Company News SECURITIES MARKET NEWS LETTER Weekly

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

State Policy in the Arctic

INFORMATION DIGEST ECONOMIC DEVELOPMENT OF THE ARCTIC October 2020 KEY TOPICS: NORTHERN SEA ROUTE INTERNATIONAL RELATIONS INDIGENOUS PEOPLES OF THE NORTH STATE POLICY IN THE ARCTIC 30 October 2020, TASS Alexander Krutikov: large economic projects will appear in almost all Arctic regions “The system of preferences that exists in the Arctic is different from the one in the Far East. <…> The first block of support measures was put into operation. It is meant for large economic projects that significantly change the economic environment. <…> Such projects are planned for practically every Arctic region,” shared Deputy Minister for Development of the Russian Far East and Arctic Alexander Krutikov during the roundtable organized by the Ministry and the Roscongress Foundation. The second block applies to small and medium businesses. It offers premium rebates: when a small business becomes a resident of the Arctic zone, its premium rate goes as low as 3.025%. The third block includes non-tax measures. tass.ru/ekonomika/9876979 26 October 2020, Rossiyskaya Gazeta, TASS, RIA Novosti, Regnum, etc. Vladimir Putin approved Arctic Zone Development Strategy President Vladimir Putin signed a decree approving the Arctic Zone Development Strategy and ensuring national security until 2035. Within the next three months, the Government will need to approve a unified action plan to implement the basics of the state policy in the Arctic and the afore-mentioned strategy. The Government will report on their status annually. rg.ru/2020/10/26/putin-utverdil-strategiiu-razvitiia-arkticheskoj-zony.html 26 October 2020, TASS Public Council of Russia’s Arctic Zone is chaired by President of Russian Association of the Indigenous Peoples of the North Grigory Ledkov, President of the Russian Association of the Indigenous Peoples of the North, Siberia, and the Far East, is now the Chairman of the Public Council of Russia’s Arctic Zone. -

An Overview of Boards of Directors at Russia's Largest Public Companies

An Overview Of Boards Of Directors At Russia’s Largest Public Companies Andrei Rakitin Milena Barsukova Arina Mazunova Translated from Russian August 2020 Key Results According to information disclosed by 109 of Russia’s largest public companies: “Classic” board compositions of 11, nine, and seven seats prevail The total number of persons on Boards of the companies under study is not as low as it might seem: 89% of all Directors were elected to only one such Board Female Directors account for 12% and are more often elected to the audit, nomination, and remuneration committees than to the strategy committee Among Directors, there are more “humanitarians” than “techies,” while the share of “techies” among chairs is greater than across the whole sample The average age for Directors is 53, 56 for Chairmen, and 58 for Independent Directors Generation X is the most visible on Boards, and Generation Y Directors will likely quickly increase their presence if the impetuous development of digital technologies continues The share of Independent Directors barely reaches 30%, and there is an obvious lack of independence on key committees such as audit Senior Independent Directors were elected at 17% of the companies, while 89% of Chairs are not independent The average total remuneration paid to the Board of Directors is RUR 69 million, with the difference between the maximum and minimum being 18 times Twenty-four percent of the companies disclosed information on individual payments made to their Directors. According to this, the average total remuneration is approximately RUR 9 million per annum for a Director, RUR 17 million for a Chair, and RUR 11 million for an Independent Director The comparison of 2020 findings with results of a similar study published in 2012 paints an interesting dynamic picture. -

Russian Withholding Tax Refund

Russian withholding tax refund Tax & Legal If you or your clients invested in Russian securities and are entitled to a substantial dividend or interest income, there is a chance that you overpaid your taxes and may qualify for a tax refund © 2018 Deloitte Consulting LLC Background Investors may apply a According to the The Russian The tax refund reduced tax rate for Russian tax withholding tax rate is practice in Russia is their interest and/or authorities, they are set at 15% on not well-developed: dividend income, ready to reimburse dividends and 20 the tax legislation depending on the overpaid taxes, if a percent on interest. does not provide for a conditions set by the full package of Effective from 1 specific list of Russian Tax Code or documents confirming January 2014, the documents to be applicable Double Tax the income payment duties of the tax collected and Treaties. Calculations chain and the agent for WHT requirements to be of a standard Russian investor’s rights to purposes were met. For these rate or the standard the income is transferred to the reasons, the process reduced Double Tax submitted. local Russian can be lengthy and Treaty rate, as well as custodian or, in a sometimes fruitless. submission of claims limited number of However, the trend is on tax can be cases, to the reassuring: the refunded, should be fiduciary, broker or number of successful made by investors issuer. refund claims and themselves within positive court three calendar years, decisions is growing. following the year in which it was withheld. -

