Bulletin PST 119, Restaurants and Liquor Sellers

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

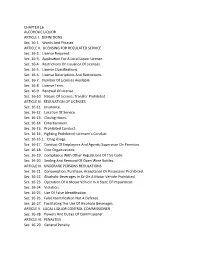

CHAPTER 16 ALCOHOLIC LIQUOR ARTICLE I. DEFINITIONS Sec. 16-1

CHAPTER 16 ALCOHOLIC LIQUOR ARTICLE I. DEFINITIONS Sec. 16-1. Words And Phrases. ARTICLE II. LICENSING FOR REGULATED SERVICE Sec. 16-2. License Required. Sec. 16-3. Application For A Local Liquor License. Sec. 16-4. Restrictions On Issuance Of Licenses. Sec. 16-5. License Classifications. Sec. 16-6. License Descriptions And Restrictions. Sec. 16-7. Number Of Licenses Available. Sec. 16-8. License Term. Sec. 16-9. Renewal Of License. Sec. 16-10. Nature Of License; Transfer Prohibited. ARTICLE III. REGULATION OF LICENSES Sec. 16-11. Insurance. Sec. 16-12. Location Of Service. Sec. 16-13. Closing Hours. Sec. 16-14. Entertainment. Sec. 16-15. Prohibited Conduct. Sec. 16-16. Fighting Prohibited; Licensee's Conduct. Sec. 16-16.1. Drug Usage. Sec. 16-17. Conduct Of Employees And Agents; Supervisor On Premises. Sec. 16-18. Civic Organizations. Sec. 16-19. Compliance With Other Regulations Of This Code. Sec. 16-20. Sealing And Removal Of Open Wine Bottles. ARTICLE IV. UNDERAGE PERSONS REGULATIONS Sec. 16-21. Consumption, Purchase, Acceptance Or Possession Prohibited. Sec. 16-22. Alcoholic Beverages In Or On A Motor Vehicle Prohibited. Sec. 16-23. Operation Of A Motor Vehicle In A State Of Impairment. Sec. 16-24. Violation. Sec. 16-25. Use Of False Identification. Sec. 16-26. False Identification Not A Defense. Sec. 16-27. Facilitating The Use Of Alcoholic Beverages. ARTICLE V. LOCAL LIQUOR CONTROL COMMISSIONER Sec. 16-28. Powers And Duties Of Commissioner. ARTICLE VI. PENALTIES Sec. 16-29. General Penalty. ARTICLE I DEFINITIONS Sec. 16-1. WORDS AND PHRASES. Unless the context otherwise requires, the following terms shall be construed according to the definitions set forth below: ACTING IN THE COURSE OF BUSINESS. -

City of Wichita Liquor License Information Sheet

CITY OF WICHITA LIQUOR LICENSE INFORMATION SHEET BASIS “Any person who operates a Drinking Establishment, Drinking Establishment/Restaurant, Drinking Establishment/Restaurant/Caterer, Drinking Establishment/Hotel, Drinking Establishment/Caterer, Class A Club, Class B Club, Caterer, or operates pursuant to a Temporary Permit must first obtain a liquor license for such business as issued by the City of Wichita.” "Alcoholic Liquor" means alcohol, spirits, wine, beer, and every liquid or solid, patented or not, containing alcohol, spirits, wine, or beer and capable of being consumed as a beverage by a human being, but shall not include any cereal malt beverage. LEGAL REFERENCE K.S.A. Chapter 41; Chapter 4.04 and 4.16, Code of the City of Wichita, Kansas. REGULATIONS Alcohol may be sold between 9AM and 2AM. A license from the State of Kansas is also required for the sale of alcoholic liquor by the drink and may be obtained at: Kansas Department of Revenue Alcoholic Beverage Control Docking State Office Building 915 SW Harrison Street, Room 214 Topeka, KS 66625-3512 (785) 296-7015; email [email protected] Renewals: Once the information required has been provided to Licensing, at renewal, the establishment is not required to provide a business plan including hours of operation, proposed forms of entertainment, list of on-site manager(s) providing there is no change in managers, a copy of any lease or purchase agreement, a floor plan, a site plan, a food menu, projected income, copies of vendor letters of intent, proof of a CPTED (Crime Prevention Through Environmental Design) inspection, and safe bar class information. -

