An Overview of Boards of Directors at Russia's Largest Public Companies

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Expiry Notice

Expiry Notice 19 January 2018 London Stock Exchange Derivatives Expiration prices for IOB Derivatives Please find below expiration prices for IOB products expiring in January 2018: Underlying Code Underlying Name Expiration Price AFID AFI DEVELOPMENT PLC 0.1800 ATAD PJSC TATNEFT 58.2800 FIVE X5 RETAIL GROUP NV 39.2400 GAZ GAZPROM NEFT 23.4000 GLTR GLOBALTRANS INVESTMENT PLC 9.9500 HSBK JSC HALYK SAVINGS BANK OF KAZAKHSTAN 12.4000 HYDR PJSC RUSHYDRO 1.3440 KMG JSC KAZMUNAIGAS EXPLORATION PROD 12.9000 LKOD PJSC LUKOIL 67.2000 LSRG LSR GROUP 2.9000 MAIL MAIL.RU GROUP LIMITED 32.0000 MFON MEGAFON 9.2000 MGNT PJSC MAGNIT 26.4000 MHPC MHP SA 12.8000 MDMG MD MEDICAL GROUP INVESTMENTS PLC 10.5000 MMK OJSC MAGNITOGORSK IRON AND STEEL WORKS 10.3000 MNOD MMC NORILSK NICKEL 20.2300 NCSP PJSC NOVOROSSIYSK COMM. SEA PORT 12.9000 NLMK NOVOLIPETSK STEEL 27.4000 NVTK OAO NOVATEK 128.1000 OGZD GAZPROM 5.2300 PLZL POLYUS PJSC 38.7000 RIGD RELIANCE INDUSTRIES 28.7000 RKMD ROSTELEKOM 6.9800 ROSN ROSNEFT OJSC 5.7920 SBER SBERBANK 18.6900 SGGD SURGUTNEFTEGAZ 5.2450 SMSN SAMSUNG ELECTRONICS CO 1148.0000 SSA SISTEMA JSFC 4.4200 SVST PAO SEVERSTAL 16.8200 TCS TCS GROUP HOLDING 19.3000 TMKS OAO TMK 5.4400 TRCN PJSC TRANSCONTAINER 8.0100 VTBR JSC VTB BANK 1.9370 Underlying code Underlying Name Expiration Price D7LKOD YEAR 17 DIVIDEND LUKOIL FUTURE 3.2643 YEAR 17 DIVIDEND MMC NORILSK NICKEL D7MNOD 1.8622 FUTURE D7OGZD YEAR 17 DIVIDEND GAZPROM FUTURE 0.2679 D7ROSN YEAR 17 DIVIDEND ROSNEFT FUTURE 0.1672 D7SBER YEAR 17 DIVIDEND SBERBANK FUTURE 0.3980 D7SGGD YEAR 17 DIVIDEND SURGUTNEFTEGAZ FUTURE 0.1000 D7VTBR YEAR 17 DIVIDEND VTB BANK FUTURE 0.0414 Members are asked to note that reports showing exercise/assignments should be available by approx. -

Capital Markets Day Presentation (Moscow)

Capital markets day Efficiency and stability are the name of the game December 8, 2016 Moscow, Russia Capital markets day Agenda Nikolay Shulginov Chairman of • Opening remarks. Preliminary results of 1 the Management Board – RusHydro Group in 2016 General Director George Rizhinashvili • RusHydro Group Development Strategy Management Board member, 2 • Overview of capital raising to refinance RAO ES First Deputy General Director East debt Sergey Kirov Management Board member, • Optimization of capital and operating costs 3 First Deputy General Director • Operating efficiency improvement plan Q&A session 2 Capital markets day RusHydro: the leading Russian utilities and renewables company No. 2 Russian power generation company, GW No.3 world’s hydropower co. by capacity, GW 15% 15% 11% 10% 7% 6% 38.9 38.2(2) 29 27 19 16 38 36 30(2) 29 28 26 Source: companies’ data, System operator Source: companies’ data 15% - share of total installed capacity of Russia No.6 heat producer in the world, mn GCal 12% of total Russia’s electricity output in 2015 12% (2) 1,050 TWh 117 108 45 39 37 31 25 Source: companies’ data Source: companies’ data, System operator 3 Capital markets day RusHydro – a leading Russian genco Russia’s largest genco and one of the world’s largest publicly-traded predominantly hydro generation companies, with capacity of 38.7 GW (ca. 16% of the Russian total) The biggest winner from electricity market liberalization in Russia due to extensive exposure to low- cost hydro generation A developing and succesful dividend story: 5 consecutive -

