Global Expansion of Russian Multinationals After the Crisis: Results of 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

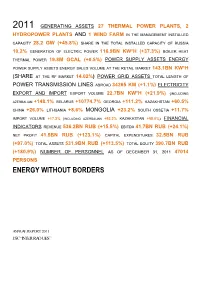

Energy Without Borders

2011 GENERATING ASSETS 27 THERMAL POWER PLANTS, 2 HYDROPOWER PLANTS AND 1 WIND FARM IN THE MANAGEMENT INSTALLED CAPACITY 28.2 GW (+45.8%) SHARE IN THE TOTAL INSTALLED CAPACITY OF RUSSIA 10.2% GENERATION OF ELECTRIC POWER 116.9BN KW*H (+37.3%) BOILER HEAT THERMAL POWER 19.8M GCAL (+0.5%) POWER SUPPLY ASSETS ENERGY POWER SUPPLY ASSETS ENERGY SALES VOLUME AT THE RETAIL MARKET 143.1BN KW*H (SHARE AT THE RF MARKET 14.02%) POWER GRID ASSETS TOTAL LENGTH OF POWER TRANSMISSION LINES ABROAD 34265 KM (+1.1%) ELECTRICITY EXPORT AND IMPORT EXPORT VOLUME 22.7BN KW*H (+21.9%) (INCLUDING AZERBAIJAN +148.1% BELARUS +10774.7% GEORGIA +111.2% KAZAKHSTAN +60.5% CHINA +26.0% LITHUANIA +8.6% MONGOLIA +23.2% SOUTH OSSETIA +11.7% IMPORT VOLUME +17.2% (INCLUDING AZERBAIJAN +93.2% KAZAKHSTAN +58.0%) FINANCIAL INDICATORS REVENUE 536.2BN RUB (+15.5%) EBITDA 41.7BN RUB (+24.1%) NET PROFIT 41.5BN RUB (+123.1%) CAPITAL EXPENDITURES 32.5BN RUB (+97.0%) TOTAL ASSETS 531.9BN RUB (+113.5%) TOTAL EQUITY 390.7BN RUB (+180.9%) NUMBER OF PERSONNEL AS OF DECEMBER 31, 2011 47014 PERSONS ENERGY WITHOUT BORDERS ANNUAL REPORT 2011 JSC “INTER RAO UES” Contents ENERGY WITHOUT BORDERS.........................................................................................................................................................1 ADDRESS BY THE CHAIRMAN OF THE BOARD OF DIRECTORS AND THE CHAIRMAN OF THE MANAGEMENT BOARD OF JSC “INTER RAO UES”..............................................................................................................8 1. General Information about the Company and its Place in the Industry...........................................................10 1.1. Brief History of the Company......................................................................................................................... 10 1.2. Business Model of the Group..........................................................................................................................12 1.4. -

Notes on Moscow Exchange Index Review

Notes on Moscow Exchange index review Moscow Exchange approves the updated list of index components and free float ratios effective from 16 March 2018. X5 Retail Group N.V. (DRs) will be added to Moscow Exchange indices with the expected weight of 1.13 per cent. As these securities were offered initially, they were added without being in the waiting list under consideration. Thus, from 16 March the indices will comprise 46 (component stocks. The MOEX Russia and RTS Index moved to a floating number of component stocks in December 2017. En+ Group plc (DRs) will be in the waiting list to be added to Moscow Exchange indices, as their liquidity rose notably over recent three months. NCSP Group (ords) with low liquidity, ROSSETI (ords) and RosAgro PLC with their weights now below the minimum permissible level (0.2 per cent) will be under consideration to be excluded from the MOEX Russia Index and RTS Index. The Blue Chip Index constituents remain unaltered. X5 Retail Group (DRs), GAZ (ords), Obuvrus LLC (ords) and TNS energo (ords) will be added to the Broad Market Index, while Common of DIXY Group and Uralkali will be removed due to delisting expected. TransContainer (ords), as its free float sank below the minimum threshold of 5 per cent, and Southern Urals Nickel Plant (ords), as its liquidity ratio declined, will be also excluded. LSR Group (ords) will be incuded into SMID Index, while SOLLERS and DIXY Group (ords) will be excluded due to low liquidity ratio. X5 Retail Group (DRs) and Obuvrus LLC (ords) will be added to the Consumer & Retail Index, while DIXY Group (ords) will be removed from the Index. -