Liquor Licensure; HB 2137

Sale of Liquor and Cereal Malt Beverage; Transfer of Liquor; Liquor Licensure; HB 2137 HB 2137 amends various provisions in the Kansas Liquor Control Act (KLCA), the Cereal Malt Beverage Act (CMBA) and the Club and Drinking Establishment Act (CDEA) concerning the sale, transfer, and licensure requirements related to alcoholic liquor and cereal malt beverage (CMB). Days and Times of Sale of Liquor and Cereal Malt Beverage The bill amends the KLCA and the CMBA to expand the time when retail sales of alcoholic liquor and CMB are allowed. The bill allows retail sales of alcoholic liquor and CMB in original packaging on Sundays between 9 a.m., rather than noon, and 8 p.m. and on Memorial Day, Independence Day, and Labor Day. Electronic Submission of Records by Special Order Shipping License Holders The bill changes the effective date of special order shipping licenses by specifying the license term begins on the date listed on the license, rather than on the date the license is issued. The bill also changes the payment of gallonage taxes by licensees and requires such taxes to be paid electronically on a quarterly basis to the Division of Alcoholic Beverage Control (ABC), Kansas Department of Revenue, rather than annually. Refillable and Sealable Containers The bill authorizes alcoholic liquor retailers, class A and B clubs, and drinking establishments to sell refillable and sealable containers of beer and CMB for consumption off the licensed premises. Formerly, alcoholic liquor retailers were restricted to selling alcoholic liquor only in the original unopened container, and class A and B clubs are not able to sell refillable and sealable containers of beer and CMB; only microbreweries are allowed to make such sales. -

Someplace Else Eating and Drinking Establishment

EATING AND DRINKING ESTABLISHMENT SPE MENU EDITION (05) sherat;on.com/krakow Warszawa Krakow Poznan Appet:easers SuPEr Salads Munchies& Sand"'iches The Foot;y liio .. ~ 22.00 Zorba bhe <lfeek .. ?7.00 Spring roAs, onion rings and liortilla chips wilih a spicy salsa Mixed letituce wilih fet;a cheese, onion, cucumbel; sweet; peppe1; oregano, Sajgonki warzywne, krqzki cebulowe i chipsy tortilla black olives, olive oi~ lemon juice Mieszanka satat z serem leta, cebulq, og6rkiem, stodkq paprykq, oregano, Mumbo Jumbo Beef Burger 32.00 z pikantnq salsq czarnymi oliwkami doprawiona oliwq z oliwek i sokiem z cytryny With french fries and coleslaw salad served lio order with or wilihouti cheese Wotowy burger z frytkami i satatkq colestaw podawany z serem lub bez Fuego·~~ 10.00 New York Salad 26.00 Spicy french fries Iceberg letituce liopped wibh chicken, bacon, t;omat;o, hard boiled egg, SPEcial Chicken Piba ,ttfJl'' 25.00 Pikantne frytki mustvooms Eo blue cheese crumbs Grilled siced chicken breast; in a lioastied pit;a bread served wilih fries Satata lodowa z dodatkiem kurczaka, bekonu, pomidor6w, jajka na twardo, and a lZatiziki sauce pieczarek i sera plesniowego ' Spicy Jack Beans 20.00 Pita z grilowanym kurczakiem podana z frytkami i sosem Tzatziki Chilkon-came with t;ort;illa chips Original Caesar Salad wibh C~un Chicken 30.00 Chilli con carne z chipsami tortilla The Beef Stieak Sandwich ''Peppioo" 42.00 Crispy iceberg salad liossed wilih a caesar dressing liopped with grilled Ccijun chicken Grilled beef medallions in a lioastied baguetite wilih bell peppers Kiss of Deabh .. 16.00 Chrupiqca satata lodowa z sosem .Caesar'' i grilowanym and mellied cheese Grilowa~e medaliony wotowe w chrupiqcej bagiet: !'l z paprykq i serem ~fried onion rings served wilih a garlic mayomaise kurczakiem w przyprawie Cajun Panierowane krqi:ki cebuli podawane z majonezem czosnkowym Chili Beef Salad ,,_-' 30.00 BLT. -

