The International Monetary and Financial

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Russia Takes Double Punch As Vanishing Workers Fan Prices Bloomberg.Com – Global Edition by Olga Tanas 2014-09-17, T14:12:11Z

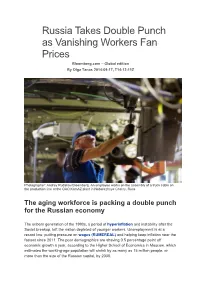

Russia Takes Double Punch as Vanishing Workers Fan Prices Bloomberg.com – Global edition By Olga Tanas 2014-09-17, T14:12:11Z Photographer: Andrey Rudakov/Bloomberg. An employee works on the assembly of a truck cabin on the production line at the OAO KamAZ plant in Naberezhnye Chelny, Russ The aging workforce is packing a double punch for the Russian economy The unborn generation of the 1990s, a period of hyperinflation and instability after the Soviet breakup, left the nation depleted of younger workers. Unemployment is at a record low, putting pressure on wages (RUMEREAL) and helping keep inflation near the fastest since 2011. The poor demographics are shaving 0.5 percentage point off economic growth a year, according to the Higher School of Economics in Moscow, which estimates the working-age population will shrink by as many as 15 million people, or more than the size of the Russian capital, by 2030. Aging populations are unsettling central bankers from Tokyo to Frankfurt in their struggle to prevent deflation as older workers tend to defer consumption in favor of savings. Russia faces the opposite threat: entrenched inflation that risks shackling monetary policy already lurching from one crisis to another since Crimea was annexed in March. “Taking into account low unemployment and tight supply on the labor market, wages will remain at a high level, affecting inflation,” said Natalia Orlova, chief economist at Alfa Bank in Moscow. With the central bank increasingly drawing attention to poor demographics, it’s “in effect saying it can do nothing for the economy, whose problems are structural in character.” Demographic Factor Russia is caught in a vise of elevated inflation and stalling economic growth. -

University of Surrey Discussion Papers in Economics By

råáp=== = = ======råáîÉêëáíó=çÑ=pìêêÉó Discussion Papers in Economics THE DISSENT VOTING BEHAVIOUR OF BANK OF ENGLAND MPC MEMBERS By Christopher Spencer (University of Surrey) DP 03/06 Department of Economics University of Surrey Guildford Surrey GU2 7XH, UK Telephone +44 (0)1483 689380 Facsimile +44 (0)1483 689548 Web www.econ.surrey.ac.uk ISSN: 1749-5075 The Dissent Voting Behaviour of Bank of England MPC Members∗ Christopher Spencer† Department of Economics, University of Surrey Abstract I examine the propensity of Bank of England Monetary Policy Committee (BoEMPC) members to cast dissenting votes. In particular, I compare the type and frequency of dissenting votes cast by so- called insiders (members of the committee chosen from within the ranks of bank staff)andoutsiders (committee members chosen from outside the ranks of bank staff). Significant differences in the dissent voting behaviour associated with these groups is evidenced. Outsiders are significantly more likely to dissent than insiders; however, whereas outsiders tend to dissent on the side of monetary ease, insiders do so on the side of monetary tightness. I also seek to rationalise why such differences might arise, and in particular, why BoEMPC members might be incentivised to dissent. Amongst other factors, the impact of career backgrounds on dissent voting is examined. Estimates from logit analysis suggest that the effect of career backgrounds is negligible. Keywords: Monetary Policy Committee, insiders, outsiders, dissent voting, career backgrounds, ap- pointment procedures. Contents 1 Introduction 2 2 Relationship to the Literature 2 3 Rationalising Dissent Amongst Insiders and Outsiders - Some Priors 3 3.1CareerIncentives........................................... 4 3.2CareerBackgrounds........................................ -

