2015 SMPHI Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Field Trip Packages

FIELD TRIP PACKAGES Affordable Educational Field Trip Packages For as low as PHP 970 / pax! Affordable Educational Field Trip Packages for Pre-School, Elementary & High School levels in the Philippines. Throycath Travel and Tours Agency brings what students learn from books to real life. Actual learning with hands- on experience helps them see and understand lessons on an exciting, and enjoyable perspective. Check out our lists of destinations and find the perfect educational tour package for you. Metro Manila Rainforest Adventure Experience Metropolitan Museum The Mind Museum Upside Down Museum Kidzania Ark Avilon AFP Museum GSIS Museo ng Sining Bantayog Kagitingan Museum National Museum Mall of Asia Museo Ng Katipunan Star City Doll Joy Museum BSP Money Museum Manila Ocean Park Planetarium Intramuros Lights & Sound Art in Island Luneta Park Fort Santiago Quezon City Experience Museo Pambata San Agustin Museum Ayala Museum SM Nido Science Discovery Phil. Aerospace Museum La Mesa Dam Eco Park Manila Crocodile Park Seri Fantasy Land Laguna Pampanga / Clark Villa Escudero SandBox Pampanga Rizal Shrine Lola Corazon Leisure Farm Enchanted Kingdom Puning Hot Spring & Restaurant Forest Club Nayong Pilipino sa Clark Expo IRRI Museum Paradise Ranch Museum of Natural History Zoocobia Makiling Botanic Garden Clark Museum Center for Philippine Raptors Air Force City Park Caliraya Resort Club Dino Island Nagcarlan Underground Cemetery Fontana Water Park 7 Lakes San Pablo Cavite Bulacan Tagaytay Picnic Grove Shercon Resort Sky Ranch Eagle Point Resort -

Fact-Sheet-Discovery-Country-Suites

FACT SHEET THE HOTEL Perched on a ridge overlooking the world-renowned Taal Volcano, Discovery Country Suites is a charming seven-suite Bed and Breakfast in cool and breezy Tagaytay, a short drive away from Manila. The cozy manor home is a haven for the majestic view of Taal Lake and breathtaking sunsets, while colorful parks, rustic farms and quaint coffee shops are just moments away. A stay in Discovery Country Suites comes with exquisite wine and cheese at sundown, and delectable milk and cookies at bedtime. The city escape is home to the revered Restaurant Verbena, known for its contemporary country cuisine and its signature Verbena Country Breakfast. LOCATION 59 kilometers from Manila (approximately 90 minutes away by car) Nearby sites: Taal Lake, Taal Volcano, and Sky Ranch Near golf courses, spiritual sites, organic farms and spas Approximately an hour away from beaches and dive sites in Batangas GUESTROOMS 7 themed suites, each with a distinct character inspired by country living Rooms Location Area Room Configuration Andalucia 3rd floor 33 sqm • Two double beds • Bathroom en suite • Two single-seater couches Ceylon Ground floor 33 sqm • One king size bed (garden level) • Bathroom en suite • Four garden seats at the porch Saint-Tropez 2nd floor 37 sqm • Two double beds (lobby level) • Bathroom en suite • Two single-seater couches Siam Ground floor 55 sqm • Two queen size beds (garden level) • Bathroom en suite • Garden seats at the porch Nara Ground floor 57 sqm • One king size bed (garden level) • Bathroom en suite • Two garden -

