Form W-9, Request for Taxpayer Identification Number (TIN)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Research Brief March 2017 Publication #2017-16

Research Brief March 2017 Publication #2017-16 Flourishing From the Start: What Is It and How Can It Be Measured? Kristin Anderson Moore, PhD, Child Trends Christina D. Bethell, PhD, The Child and Adolescent Health Measurement Introduction Initiative, Johns Hopkins Bloomberg School of Every parent wants their child to flourish, and every community wants its Public Health children to thrive. It is not sufficient for children to avoid negative outcomes. Rather, from their earliest years, we should foster positive outcomes for David Murphey, PhD, children. Substantial evidence indicates that early investments to foster positive child development can reap large and lasting gains.1 But in order to Child Trends implement and sustain policies and programs that help children flourish, we need to accurately define, measure, and then monitor, “flourishing.”a Miranda Carver Martin, BA, Child Trends By comparing the available child development research literature with the data currently being collected by health researchers and other practitioners, Martha Beltz, BA, we have identified important gaps in our definition of flourishing.2 In formerly of Child Trends particular, the field lacks a set of brief, robust, and culturally sensitive measures of “thriving” constructs critical for young children.3 This is also true for measures of the promotive and protective factors that contribute to thriving. Even when measures do exist, there are serious concerns regarding their validity and utility. We instead recommend these high-priority measures of flourishing -

FIGUEROA 865 South Figueroa, Los Angeles, California

FIGUEROA 865 South Figueroa, Los Angeles, California E T PAU The Westin INGRAHAM ST S Bonaventure Hotel W W 7TH S 4T H ST T S FREMONT AV FINANCIAL Jonathan Club DISTRICT ST W 5TH ST IGUEROA S FLOWER ST Los Angeles ISCO ST L ST S F E OR FWY Central Library RB HA FRANC The California Club S BIX WILSHIR W 8TH ST W 6 E B TH ST LVD Pershing Square Fig at 7th 7th St/ Metro Center Pershing E T Square S AV O D COC ST N S TheThe BLOCBLO R FWY I RA C N ANCA S G HARBO R W 9TH ST F Figueroa HIS IVE ST Los Angeles, CA L O DOW S W 8T 8T H STS T W 6 TH S T S HILL ST W S OLY A MPIC B OOA ST R LVD FIGUE W 9 S ER ST TH ST W O W 7 L Y 7 A TTHH ST S F W S D T LEGENDAADWAY O FIDM/Fashion R Nokia Theatre L.A. LIVE BROB S Metro Station T W Institute of Design S OLYMPI G ST Light Rail StationIN & Merchandising R PPR C BLVD Green SpacesS S T Sites of Interest SST STAPLES Center IN SOUTH PARK ST MA E Parking S IV L S O LA Convention Center E W 1 L ST 1 ND AV Property Description Figueroa is a 35-storey, 692,389 sq ft granite and reflective glass office tower completed in 1991 that is located at the southwest corner of Figueroa Street and 8th Place in Downtown Los Angeles, California. -