Energy Without Borders

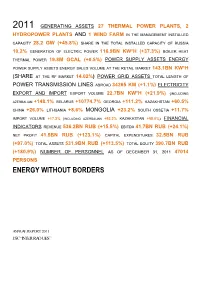

2011 GENERATING ASSETS 27 THERMAL POWER PLANTS, 2 HYDROPOWER PLANTS AND 1 WIND FARM IN THE MANAGEMENT INSTALLED CAPACITY 28.2 GW (+45.8%) SHARE IN THE TOTAL INSTALLED CAPACITY OF RUSSIA 10.2% GENERATION OF ELECTRIC POWER 116.9BN KW*H (+37.3%) BOILER HEAT THERMAL POWER 19.8M GCAL (+0.5%) POWER SUPPLY ASSETS ENERGY POWER SUPPLY ASSETS ENERGY SALES VOLUME AT THE RETAIL MARKET 143.1BN KW*H (SHARE AT THE RF MARKET 14.02%) POWER GRID ASSETS TOTAL LENGTH OF POWER TRANSMISSION LINES ABROAD 34265 KM (+1.1%) ELECTRICITY EXPORT AND IMPORT EXPORT VOLUME 22.7BN KW*H (+21.9%) (INCLUDING AZERBAIJAN +148.1% BELARUS +10774.7% GEORGIA +111.2% KAZAKHSTAN +60.5% CHINA +26.0% LITHUANIA +8.6% MONGOLIA +23.2% SOUTH OSSETIA +11.7% IMPORT VOLUME +17.2% (INCLUDING AZERBAIJAN +93.2% KAZAKHSTAN +58.0%) FINANCIAL INDICATORS REVENUE 536.2BN RUB (+15.5%) EBITDA 41.7BN RUB (+24.1%) NET PROFIT 41.5BN RUB (+123.1%) CAPITAL EXPENDITURES 32.5BN RUB (+97.0%) TOTAL ASSETS 531.9BN RUB (+113.5%) TOTAL EQUITY 390.7BN RUB (+180.9%) NUMBER OF PERSONNEL AS OF DECEMBER 31, 2011 47014 PERSONS ENERGY WITHOUT BORDERS ANNUAL REPORT 2011 JSC “INTER RAO UES” Contents ENERGY WITHOUT BORDERS.........................................................................................................................................................1 ADDRESS BY THE CHAIRMAN OF THE BOARD OF DIRECTORS AND THE CHAIRMAN OF THE MANAGEMENT BOARD OF JSC “INTER RAO UES”..............................................................................................................8 1. General Information about the Company and its Place in the Industry...........................................................10 1.1. Brief History of the Company......................................................................................................................... 10 1.2. Business Model of the Group..........................................................................................................................12 1.4. -

Notes on Moscow Exchange Index Review

Notes on Moscow Exchange index review Moscow Exchange approves the updated list of index components and free float ratios effective from 16 March 2018. X5 Retail Group N.V. (DRs) will be added to Moscow Exchange indices with the expected weight of 1.13 per cent. As these securities were offered initially, they were added without being in the waiting list under consideration. Thus, from 16 March the indices will comprise 46 (component stocks. The MOEX Russia and RTS Index moved to a floating number of component stocks in December 2017. En+ Group plc (DRs) will be in the waiting list to be added to Moscow Exchange indices, as their liquidity rose notably over recent three months. NCSP Group (ords) with low liquidity, ROSSETI (ords) and RosAgro PLC with their weights now below the minimum permissible level (0.2 per cent) will be under consideration to be excluded from the MOEX Russia Index and RTS Index. The Blue Chip Index constituents remain unaltered. X5 Retail Group (DRs), GAZ (ords), Obuvrus LLC (ords) and TNS energo (ords) will be added to the Broad Market Index, while Common of DIXY Group and Uralkali will be removed due to delisting expected. TransContainer (ords), as its free float sank below the minimum threshold of 5 per cent, and Southern Urals Nickel Plant (ords), as its liquidity ratio declined, will be also excluded. LSR Group (ords) will be incuded into SMID Index, while SOLLERS and DIXY Group (ords) will be excluded due to low liquidity ratio. X5 Retail Group (DRs) and Obuvrus LLC (ords) will be added to the Consumer & Retail Index, while DIXY Group (ords) will be removed from the Index. -