Russia's 2020 Strategic Economic Goals and the Role of International

Russia’s 2020 Strategic Economic Goals and the Role of International Integration 1800 K Street NW | Washington, DC 20006 Tel: (202) 887-0200 | Fax: (202) 775-3199 E-mail: [email protected] | Web: www.csis.org authors Andrew C. Kuchins Amy Beavin Anna Bryndza project codirectors Andrew C. Kuchins Thomas Gomart july 2008 europe, russia, and the united states ISBN 978-0-89206-547-9 finding a new balance Ë|xHSKITCy065479zv*:+:!:+:! CENTER FOR STRATEGIC & CSIS INTERNATIONAL STUDIES Russia’s 2020 Strategic Economic Goals and the Role of International Integration authors Andrew C. Kuchins Amy Beavin Anna Bryndza project codirectors Andrew C. Kuchins Thomas Gomart july 2008 About CSIS In an era of ever-changing global opportunities and challenges, the Center for Strategic and International Studies (CSIS) provides strategic insights and practical policy solutions to decisionmakers. CSIS conducts research and analysis and develops policy initiatives that look into the future and anticipate change. Founded by David M. Abshire and Admiral Arleigh Burke at the height of the Cold War, CSIS was dedicated to the simple but urgent goal of finding ways for America to survive as a nation and prosper as a people. Since 1962, CSIS has grown to become one of the world’s preeminent public policy institutions. Today, CSIS is a bipartisan, nonprofit organization headquartered in Washington, DC. More than 220 full- time staff and a large network of affiliated scholars focus their expertise on defense and security; on the world’s regions and the unique challenges inherent to them; and on the issues that know no boundary in an increasingly connected world. -

About the Contributors

STRATEGIES for MONETARY POLICY EDITED BY JOHN H. COCHRANE JOHN B. TAYLOR About the Contributors JAMES “JIM” BULLARD is the president and CEO of the Federal Reserve Bank of St. Louis. In that role, he is a participant on the Fed- eral Reserve’s Federal Open Market Committee, which meets regularly to set the direction of US monetary policy. He also oversees the Federal Reserve’s Eighth District, including activities at the St. Louis headquar- ters and its branches in Little Rock, Arkansas; Louisville, Kentucky; and Memphis, Tennessee. Bullard is a noted economist and scholar, and his positions are founded on research-based thinking and an intellectual open- ness to new theories and explanations. He is often an early voice for change. Bullard makes public outreach and dialogue a priority to help build a more transparent and accessible Fed. A native of Forest Lake, Minnesota, Bullard received his PhD in economics from Indiana University in Bloomington. He holds BS degrees in economics and in quantitative methods and infor- mation systems from St. Cloud State University in St. Cloud, Minnesota. RICHARD H. CLARIDA serves on the Board of Governors of the Federal Reserve System and has been vice chair since 2018, filling a term ending in 2022. Clarida previously served as the C. Lowell Harriss Professor of Economics and International Affairs and chaired the Department of Economics at Columbia University. In addition to his academic experience, Clarida was the assistant secretary for economic policy of the US Treasury, where he was awarded the Treasury Medal in recognition of his service; and served on the Council of Economic Advisers under President Reagan. -

Occasional Paper by Alastair Clark and Andrew

Macroprudential Policy: Addressing the Things We Don’t Know Alastair Clark Andrew Large Occasional Paper 83 30 Group of Thirty, Washington, DC About the Authors Alastair Clark, CBE, formerly Executive Director and Adviser to the Governor of the Bank of England, has since 2009 been Senior Adviser to HM Treasury on Financial Stability and is a member of the UK’s new interim Financial Policy Committee. He has also acted as an independent adviser to overseas public authorities in relation to financial stability and crisis prevention issues. He has been at various times a member of many international groups linked to the G20, the Financial Stability Board, and the Bank for International Settlements. In 2005 he co-chaired, with Walter Kielholz, a G30 Study Group looking at the systemic impact of reinsurance. He holds degrees from Cambridge University and the London School of Economics. Sir Andrew Large retired in 2006 as Deputy Governor of the Bank of England where he had served since 2002. He now acts independently for central banks and governments in relation to financial stability and crisis prevention issues. Andrew Large’s career has covered a wide range of senior positions in the world of global finance, within both the private and public sectors. He is in addition Chairman of the Senior Advisory Board of Oliver Wyman, Senior Adviser to the Hedge Fund Standards Board, Chairman of the Advisory Committee of Marshall Wace, and Chairman of the Board Risk Committee of Axis, Bermuda. ISBN 1-56708-154-1 Copies of this paper are available for $10 from: The Group of Thirty 1726 M Street, N.W., Suite 200 Washington, D.C. -

