SHAPING a BETTER TOMORROW Conrad Hotel

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2015 SMPHI Annual Report

SUSTAINING GROWTH, DELIVERING VALUE 10th Floor, OneE-com Center Harbor Drive, Mall of Asia Complex Pasay City 1300, Philippines Email: [email protected] www.sminvestments.com 2 IFC Our Business Philosophy 2 Business Highlights & Impact 6 Financial Highlights 7 Shareholder Value SM INVESTMENTS CORPORATION SM INVESTMENTS OUR BUSINESS PHILOSOPHY 8 Ten-Year Performance Overview 10 Our Business Footprint 12 Message to Shareholders SM Investments Corporation is the Philippines’ largest 14 President’s Report publicly-listed holding company that holds a group of sustainable businesses in retail, property and financial services. The Group thrives on leadership, innovation 18 RETAIL OPERATIONS and highly synergistic operations. • THE SM STORE Our Vision is to build world-class businesses that are • SM Markets catalysts for development in the communities we serve. Our long history of sustained growth is an indication of our ability to deliver value for all our stakeholders through sound financial management, leadership, innovation, long-term sustainability efforts and a comprehensive development program for all our host communities. Through our interests and activities, Our Mission is to strive to be a good corporate citizen by partnering with our host communities in providing consistently high standards of service to our customers, look after the welfare of our employees, and deliver sustainable returns to our shareholders at all times, upholding the highest standards of corporate governance in all our businesses. 28 PROPERTY Over the years, we have been committed to sustaining • Malls our growth, in creating value and delivering quality • Residences products and services that our millions of customers aspire for. We are here to serve. -

Taiwan 19 Thailand & Turkey 20 United Arab Emirates & United Kingdom 21 United States of America & Vietnam 22 Branch List

“THE DISTANCES FROM ONE POINT TO ANOTHER ARE GETTING CLOSER EVERY DAY. People travel from one country to another with high expectations to have an unforgettable holiday. To experience the destination is a whole package including; Culture, Daily Life, Religion, Entainment and many more. As your travel partner we aim to make your business process easier, faster and more convenient. As your guests travel companion we assist them to get the maximum experience out of their holiday. 03 Map 04 Service 05 Sales Office 06 www.mySKYhub.com 07 Australia & Brazil 08 Cambodia & China 09 Egypt & France 10 Guam & Hawaii 11 Hong Kong & India 12 Indonesia & Italy 13 Japan & Kenya 14 Laos & Macau 15 Malaysia & Maldives 16 Myanmar & Philippine 17 Russia & Singapore 18 Sri Lanka & Taiwan 19 Thailand & Turkey 20 United Arab Emirates & United Kingdom 21 United States of America & Vietnam 22 Branch List SKYhub Global Network 425 BRANCHES IN 154 CITIES ALL AROUND THE WORLD OPERATES 7,000 EMPLOYEES VIENNA MUNICH MACAU HONG KONG FRANKFURT GUANGZHOU DUSSELDORF BEIJING AMSTERDAM MOSCOW HAINAN QINGDAO PARIS SHANGHAI DANANG LONDON DALIAN BANFF ULAN BATOR SEOUL HANOI VANCOUVER ZURICH PHNOM PENH BUSAN SEATTLE TORONTO MILAN ISTANBUL SIEM REAP CHICAGO BOSTON VIENTIANE SAN FRANCISCO CAPPADOCIA JAPAN NEW YORK MADRID CHENGDU LAS VEGAS CAIRO DHAKA LOS ANGELES BARCELONA SAN DIEGO DUBAI DELHI ORLANDO FLORENCE CHIANG MAI TAIPEI MIAMI YANGON HONOLULU MAUI ROME XIAMEN MEXICO CITY SRIRACHA CANCUN BANGKOK MANILA SAIPAN KONA CHENNAI Map CEBU GUAM NAIROBI COLUMBO KOTA KINABALU Service MALDIVES SURABAYA Sales Office PATTAYA BALI PHUKET CAIRNS SAO PAULO LANGKAWI FIJI www.mySKYhub.com BRISBANE PENANG PERTH GOLD COAST Australia & Brazil KUALA LUMPUR SYDNEY SINGAPORE MELBOURNE AUCKLAND Cambodia & China HO CHI MINH Egypt & France JAKARTA Guam & Hawaii Hong Kong & India Indonesia & Italy Japan & Kenya Our ever-expanding network enables us to get Laos & Macau timely information about countries worldwide Malaysia & Maldives Myanmar & Philippine and make all kinds of arrangements smoothly. -