An Overview of Boards of Directors at Russia's Largest Public Companies

An Overview Of Boards Of Directors At Russia’s Largest Public Companies Andrei Rakitin Milena Barsukova Arina Mazunova Translated from Russian August 2020 Key Results According to information disclosed by 109 of Russia’s largest public companies: “Classic” board compositions of 11, nine, and seven seats prevail The total number of persons on Boards of the companies under study is not as low as it might seem: 89% of all Directors were elected to only one such Board Female Directors account for 12% and are more often elected to the audit, nomination, and remuneration committees than to the strategy committee Among Directors, there are more “humanitarians” than “techies,” while the share of “techies” among chairs is greater than across the whole sample The average age for Directors is 53, 56 for Chairmen, and 58 for Independent Directors Generation X is the most visible on Boards, and Generation Y Directors will likely quickly increase their presence if the impetuous development of digital technologies continues The share of Independent Directors barely reaches 30%, and there is an obvious lack of independence on key committees such as audit Senior Independent Directors were elected at 17% of the companies, while 89% of Chairs are not independent The average total remuneration paid to the Board of Directors is RUR 69 million, with the difference between the maximum and minimum being 18 times Twenty-four percent of the companies disclosed information on individual payments made to their Directors. According to this, the average total remuneration is approximately RUR 9 million per annum for a Director, RUR 17 million for a Chair, and RUR 11 million for an Independent Director The comparison of 2020 findings with results of a similar study published in 2012 paints an interesting dynamic picture. -

Press Release (PDF)

MECHEL REPORTS THE FY2020 FINANCIAL RESULTS Consolidated revenue – 265.5 bln rubles (-8% compared to FY 2019) EBITDA* – 41.1 bln rubles (-23% compared to FY 2019) Profit attributable to equity shareholders of Mechel PAO – 808 mln rubles Moscow, Russia – March 11, 2021 – Mechel PAO (MOEX: MTLR, NYSE: MTL), a leading Russian mining and steel group, announces financial results for the FY 2020. Mechel PAO’s Chief Executive Officer Oleg Korzhov commented: “The Group’s consolidated revenue in 2020 totaled 265.5 billion rubles, which is 8% less compared to 2019. EBITDA amounted to 41.1 billion rubles, which is 23% less year-on-year. “The mining division accounted for about 60% of the decrease in revenue. This was due to a significant decrease in coal prices year-on-year. In conditions of coronavirus limitations, many steelmakers around the world cut down on production, which could not fail to affect the demand for metallurgical coals and their price accordingly. By the year’s end the market demonstrated signs of a recovery, but due to China’s restrictions on Australian coal imports, coal prices outside on China remained low under this pressure. High prices in China have supported our mining division’s revenue to a certain extent. In 4Q2020 we increased shipments to China as best we could considering our long-term contractual obligations to partners from other countries. These circumstances became in many ways the reason for a decrease in our consolidated EBITDA. In Mechel’s other divisions EBITDA dynamics were positive year-on-year. “The decrease in the steel division’s revenue was also due to the coronavirus pandemic. -

William R. Spiegelberger the Foreign Policy Research Institute Thanks the Carnegie Corporation for Its Support of the Russia Political Economy Project