Annual Report

2014 ANNUAL REPORT TABLE OF CONTENTS Sistema today 2 Corporate governance system 91 History timeline 4 Corporate governance principles 92 Company structure 8 General Meeting of shareholders 94 President’s speech 10 Board of Directors 96 Strategic Review 11 Commitees of the Board of Directors 99 Strategy 12 President and the Management Board 101 Sistema’s financial results 20 Internal control and audit 103 Shareholder capital and securities 24 Development of the corporate 104 governance system in 2014 Our investments 27 Remuneration 105 MTS 28 Risks 106 Detsky Mir 34 Sustainable development 113 Medsi Group 38 Responsible investor 114 Lesinvest Group (Segezha) 44 Social investment 115 Bashkirian Power Grid Company 52 Education, science, innovation 115 RTI 56 Culture 117 SG-trans 60 Environment 119 MTS Bank 64 Society 121 RZ Agro Holding 68 Appendices 124 Targin 72 Binnopharm 76 Real estate 80 Sistema Shyam TeleServices 84 Sistema Mass Media 88 1 SISTEMA TODAY Established in 1993, today Sistema including telecommunications, companies. Sistema’s competencies is a large private investor operating utilities, retail, high tech, pulp and focus on improvement of the in the real sector of the Russian paper, pharmaceuticals, healthcare, operational efficiency of acquired economy. Sistema’s investment railway transportation, agriculture, assets through restructuring and portfolio comprises stakes in finance, mass media, tourism, attracting industry partners to predominantly Russian companies etc. Sistema is the controlling enhance expertise and reduce -

Tatneft Group IFRS CONSOLIDATED INTERIM CONDENSED

Tatneft Group IFRS CONSOLIDATED INTERIM CONDENSED FINANCIAL STATEMENTS (UNAUDITED) AS OF AND FOR THE THREE AND SIX MONTHS ENDED 30 JUNE 2019 Contents Report on Review of Consolidated Interim Condensed Financial Statements Consolidated Interim Condensed Financial Statements Consolidated Interim Condensed Statement of Financial Position (unaudited) ........................................ 1 Consolidated Interim Condensed Statement of Profit or Loss and Other Comprehensive Income (unaudited) ..................................................................................................................................... 2 Consolidated Interim Condensed Statement of Changes in Equity (unaudited) ........................................ 4 Consolidated Interim Condensed Statement of Cash Flows (unaudited) .................................................. 5 Notes to the Consolidated Interim Condensed Financial Statements (unaudited) Note 1: Organisation ................................................................................................................................. 7 Note 2: Basis of preparation ...................................................................................................................... 7 Note 3: Adoption of new or revised standards and interpretations .......................................................... 10 Note 4: Cash and cash equivalents .......................................................................................................... 12 Note 5: Accounts receivable ................................................................................................................... -

Annual Report 2014

APPROVED: by the General Shareholders’ Meeting of Open Joint-Stock Company Enel Russia on June 17, 2015 Minutes № 2/15 dd. June 17, 2015 PRELIMINARY APPROVED: by the OJSC Enel Russia Board of Directors on April 22, 2015 Minutes № 05/15 dd. April 22, 2015 2014 ANNUAL REPORT General Director of OJSC Enel Russia June ___, 2015 __________ / K. Palasciano Villamagna/ Chief Accountant of OJSC Enel Russia June ___, 2015 _________ / E.A. Dubtsova/ Moscow 2015 TABLE OF CONTENTS 1. Address of the company management to shareholders .................................................................... 4 1.1. Address of the chairman of the board of directors .................................................................... 4 1.2. Address of the general director .................................................................................................. 6 2. Calendar of events ............................................................................................................................ 8 3. The company’s background............................................................................................................ 11 4. The board of directors report: results of the company priority activities ...................................... 12 4.1. Financial and economic performance of the company ............................................................ 12 4.1.1. Analysis of financial performance dynamics in comparison with the previous period........ 12 4.1.2. Dividend history .................................................................................................................. -