1 Sustainability Report 2018

K C M Y RED 80K 40K K C M Y GREEN 80C 40C K C M Y BLUE 80M 40M K C M Y 80Y 40Y Paper K C M Y RED 80K 40K K C M Y GREEN 80C 40C K C M Y BLUE 80M 40M K C M Y 80Y 40Y Paper K C M Y RED 80K 40K K C M Y GREEN 80C 40C K C M Y BLUE 80M 40M K C M Y 80Y 40Y Paper K C M Y RED 80K 40K K C Prime SR Cover proofing.pdf 1 4/8/19 10:10 PM C M Y CM MY CY CMY K Sustainability Report 2018 1 SM @ 60 Years About this Report (102-46,47,49,50,51,54) SM Prime Holdings, Inc. presents the 11th annual Sustainability Report and the 7th edition following the Global Reporting Initiative (GRI). This Sustainability Report features highlights from the Company’s material topics on: ECONOMIC ENVIRONMENTAL SOCIAL Economic Performance Energy Employment Indirect Economic Impacts Water Occupational Health and Safety Anti-Corruption Emissions Training and Education Anti-competitive Behavior Effluents and Waste Diversity and Equal Opportunities Biodiversity Non-discrimination Environmental Compliance Security Practices Human Rights Assessment Local Communities Socio-economic Compliance The sustainability information contained herein covers reporting from January to December 2018 and will discuss SM Prime’s assets where the business has organizational boundary. This report has been prepared in accordance with the GRI Standards: Core option. The 2018 SM Prime Sustainability Report must be read in conjunction with the 2018 SM Prime Annual Report. -

The Performance of the Smart Cities in China—A Comparative Study by Means of Self-Organizing Maps and Social Networks Analysis

Sustainability 2015, 7, 7604-7621; doi:10.3390/su7067604 OPEN ACCESS sustainability ISSN 2071-1050 www.mdpi.com/journal/sustainability Article The Performance of the Smart Cities in China—A Comparative Study by Means of Self-Organizing Maps and Social Networks Analysis Dong Lu 1, Ye Tian 2, Vincent Y. Liu 3,* and Yi Zhang 4 1 School of Business, Sichuan Normal University, Chengdu 610101, China; E-Mail: [email protected] 2 School of Economics and Management, Southwest Jiaotong University, Chengdu 610031, China; E-Mail: [email protected] 3 School of Business, Macau University of Science and Technology, Taipa, Macau 4 Department of Mathematics, Tongji University, Shanghai 200092, China; E-Mail: [email protected] * Author to whom correspondence should be addressed; E-Mail: [email protected]; Tel.: +853-8897-2862. Academic Editor: Marc A. Rosen Received: 3 November 2014 / Accepted: 2 June 2015 / Published: 12 June 2015 Abstract: Smart cities link the city services, citizens, resource and infrastructures together and form the heart of the modern society. As a “smart” ecosystem, smart cities focus on sustainable growth, efficiency, productivity and environmentally friendly development. By comparing with the European Union, North America and other countries, smart cities in China are still in the preliminary stage. This study offers a comparative analysis of ten smart cities in China on the basis of an extensive database covering two time periods: 2005–2007 and 2008–2010. The unsupervised computational neural network self-organizing map (SOM) analysis is adopted to map out the various cities based on their performance. -

