SPIEF Review November '2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Russia Takes Double Punch As Vanishing Workers Fan Prices Bloomberg.Com – Global Edition by Olga Tanas 2014-09-17, T14:12:11Z

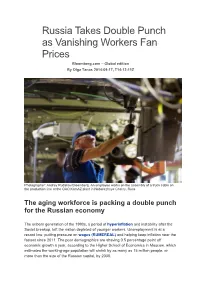

Russia Takes Double Punch as Vanishing Workers Fan Prices Bloomberg.com – Global edition By Olga Tanas 2014-09-17, T14:12:11Z Photographer: Andrey Rudakov/Bloomberg. An employee works on the assembly of a truck cabin on the production line at the OAO KamAZ plant in Naberezhnye Chelny, Russ The aging workforce is packing a double punch for the Russian economy The unborn generation of the 1990s, a period of hyperinflation and instability after the Soviet breakup, left the nation depleted of younger workers. Unemployment is at a record low, putting pressure on wages (RUMEREAL) and helping keep inflation near the fastest since 2011. The poor demographics are shaving 0.5 percentage point off economic growth a year, according to the Higher School of Economics in Moscow, which estimates the working-age population will shrink by as many as 15 million people, or more than the size of the Russian capital, by 2030. Aging populations are unsettling central bankers from Tokyo to Frankfurt in their struggle to prevent deflation as older workers tend to defer consumption in favor of savings. Russia faces the opposite threat: entrenched inflation that risks shackling monetary policy already lurching from one crisis to another since Crimea was annexed in March. “Taking into account low unemployment and tight supply on the labor market, wages will remain at a high level, affecting inflation,” said Natalia Orlova, chief economist at Alfa Bank in Moscow. With the central bank increasingly drawing attention to poor demographics, it’s “in effect saying it can do nothing for the economy, whose problems are structural in character.” Demographic Factor Russia is caught in a vise of elevated inflation and stalling economic growth. -

Russian Art+ Culture

RUSSIAN ART+ CULTURE WINTER GUIDE RUSSIAN ART WEEK, LONDON 23-30 NOVEMBER 2018 Russian Art Week Guide, oktober 2018 CONTENTS Russian Sale Icons, Fine Art and Antiques AUCTION IN COPENHAGEN PREVIEW IN LONDON FRIDAY 30 NOVEMBER AT 2 PM Shapero Modern 32 St George Street London W1S 2EA 24 november: 2 pm - 6 pm 25 november: 11 am - 5 pm 26 november: 9 am - 6 pm THIS ISSUE WELCOME RUSSIAN WORKS ON PAPER By Natasha Butterwick ..................................3 1920’s-1930’s ............................................. 12 AUCTION HIGHLIGHTS FEATURED EVENTS ...........................14 By Simon Hewitt ............................................ 4 RUSSIAN TREASURES IN THE AUCTION SALES ROYAL COLLECTION Christie's, Sotheby's ........................................8 Interview with Caroline de Guitaut ............... 24 For more information please contact MacDougall's, Bonhams .................................9 Martin Hans Borg on +45 8818 1128 Bruun Rasmussen, Roseberys ........................10 RA+C RECOMMENDS .....................30 or [email protected] Stockholms Auktionsverk ................................11 PARTNERS ...............................................32 Above: Georgy Rublev, Anti-capitalist picture "Demonstration", 1932. Tempera on paper, 30 x 38 cm COPENHAGEN, DENMARK TEL +45 8818 1111 Cover: Laurits Regner Tuxen, The Marriage of Nicholas II, Emperor of Russia, 26th November 1894, 1896 BRUUN-RASMUSSEN.COM Credit: Royal Collection Trust/ © Her Majesty Queen Elizabeth II 2018 russian art week guide_1018_150x180_engelsk.indd 1 11/10/2018 14.02 INTRODUCTION WELCOME Russian Art Week, yet again, strong collection of 19th century Russian provides the necessary Art featuring first-class work by Makovsky cultural bridge between and Pokhitonov, whilst MacDougall's, who Russia and the West at a time continue to provide our organisation with of even worsening relations fantastic support, have a large array of between the two. -