Russia and Saudi Arabia: Old Disenchantments, New Challenges by John W

STRATEGIC PERSPECTIVES 35 Russia and Saudi Arabia: Old Disenchantments, New Challenges by John W. Parker and Thomas F. Lynch III Center for Strategic Research Institute for National Strategic Studies National Defense University Institute for National Strategic Studies National Defense University The Institute for National Strategic Studies (INSS) is National Defense University’s (NDU’s) dedicated research arm. INSS includes the Center for Strategic Research, Center for the Study of Chinese Military Affairs, and Center for the Study of Weapons of Mass Destruction. The military and civilian analysts and staff who comprise INSS and its subcomponents execute their mission by conducting research and analysis, publishing, and participating in conferences, policy support, and outreach. The mission of INSS is to conduct strategic studies for the Secretary of Defense, Chairman of the Joint Chiefs of Staff, and the unified combatant commands in support of the academic programs at NDU and to perform outreach to other U.S. Government agencies and the broader national security community. Cover: Vladimir Putin presented an artifact made of mammoth tusk to Crown Prince Mohammad bin Salman Al Saud in Riyadh, October 14–15, 2019 (President of Russia Web site) Russia and Saudi Arabia Russia and Saudia Arabia: Old Disenchantments, New Challenges By John W. Parker and Thomas F. Lynch III Institute for National Strategic Studies Strategic Perspectives, No. 35 Series Editor: Denise Natali National Defense University Press Washington, D.C. June 2021 Opinions, conclusions, and recommendations expressed or implied within are solely those of the contributors and do not necessarily represent the views of the Defense Department or any other agency of the Federal Government. -

Programme 2019 Pdf 0.16 MB

Programme of the 16th Annual Meeting of the Valdai Discussion Club “The Dawn of the East and the World Political Order” Sochi, September 30 – October 3, 2019 September 30, Monday 10:00 – 10:10 Opening of the 16th Annual Meeting of the Valdai Club Andrey Bystritskiy, Chairman of the Board of the Foundation for Development and Support of the Valdai Discussion Club 10:10 – 12:00 Session 1. The Strategic Landscape: An Eastern Perspective. Presentation of the Valdai Club Report The world politics is experiencing fundamental changes. They are not only about the shifting balance of forces or redistribution of financial streams and economic capabilities. Countries, whose political and strategic culture is fundamentally different from the western notions, which have been dominant in the previous centuries, are beginning to play the leading roles on the international arena. The future world order will emerge in an environment of pluralism of ideas, taking into account views and positions of the leading non-western countries. What are these views? What does Russia’s role look like in these systems of coordinates? Speakers: • Yuichi Hosoya, Professor of International Politics, Keio University • C Raja Mohan, Director, Institute of South Asian Studies, National University of Singapore • Wang Yiwei, Director, Institute of International Affairs and Centre for European Union Studies, Renmin University of China • Hasan Basri Yalçın, Director of Strategic Studies, SETA Foundation for Political, Economic and Social Research Moderator: Fyodor Lukyanov, Research Director of the Foundation for Development and Support of the Valdai Discussion Club 2 12:30 – 14:30 Session 2. Middle East as a World Politics Lab Since the early 21st century, the Middle East has been in the international spotlight. -