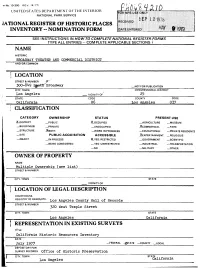

Jational Register of Historic Places Inventory -- Nomination Form

•m No. 10-300 REV. (9/77) UNITED STATES DEPARTMENT OF THE INTERIOR NATIONAL PARK SERVICE JATIONAL REGISTER OF HISTORIC PLACES INVENTORY -- NOMINATION FORM SEE INSTRUCTIONS IN HOW TO COMPLETE NATIONAL REGISTER FORMS ____________TYPE ALL ENTRIES -- COMPLETE APPLICABLE SECTIONS >_____ NAME HISTORIC BROADWAY THEATER AND COMMERCIAL DISTRICT________________________ AND/OR COMMON LOCATION STREET & NUMBER <f' 300-8^9 ^tttff Broadway —NOT FOR PUBLICATION CITY. TOWN CONGRESSIONAL DISTRICT Los Angeles VICINITY OF 25 STATE CODE COUNTY CODE California 06 Los Angeles 037 | CLASSIFICATION CATEGORY OWNERSHIP STATUS PRESENT USE X.DISTRICT —PUBLIC ^.OCCUPIED _ AGRICULTURE —MUSEUM _BUILDING(S) —PRIVATE —UNOCCUPIED .^COMMERCIAL —PARK —STRUCTURE .XBOTH —WORK IN PROGRESS —EDUCATIONAL —PRIVATE RESIDENCE —SITE PUBLIC ACQUISITION ACCESSIBLE ^ENTERTAINMENT _ REUGIOUS —OBJECT _IN PROCESS 2L.YES: RESTRICTED —GOVERNMENT —SCIENTIFIC —BEING CONSIDERED — YES: UNRESTRICTED —INDUSTRIAL —TRANSPORTATION —NO —MILITARY —OTHER: NAME Multiple Ownership (see list) STREET & NUMBER CITY. TOWN STATE VICINITY OF | LOCATION OF LEGAL DESCRIPTION COURTHOUSE. REGISTRY OF DEEDSETC. Los Angeie s County Hall of Records STREET & NUMBER 320 West Temple Street CITY. TOWN STATE Los Angeles California ! REPRESENTATION IN EXISTING SURVEYS TiTLE California Historic Resources Inventory DATE July 1977 —FEDERAL ^JSTATE —COUNTY —LOCAL DEPOSITORY FOR SURVEY RECORDS office of Historic Preservation CITY, TOWN STATE . ,. Los Angeles California DESCRIPTION CONDITION CHECK ONE CHECK ONE —EXCELLENT —DETERIORATED —UNALTERED ^ORIGINAL SITE X.GOOD 0 —RUINS X_ALTERED _MOVED DATE- —FAIR _UNEXPOSED DESCRIBE THE PRESENT AND ORIGINAL (IF KNOWN) PHYSICAL APPEARANCE The Broadway Theater and Commercial District is a six-block complex of predominately commercial and entertainment structures done in a variety of architectural styles. The district extends along both sides of Broadway from Third to Ninth Streets and exhibits a number of structures in varying condition and degree of alteration. -

August 2, 2018 Oliver Netburn City of Los Angeles Department of City

August 2, 2018 Oliver Netburn City of Los Angeles Department of City Planning 200 N. Spring Street Los Angeles, CA 90012 [email protected] RE: 2803 W. Broadway - CPC-2017-4388-GPA-ZC-CU-ZV-ZAD-SPR Dear Mr. Netburn: On behalf of The Eagle Rock Association (TERA), I am writing to you regarding the application for development entitlements at 2803 W. Broadway. The proposed project consists of a four-story, 65-foot-tall, approximately 85,000 square foot self-storage facility with fourteen parking spaces. Over the last three years, TERA has met with the applicant regarding this project. In January of this year, TERA met with the applicant and, after careful consideration, decided not to support the project. Our reasons for taking this position were that (1) the project was on an expedited track that made it difficult to for the community to provide constructive feedback and (2) that the scope of the development required sufficient community benefit. Since then, the applicant has taken the project off of the expedited track and has met with members of the community and with community groups, including TERA, which has helped to allay our initial concerns. Since these meetings, the applicant has committed to several items that we feel will benefit the community. These commitments include: A change in the architectural style of the building so that it is no longer contemporary but more in line with existing Eagle Rock architecture and design A 600 square foot community room with separate access from the facility, including a dedicated restroom. The room will be available to all local non-profit organizations on a first come, first served basis. -

Ligature Modeling for Recognition of Characters Written in 3D Space Dae Hwan Kim, Jin Hyung Kim

Ligature Modeling for Recognition of Characters Written in 3D Space Dae Hwan Kim, Jin Hyung Kim To cite this version: Dae Hwan Kim, Jin Hyung Kim. Ligature Modeling for Recognition of Characters Written in 3D Space. Tenth International Workshop on Frontiers in Handwriting Recognition, Université de Rennes 1, Oct 2006, La Baule (France). inria-00105116 HAL Id: inria-00105116 https://hal.inria.fr/inria-00105116 Submitted on 10 Oct 2006 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. Ligature Modeling for Recognition of Characters Written in 3D Space Dae Hwan Kim Jin Hyung Kim Artificial Intelligence and Artificial Intelligence and Pattern Recognition Lab. Pattern Recognition Lab. KAIST, Daejeon, KAIST, Daejeon, South Korea South Korea [email protected] [email protected] Abstract defined shape of character while it showed high recognition performance. Moreover when a user writes In this work, we propose a 3D space handwriting multiple stroke character such as ‘4’, the user has to recognition system by combining 2D space handwriting write a new shape which is predefined in a uni-stroke models and 3D space ligature models based on that the and which he/she has never seen. -