Russia's 2020 Strategic Economic Goals and the Role of International

Russia’s 2020 Strategic Economic Goals and the Role of International Integration 1800 K Street NW | Washington, DC 20006 Tel: (202) 887-0200 | Fax: (202) 775-3199 E-mail: [email protected] | Web: www.csis.org authors Andrew C. Kuchins Amy Beavin Anna Bryndza project codirectors Andrew C. Kuchins Thomas Gomart july 2008 europe, russia, and the united states ISBN 978-0-89206-547-9 finding a new balance Ë|xHSKITCy065479zv*:+:!:+:! CENTER FOR STRATEGIC & CSIS INTERNATIONAL STUDIES Russia’s 2020 Strategic Economic Goals and the Role of International Integration authors Andrew C. Kuchins Amy Beavin Anna Bryndza project codirectors Andrew C. Kuchins Thomas Gomart july 2008 About CSIS In an era of ever-changing global opportunities and challenges, the Center for Strategic and International Studies (CSIS) provides strategic insights and practical policy solutions to decisionmakers. CSIS conducts research and analysis and develops policy initiatives that look into the future and anticipate change. Founded by David M. Abshire and Admiral Arleigh Burke at the height of the Cold War, CSIS was dedicated to the simple but urgent goal of finding ways for America to survive as a nation and prosper as a people. Since 1962, CSIS has grown to become one of the world’s preeminent public policy institutions. Today, CSIS is a bipartisan, nonprofit organization headquartered in Washington, DC. More than 220 full- time staff and a large network of affiliated scholars focus their expertise on defense and security; on the world’s regions and the unique challenges inherent to them; and on the issues that know no boundary in an increasingly connected world. -

State Policy in the Arctic

INFORMATION DIGEST ECONOMIC DEVELOPMENT OF THE ARCTIC October 2020 KEY TOPICS: NORTHERN SEA ROUTE INTERNATIONAL RELATIONS INDIGENOUS PEOPLES OF THE NORTH STATE POLICY IN THE ARCTIC 30 October 2020, TASS Alexander Krutikov: large economic projects will appear in almost all Arctic regions “The system of preferences that exists in the Arctic is different from the one in the Far East. <…> The first block of support measures was put into operation. It is meant for large economic projects that significantly change the economic environment. <…> Such projects are planned for practically every Arctic region,” shared Deputy Minister for Development of the Russian Far East and Arctic Alexander Krutikov during the roundtable organized by the Ministry and the Roscongress Foundation. The second block applies to small and medium businesses. It offers premium rebates: when a small business becomes a resident of the Arctic zone, its premium rate goes as low as 3.025%. The third block includes non-tax measures. tass.ru/ekonomika/9876979 26 October 2020, Rossiyskaya Gazeta, TASS, RIA Novosti, Regnum, etc. Vladimir Putin approved Arctic Zone Development Strategy President Vladimir Putin signed a decree approving the Arctic Zone Development Strategy and ensuring national security until 2035. Within the next three months, the Government will need to approve a unified action plan to implement the basics of the state policy in the Arctic and the afore-mentioned strategy. The Government will report on their status annually. rg.ru/2020/10/26/putin-utverdil-strategiiu-razvitiia-arkticheskoj-zony.html 26 October 2020, TASS Public Council of Russia’s Arctic Zone is chaired by President of Russian Association of the Indigenous Peoples of the North Grigory Ledkov, President of the Russian Association of the Indigenous Peoples of the North, Siberia, and the Far East, is now the Chairman of the Public Council of Russia’s Arctic Zone. -