Emerging Index - QSR

2 FTSE Russell Publications 19 August 2021 FTSE RAFI Emerging Index - QSR Indicative Index Weight Data as at Closing on 30 June 2021 Index Index Index Constituent Country Constituent Country Constituent Country weight (%) weight (%) weight (%) Absa Group Limited 0.29 SOUTH BRF S.A. 0.21 BRAZIL China Taiping Insurance Holdings (Red 0.16 CHINA AFRICA BTG Pactual Participations UNT11 0.09 BRAZIL Chip) Acer 0.07 TAIWAN BYD (A) (SC SZ) 0.03 CHINA China Tower (H) 0.17 CHINA Adaro Energy PT 0.04 INDONESIA BYD (H) 0.12 CHINA China Vanke (A) (SC SZ) 0.09 CHINA ADVANCED INFO SERVICE 0.16 THAILAND Canadian Solar (N Shares) 0.08 CHINA China Vanke (H) 0.2 CHINA Aeroflot Russian Airlines 0.09 RUSSIA Capitec Bank Hldgs Ltd 0.05 SOUTH Chongqing Rural Commercial Bank (A) (SC 0.01 CHINA Agile Group Holdings (P Chip) 0.04 CHINA AFRICA SH) Agricultural Bank of China (A) (SC SH) 0.27 CHINA Catcher Technology 0.2 TAIWAN Chongqing Rural Commercial Bank (H) 0.04 CHINA Agricultural Bank of China (H) 0.66 CHINA Cathay Financial Holding 0.29 TAIWAN Chunghwa Telecom 0.32 TAIWAN Air China (A) (SC SH) 0.02 CHINA CCR SA 0.14 BRAZIL Cia Paranaense de Energia 0.01 BRAZIL Air China (H) 0.06 CHINA Cemex Sa Cpo Line 0.7 MEXICO Cia Paranaense de Energia (B) 0.07 BRAZIL Airports of Thailand 0.04 THAILAND Cemig ON 0.03 BRAZIL Cielo SA 0.13 BRAZIL Akbank 0.18 TURKEY Cemig PN 0.18 BRAZIL CIFI Holdings (Group) (P Chip) 0.03 CHINA Al Rajhi Banking & Investment Corp 0.52 SAUDI Cencosud 0.04 CHILE CIMB Group Holdings 0.11 MALAYSIA ARABIA Centrais Eletricas Brasileiras S.A. -

Russia & Cis' Largest Virtual Capital Markets Event

REGISTER YOUR PLACE TODAY AT WWW.BONDSLOANSRUSSIA.COM RUSSIA & CIS’ LARGEST VIRTUAL CAPITAL MARKETS EVENT 500+ 40+ 250+ 100+ 2,100+ SENIOR WORLD CLASS SOVEREIGN, CORPORATE INVESTORS CONTACTS AVAILABLE TO ATTENDEES SPEAKERS & FI BORROWERS NETWORK WITH ONLINE It’s great to have Bonds & Loans with us in all times - good and bad. Our team has particularly enjoyed the networking opportunities, the program is excellent too, and you’ve proved once again your reputation of the leading capital markets event in Russia. Dmitri Surkov, Global Head of Revenue Management, Fitch Ratings Gold Sponsor: Silver Sponsors: Bronze Sponsors: Corporate Sponsors: www.BondsLoansRussia.com BRINGING GLOBAL FINANCE LEADERS TOGETHER WITH THE RUSSIA & CIS CAPITAL MARKETS COMMUNITY Meet senior decision-makers from Russia & the CIS sovereigns, corporates and banks; share knowledge; debate; network; and move your business forward in the current economic climate without having to travel. 500+ 40+ 250+ SENIOR WORLD CLASS SOVEREIGN, CORPORATE 100+ ATTENDEES SPEAKERS & FI BORROWERS INVESTORS Access top market practitioners from Industry leading speakers will share Hear first-hand how local and international Leverage our concierge across the globe who are active in “on-the-ground” market intelligence industry leaders are navigating Russia & the meeting service the Russia & CIS markets, including: and updates on Russia & the CIS’s CIS’s current economic climate/what they to engage with global senior borrowers, investors, bankers & economic backdrop. Gain actionable expect in -