Russia Political Economy Project William R. Spiegelberger The Foreign Policy Research Institute thanks the Carnegie Corporation for its support of the Russia Political Economy Project. All rights reserved. Printed in the United States of America. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording, or any information storage and retrieval system, without permission in writing from the publisher. Author: William R. Spiegelberger Eurasia Program Leadership Director: Chris Miller Deputy Director: Maia Otarashvili Edited by: Thomas J. Shattuck Designed by: Natalia Kopytnik © 2019 by the Foreign Policy Research Institute April 2019 COVER: Designed by Natalia Kopytnik. Photography: Oleg Deripaska (World Economic Forum); St. Basil’s Cathedral (Adob Stock); Ruble (Adobe Stock); Vladimir Putin (kremlin.ru); Rusal logo (rusal.ru); United States Capitol (Adobe Stock; Viktor Vekselberg (Aleshru/Wikimedia Commons); Alumnium rolls (Adobe Stock); Trade War (Adobe Stock). Our Mission The Foreign Policy Research Institute is dedicated to bringing the insights of scholarship to bear on the foreign policy and national security challenges facing the United States. It seeks to educate the public, teach teachers, train students, and offer ideas to advance U.S. national interests based on a nonpartisan, geopolitical perspective that illuminates contemporary international affairs through the lens of history, geography, and culture. Offering Ideas In an increasingly polarized world, we pride ourselves on our tradition of nonpartisan scholarship. We count among our ranks over 100 affiliated scholars located throughout the nation and the world who appear regularly in national and international media, testify on Capitol Hill, and are consulted by U.S. -

Deal Drivers Russia

February 2010 Deal Drivers Russia A survey and review of Russian corporate finance activity Contents Introduction 1 01 M&A Review 2 Overall deal trends 3 Domestic M&A trends 6 Cross-border M&A trends 8 Private equity 11 Acquisition finance 13 Valuations 14 02 Industries 15 Automotive 16 Energy 18 Financial Services 20 Consumer & Retail 22 Industrial Markets 24 Life Sciences 26 Mining 28 Technology, Media & Telecommunications 30 03 Survey Analysis 32 Introduction Prediction may be fast going out of fashion. At the end of 2008, CMS commissioned mergermarket to interview 100 Russian M&A and corporate decision makers to find out what they thought about the situation at the time and what their views on the future were. Falling commodity prices were viewed as the biggest threat, the Financial Services sector was expected to deliver the greatest growth for M&A activity and the bulk of inward investment was expected from Asia. The research revealed that two thirds of the respondents expected the overall level of M&A activity to increase over the course of 2009, with only one third predicting a fall. That third of respondents was right and, in general, the majority got it wrong or very wrong. The survey did get some things right – the predominance of Who knows? What’s the point? We consider the point to be the domestic players, the increase of non-money deals, the in the detail. Our survey looks at the market in 2009 sector number of transactions against a restructuring background, by sector – what was ‘in’ and what was ‘out’. -

Yakutia) “…The Republic of Sakha (Yakutia) Is the Largest Region in the Russian Federation and One of the Richest in Natural Resources

Investor's Guide to the Republic of Sakha (Yakutia) “…The Republic of Sakha (Yakutia) is the largest region in the Russian Federation and one of the richest in natural resources. Needless to say, the stable and dynamic development of Yakutia is of key importance to both the Far Eastern Federal District and all of Russia…” President of the Russian Federation Vladimir Putin “One of the fundamental priorities of the Government of the Republic of Sakha (Yakutia) is to develop comfortable conditions for business and investment activities to ensure dynamic economic growth” Head of the Republic of Sakha (Yakutia) Egor Borisov 2 Contents Welcome from Egor Borisov, Head of the Republic of Sakha (Yakutia) 5 Overview of the Republic of Sakha (Yakutia) 6 Interesting facts about the Republic of Sakha (Yakutia) 7 Strategic priorities of the Republic of Sakha (Yakutia) investment policy 8 Seven reasons to start a business in the Republic of Sakha (Yakutia) 10 1. Rich reserves of natural resources 10 2. Significant business development potential for the extraction and processing of mineral and fossil resources 12 3. Unique geographical location 15 4. Stable credit rating 16 5. Convenient conditions for investment activity 18 6. Developed infrastructure for the support of small and medium-sized enterprises 19 7. High level of social and economic development 20 Investment infrastructure 22 Interaction with large businesses 24 Interaction with small and medium-sized enterprises 25 Other organisations and institutions 26 Practical information on doing business in the Republic of Sakha (Yakutia) 27 Public-Private Partnership 29 Information for small and medium-sized enterprises 31 Appendix 1. -