Rethinking Smart Cities

RETHINKING SMART CITIES ICT for New-type Urbanization and Public Participation at the City and Community Level in China © 2015 United Nations Development Programme China 2 Liangmahe Nanlu Beijing 100600, P.R. China Telephone: +86-10 8532-0800 Internet: www.cn.undp.org Authors of the report: James Kin-Sing Chan Programme Coordinator (Governance & Urbanization), Poverty Equity and Governance Team, UNDP China. Email: [email protected] Samantha Anderson Senior Advisor on Sustainable Cities and Climate Change, Climate Change Team, UNDP China. Email: [email protected] Cover design: Lucy Huang The analyses and recommendations expressed in this publication are those of the authors and do not necessarily represent those of the United Nations, including UNDP, or the UN Member States. CONTENTS FOREWORDS 01 ACKNOWLEDGEMENTS 04 INTRODUCTION 05 PART I BACKGROUND AND POLICY OVERVIEW 07 OVERVIEW OF CHINESE POLICIES ON SMART CITIES 07 IN TRANSITION: FROM TECHCENTRED TO HUMANCENTRED 09 LONG ROAD AHEAD: THE IMPLEMENTATION OF PUBLIC PARTICIPATION IN CHINA 10 PART II CASE STUDIES OF CITY AND COMMUNITY ICT INITIATIVES FOR PUBLIC PARTICIPATION 13 1. FEEDBACK MECHANISMS FOR INCREASING CITIZEN ENGAGEMENT AND GOVERNMENT ACCOUNTABILITY 13 2. MEASURES TO IMPROVE THE QUALITY AND RESPONSIVENESS OF PUBLIC SERVICE DELIVERY 14 USING SOCIAL MEDIA TO IMPROVE RESPONSIVENESS OF SOCIAL SERVICES 15 USING SMART INITIATIVES TO IMPROVE QUALITY OF HEALTHCARE AND EDUCATION 16 3. INFORMATION ACCESS INITIATIVES TO HELP CITIZENS MAKE BETTER MARKET AND LIFE CHOICES 17 4. PLATFORMS FOR COMMUNITY AND NEIGHBOURHOODBUILDING 18 PART III ANALYSIS AND POLICY RECOMMENDATIONS 19 1. FORMULATE A CLEAR VISION AND STRATEGIC PLAN FOR SMART CITY DEVELOPMENT 19 2. -

3M-NANO 2012: Keynote Reports

Conference Program Digest The 7th International Conference on Manipulation, Manufacturing and Measurement on the Nanoscale IEEE 3M-NANO 2017 Shanghai, China 7 – 11 August 2017 Organized by: IEEE Nanotechnology Council Shanghai Jiao Tong University, China Changchun University of Science and Technology, China International Research Centre for Nano Handling and Manufacturing of China, China 3M-NANO International Society University of Bedfordshire, UK Aarhus University, Denmark University of Warwick, UK University of South Wales, UK Tampere University of Technology, Finland University of Shanghai Cooperation Organization Sponsored by: National Natural Science Foundation of China Ministry of Science and Technology of the People's Republic of China Ministry of Education of the People’s Republic of China Research Executive Agency (REA), European Commission Jilin Provincial Science & Technology Department, China IFToMM (technically sponsored) International Society for Nanomanufacturing Greetings On behalf of the organizing committee, it is our great pleasure and honor to welcome you in Shanghai at IEEE 3M-NANO 2017 conference! 3M-NANO is an annual International Conference on Manipulation, Manufacturing and Measurement on the Nanoscale, held for the seventh time in Shanghai. 3M-NANO covers advanced technologies for handling and fabrication on the nanoscale. The ultimate ambition of this conference series is to bridge the gap between nanosciences and engineering sciences, aiming at emerging market and technology opportunities. The advanced technologies for manipulation, manufacturing and measurement on the nanoscale promise novel revolutionary products and methods in numerous areas of application. Scientists working in different research fields are invited to discuss theories, technologies and applications related to manipulation, manufacturing and measurement on the nanoscale. -

China City Profiles 2012 an Overview of 20 Retail Locations

China City Profiles 2012 An Overview of 20 Retail Locations joneslanglasalle.com.cn China Retail Profiles 2012 The China market presents a compelling opportunity for retailers. China’s retail sector has long been firmly underpinned by solid demand fundamentals–massive population, rapid urbanization and an emerging consumer class. Annual private consumption has tripled in the last decade, and China is on track to become the world’s second largest consumer market by 2015. China’s consumer class will more than double from 198 million people today to 500 million by 2022, if we define it as people earning over USD 5,000 per annum in constant 2005 dollars. It is never too late to enter the China market. China’s economic growth model is undergoing a shift from investment- led growth to consumption-led growth. It is widely recognized that government-led investment, while effective in the short term, is not the solution to long-term growth. With its massive accumulated household savings and low household debt levels, China’s domestic consumption offers immense headroom for growth. China’s leaders are acutely aware of the urgency to effect changes now and are more eager than ever before to tap its consumers for growth. Already, the government has set in motion a comprehensive range of pro-consumption policies to orchestrate a consumption boom. Broadly, the wide-ranging policies include wage increases, tax adjustments, strengthening of the social safety net, job creation, promotion of urbanization and affordable housing. While the traditional long-term demand drivers–urbanization, rising wealth and robust income growth–remain firmly intact, China’s retail story has just been given a structural boost. -

