINUTE DRIVE NEIGHBORING SKILLED WORKFORCE: 760,000 UPWARDLY MOBILE PEOPLE 10 13 HEADQUARTERS SMART PEOPLE: 75% OF POPULATION WITH AT LEAST SOME COLLEGE 7 11 1 Orthofix 12 2 Pizza Inn FAST GROWING: PROJECTED POPULATION OF 1.4 MILLION AND 547,855 HOUSEHOLDS BY 2019 8 9 14 121 3 Edward Don 1 2 3 4 Sanyo 4 5 Freddie Mac LEWISVILLE 6 Beauticontrol 7 Toyota 8 Frito Lay 5 9 Pizza Hut 6 10 FedEx Office DALLAS NORTH PLANO THE REGION TOLLWAY 11 JCPenney DEMOGRAPHICS 12 Ericsson 1 MILE 3 MILES 5 MILES 13 Granite Park 2014 POPULATION 9,941 69,305 202,193 14 HP DALLAS-FORT WORTH CONTINUES TO 2014 AVERAGE HH INCOME $98,524 $104,187 $112,289 2014 DAYTIME POPULATION 10,087 51,144 102,205 190 DRAW FORTUNE AND GLOBAL 500 2013 TOTAL EMPLOYEES 10,080 57,620 125,113 190 % POPULATION CHANGE SINCE 2000 457% 100% 81% HEADQUARTERS, BY GROWTH AND EXPANSION % HOUSEHOLD CHANGE SINCE 2000 402% 128% 83% FAR NORTH DALLAS OF LOCAL COMPANIES AS WELL AS BY CARROLLTON RELOCATIONS OF HEADQUARTER OPERATIONS. -

Market Insights 2020

Market Insights Dallas/Fort Worth Office 1Q 2020 Bradford Commercial Real Estate Services 3100 McKinnon Street, Suite 400 Dallas, Texas 75201 DALLAS-FORT WORTH OFFICE MARKET INSIGHTS 4Q2019 Table of Contents BRADFORD DALLAS-FORT WORTH OFFICE TEAM 1 DALLAS - FORT WORTH OVERALL MARKET INSIGHT 2 SUBMARKET EXPERTISE • Central Expressway • Dallas CBD • East Dallas 3 • Far North Dallas • Fort Worth CBD • Las Colinas • LBJ Freeway • Mid Cities • Preston Center • Richardson Plano • Stemmons • Uptown-Turtle Creek The information contained herein was obtained from CoStar; however, Bradford Companies makes no guarantees, warranties, or representation as to the completeness or accuracy thereof. The presentation of this property is submitted subject to errors, omissions, change of price or conditions prior to sale or lease or withdrawal without notice. 1 DFW OFFICE COVERAGE OFFICE MARKET EXPERTS • Bradford Corporate Office • Bradford Field Offices 2 BinformedOFFICE MARKET EXPERTS Melanie Hughes Richmond Collinsworth Erik Blais Jared Laake Senior Vice President First Vice President Vice President Vice President 972.776.7046 972.776.7041 817.921.8179 972.776.7045 Dallas Dallas Fort Worth Dallas Susan Singer, CCIM Paul Richter Shane Benner Executive Vice President Vice President Vice President Brokerage Services 972.776.7036 817.921.8174 972.776.7043 Dallas Fort Worth Dallas Bret Cooper Elizabeth Robertson Kyle Espie Market Director Market Director Senior Associate 972.776.7035 972.776.7199 972.776.7070 Dallas Dallas Dallas 3 CENTRAL EXPRESSWAY OFFICE -

Victory Park

SOUTH VICTORY DISTRICT Victory Park DALLAS, TEXAS Victory Park, a walkable, urban development in the Uptown neighborhood of Dallas, is home to some of the cities best restaurants, entertainment, and retail. • Victory Park is a 75 acre masterplanned, mixed-use development in Downtown Dallas anchored by the American Airlines Center (home of the Dallas Mavericks & Stars), The House of Blues, HERO, Tom Thumb, W Dallas Hotel and the new 44,000 SF Cinepolis Luxury Cinemas. • The bar and restaurant scene at Victory Park is about to experience a dramatic change as we welcome new concepts, opening later this year, from some of Dallas' top food and beverage operators. • WeWork opened in early 2019 on the 2nd & 3rd floors of the Victory Plaza Office building. The space features their signature mid-century modern decor, open floor plan, floor to ceiling glass and steel framing, private office suites and communal working space. 2 Demographics DALLAS LOVE NORTHEAST FIELD AIRPORT PARK DALLAS CITIES 1 MI RADIUS GREENWAY Population (2018) – 29,603 PARKS 75 Households – 13,124 Avg. HH Income – $117,552 3 MILES Median Age – 33 Daytime Demo – 141,525 Education (Bach+) – 57% 3 MI RADIUS 35E Population (2018) – 187,692 Households – 87,023 1 MILE Avg. HH Income – $91,322 Trinity UPTOWN OLD EAST Median Age – 34 River DALLAS Daytime Demo – 393,259 30 Education (Bach+) – 48% Victory Park 5 MI RADIUS Deep DOWNTOWN Ellum Population (2018) – 398,518 DALLAS Households – 163,296 Avg. HH Income – $94,878 CEDARS Median Age – 34 Daytime Demo – 642,221 30 Education (Bach+) -