Holborn Gate Master Fax Template

**CONFERENCE CALL** MECHEL OAO (NYSE:MTL) Scheduled for: Thursday, December 18, 2008 10:00 AM New York Time 3:00 PM London Time 6:00 PM Moscow Time __________________________________________________________________ You are cordially invited to participate on a conference call with the management of Mechel OAO to discuss our 2008 first half and nine months results. Igor Zyuzin, Chief Executive Officer, will host the call. Please call the number below approximately 10 minutes prior to the scheduled time of the call, quoting Mechel, and the chairperson’s name, Alexander Tolkach. Conference Call Phone Numbers: US: +1 718 354 1158 International: +44 20 7138 0810 Confirmation Code: 8468348 The earnings release will be distributed prior to the conference call. In addition, the conference call will be available live via the Internet. To access the call and associated slides, please visit our website at: http://www.mechel.com/investors/fresults/index.wbp on the day of the call. A replay of the call will be available until 11:59PM New York time on December 24th. To access, please dial, US: +1 718 354 1112; UK: +44 20 7806 1970. From both areas, enter: 8468348# to access. MECHEL 2008 FIRST HALF AND NINE MONTHS RESULTS CONFERENCE CALL TO BE BROADCAST OVER THE INTERNET Moscow, Russia — December 15, 2008 — Mechel OAO (NYSE: MTL) announces that it intends to release its results for the first half ending June 30, 2008, and the nine months ending on September 30, 2008 on Thursday, December 18, 2008. In conjunction with this release, Mechel will host a conference call, which will be simultaneously broadcast live over the Internet. -

Evolution in the Russian Gas Market – the Competition for Customers

Evolution in the Russian Gas Market – The Competition for Customers James Henderson NG 73 January 2013 The contents of this paper are the author’s sole responsibility. They do not necessarily represent the views of the Oxford Institute for Energy Studies, of any of the Institute’s members, and/or of the author’s other affiliations. Copyright © 2013 Oxford Institute for Energy Studies (Registered Charity, No. 286084) This publication may be reproduced in part for educational or non-profit purposes without special permission from the copyright holder, provided acknowledgment of the source is made. No use of this publication may be made for resale or for any other commercial purpose whatsoever without prior permission in writing from the Oxford Institute for Energy Studies. ISBN 978-1-907555-66-4 ii Abbreviations and Units of Measurement bbls Barrels bcm Billion cubic metres bcma Billion cubic metres per annum bn bbls Billion barrels boepd Barrels of oil equivalent per day bpd Barrels per day E&P Exploration and Production ESPO East Siberia – Pacific Ocean (Pipeline) FSU Former Soviet Union IOC International Oil Company kboepd Thousands of barrels of oil equivalent per day kbpd Thousands of barrels per day km Kilometres mm bbls Million barrels mcm Thousands of cubic metres mmboepd Millions of barrels of oil equivalent per day] mmbpd Millions of barrels per day mmbtu Million British thermal units mmcm Millions of cubic metres mmt Millions of tonnes mmtpa Millions of tonnes per annum Mm tonnes Millions of tonnes P&P Proved and Probable tcm -