Anniversary Conference September 08-09, 2016 Moscow, Leninskie

Anniversary Conference September 08-09, 2016 Thursday, September 08th, 2016 09:00-09:30 Reception and Registration 09:30-10:00 Conference Opening Round Table «Academic Research and Economic Policy-making» Participants: Andrey Belousov* (President Administration), Arkadiy 10:00-11:30 Dvorkovitch* (Government of Russia), Galina Hale (FRB San-Francisco), Andrey Klepatch (MSU), Alexey Ulyukaev* (Ministry of Economic Development), Ksenia Yudaeva (Bank of Russia), Chair: Elvira Nabiullina (Bank of Russia) 11:30-12:00 Coffee-break Irina Kirisheva (’06, Nazarbayev University) 12:00-12:45 Contests with sabotage and their optimal design Anna Chorniy (’06, Princeton) 12:45-13:30 Health economics: Human capital framework 13:30-15:00 Lunch Bank of Russia Workshop 15:00-15:45 DSGE modeling for policymaking in an Emerging market economy: some experience of the Bank of Russia Ruben Enikolopov (Barselona GSE, NES) 16:00-16:45 Social Media and Collective Action Oleg Itskhoki (‘03, Princeton) 16:45-17:30 Firms and the International Transmission of Shocks 17:30-18:00 Coffee-break Keynote Speech 18:00-19:15 Helene Rey (London Business School) TBA Moscow, Leninskie Gory, 1-46 MSU Department of Economics, Lecture Hall, П5 Anniversary Conference September 08-09, 2016 Friday, September 09th, 2016 Round Table «Modern Universities and Economic Education» Speakers: Alexey Belyanin (HSE), Shlomo Weber* (NES), Oleg Zamulin* 10:00-11:30 (NES), Oleg Itskhoki (Princeton), Philipp Kartaev (MSU), Evgeniy Kuznetsov (RVC), Andrey Markov (MSU) Chair: Alexandr Auzan 11:30-12:00 Coffee-break Vilen Lipatov (’98,Compass Lexecon) 12:00-12:45 Competition Policy Michael Alexeev (’75, Indiana University) 12:45-13:30 The 'Oil Curse' and Institutions: A Brief Survey 13:30-15:30 Lunch. -

Russia and Saudi Arabia: Old Disenchantments, New Challenges by John W

STRATEGIC PERSPECTIVES 35 Russia and Saudi Arabia: Old Disenchantments, New Challenges by John W. Parker and Thomas F. Lynch III Center for Strategic Research Institute for National Strategic Studies National Defense University Institute for National Strategic Studies National Defense University The Institute for National Strategic Studies (INSS) is National Defense University’s (NDU’s) dedicated research arm. INSS includes the Center for Strategic Research, Center for the Study of Chinese Military Affairs, and Center for the Study of Weapons of Mass Destruction. The military and civilian analysts and staff who comprise INSS and its subcomponents execute their mission by conducting research and analysis, publishing, and participating in conferences, policy support, and outreach. The mission of INSS is to conduct strategic studies for the Secretary of Defense, Chairman of the Joint Chiefs of Staff, and the unified combatant commands in support of the academic programs at NDU and to perform outreach to other U.S. Government agencies and the broader national security community. Cover: Vladimir Putin presented an artifact made of mammoth tusk to Crown Prince Mohammad bin Salman Al Saud in Riyadh, October 14–15, 2019 (President of Russia Web site) Russia and Saudi Arabia Russia and Saudia Arabia: Old Disenchantments, New Challenges By John W. Parker and Thomas F. Lynch III Institute for National Strategic Studies Strategic Perspectives, No. 35 Series Editor: Denise Natali National Defense University Press Washington, D.C. June 2021 Opinions, conclusions, and recommendations expressed or implied within are solely those of the contributors and do not necessarily represent the views of the Defense Department or any other agency of the Federal Government. -

20E FESTIVAL

1 21e FESTIVAL DU CINÉMA RUSSE À HONFLEUR 26 NOVEMBRE - 1er DÉCEMBRE 2013 Demandes d’accréditations : [email protected] Service de presse : +33 1 55 57 05 57 Durant le Festival : +33 6 63 57 09 44 2 PRÉSENTATION Créé en 1995, le Festival du Cinéma Russe à Honfleur est le plus ancien et le plus important des festivals de cinéma russe en France. Il a pour objet de faire connaître en France le cinéma russe et de participer ainsi au développement des liens culturels entre la France et la Russie. Il enregistre plus de 10.000 entrées chaque année. Les festivaliers viennent en majorité de la Normandie et de la Région parisienne, mais aussi d'autres provinces françaises, de Belgique, de Suisse et de Russie. Le Festival rend possible la découverte par le grand public français d’œuvres de cinéastes russes inconnus en France. La présence des plus grands professionnels du cinéma russe et l’atmosphère très conviviale du Festival favorisent de nombreux échanges. Le Festival présente en compétition une sélection de films de fiction russes de l’année, ainsi que des documentaires, des dessins animés, un programme « Jeune Public », un programme « Panorama », une rétrospective thématique, et d'autres animations. La Ville de Honfleur, avec son Festival du Cinéma Russe et la Ville de Deauville, avec son Festival du Film Asiatique ont établi, depuis cinq ans, un partenariat d’échanges de films et de rencontres avec le public. Dans le cadre de ce partenariat le Festival d’Honfleur organise chaque année une projection d’un des films de compétition à Deauville. -