Journals | Penn State Libraries Open Publishing

I I • I • I• .1.1' D . , I * ' PA « ~** • * ' > . Mechanized streetcars rose out ofa need toreplace horse- the wide variety ofdifferent electric railway systems, no single drawn streetcars. The horse itselfpresented the greatest problems: system had yet emerged as the industry standard. Early lines horses could only work a few hours each day; they were expen- tended tobe underpowered and prone to frequent equipment sive to house, feed and clean up after; ifdisease broke out within a failure. The motors on electric cars tended to make them heavier stable, the result could be a financial catastrophe for a horsecar than either horsecars or cable cars, requiring a company to operator; and, they pulled the car at only 4 to 6 miles per hour. 2 replace its existing rails withheavier ones. Due to these circum- The expenses incurred inoperating a horsecar line were stances, electric streetcars could not yet meet the demands of staggering. For example, Boston's Metropolitan Railroad required densely populated areas, and were best operated along short 3,600 horses to operate its fleet of700 cars. The average working routes serving relatively small populations. life of a car horse was onlyfour years, and new horses cost $125 to The development of two rivaltechnological systems such as $200. Itwas common practice toprovide one stable hand for cable and electric streetcars can be explained by historian every 14 to 20horses inaddition to a staff ofblacksmiths and Thomas Parke Hughes's model ofsystem development. Inthis veterinarians, and the typical car horse consumed up to 30 pounds model, Hughes describes four distinct phases ofsystem growth: ofgrain per day. -

ISO Basic Latin Alphabet

ISO basic Latin alphabet The ISO basic Latin alphabet is a Latin-script alphabet and consists of two sets of 26 letters, codified in[1] various national and international standards and used widely in international communication. The two sets contain the following 26 letters each:[1][2] ISO basic Latin alphabet Uppercase Latin A B C D E F G H I J K L M N O P Q R S T U V W X Y Z alphabet Lowercase Latin a b c d e f g h i j k l m n o p q r s t u v w x y z alphabet Contents History Terminology Name for Unicode block that contains all letters Names for the two subsets Names for the letters Timeline for encoding standards Timeline for widely used computer codes supporting the alphabet Representation Usage Alphabets containing the same set of letters Column numbering See also References History By the 1960s it became apparent to thecomputer and telecommunications industries in the First World that a non-proprietary method of encoding characters was needed. The International Organization for Standardization (ISO) encapsulated the Latin script in their (ISO/IEC 646) 7-bit character-encoding standard. To achieve widespread acceptance, this encapsulation was based on popular usage. The standard was based on the already published American Standard Code for Information Interchange, better known as ASCII, which included in the character set the 26 × 2 letters of the English alphabet. Later standards issued by the ISO, for example ISO/IEC 8859 (8-bit character encoding) and ISO/IEC 10646 (Unicode Latin), have continued to define the 26 × 2 letters of the English alphabet as the basic Latin script with extensions to handle other letters in other languages.[1] Terminology Name for Unicode block that contains all letters The Unicode block that contains the alphabet is called "C0 Controls and Basic Latin". -