The Australian Bitters Dry July Survival Guide 2016

THE AUSTRALIAN BITTERS DRY JULY SURVIVAL GUIDE 2016 www.dryjulysurvivalguide.com.au #AustralianBittersxDryJuly The Australian Bitters Co. Guide To Dry July Welcome to the The Australian Bitters Co. guide to DRY JULY. Australian Bitters is an official partner of Dry July and is here to support you giving up alcohol for the month, all in a combined effort to support Australians affected by cancer. The following guide has all the tips, tricks, recipes and Dry July-friendly venues so you don’t have to give up your social life! Refer back to these pages whenever you need a little love and support! CONTENTS Page 5: Dry July Friendly Venues Page 6: Michael Chiem, PS40 - Top tips, and Australian Bitters mocktail recipes Page 7- 17: Dry July friendly venue mocktail recipes using Australian Bitters Page 17: About Australian Bitters products Dry July & Australian Bitters Australian Bitters is hand-crafted in Seven Hills, Sydney, from a secret recipe of 25 mainly Australian ingredients, including 20 different aromatics. Its premium flavour and local credentials have seen it gain considerable support from the nation’s leading bartenders. When you’re diagnosed with cancer, it’s hard to find the time or energy to think about anything other than treating the cancer. By giving up alcohol for the month of July and raising funds, Dry July participants help us to ease the burden, reduce stress and add a bit of comfort for those affected by cancer. To sign up to and raise money for Dry July please visit www.dryjuly.com www.dryjulysurvivalguide.com.au #AustralianBittersxDryJuly To the uneducated palate, all bitters could taste the same but to a connoisseur or mixologistTo the uneducated with a taste forpalate, the finer all bitters things, couldour range taste of theAustralian same Bitters but to a connoisseurmakes or mixologist all the difference. -

Eating and Drinking Establishment COVID-19 Requirements

ARCHIVED DOCUMENT As of June 30th, this document is no longer in force. It may be used as guidance. Eating and Drinking Establishment COVID-19 Requirements Summary of June 2, 2021 changes: 1. Clarified changes for fully vaccinated individuals. 2. Linked updated Department of Labor & Industries guidance. 3. Removed language that is duplicated in the Labor & industries guidance or outdated. Summary of the March 17, 2021 changes: 1. Added Phase 3 requirements and modifications: a. Indoor dining capacity allowed at 50%. b. Table size increased to 10 with no household restrictions. c. Alcohol service allowed until 12 a.m. 2. Other minor wording clarifications. Eating and drinking establishments must adopt a written procedure that is at least as strict as the requirements in this document and that complies with the appropriate safety and health requirements and guidelines established by the Washington State Department of Labor & Industries and the Washington State Department of Health. For purposes of this document an eating and drinking establishment includes, but is not limited to, restaurants, cafes, food courts, breweries, brewpubs, taverns, wine bars, wineries, distilleries, tasting rooms, private clubs and night clubs, or other establishments where food is offered/sold. Prior to recommencing on-site services, all business owners are required to develop at each establishment, a comprehensive COVID-19 exposure control, mitigation, and recovery plan which must be adhered to. A site-specific COVID-19 monitor shall be designated at each location to monitor the health of individuals and enforce the COVID-19 job site safety plan. A copy of the plan must be available at all locations and available for inspection by state and local authorities. -

Allowance for Outdoor Seating Areas for Eating And

Temporary Outdoor Seating Jefferson County, CO Adopted June 1, 2020 Allowance for Outdoor Seating Areas for Eating and Drinking Establishments Temporary Regulations The Jefferson County Board of County Commissioners, pursuant to the authority under C.R.S. 30-28-121 adopts these Temporary Allowance for Outdoor Seating Areas for Eating and Drinking Establishments Regulations. These temporary regulations are necessary to quickly address the changing regulatory environment as a result of the public health orders being issued surrounding the COVID-19 pandemic and will allow businesses to modify their operations within unincorporated Jefferson County to comply with the public health orders and Jefferson County rules and regulations. These temporary regulations will be valid until the Board of County Commissioners adopts a resolution indicating that for the purpose of these COVID-19 Regulations the public health emergency has ended. All improvements installed under this program must be removed no later than 30 days after the Board of County Commissioners adopts a resolution indicating that for the purpose of these COVID-19 Regulations the public health emergency has ended. These temporary zoning regulations shall apply to all eating and drinking establishments operating within unincorporated Jefferson County: Definitions Eating and Drinking Establishment: A retail establishment offering food, beverages, or alcoholic beverages for on-premises consumption. Temporary Outdoor Seating Area: An area not currently approved for outdoor seating of an eating and drinking establishment, used to temporarily expand seating capacity of the eating and drinking establishment to operate in an outdoor setting adjacent to their business. Hours of Operation Outdoor seating areas opened under these temporary regulations must close by: 10 p.m. -