8-11 July 2021 Venice - Italy

3RD G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS MEETING AND SIDE EVENTS 8-11 July 2021 Venice - Italy 1 CONTENTS 1 ABOUT THE G20 Pag. 3 2 ITALIAN G20 PRESIDENCY Pag. 4 3 2021 G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS MEETINGS Pag. 4 4 3RD G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS MEETING Pag. 6 Agenda Participants 5 MEDIA Pag. 13 Accreditation Media opportunities Media centre - Map - Operating hours - Facilities and services - Media liaison officers - Information technology - Interview rooms - Host broadcaster and photographer - Venue access Host city: Venice Reach and move in Venice - Airport - Trains - Public transports - Taxi Accomodation Climate & time zone Accessibility, special requirements and emergency phone numbers 6 COVID-19 PROCEDURE Pag. 26 7 CONTACTS Pag. 26 2 1 ABOUT THE G20 Population Economy Trade 60% of the world population 80 of global GDP 75% of global exports The G20 is the international forum How the G20 works that brings together the world’s major The G20 does not have a permanent economies. Its members account for more secretariat: its agenda and activities are than 80% of world GDP, 75% of global trade established by the rotating Presidencies, in and 60% of the population of the planet. cooperation with the membership. The forum has met every year since 1999 A “Troika”, represented by the country that and includes, since 2008, a yearly Summit, holds the Presidency, its predecessor and with the participation of the respective its successor, works to ensure continuity Heads of State and Government. within the G20. The Troika countries are currently Saudi Arabia, Italy and Indonesia. -

Global University Summit-2014 «Managing Global Risks, Managing the Future

j With informational support by Global University Summit-2014 «Managing global risks, managing the future. The prognostic role of universities» Moscow, April 23-25th 2014 Global University Summit will be held within 2 days, on April 24-25th. The first day embraces the opening ceremony and 3 plenary sessions (all participants invited) while the second day will be devoted to section activities on the venues of 4 universities – MGIMO, Lomonosov Moscow State University, People’s Friendship University, National University of Science and Technology "MISiS". Russian and English are the working languages of the Summit. Wednesday, April 23th During Participants’ arrival in Moscow. Accomodation in Radisson Blu Belorusskaya and Novotel the day Moscow City Exhibition “Countries, cities, journeys” (MGIMO Chess club, MGIMO Conference Hall lobby) Exhibitions/presentation of Russian and foreign universities in MGIMO (MGIMO, New Building) 19:00 Transfer from Hotels to The Pashkov House 20:00 – Official reception on behalf of S. Sobyanin, the Mayor of Moscow 22:00 Presentation of a Report to Global University Summit-2014 participants: “Universities on the future. The future of universities”. Cultural and Exhibition Center “The Pashkov House”, Vozdvizhenka str. 3/5 - 1 22:00 Transfer to Hotels Thursday, April 24th All session are held at MGIMO Conference Hall, 76, Prospect Vernadskogo During Exhibition “Countries, cities, journeys” (MGIMO Chess club, MGIMO Conference Hall lobby) the day Exhibitions/presentation of Russian and foreign universities in MGIMO -