Transmissibility of COVID-19 in 11 Major Cities in China and Its

Guo et al. Infectious Diseases of Poverty (2020) 9:87 https://doi.org/10.1186/s40249-020-00708-0 RESEARCH ARTICLE Open Access Transmissibility of COVID-19 in 11 major cities in China and its association with temperature and humidity in Beijing, Shanghai, Guangzhou, and Chengdu Xiao-Jing Guo, Hui Zhang* and Yi-Ping Zeng Abstract Background: The new coronavirus disease COVID-19 began in December 2019 and has spread rapidly by human-to-human transmission. This study evaluated the transmissibility of the infectious disease and analyzed its association with temperature and humidity to study the propagation pattern of COVID-19. Methods: In this study, we revised the reported data in Wuhan based on several assumptions to estimate the actual number of confirmed cases considering that perhaps not all cases could be detected and reported in the complex situation there. Then we used the equation derived from the Susceptible-Exposed-Infectious-Recovered (SEIR) model to calculate R0 from January 24, 2020 to February 13, 2020 in 11 major cities in China for comparison. With the calculation results, we conducted correlation analysis and regression analysis between R0 and temperature and humidity for four major cities in China to see the association between the transmissibility of COVID-19 and the weather variables. Results: It was estimated that the cumulative number of confirmed cases had exceeded 45 000 by February 13, 2020 in Wuhan. The average R0 in Wuhan was 2.7, significantly higher than those in other cities ranging from 1.8 to 2.4. The inflection points in the cities outside Hubei Province were between January 30, 2020 and February 3, 2020, while there had not been an obvious downward trend of R0 in Wuhan. -

Current Trends in Chinese Fashion Markets - Characteristics of Chinese Fashion Markets and Launching Strategies to Success

Journal of Fashion Business Vol. 7, No. 3, pp.45~53(2003) Current Trends in Chinese Fashion Markets - Characteristics of Chinese Fashion Markets and Launching Strategies to Success- Cheng Chung Chung CEO, Lace International Development Co., Ltd. Shanghai Abstract In the face of trade opportunity of Chinese reformation and opening and the future largest single market, global or multinational companies and Korean, Japanese, Chinese, Hong Kong’s and Taiwan’s companies will go all out to catch hold of one quotient. One trading war is about to start for funds, elitists, technique, and management in China now. It might be difficult to get profits in Chinese markets. However, risks can bring challenges, and competition can make progress. It’s time to prepare for the challenges in the golden opportunity laid in front of us all. Key words: China, department store, fashion market, shopping mall I. Introduction investments were focused on the low-grade products or outdated ones in the foreign markets. Since the policy of reformation and opening Meanwhile, labor quality was low, and efficiency took place in the 1980s, there had been great was very low partly due to the bureaucracy.1) economic development in the Mainland China. Especially after Deng Xiao Ping made a round of visits in South China in 1992, the reformation and II. Retrospections and Current Trends opening accelerated been fully speeded. In the in Chinese Fashion Industries recent 10 years, China’s economic growth rate has been over 7 % each year, which is more 1. Decision on entry into Shanghai significant when the global economics is declining today. -

2017 Sustainability Report

2017 SUSTAINABILITY REPORT SM PRIME HOLDINGS, INC. 10th Floor, Mall of Asia Arena Annex Building Coral Way cor. J.W. Diokno Boulevard Mall of Asia Complex Pasay City 1300 Philippines Email: [email protected] www.smprime.com Vision To build and manage innovative integrated property developments that are catalysts for a better quality of life. Mission We will serve the ever-changing needs and aspirations of our customers, provide opportunities for the professional growth of our employees, foster social responsibility in the communities we serve, enhance shareholder value for our investors and ensure that everything we do safeguards Contents a healthy environment for future generations. 2 About SM Prime 3 About this Report 4 President’s Report 5 Aligning Shared Values 11 Economic Value Performance 13 Sustainable Operations 20 Employee Engagement 26 Corporate Governance 33 Awards and Accolades 34 GRI Content Index 37 Corporate Information 1 SM Prime Holdings, Inc. Sustainability Report 2017 About SM Prime SM Prime Holdings, Inc. (SMPH) is one of the largest integrated property developers in Southeast Asia. It offers innovative and sustainable lifestyle cities with the development of malls, residences, offices, hotels and convention centers. It is also the largest, in terms of asset, in the Philippines. 2 SM Prime Holdings, Inc. Sustainability Report 2017 About this Report This is SM Prime’s 10th annual Sustainability Report and sixth time following the Global Reporting Initiative (GRI) Guidelines. This report is in accordance with the GRI Sustainability Reporting Standards. It covers the environmental, social, economic, and governance information of SM Prime in the Philippines and in China for the year 2017. -