Atti Parlamentari

Camera dei Deputati – 530529 – Senato della Repubblica XVII LEGISLATURA - DISEGNI DI LEGGE E RELAZIONI - DOCUMENTI - DOC. XV N. 614 %di Denominazione Capitale Metodo di Detenuta %di possesso sociale Sede legale Nazione sociale Valuta Attività consol(damento da possesso del Gruppo Enel Green Power Rio de Janeiro Brasile 144.640.892,85 BRL Produzione e vendita integrale Enel Green 1,00% 100,00% Cristal E61ica SA di energia elettrica da Power fonte rinnovabile Desenvolvimento ;Ltda Enel Green 99,00% PowerBrasil Participaçòes Ltda Enel Green Power Rio de Janeiro Brasile 1.000.000,00 BRL Produzione di energia Integrale Enel Green 99,90% 99,90% Cristalandia I E6lica SA elettrica da fonte Power Brasi! rinnovabile Participaçées Ltda Enel Green Power Rio de Janeiro Brasile 1.000.000,00 BRL Produzione di energia Integrale Enel Green 99,90% 99,90% Cristalandia Il E61ica SA elettrica da fonte Power Brasi! rinnovabile Participaçoes Ltda Enel Green Power Rio de Janeiro Brasile 70.000.000,00 BRL Produzione di energia Integrale Enel Green 1,00% 100,00% Damascena E61ica SA elettrica da fonte Power rinnovabile Desenvolvimento Ltda Enel Green 99,00% Power Brasil Participaçées Ltda Enel Green Power del Santiago Cile 1.000.000,00 CLP Produzione di energia Integrale Enel Green 100,00% 99,91% Sur SpA (già Parque elettrica da fonte Power Chile Ltda E61ico Renaico SpAJ rinnovabile Enel Green Power Rio de Janeiro Brasile 70.379.344,85 BRL Produzione di energia Integrale Enel Green 99,90% 99,90% Delfina A E6lica SA elettrica da fonte Power Brasil rinnovabile Participaçoes -

PRESS RELEASE JSC ALROSA Announces Purchase of a 25

PRESS RELEASE JSC ALROSA Announces Purchase of a 25 Percent Interest in OJSC Polyus Gold August, 2007, Moscow. Joint-Stock Company ALROSA signed an agreement with ONEXIM Group to buy a 25 percent stake in the Open Joint-Stock Company Polyus Gold (RTS, MICEX, and LSE – PLZL), Russia’s largest gold producer. “This deal was implemented as part of the development strategy approved by the Supervisory Board of JSC ALROSA. Among other things, ALROSA focuses on diversifying into other sectors. The purchase of a significant stake in Polyus Gold, which pursues an effective production strategy, will enable ALROSA to access a market with considerable long-term prospects and will further boost the development and economic growth of regions in Central and Eastern Siberia,” said President of ALROSA Sergei Vybornov. Open Joint-Stock Company Polyus Gold (RTS, MICEX, and LSE – PLZL) – is the leading gold producer in Russia and one of the biggest players in gold mining in the world in terms of deposits and production. The asset portfolio of Polyus Gold includes ore and alluvial gold deposits in the Krasnoyarsk Territory, the Irkutsk, Magadan, and Amur regions, and in the Republic of Sakha (Yakutia), where the company operates gold exploration and mining projects. As of January 1, 2007, the mineral resource base of OJSC Polyus Gold comprises 3,000.7 tons of gold in B+C1+C2 reserves, including 2,149 tons of B+C1 reserves. Joint-Stock Company ALROSA – is a global leader in diamond exploration, mining and sales of rough diamonds, and in cut diamond manufacture. ALROSA accounts for 97 percent of Russia’s rough diamond production and for 25 percent of the global output of rough diamonds. -

Global Expansion of Russian Multinationals After the Crisis: Results of 2011

Global Expansion of Russian Multinationals after the Crisis: Results of 2011 Report dated April 16, 2013 Moscow and New York, April 16, 2013 The Institute of World Economy and International Relations (IMEMO) of the Russian Academy of Sciences, Moscow, and the Vale Columbia Center on Sustainable International Investment (VCC), a joint center of Columbia Law School and the Earth Institute at Columbia University in New York, are releasing the results of their third survey of Russian multinationals today.1 The survey, conducted from November 2012 to February 2013, is part of a long-term study of the global expansion of emerging market non-financial multinational enterprises (MNEs).2 The present report covers the period 2009-2011. Highlights Russia is one of the leading emerging markets in terms of outward foreign direct investments (FDI). Such a position is supported not by several multinational giants but by dozens of Russian MNEs in various industries. Foreign assets of the top 20 Russian non-financial MNEs grew every year covered by this report and reached US$ 111 billion at the end of 2011 (Table 1). Large Russian exporters usually use FDI in support of their foreign activities. As a result, oil and gas and steel companies with considerable exports are among the leading Russian MNEs. However, representatives of other industries also have significant foreign assets. Many companies remained “regional” MNEs. As a result, more than 66% of the ranked companies’ foreign assets were in Europe and Central Asia, with 28% in former republics of the Soviet Union (Annex table 2). Due to the popularity of off-shore jurisdictions to Russian MNEs, some Caribbean islands and Cyprus attracted many Russian subsidiaries with low levels of foreign assets. -