World Class Capital Group & Colliers International 717Harwood.Com

717 Harwood is both Energy Star and LEED Gold certified REPRESENTED BY Colliers International +1 214 692 1100 David N. Quisenberry +1 214 217 1226 [email protected] John Conger +1 972 759 7850 [email protected] Lindsay Wolcott +1 214 217 1243 [email protected] PRESENTED BY World Class Capital Group 401 Congress Avenue & Colliers International 33rd Floor Austin, TX 78701 512.327.3300 colliers.com/texas wccapitalgroup.com 717harwood.com THE ART OF BUSINESS THE HEART OF DALLAS THE ART OF BUSINESS THE HEART OF DALLAS WI-FI POWERED COMMUNITY WORKSPACE REDESIGNED LOBBY a renovation that sparks innovation AND STREETSCAPE 717 Harwood features streamlined, tech-savvy, tenant focused services, in order to meet the needs of a 21st century tenant. WI-FI POWERED modern COMMUNITY WORKSPACE ACCESS TO MULTIPLE FIBER PROVIDERS CONTEMPORARY FURNITURE AND CURATED ARTWORK ON DISPLAY DUAL BACK-UP POWER FROM SEPARATE SUBSTITUTIONS RENOVATED LOBBY MODERN WORKING SPACE PRIVATE MEETING ROOMS WI-FI POWERED COMMUNITY WORKSPACE REDESIGNED LOBBY a renovation that sparks innovation AND STREETSCAPE 717 Harwood features streamlined, tech-savvy, tenant focused services, in order to meet the needs of a 21st century tenant. WI-FI POWERED modern COMMUNITY WORKSPACE ACCESS TO MULTIPLE FIBER PROVIDERS CONTEMPORARY FURNITURE AND CURATED ARTWORK ON DISPLAY DUAL BACK-UP POWER FROM SEPARATE SUBSTITUTIONS RENOVATED LOBBY MODERN WORKING SPACE PRIVATE MEETING ROOMS ONE BLOCK FROM DART AND LIGHT RAIL STATION (SERVICE TO ALL LINES) 24/7 MANNED AND MONITORED -

Concierge Newsletter

November 2018 Concierge newsletter Honey Baked Hams & Turkeys Delivered We are happy to continue HoneyBaked’s Holiday Online Employee Purchasing Program! This is your chance to order these delicious products with exclusive free delivery directly to Trammell Crow Center at lower prices and no standing in long lines at HBH stores. To complete your order through the EPP (Employee Purchasing Program) site: 1. Go to https://myhoneybakedstore.com/dallas/4308/epp/index.asp Concierge Comments 2. Enter your code: TCC 3. Select your items and pre-pay credit or debit card. I wish everyone a festive and memorable month of thankfulness. 4. Show up at the Concierge Desk in the management office in suite 540 on the 5th floor of Relax…and schedule a chair massage at Trammell Crow Center. I have Trammell Crow Center on Monday, November 19 between 11:00 a.m. and 11:30 a.m. to pick up your HoneyBaked items, hand crafted just for you. This year’s prices are a better discount than last arranged for a chair massage therapist to come to Trammell Crow Center year. When your order is complete, please put the pickup date and time in your calendar, 11/19/18 at 11. for your convenience every other Friday. Contact Charlotte directly to make Deadline to order is Friday, November 16 at midnight. Please note: This discount cannot be your appointment at 817-966-8794. It is $5 per 5 minutes with a 30-minute combined with any other coupons or offers. Only credit or debit cards are accepted on the EPP site. -

Living in Dallas, Texas Demographics Dallas Is the Third-Largest City in Texas and the Ninth-Largest in the United States

Living in Dallas, Texas Demographics Dallas is the third-largest city in Texas and the ninth-largest in the United States. Dallas forms the heart of the large metropolitan area in north central Texas, commonly referred to as the “metroplex”. The metroplex, a 12-county area encompassing more than 120 cities, is anchored by the City of Dallas in the east and the City of Fort Worth in the west. The population of Dallas is around 1.3 million according to the US Census Bureau. This ultra- modern and sophisticated city is the largest economic center of the 12-county Dallas-Fort Worth metropolitan area, which is the fourth-largest metropolitan area in the United States. The Dallas community is world-class with a diverse population located on a total land area of 384 square miles. Dallas is centrally located within the US and serves as a commercial and cultural hub of the Southwest region. Within a four-hour flight from most North American destinations, the travel possibilities are endless. Dallas is also a leading business and meeting city. Dallas-Fort Worth is home to 24 Fortune 500 companies and has become a hotspot in recent years for corporate relocations. Notable Fortune 500 companies include: Exxon Mobil, AT&T, Energy Transfer Equity, American Airlines Group, Southwest Airlines, Texas Instruments, GameStop, D.R. Horton, and Dr. Pepper Snapple Group. Entertainment/Culture With many entertainment districts within a short distance of downtown, Dallas is a unique melting pot which mixes local history with arts, culture, dining, and more. Dallas is stylish and cosmopolitan, a city with a well-earned reputation for fashion, shopping, and prosperity. -