Commercial Real Estate Development in China

IRE|BS Beiträge zur Immobilienwirtschaft COMMERCIAL REAL ESTATE DEVELOPMENT IN CHINA FRAMEWORK AND CASE STUDIES Editoren: Prof. Dr. Tobias Just Xin Lu Heft 20 Herausgeber: IRE|BS International Real Estate Business School, Universität Regensburg www.irebs.de ISSN 2197 - 7720 Copyright © IRE|BS International Real Estate Business School 2018, alle Rechte vorbehalten Verantwortlich für den Inhalt dieses Bandes: Prof. Dr. Tobias Just, IREBS Xin Lu, ECE Europa Bau- und Projektmanagement GmbH RECHTLICHE HINWEISE ZUGANG Die Publikation von und der Zugang zu Informationen in dieser Studie kann durch lokale Vorschriften in gewissen Ländern eingeschränkt sein. Diese Studie richtet sich ausdrücklich nicht an Personen in Staaten, in denen (aufgrund der Staatsangehörigkeit bzw. des Wohnsitzes der jeweiligen Person oder aus anderen Gründen) entsprechende Einschränkungen gelten. Insbesondere richtet sich die Studie nicht an Bürger der USA sowie an Personen, die in den USA oder in einem ihrer Territorien, Besitzungen oder sonstigen Gebieten, die der Gerichtshoheit der USA unterstehen, wohnhaft sind oder dort ihren gewöhnlichen Aufenthalt haben. Personen, für welche entsprechende Beschränkungen gelten, dürfen nicht, weder online noch in anderer Form, auf diese Studie zugreifen. KEIN ANGEBOT Der Inhalt dieser Studie dient ausschließlich Informationszwecken und stellt keine Werbung, kein Angebot und keine Empfehlung zum Kauf oder Verkauf von Finanzinstrumenten oder zum Tätigen irgendwelcher Anlagegeschäfte oder sonstiger Transaktionen dar. Diese Studie (einschließlich -

SM Prime Holdings, Inc. SEC Form 17-A-2020 15April2021 With

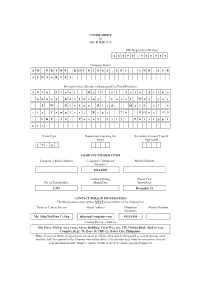

COVER SHEET for SEC FORM 17-A SEC Registration Number A S 0 9 4 - 0 0 0 0 8 8 Company Name S M P R I M E H O L D I N G S , I N C . A N D S U B S I D I A R I E S Principal Office (No./Street/Barangay/City/Town/Province) 1 0 t h F l o o r , M a l l o f A s i a A r e n a A n n e x B u i l d i n g , C o r a l W A y c o r . J . W . D i o k n o B l v d . , M a l L o f A s i a C o m p l e x , B r g y . 7 6 , Z O n e 1 0 , C B P - 1 A , P a s a y C i t y , P h i l i p p i n e s Form Type Department requiring the Secondary License Type, If report Applicable 1 7 - A COMPANY INFORMATION Company’s Email Address Company’s Telephone Mobile Number Number/s 8831-1000 Annual Meeting Fiscal Year No. of Stockholders Month/Day Month/Day 2,395 December 31 CONTACT PERSON INFORMATION The designated contact person MUST be an Officer of the Corporation Name of Contact Person Email Address Telephone Mobile Number Number/s Mr. John Nai Peng C. Ong [email protected] 8831-1000 Contact Person’s Address 10th Floor, Mall of Asia Arena Annex Building, Coral Way cor.