Enel Russia Discloses Its 2020 Financial Results

Media Relations PJSC Enel Russia Pavlovskaya 7, bld. 1, Moscow, Russia T +7(495) 539 31 31 ext. 7824 [email protected] enel.ru ENEL RUSSIA DISCLOSES ITS 2020 FINANCIAL RESULTS • 2020 financial results are expectedly lower compared to the previous year, mostly due to change in assets perimeter • Enel Russia’s performance was affected by weak market context due to the continuing low economic activity caused by the COVID-19 pandemic • Throughout 2020 Enel Russia was focused on ensuring continuous business operations and on completing its ongoing construction projects, considering the outbreak of COVID-19 MAIN FINANCIAL HIGHLIGHTS (millions of RUB) 2020 2019 Change Revenues 44,037 65,835 -33.1% EBITDA 9,017 15,318 -41.1% EBIT 5,532 2,842 +94.7% Ordinary EBIT 6,595 11,039 -40.3% Net income 3,625 896 +304.6% Ordinary net income 4,467 7,453 -40.1% Net debt at the end of the period 13,697 4,171 +228.4% Stephane Zweguintzow, General Director of Enel Russia, said: “The change in the company’s assets perimeter after the disposal of Reftinskaya GRES and lower economic activity due to the COVID-19 pandemic were the main factors impacting our ordinary 2020 results. In a challenging context characterized by the pandemic, our company focused on ensuring continuous business operations and actively invested in its renewable projects realization.” Moscow, March 16th, 2021 – PJSC Enel Russia has published its audited consolidated financial statements for 2020 in accordance with the International Financial Reporting Standards (IFRS). • Revenues showed negative dynamics year-over-year mostly due to: – a decrease in electricity and capacity sales considering the company’s new perimeter after Reftinskaya GRES disposal; – a decline in market electricity (DAM) prices, as a result of lower demand in the energy system, caused by weak economic activity due to the COVID-19 pandemic, coupled with stable supply by 1 PJSC Enel Russia – Pavlovskaya 7, bld. -

Russia & Cis' Largest Virtual Capital Markets Event

REGISTER YOUR PLACE TODAY AT WWW.BONDSLOANSRUSSIA.COM RUSSIA & CIS’ LARGEST VIRTUAL CAPITAL MARKETS EVENT 500+ 40+ 250+ 100+ 2,100+ SENIOR WORLD CLASS SOVEREIGN, CORPORATE INVESTORS CONTACTS AVAILABLE TO ATTENDEES SPEAKERS & FI BORROWERS NETWORK WITH ONLINE It’s great to have Bonds & Loans with us in all times - good and bad. Our team has particularly enjoyed the networking opportunities, the program is excellent too, and you’ve proved once again your reputation of the leading capital markets event in Russia. Dmitri Surkov, Global Head of Revenue Management, Fitch Ratings Gold Sponsor: Silver Sponsors: Bronze Sponsors: Corporate Sponsors: www.BondsLoansRussia.com BRINGING GLOBAL FINANCE LEADERS TOGETHER WITH THE RUSSIA & CIS CAPITAL MARKETS COMMUNITY Meet senior decision-makers from Russia & the CIS sovereigns, corporates and banks; share knowledge; debate; network; and move your business forward in the current economic climate without having to travel. 500+ 40+ 250+ SENIOR WORLD CLASS SOVEREIGN, CORPORATE 100+ ATTENDEES SPEAKERS & FI BORROWERS INVESTORS Access top market practitioners from Industry leading speakers will share Hear first-hand how local and international Leverage our concierge across the globe who are active in “on-the-ground” market intelligence industry leaders are navigating Russia & the meeting service the Russia & CIS markets, including: and updates on Russia & the CIS’s CIS’s current economic climate/what they to engage with global senior borrowers, investors, bankers & economic backdrop. Gain actionable expect in