The Making of Hawks and Doves: Inflation Experiences on the FOMC

The Making of Hawks and Doves? Ulrike Malmendier1,∗ UC Berkeley, NBER, CEPR, and CESIfo Stefan Nagel2 University of Chicago, NBER, CEPR, and CESIfo Zhen Yan3 Cornerstone Research Abstract Personal experiences of inflation strongly influence the hawkish or dovish leanings of central bankers. For all members of the Federal Open Market Committee (FOMC) since 1951, we estimate an adaptive learning rule based on their lifetime inflation data. The resulting experience-based forecasts have significant predictive power for members' FOMC voting decisions, the hawkishness of the tone of their speeches, as well as the heterogeneity in their semi-annual inflation projections. Averaging over all FOMC members present at a meeting, inflation experiences also help to explain the federal funds target rate, over and above conventional Taylor rule components. Keywords: Monetary policy, Experience effects, Availability bias, Inflation forecasts, Federal Funds rate JEL: E50, E03, D84 ?We thank Scott Baker, Michael McMahon, Ricardo Reis, David Robinson, Christina Romer, David Romer, Jeremy Stein, and workshop participants at the Bank of Finland (Finlands Bank/Suomen Pankki), Bank of Sweden (Sveriges Riksbank), Harvard University, London School of Economics, Max Planck Institute for Research on Collective Goods, Northwestern University, Stanford University, Stockholm School of Economics, Temple University, UC Berkeley, University of Bonn, University of Chicago, University of Michigan Economics Department and Law School, Vanderbilt University, as well as the NBER SI Monetary Economics meeting and the American Economic Assocation meeting, Research in Behavioral Finance Conference 2016, and Annual Research Conference of the European Central Bank for helpful comments. Canyao Liu, Jonas Sobott, Marius G¨unzel,Jeffrey Zeidel, and Albert Lee provided excellent research assistance. -

O Ccasional P Aper 95

Is This the Beginning of the End of Central Bank Independence? Kenneth Rogoff Occasional Paper 95 GROUP OF THIRTY WASHINGTON, D.C. About the Author Kenneth Rogoff is Thomas D. Cabot Professor of Public Policy at Harvard University. From 2001 to 2003, Rogoff served as Chief Economist at the International Monetary Fund. His 2009 book with Carmen Reinhart, This Time is Different: Eight Centuries of Financial Folly, has been widely cited by academics, policymakers, and journalists. One regularity that Reinhart and Rogoff illustrate in their book is the remarkable quantitative similarities across time and countries in the run-up and the aftermath of severe financial crises. Rogoff’s most recent book is The Curse of Cash, which looks at the past, present, and future of currency, from the first standardized coinage to negative interest rate policy to the impact of cryptocurrencies on the global financial system. Rogoff is also known for his seminal work on exchange rates and on central bank independence. His treatise Foundations of International Macroeconomics (jointly with Maurice Obstfeld) is the standard graduate text in the field worldwide. His monthly syndicated column on global economic issues is published in over 50 countries. He is a member of the Council on Foreign Relations. Rogoff is an elected member of the National Academy of Sciences, the American Academy of Arts and Sciences, and the Group of Thirty. Rogoff is among the top eight on RePEc’s (Research Papers in Economics’) ranking of economists by scholarly citations. He is also an international grandmaster of chess. DISCLAIMER The views expressed in this paper are those of the author and do not represent the views of the Group of Thirty, its members, or their respective institutions. -