CITY of NEWPORT BEACH ZONING ADMINISTRATOR STAFF REPORT March 14, 2013 Agenda Item No

COMMUNITY DEVELOPMENT DEPARTMENT PLANNING DIVISION 3300 Newport Boulevard, Building C, Newport Beach, CA 92663 (949) 644-3200 Fax: (949) 644-3229 www.newportbeachca.gov CITY OF NEWPORT BEACH ZONING ADMINISTRATOR STAFF REPORT March 14, 2013 Agenda Item No. 2 SUBJECT: Johnny’s Real New York Pizza - (PA2013-013) 1320 Bison Avenue . Minor Use Permit No. UP2013-002 APPLICANT: John Younesi, Johnny’s Real New York Pizza PLANNER: Gregg Ramirez, Senior Planner (949) 644-3219, [email protected] ZONING DISTRICT/GENERAL PLAN Zone: PC-50 (Bonita Canyon, Sub-Area 5, Commerical) General Plan: CG (General Commercial) PROJECT SUMMARY A minor use permit to allow a Type 41 (On-Sale Beer and Wine) Alcoholic Beverage Control License in conjunction with an allowed eating and drinking establishment previously approved by Use Permit No. UP2003-016. If approved, this Minor Use Permit would supersede Use Permit No. UP2003-016. Approval of this MUP is not required for the business to open and operate without alcoholic beverage service and tenant improvement building permits have been issued. RECOMMENDATION 1) Conduct a public hearing; and 2) Adopt Draft Zoning Administrator Resolution No. _ approving Minor Use Permit No. UP2013-002 (Attachment No. ZA 1). DISCUSSION The proposed restaurant is located in the Bluff’s shopping center at the corner of MacArthur Boulevard and Bison Avenue. 1 2 Johnny’s Real New York Pizza March 14, 2013 Page 2 The gross floor area of the establishment is approximately 1,495 square feet, the interior net public area will be approximately 500 square feet and includes seating for 36. -

Raising the Bar: Consumption, Gender, and the Birth of a New Public Drinking Culture Adam Blahut

University of New Mexico UNM Digital Repository History ETDs Electronic Theses and Dissertations 7-12-2014 Raising the Bar: Consumption, Gender, and the Birth of a New Public Drinking Culture Adam Blahut Follow this and additional works at: https://digitalrepository.unm.edu/hist_etds Recommended Citation Blahut, Adam. "Raising the Bar: Consumption, Gender, and the Birth of a New Public Drinking Culture." (2014). https://digitalrepository.unm.edu/hist_etds/9 This Dissertation is brought to you for free and open access by the Electronic Theses and Dissertations at UNM Digital Repository. It has been accepted for inclusion in History ETDs by an authorized administrator of UNM Digital Repository. For more information, please contact [email protected]. Adam Blahut Candidate History Department This dissertation is approved, and it is acceptable in quality and form for publication: Approved by the Dissertation Committee: Dr. Andrew K. Sandoval-Strausz, Chairperson Dr. Larry Ball Dr. Paul Andrew Hutton Dr. Sharon Wood i RAISING THE BAR: CONSUMPTION, GENDER, AND THE BIRTH OF A NEW PUBLIC DRINKING CULTURE by ADAM BLAHUT B.A., HISTORY, MERCYHURST UNIVERSITY, 2002 M.A., SOCIAL SCIENCE, EDINBORO UNIVERSITY OF PENNSYLVANIA, 2005 DISSERTATION Submitted in Partial Fulfillment of the Requirements for the Degree of DOCTOR OF PHILOSOPHY HISTORY The University of New Mexico Albuquerque, New Mexico May, 2014 ii ACKNOWLEDGEMENTS I would like to thank Durwood Ball, Paul Andrew Hutton, and Sharon Wood for their advice and help while working with me on this dissertation. I would especially like to thank Andrew K. Sandoval-Strausz, my adviser and dissertation committee chair, who guided me through this project and made me a better historian in the process. -

Responses to Alcohol-Related Problems in Four Western Countries: Characterising and Explaining Cultural Wetness and Dryness