Atomic Order in Non-Equilibrium Silicon-Germanium-Tin Semiconductors

Atomic Order in Non-Equilibrium Silicon-Germanium-Tin Semiconductors S. Mukherjee1, N. Kodali1, D. Isheim2, S. Wirths3, J. M. Hartmann4, D. Buca3, D. N. Seidman2, and O. Moutanabbir1,* 1 Department of Engineering Physics, École Polytechnique de Montréal, Montréal, C. P. 6079, Succ. Centre-Ville, Montréal, Québec H3C 3A7, Canada. 2 Department of Materials Science and Engineering and Northwestern University Center for Atom-Probe Tomography, Northwestern University, Evanston, IL 60208-3108, USA. 3 Peter Grünberg Institute 9 and JARA - FIT, Forschungszentrum Juelich, Juelich 52425, Germany. 4 CEA, LETI, Minatec Campus, 17 rue des Martyrs, Grenoble 38054, France. The precise knowledge of the atomic order in monocrystalline alloys is fundamental to understand and predict their physical properties. With this perspective, we utilized laser-assisted atom probe tomography to investigate the three-dimensional distribution of atoms in non-equilibrium epitaxial Sn-rich group IV SiGeSn ternary semiconductors. Different atom probe statistical analysis tools including frequency distribution analysis, partial radial distribution functions, and nearest neighbor analysis were employed in order to evaluate and compare the behavior of the three elements to their spatial distributions in an ideal solid solution. This atomistic-level analysis provided clear evidence of an unexpected repulsive interaction between Sn and Si leading to the deviation of Si atoms from the theoretical random distribution. This departure from an ideal solid solution is supported by first principal calculations and attributed to the tendency of the system to reduce its mixing enthalpy throughout the layer-by-layer growth process. PACS: 68.35 bd, 38.35 bg, 34.20 Gj, 68.35 Dv 1 The assumption that the arrangement of atoms within the crystal lattice is perfectly random is a broadly used approximation to establish the physical properties of semiconductor alloys. -

Form W-4, Employee's Withholding Certificate

Employee’s Withholding Certificate OMB No. 1545-0074 Form W-4 ▶ (Rev. December 2020) Complete Form W-4 so that your employer can withhold the correct federal income tax from your pay. ▶ Department of the Treasury Give Form W-4 to your employer. 2021 Internal Revenue Service ▶ Your withholding is subject to review by the IRS. Step 1: (a) First name and middle initial Last name (b) Social security number Enter Address ▶ Does your name match the Personal name on your social security card? If not, to ensure you get Information City or town, state, and ZIP code credit for your earnings, contact SSA at 800-772-1213 or go to www.ssa.gov. (c) Single or Married filing separately Married filing jointly or Qualifying widow(er) Head of household (Check only if you’re unmarried and pay more than half the costs of keeping up a home for yourself and a qualifying individual.) Complete Steps 2–4 ONLY if they apply to you; otherwise, skip to Step 5. See page 2 for more information on each step, who can claim exemption from withholding, when to use the estimator at www.irs.gov/W4App, and privacy. Step 2: Complete this step if you (1) hold more than one job at a time, or (2) are married filing jointly and your spouse Multiple Jobs also works. The correct amount of withholding depends on income earned from all of these jobs. or Spouse Do only one of the following. Works (a) Use the estimator at www.irs.gov/W4App for most accurate withholding for this step (and Steps 3–4); or (b) Use the Multiple Jobs Worksheet on page 3 and enter the result in Step 4(c) below for roughly accurate withholding; or (c) If there are only two jobs total, you may check this box. -

Growth and Characterization of Silicon-Germanium-Tin Semiconductors for Future Nanophotonics Devices" (2018)

University of Arkansas, Fayetteville ScholarWorks@UARK Theses and Dissertations 12-2018 Growth and Characterization of Silicon- Germanium-Tin Semiconductors for Future Nanophotonics Devices Bader Saad Alharthi University of Arkansas, Fayetteville Follow this and additional works at: https://scholarworks.uark.edu/etd Part of the Electromagnetics and Photonics Commons, and the Semiconductor and Optical Materials Commons Recommended Citation Alharthi, Bader Saad, "Growth and Characterization of Silicon-Germanium-Tin Semiconductors for Future Nanophotonics Devices" (2018). Theses and Dissertations. 3012. https://scholarworks.uark.edu/etd/3012 This Dissertation is brought to you for free and open access by ScholarWorks@UARK. It has been accepted for inclusion in Theses and Dissertations by an authorized administrator of ScholarWorks@UARK. For more information, please contact [email protected], [email protected]. Growth and Characterization of Silicon-Germanium-Tin Semiconductors for Future Nanophotonics Devices A dissertation submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Engineering with a concentration in Electrical Engineering by Bader Saad Alharthi King Saud University Bachelor of Science in Physics, 2003 King Fahd University of Petroleum and Minerals Master of Science in Physics, 2009 University of Arkansas Master of Science in Electrical Engineering, 2018 December 2018 University of Arkansas This dissertation is approved for recommendation to the Graduate Council. Hameed A. Naseem, Ph.D. Shui-Qing (Fisher) Yu, Ph.D. Dissertation Director Dissertation Co-Director Simon Ang, Ph.D. Zhong Chen, Ph.D. Committee Member Committee Member Hugh Churchill, Ph.D. Committee Member Abstract The bright future of silicon (Si) photonics has attracted research interest worldwide. The ultimate goal of this growing field is to develop a group IV based Si foundries that integrate Si-photonics with the current complementary metal–oxide–semiconductor (CMOS) on a single chip for mid- infrared optoelectronics and high speed devices. -