Russia Macro-Politics: Political Pragmatism Or, Economic Necessity

The National Projects December 2019 Population and GDP (2020E data) The long and winding road Population 146.8 GDP, Nominal, US$ bln $1,781 Plans are worthless. Planning is essential” GDP/Capita, US$ $12,132 Dwight D. Eisenhower GDP/Capita, PPP, US$ $27,147 Source: World Bank, World-o-Meters, MA The National Projects (NP) are at the core of the Russian government’s efforts to pull the economy out of the current slump, National Projects - Spending* to create sustainable diversified long-term growth and to improve Rub, Bln US$ Bln lifestyle conditions in Russia. It is the key element of President Putin’s Human Capital 5,729 $88 effort to establish his legacy. Health 1,726 $27 Education 785 $12 We are now initiating coverage of the National Projects strategy. We Demographics 3,105 $48 will provide regular detailed updates about the progress in each of Culture 114 $2 the major project sectors, focusing especially on the opportunities Quality of Life 9,887 $152 Safer Roads 4,780 $74 for foreign investors and on the mechanisms for them to take part. Housing 1,066 $16 ▪ What is it? A US$390 billion program of public spending, designed Ecology 4,041 $62 to stimulate investment, build infrastructure and improve health Economic Growth 10,109 $156 and well-being by 2024, i.e. the end of the current presidential Science 636 $10 Small Business Development 482 $7 term. Digital Economy 1,635 $25 ▪ Is this a return to Soviet-style planning? For some of the NPs, Labour productivity 52 $1 Export Support 957 $15 especially those involving infrastructure, it certainly looks like it. -

US Sanctions on Russia

U.S. Sanctions on Russia Updated January 17, 2020 Congressional Research Service https://crsreports.congress.gov R45415 SUMMARY R45415 U.S. Sanctions on Russia January 17, 2020 Sanctions are a central element of U.S. policy to counter and deter malign Russian behavior. The United States has imposed sanctions on Russia mainly in response to Russia’s 2014 invasion of Cory Welt, Coordinator Ukraine, to reverse and deter further Russian aggression in Ukraine, and to deter Russian Specialist in European aggression against other countries. The United States also has imposed sanctions on Russia in Affairs response to (and to deter) election interference and other malicious cyber-enabled activities, human rights abuses, the use of a chemical weapon, weapons proliferation, illicit trade with North Korea, and support to Syria and Venezuela. Most Members of Congress support a robust Kristin Archick Specialist in European use of sanctions amid concerns about Russia’s international behavior and geostrategic intentions. Affairs Sanctions related to Russia’s invasion of Ukraine are based mainly on four executive orders (EOs) that President Obama issued in 2014. That year, Congress also passed and President Rebecca M. Nelson Obama signed into law two acts establishing sanctions in response to Russia’s invasion of Specialist in International Ukraine: the Support for the Sovereignty, Integrity, Democracy, and Economic Stability of Trade and Finance Ukraine Act of 2014 (SSIDES; P.L. 113-95/H.R. 4152) and the Ukraine Freedom Support Act of 2014 (UFSA; P.L. 113-272/H.R. 5859). Dianne E. Rennack Specialist in Foreign Policy In 2017, Congress passed and President Trump signed into law the Countering Russian Influence Legislation in Europe and Eurasia Act of 2017 (CRIEEA; P.L. -

Share Listing

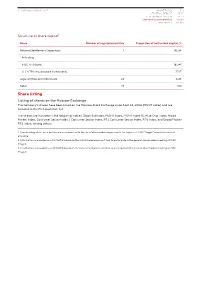

Annual Report 2018 | MAGNIT MAGNIT TODAY 3-11 99 STRATEGIC REPORT 13-27 PERFORMANCE REVIEW 29-53 CORPORATE GOVERNANCE 55-113 APPENDICES 115-189 Structure of share capital1 Name Number of registered entities Proportion of authorized capital, % National Settlement Depositary 1 95.54 Including: PJSC VTB Bank 18.342 LLC VTB Infrastructure Investments 7.723 Legal entities and individuals 24 4.46 Total: 25 100 Share listing Listing of shares on the Moscow Exchange The Company’s shares have been listed on the Moscow Stock Exchange since April 24, 2006 (MGNT ticker) and are included in the first quotation list. The shares are included in the following indices: Stock Subindex, MOEX Index, MOEX Index 10, Blue Chip Index, Broad Market Index, Consumer Sector Index / Consumer Sector Index, RTS Consumer Sector Index, RTS Index, and Broad Market RTS Index, among others. 1. Shareholding structure is provided in accordance with the list of shareholders registered in the register of PJSC “Magnit” shareholders as of 31.12.2018 2. Information is provided as of 12.11.2018 based on the list of shareholders entitled to participate in the general shareholders meeting of PJSC “Magnit 3. Information is provided as of 12.11.2018 based on the list of shareholders entitled to participate in the general shareholders meeting of PJSC “Magnit 100 101 Weight of shares in indices Ticker Index name Weight in index, % RDXUSD Russian Depositary Index USD 2.85 RDX Russian Depositary Index EUR 2.85 NU137529 MSCI EM IMI (VRS Taxes) Net Return USD Index 0.09 RIOB FTSE Russia IOB -