UNIVERSITY OF LONDON RESPONSES TO ALCOHOL-RELATED PROBLEMS IN FOUR WESTERN COUNTRIES: CHARACTERISING AND EXPLAINING CULTURAL WETNESS AND DRYNESS A DISSERTATION SUBMITTED TO THE DEPARTMENT OF SOCIAL POLICY IN CANDIDACY FOR THE DEGREE OF DOCTOR OF PHILOSOPHY LONDON SCHOOL OF ECONOMICS AND POLITICAL SCIENCE BY CATHERINE ELAINE GILCHRIST TORONTO, CANADA DECEMBER 2003 UMI Number: U615617 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. Dissertation Publishing UMI U615617 Published by ProQuest LLC 2014. Copyright in the Dissertation held by the Author. Microform Edition © ProQuest LLC. All rights reserved. This work is protected against unauthorized copying under Title 17, United States Code. ProQuest LLC 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106-1346 rM £S£S a225 loiwtz Copyright 2003 by Catherine Gilchrist All rights reserved CATHERINE ELAINE GILCHRIST RESPONSES TO ALCOHOL RELATED PROBLEMS IN FOUR WESTERN COUNTRIES: CHARACTERISING AND EXPLAINING CULTURAL WETNESS AND DRYNESS DOCTOR OF PHILOSOPHY ABSTRACT There have been many variations on the theme of “wet” versus “dry” patterns of alcohol consumption. “Wet” and “dry” ideal types, primarily based on the extent to which alcohol customs are integrated and consistent with or antithetical to societal norms, can be located at opposite ends of a continuum and include distinctive patterns of consequences of drinking as well as different assumptions regarding societal responses to drinking. -

Kansas Administrative Regulations Article 21 Drinking Establishments

KANSAS ADMINISTRATIVE REGULATIONS ARTICLE 21 DRINKING ESTABLISHMENTS Division of Alcoholic Beverage Control Kansas Department of Revenue Docking State Office Building 915 SW Harrison Street Topeka, Kansas 66612-1558 Phone: 785-296-7015 / Fax: 785-296-7185 Website: www.ksrevenue.org/abc.html Email: [email protected] Rev. 7.01.2016 Kansas Administrative Regulations Article 21 Drinking Establishments Page 1 Table of Contents Subject Page 14-21-1. Definitions ......................................................................................................................... 3 14-21-2. Applications and renewals; documents required ............................................................... 4 14-21-3. Requirements for drinking establishment license ............................................................. 5 14-21-4. Issuance of license ............................................................................................................. 6 14-21-5. Licenses, loss or destruction of; application for and issuance of duplicate ...................... 7 14-21-6. Change of drinking establishment status ........................................................................... 7 14-21-7. Refund upon cancellation .................................................................................................. 8 14-21-8. Restaurant drinking establishments determination; gross receipts; affidavit; estimates ... 8 14-21-9. Employees; registration of same; prohibitions ................................................................. -

11 Communities with One Definition for Nightclub, Bar Or Lounge

11 Communities with One Definition for Nightclub, COMMUNITY Bar or Lounge Charlotte, NC Nightclub: Any commercial establishment serving alcoholic beverages and providing entertainment for patrons including bars, lounges, and cabarets. Austin, TX Cocktail lounge: use of a site for retail sale of alcoholic beverages for consumption on the premises, including taverns, bars, and similar uses, except for restaurants. Tavern: A business establishment that: (1) is devoted primarily Baltimore, MD to serving alcoholic beverages to the public for on premises consumption; and (2) might or might not also: (i) serve food; and (ii) sell alcoholic beverages for off-premises consumption. Boston. MA Bar: An establishment devoted primarily to the retailing and on- premises drinking of alcoholic beverages. Such establishment may or may not serve food, and may or may not include dancing or entertainment. Chicago, IL Tavern: An establishment that is primarily engaged in serving alcoholic liquor for consumption on the premises and in which the serving of prepared food, live entertainment and dancing are permitted. Cincinnati, OH Drinking Establishments: Bars, nightclubs, lounges or dance halls serving beverages for consumption on the premises as a primary use and including on-site service of alcohol, including beer, wine and mixed drinks. Columbia SC Drinking place: An establishment engaged in the retail sale of drinks, such as beer, ale or wine for consumption on the premises. Huntersville, NC Nightclub: Any commercial establishment serving alcoholic beverages and/or providing entertainment for patrons, including bars, lounges, taverns, cabarets, and similar establishments. Nashville/Davidson County After hours establishment: Any establishment open to the Metro , TN general public at any time between the hours of 3:00 a.m.