LEONE FILM GROUP E KEY FILMS Dal 13 Aprile Al Cinema

LEONE FILM GROUP e KEY FILMS sono lieti di presentarvi Un film scritto e diretto da ILYA NAISHULLER Prodotto da TIMUR BEKMAMBETOV con SHARLTO COPLEY DANILA KOZLOVSKY HALEY BENNETT Durata 95' Dal 13 aprile al cinema distribuito da Sito ufficiale: http://hardcore.multiplayer.it/ Pagina FB: www.facebook.com/HardcoreIlFilm Ufficio Stampa Film: Marianna Giorgi +39 338 1946062 - [email protected] Ufficio Stampa Lucky Red: Alessandra Tieri + 39.335.8480787 - [email protected] Georgette Ranucci + 39.335.5943393 - [email protected] Olga Brucciani + 39.345.8670603 - [email protected] 1 SINOSSI Non ricordi nulla. Sei appena stato salvato da tua moglie che ti ha riportato in vita (Haley Bennet). Lei sostiene che ti chiami Henry. Dopo 5 minuti vieni colpito, tua moglie rapita, e forse è il caso che tu vada a riprendertela.Chi l'ha rapita? Il suo nome è Akan (Danila Kozlovsky), un folle personaggio a capo di un gruppo di mercenari e con un piano per dominare il mondo. Ti trovi a Mosca, città a te sconosciuta e tutti intorno vogliono ucciderti. Tutti tranne un misterioso alleato inglese di nome Jimmy (Sharlto Copley). É probabile che lui sia dalla tua parte, ma non ne sei sicuro. Se riuscirai a sopravvivere alla follia, e a risolvere il mistero, potrai probabilmente capire il tuo obiettivo e la tua vera identità. Buona Fortuna. Ne avrai parecchio bisogno. Per ogni generazione c’è un flm che cambia tutto per sempre: dal 13 aprile arriva al cinema Hardcore!, il flm completamente in prima persona che ridefnisce una volta per tutte i confni del cinema d’azione. -

Macro-Advisory Ltd. Bespoke Deliverables and Services

May 2018 Russia Business Update Tom Adshead Head of Research, Macro-Advisory Ltd. [email protected] 1 New Russian Government ❑ “What?” is more important than “Who?”. Putin set out his strategy for his fourth term in office before he appointed his Prime Minister – he then chose a team that will implement the strategy ❑ Expected departures. The departure of Dvorkovich, Shuvalov and Rogozin were not unexpected. It remains to be seen if they are appointed to other posts in the Administration or Government ❑ Dependable Deputies. The Deputy PMs are likely Putin’s choice – they are all people he has known for a long time and have a track record of delivering big projects ❑ Ministers. Shows the outcome of various different influence groups – tilt towards youth. ❑ Kudrin’s position is unclear. Kudrin will be Head of Audit Chamber. In this role he can complain a lot and bring to the attention of the President waste and theft. 2 May Decrees ❑ Ambitious targets for the new government. Shortly after his inauguration, President Putin signed a decree establishing national development targets up to 2024. By signing a major decree immediately after taking office, Putin continued the tradition of eleven decrees of 7 May, 2012, which identified the main tasks of the country's socio-economic development for the years to come. The President has given the government until 1 October to come up with specific proposals for implementing the decrees ❑ Aims to be a top-five economy. The document sets several goals to achieve by 2024, with the aim of Russia’s economy being the world’s fifth-largest by the end of Putin’s term. -

Russia's International Activity in Response to the Global Financial

BULLETIN No. 37 (37) June 25, 2009 © PISM Editors: Sławomir Dębski (Editor-in-Chief), Łukasz Adamski, Bartosz Cichocki, Mateusz Gniazdowski, Beata Górka-Winter, Leszek Jesień, Agnieszka Kondek (Executive Editor), Łukasz Kulesa, Ernest Wyciszkiewicz Russia’s International Activity in Response to the Global Financial Crisis by Jarosław Ćwiek-Karpowicz Russia has striven to exploit the global financial crisis to bolster its international position. The build- ing of an international coalition of developing states, which Russia wants to head, is a means to that end. Among other things, the Russian authorities have championed new regional powers’ increased participation in international financial institutions, at the expense of the U.S. and other Western state. These efforts of the Russian Federation are laden with the risk of failure, primarily because of the Russia’s weak economic potential and vastly diverse interests of the prospective coalition members. This June Russia launched a major push on the international forum. Representatives of global business, science and politics had an opportunity to exchange views during the St. Petersburg International Economic Forum (4–6 June) dubbed “a Russian Davos.” Several days later Moscow hosted a summit of the Collective Security Treaty Organization (CSTO) and a meeting of the Inter- state Council of the Euro-Asian Economic Community (EAEC)—two foremost (from Russia’s pers- pective) initiatives to reintegrate the post-Soviet area. From there, the leaders of China, Russia, India, Brazil, Pakistan, Afghanistan and the Central Asian states met in Yekaterinburg (16–17 June) at Shanghai Cooperation Organization (SCO) and Brazil–Russia–India–China (BRIC) summits. A majority of these meetings were attended by Russian President Dmitry Medvedev whose addresses were focused on international financial crisis issues and on the need to overhaul the international financial system.