8-11 July 2021 Venice - Italy

3RD G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS MEETING AND SIDE EVENTS 8-11 July 2021 Venice - Italy 1 CONTENTS 1 ABOUT THE G20 Pag. 3 2 ITALIAN G20 PRESIDENCY Pag. 4 3 2021 G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS MEETINGS Pag. 4 4 3RD G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS MEETING Pag. 6 Agenda Participants 5 MEDIA Pag. 13 Accreditation Media opportunities Media centre - Map - Operating hours - Facilities and services - Media liaison officers - Information technology - Interview rooms - Host broadcaster and photographer - Venue access Host city: Venice Reach and move in Venice - Airport - Trains - Public transports - Taxi Accomodation Climate & time zone Accessibility, special requirements and emergency phone numbers 6 COVID-19 PROCEDURE Pag. 26 7 CONTACTS Pag. 26 2 1 ABOUT THE G20 Population Economy Trade 60% of the world population 80 of global GDP 75% of global exports The G20 is the international forum How the G20 works that brings together the world’s major The G20 does not have a permanent economies. Its members account for more secretariat: its agenda and activities are than 80% of world GDP, 75% of global trade established by the rotating Presidencies, in and 60% of the population of the planet. cooperation with the membership. The forum has met every year since 1999 A “Troika”, represented by the country that and includes, since 2008, a yearly Summit, holds the Presidency, its predecessor and with the participation of the respective its successor, works to ensure continuity Heads of State and Government. within the G20. The Troika countries are currently Saudi Arabia, Italy and Indonesia. -

Bank of England Annual Report 2003 Contents

Bank of England Annual Report 2003 Bank of England Annual Report 2003 Contents 3Governor’s Foreword 6 The Court of Directors 8Governance and Accountability 10 The Bank’s Core Purposes 12 Organisation Overview 14 The Executive and Senior Management 16 Review of Performance against Objectives and Strategy 30 Monetary Policy Committee Processes 34 Objectives and Strategy for 2003/04 35 Financial Framework for 2003/04 39 Personnel and Community Activities 43 Remuneration of Governors, Directors and MPC Members 47 Report from Members of Court 52 Risk Management 55 Report by the Non-Executive Directors 58 Report of the Independent Auditors The Bank’s Financial Statements 60 Banking Department Profit and Loss Account 61 Banking Department Balance Sheet 62 Banking Department Cash Flow Statement 63 Notes to the Banking Department Financial Statements 92 Issue Department Statements of Account 93 Notes to the Issue Department Statements of Account 95 Addresses and Telephone Numbers Eddie George, Governor 2 Bank of England Annual Report 2003 Governor’s Foreword This is the last occasion on which I will write the foreword to the Bank of England’s Annual Report, having had the immense privilege – and enormous pleasure – of serving the Bank as its Governor for the past ten years. At the time of my appointment in 1993, many of our preoccupations were very similar to those we have today – I see that in my first foreword I wrote about the importance of price stability as the primary objective for monetary policy. But what we did not fully appreciate as the Bank entered its fourth century was the extent and speed of the changes it was about to experience, which have proved to be among the most dramatic and interesting in its history. -