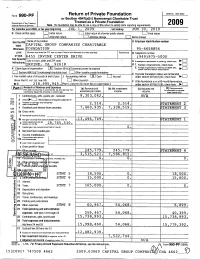

Form 990-PF Return of Private Foundation Or Section 4947(A)(1) Nonexempt Charitable Trust

OMB No 1545-0052 Form 990-PF Return of Private Foundation or Section 4947(a)(1) Nonexempt Charitable Trust Department of the Treasury Treated as a Private. Foundation Internal Revenue Service Note. The foundation may be able to use a copy of this return to satisfy state reporting requirements 2 00 9 For calendar year 2009 , or tax year beginning JUL 1, 2009 , and ending JUN 30 , 2010 G Check all that apply 0 Initial return initial return of a former public charity Final return 0 Amended return 0 Address change LI Name change Use the IRS Name of foundation A Employer identification number label. CAPITAL GROUP COMPANIES CHARITABLE Otherwise , F OUNDATION 95-4658856 print Number and street (or P O box number if mail is not delivered to street address) Room/suite B Telephone number ortype . 6455-IRVINE CENTER DRIVE ( 949 ) 975-5000 See Specific ^ City or town, state, and ZIP code C exemption ► Instructions . If application is pending, check here IRVINE , CA 92618 0 1. Foreign organizations, check here 2. Foreign organizations meeting the 85% test, ► H Check typea of organization Section 501(c)(3) exempt private foundation check here and attach computation Section 4947 (a )( 1 ) nonexem pt charitable trust 0 Other taxable p rivate foundation E If private foun dation status was terminated I Fair market value of all assets at end of year J Accounting method OX Cash LI Accrual under section 507(b)(1)(A), check here ► ll, (c), (from Part co! line 16) 0 Other (specify) F If the foundation is in a 60-month termination ► $ 218 , 995 , 94 5 . -

Concierge Newsletter Blood Drive Tuesday, January 14, 2020 from 10:00 A.M

January 2020 Concierge newsletter Blood Drive Tuesday, January 14, 2020 from 10:00 a.m. to 4:00 p.m., Donor Coach on Flora Street Concierge Comments Please call 1-800-RED-CROSS We welcome this new year and new decade that hold so many (1-800-733-2767) or visit possibilities. It is up to each of us to make the changes within ourselves RedCrossBlood.org and enter: trammellcrowcenter to schedule an appointment. to make the changes we want to see happen. There are ways to improve your public speaking, improve your health, connect to our community and even give back to our community. Shred Truck on Flora Street I am relocated in my new Concierge desk. Please come by and see me Tuesday, January 28 from 8:00 a.m. to Noon on the 2nd floor in the Trammell Crow Center Conference Center near Flora Street the East Parking Garage elevators or the lobby Concierge Desk. I may www.Balcones.com still be found in the management office in suite 540 occasionally. Email is still the best way to reach me. Relax…and schedule a chair massage at Trammell Crow Center. E-Waste Recycling Truck on I have arranged for a chair massage therapist to come to Trammell Crow Center for your convenience every other Friday. Contact Charlotte directly to make your appointment at 817-966-8794. It is $5 per 5 Loading Dock minutes with a 30-minute maximum. Friday, January 10 and 24, 2020 Wednesday, January 29 from 9:30 am to Noon at Loading Dock in suite 570 from 10:30 a.m. -

Member FDIC Bishop Arts Downtown Dallas Cedars Deep Ellum Garland

Uptown Garland Deep Ellum Bishop Arts Cedars Downtown Dallas 2020 Member FDIC “What a long, strange trip it’s been.” GROWTH - Year-end assets increased DEAR SHAREHOLDERS, 2020 was best described by the 34.37% to $307,327,273. Deposits famous song line by the Grateful Dead – were up 37.8% to $274,208,306, while “What a long, strange trip it’s been.” our loan portfolio increased 23.5% to We went from a booming economy $235,296,015. We anticipate continued early in the year, to a massive drop strong growth in 2021, although we in the stock market and an almost expect that growth to be at slower total lockdown of the country due to levels than the record increases that the worst pandemic in over 100 years we saw in 2020. in the spring, to civil unrest in the CAPITAL - Our capital to assets ratio, summer and finally to the anticipation considered by many the primary of a new administration and a stock indicator of bank strength and market boom in the fall. solvency, was 9.97% at year end, Last year was truly a year like no significantly above “well capitalized” other in recent memory. regulatory requirements. Despite our Despite all of these headwinds, strong capital ratio, our after-tax Texas Brand Bancshares, Inc., return on equity from continuing and Texas Brand Bank are pleased operations was 9.66%. Return on to announce a record year. average assets was 0.99%. Borrower dissatisfaction with large, money center banks, EARNINGS – Earnings were up sharply particularly with respect to the in 2020, rising 41.42% over 2019.