The Alternative Minimum Tax

Updated December 4, 2017 Tax Reform: The Alternative Minimum Tax The U.S. federal income tax has both a personal and a Individual AMT corporate alternative minimum tax (AMT). Both the The modern individual AMT originated with the Revenue corporate and individual AMTs operate alongside the Act of 1978 (P.L. 95-600) and operated in tandem with an regular income tax. They require taxpayers to calculate existing add-on minimum tax prior to its repeal in 1982. their liability twice—once under the rules for the regular Table 2 details selected key individual AMT parameters. income tax and once under the AMT rules—and then pay the higher amount. Minimum taxes increase tax payments Table 2. Selected Individual AMT Parameters, 2017 from taxpayers who, under the rules of the regular tax system, pay too little tax relative to a standard measure of Single/ Married their income. Head of Filing Married Filing Household Jointly Separately Corporate AMT Exemption $54,300 $84,500 $42,250 The corporate AMT originated with the Tax Reform Act of 1986 (P.L. 99-514), which eliminated an “add-on” 28% bracket 187,800 187,800 93,900 minimum tax imposed on corporations previously. The threshold corporate AMT is a flat 20% tax imposed on a Source: Internal Revenue Code. corporation’s alternative minimum taxable income less an exemption amount. A corporation’s alternative minimum The individual AMT tax base is broader than the regular taxable income is the corporation’s taxable income income tax base and starts with regular taxable income and determined with certain adjustments (primarily related to adds back various deductions, including personal depreciation) and increased by the disallowance of a exemptions and the deduction for state and local taxes. -

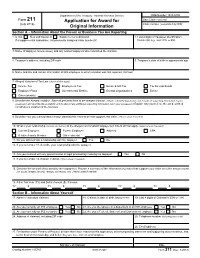

Form 211, Application for Award for Original Information

Department of the Treasury - Internal Revenue Service OMB Number 1545-0409 Form 211 Application for Award for Date Claim received (July 2018) Claim number (completed by IRS) Original Information Section A – Information About the Person or Business You Are Reporting 1. Is this New submission or Supplemental submission 2. Last 4 digits of Taxpayer Identification If a supplemental submission, list previously assigned claim number(s) Number(s) (e.g., SSN, ITIN, or EIN) 3. Name of taxpayer (include aliases) and any related taxpayers who committed the violation 4. Taxpayer's address, including ZIP code 5. Taxpayer's date of birth or approximate age 6. Name and title and contact information of IRS employee to whom violation was first reported, if known 7. Alleged Violation of Tax Law (check all that apply) Income Tax Employment Tax Estate & Gift Tax Tax Exempt Bonds Employee Plans Governmental Entities Exempt Organizations Excise Other (identify) 8. Describe the Alleged Violation. State all pertinent facts to the alleged violation. (Attach a detailed explanation and include all supporting information in your possession and describe the availability and location of any additional supporting information not in your possession.) Explain why you believe the act described constitutes a violation of the tax laws 9. Describe how you learned about and/or obtained the information that supports this claim. (Attach sheet if needed) 10. What is your relationship (current and former) to the alleged noncompliant taxpayer(s)? Check all that apply. (Attach sheet if needed) Current Employee Former Employee Attorney CPA Relative/Family Member Other (describe) 11. Do you still maintain a relationship with the taxpayer Yes No 12.