India Policy Forum July 13–16, 2020

Inflation Targeting in India: An Interim Assessment Barry Eichengreen University of California, Berkeley Poonam Gupta World Bank Rishabh Choudhary World Bank India Policy Forum July 13–16, 2020 NCAER | National Council of Applied Economic Research NCAER India Centre, 11 Indraprastha Estate, New Delhi 110002 Tel: +91-11-23452698, www.ncaer.org NCAER | Quality . Relevance . Impact Inflation Targeting in India: An Interim Assessment* Barry Eichengreen University of California, Berkeley Poonam Gupta World Bank Rishabh Choudhary World Bank India Policy Forum July 13–16, 2020 Abstract We provide an interim assessment of India’s inflation-targeting (IT) regime. We show that the RBI is best characterised as a flexible inflation targeter: contrary to criticism, it does not neglect changes in the output gap when setting policy rates. Rather than acting as an “inflation nutter,” it has if anything adjusted policy rates by less in response to inflation following the change in regime. We interpret this as an increase in policy credibility: smaller changes in the policy rate are needed to signal the central bank’s intent. This is consistent with the fact that the inflation expectations of forecasters have become better anchored with the shift to IT, and that other inflation-related outcomes are more stable than before. We also ask whether the shift to IT has enhanced the credibility of monetary policy such that the RBI is in a position to take extraordinary action in response to the COVID-19 crisis. We argue that the rules and understandings governing IT regimes come with escape clauses allowing central banks to disregard their inflation targets, under specific circumstances satisfied by the COVID-19 pandemic. -

Russia's International Activity in Response to the Global Financial

BULLETIN No. 37 (37) June 25, 2009 © PISM Editors: Sławomir Dębski (Editor-in-Chief), Łukasz Adamski, Bartosz Cichocki, Mateusz Gniazdowski, Beata Górka-Winter, Leszek Jesień, Agnieszka Kondek (Executive Editor), Łukasz Kulesa, Ernest Wyciszkiewicz Russia’s International Activity in Response to the Global Financial Crisis by Jarosław Ćwiek-Karpowicz Russia has striven to exploit the global financial crisis to bolster its international position. The build- ing of an international coalition of developing states, which Russia wants to head, is a means to that end. Among other things, the Russian authorities have championed new regional powers’ increased participation in international financial institutions, at the expense of the U.S. and other Western state. These efforts of the Russian Federation are laden with the risk of failure, primarily because of the Russia’s weak economic potential and vastly diverse interests of the prospective coalition members. This June Russia launched a major push on the international forum. Representatives of global business, science and politics had an opportunity to exchange views during the St. Petersburg International Economic Forum (4–6 June) dubbed “a Russian Davos.” Several days later Moscow hosted a summit of the Collective Security Treaty Organization (CSTO) and a meeting of the Inter- state Council of the Euro-Asian Economic Community (EAEC)—two foremost (from Russia’s pers- pective) initiatives to reintegrate the post-Soviet area. From there, the leaders of China, Russia, India, Brazil, Pakistan, Afghanistan and the Central Asian states met in Yekaterinburg (16–17 June) at Shanghai Cooperation Organization (SCO) and Brazil–Russia–India–China (BRIC) summits. A majority of these meetings were attended by Russian President Dmitry Medvedev whose addresses were focused on international financial crisis issues and on the need to overhaul the international financial system. -

Opening Speech

OPENING SPEECH Christian Noyer Governor Banque de France am delighted to open this 5th international We are facing a combination of two diffi culties. symposium of the Banque de France, which I is an opportunity to bring together heads of First, at present, for all countries, the risks for growth central banks and international institutions, leading are on the downside and for infl ation on the upside. academics and directors of private banks, as well Beyond the diversity of their mandates, this represents as representatives of industrialised and emerging a common challenge for all central banks. countries, in order to address a topical issue of common interest and concern to us all. Today’s debate Second, we are all affected, to differing degrees, by will be rich and intense. The fi rst session, chaired the turmoil of the past eight months in the credit by Jean-Claude Trichet, President of the European markets. In the coming hours we shall hold an in-depth Central Bank, will present the main concepts and debate on the relationship between fi nancial stability stylised facts of globalisation and world infl ation. and price stability. But I believe that we will all agree The second session, chaired by Jean-Pierre Roth, that the conduct of monetary policy is more diffi cult President of the Swiss National Bank, will focus on the and more uncertain in a less stable and more volatile links between globalisation and the determinants of fi nancial environment. domestic infl ation. The third session, which will take the form of a round table chaired by Nout Wellink, I would briefl y like to develop these two points.