Program Structure* August 8, 2019

PROGRAM STRUCTURE* AUGUST 8, 2019 09:00 Registration of participants Plenary session 10:00-12:00 Digital transformation and reset of the legislation: scenarios for the development of a civilized taxi market in Russia 12:00-12:30 Coffee-break / Visiting the exposition Working session Round table 12:30-14:00 Business to business: the best products and Urban transport of the future: innovation against services for the taxi industry habits 14:00-14:45 Lunch Working session Panel session 14:45-16:15 Control 2.0: Technological control and data Taxi fares: Is there justice and who will establish it? usage in the taxi industry 16:15-16:30 Break 16:30-18:00 Panel discussion "What is a legal taxi?" AUGUST 9, 2019 09:30 Registration of participants Plenary session 10:30-12:00 Development trends of the world taxi market 12:00-12:15 Coffee-break Working session Working session 12:15-13:45 Regional markets: common rules - different Driver: employee, contractor, partner or slave to the solutions system? 13:45-14:15 Lunch Working session Panel discussion 14:15-15:45 Taxi insurance system transformation: Play by own rules: how to create a competitive advantage challenges and solutions in the modern market 15:45-16:00 Break Panel session Working session 16:00-17:00 Mobility 4.0: transport as an integrated Finance and taxes: calculations and reporting in the taxi service business 17:00-17:10 Break 17:10-18:00 MEFT Public Council Meeting 18:00-19:00 Closing cocktail *subject to change without notice AUGUST 8, 2019 Plenary session 10:00 – 12:00 Digital transformation -

25 YEARS of GROWTH in HARMONY with OUR CUSTOMERS Highlights 1

ANNUAL REPORT 2016 25 YEARS OF GROWTH IN HARMONY WITH OUR CUSTOMERS Highlights 1. Strategic Report 5. For Shareholders and Investors Key Financial Performance Indicators 2. Overview of Operations 6. Sustainable Development Mission and Values 3. Financial Results Contacts 2 / 197 4. Corporate Governance System Appendices www.mkb.ru Annual Report 2016 / Table of Contents Table of Contents Highlights Key Financial Performance Indicators Mission and Values 1. Strategic Report 2. Overview of operations 5. For shareholders and investors Appendices 1.1. Address of the Chairman of the 2.1. Corporate banking 6. Sustainable development Appendix 1. Supervisory Board IFRS Statements 2.2. Retail banking 6.1. Human Resources 1.2. Address of the Chairman of the Appendix 2. Management Board 2.3. Cash handling 6.2. Corporate Culture RAS Statements and Social Responsibility 1.3. Management Responsibility 3. Financial results Appendix 3. Statement 6.3. Information technologies List of interested party transactions 3.1. Income statement analysis made in the reporting year (2016) 1.4. Economy and banking sector 6.4. Society 3.2. Key Results List of major transactions made in 1.5. Business model. 6.5. Environmental Management the reporting year (2016) Competitive advantages. 3.3. Income statement analysis Position in the industry. Contacts List of transactions requiring 3.4. Structure of assets and liabilities approval under the Charter made in 1.6. Strategy under IFRS the reporting year (2016) 1.7. Risk Management 4. Corporate governance system Appendix 4. Report on Compliance with the Principles and Recommendations of the Corporate Governance Code. Highlights 1. Strategic Report 5.