US Sanctions on Russia

U.S. Sanctions on Russia Updated January 17, 2020 Congressional Research Service https://crsreports.congress.gov R45415 SUMMARY R45415 U.S. Sanctions on Russia January 17, 2020 Sanctions are a central element of U.S. policy to counter and deter malign Russian behavior. The United States has imposed sanctions on Russia mainly in response to Russia’s 2014 invasion of Cory Welt, Coordinator Ukraine, to reverse and deter further Russian aggression in Ukraine, and to deter Russian Specialist in European aggression against other countries. The United States also has imposed sanctions on Russia in Affairs response to (and to deter) election interference and other malicious cyber-enabled activities, human rights abuses, the use of a chemical weapon, weapons proliferation, illicit trade with North Korea, and support to Syria and Venezuela. Most Members of Congress support a robust Kristin Archick Specialist in European use of sanctions amid concerns about Russia’s international behavior and geostrategic intentions. Affairs Sanctions related to Russia’s invasion of Ukraine are based mainly on four executive orders (EOs) that President Obama issued in 2014. That year, Congress also passed and President Rebecca M. Nelson Obama signed into law two acts establishing sanctions in response to Russia’s invasion of Specialist in International Ukraine: the Support for the Sovereignty, Integrity, Democracy, and Economic Stability of Trade and Finance Ukraine Act of 2014 (SSIDES; P.L. 113-95/H.R. 4152) and the Ukraine Freedom Support Act of 2014 (UFSA; P.L. 113-272/H.R. 5859). Dianne E. Rennack Specialist in Foreign Policy In 2017, Congress passed and President Trump signed into law the Countering Russian Influence Legislation in Europe and Eurasia Act of 2017 (CRIEEA; P.L. -

(31) December 2014

The Year An Interview with Chairman Electrification in Pictures: of Completed Ins of the State Duma’s Committee some facts from the history and Expected Outs for Energy Ivan GRACHEV of energy posters 14 20 32 Magazine about Russia’s Power Industry ENERGY WITHOUT BORDERS № 6 (31) December 2014 – January 2015 Happy Payments! The industry is anticipating tougher measures against non- payers in the retail electricity market IN RUSSIAN AND ENGLISH peretok.ru ENERGETICS IN RUSSIA AND IN THE WORLD peretok.ru NETWORKED! Dear readers, he end of the year is the time to sum up results. One of the un- solved problems of the year of 2014 is the outstanding debt for power supply. As of November 1, the amount owed to guaranteed supply companies in Russia reached 165 billion rubles. At the same time, the guaranteed supply companies have to pay on the wholesale market just in time and are forced to arrange loans to fulfill their obligations. Consumers’ poor payment discipline caus- es payment problems along the entire chain, undermining power companies’ financial stability, while the situation with non-pay- ments adversely affects the industry as a whole. Today, power supply companies do everything possible to get their money from consumers, including sending notices, cutting off electricity supply, filing lawsuits, and, jointly with court bai- liffs, prohibiting debtors from travelling abroad. It is clear that power supply companies will not be able to address this problem independently; this will require a systematic approach at the highest Tlevel. The State Duma is now developing a whole series of amendments to legislation aimed at tightening payment discipline on the retail market. -

Investment from Russia Stabilizes After the Global Crisis 1

Institute of World Economy and International Relations (IMEMO) of Russian Academy of Sciences Investment from Russia stabilizes after the global crisis 1 Report dated June 23, 2011 EMBARGO: The contents of this report must not be quoted or summarized in the print, broadcast or electronic media before June 23, 2011, 3:00 p.m. Moscow; 11 a.m. GMT; and 7 a.m. New York. Moscow and New York, June 23, 2011 : The Institute of World Economy and International Relations (IMEMO) of the Russian Academy of Sciences, Moscow, and the Vale Columbia Center on Sustainable International Investment (VCC), a joint undertaking of the Columbia Law School and the Earth Institute at Columbia University in New York, are releasing the results of their second joint survey of Russian outward investors today 2. The survey is part of a long-term study of the rapid global expansion of multinational enterprises (MNEs) from emerging markets. The present survey, conducted at the beginning of 2011, covers the period 2007-2009. Highlights Despite the global crisis of the last few years, Russia has remained one of the leading outward investors in the world. The foreign assets of Russian MNEs have grown rapidly and only China and Mexico are further ahead among emerging markets. As the results of our survey show, several non- financial 3 Russian MNEs are significant actors in the world economy. The foreign assets of the 20 leading non-financial MNEs were about USD 107 billion at the end of 2009 (table 1). Their foreign sales 4 were USD 198 billion and they had more than 200,000 employees abroad.