Cost of Doing Business in the Province of Iloilo 2017 1

COST OF DOING BUSINESS IN THE PROVINCE OF ILOILO 2017 Cost of Doing Business in the Province of Iloilo 2017 1 2 Cost of Doing Business in the Province of Iloilo 2017 F O R E W O R D The COST OF DOING BUSINESS is Iloilo Provincial Government’s initiative that provides pertinent information to investors, researchers, and development planners on business opportunities and investment requirements of different trade and business sectors in the Province This material features rates of utilities, such as water, power and communication rates, minimum wage rates, government regulations and licenses, taxes on businesses, transportation and freight rates, directories of hotels or pension houses, and financial institutions. With this publication, we hope that investors and development planners as well as other interested individuals and groups will be able to come up with appropriate investment approaches and development strategies for their respective undertakings and as a whole for a sustainable economic growth of the Province of Iloilo. Cost of Doing Business in the Province of Iloilo 2017 3 4 Cost of Doing Business in the Province of Iloilo 2017 TABLE OF CONTENTS Foreword I. Business and Investment Opportunities 7 II. Requirements in Starting a Business 19 III. Business Taxes and Licenses 25 IV. Minimum Daily Wage Rates 45 V. Real Property 47 VI. Utilities 57 A. Power Rates 58 B. Water Rates 58 C. Communication 59 1. Communication Facilities 59 2. Land Line Rates 59 3. Cellular Phone Rates 60 4. Advertising Rates 61 5. Postal Rates 66 6. Letter/Cargo Forwarders Freight Rates 68 VII. -

List of Payment Centers (As of January 2016)

List of Payment Centers (as of January 2016) BRANCH NAME LOCATION NAME LOCATION ADDRESS CUBAO DEPARTMENT STORE SM Cubao Bldg., Araneta Center, Socorro Cubao, Quezon City SAVEMORE NEPA Q. MART SAVEMORE NEPA Q. MART Savemore Market Nepa Q-Mart, G/F & 2F 770 St., Rose Bldg. Edsa cor K-G St. West Kamias, Q.C. SAVEMORE P. TUAZON SAVEMORE P. TUAZON Savemore Market P. Tuazon A.D. Legaspi St.,cor P. Tuazon Blvd., Marilag,Proj 4, Q.C. 1109 SAVEMORE ARANETA SAVEMORE ARANETA Savemore Market COD Cubao Gen Romulo St., Araneta Center Cubao Quezon City SAVEMORE ANONAS SAVEMORE ANONAS Savemore Market Anonas, Maamo St. Road, Lot 30 V. Luna and Anonas Extn. Sikatuna, Q.C. 1101 HYPERMARKET CUBAO HYPERMARKET CUBAO SM Hypermarket Cubao, Main Ave cor EDSA, Quezon QUIAPO DEPARTMENT STORE SM Quiapo , MDC Bldg., C. Palanca St., Quiapo, Manila SAVEMORE STA. CRUZ SAVEMORE STA. CRUZ Savemore Market Sta Cruz 665 Rizal Avenue, Jennet & Lord Theater, Sta Cruz, Manila MAKATI DEPARTMENT STORE SM Makati Building Ayala Center, Brgy. San Lorenzo Village, Makati City SAVEMORE PASONG TAMO SAVEMORE PASONG TAMO Savemore-Market Pasong Tamo, 2256 Chino Roces Ave.,Ext EDSA, Brgy. Magallanes, Makati City 1231 SAVEMORE MARKET PLACE SAVEMORE MARKET PLACE SM Marketplace A Venue Hall, Antel Lifestyle City, 7829, Makati Avenue, Poblacion, Makati City HYPERMARKET JAZZ HYPERMARKET JAZZ SM Hypermarket Jazz Nicanor Garcia corner Jupiter Street, Brgy Bel Air, Makati City SAVEMORE LIGHT RESIDENCES SAVEMORE LIGHT RESIDENCES Savemore Market Light Residences Edsa Cor. Madison St. Brgy. Barranca, Mandaluyong City HARRISON DEPARTMENT STORE SM Harrison Plaza Complex, Malate, Manila 1004 HYPERMARKET ADRIATICO DEPARTMENT STORE SM Hypermart Adriatico M.H. -

Jcb Unique Dining Experience Merchants

JCB UNIQUE DINING EXPERIENCE MERCHANTS 7107 Culture + Cuisine Restaurant • G/F, Treston Bldg., BGC Alba Restaurante Espaǹol • Bel-Air, Makati City • Tomas Morato Quezon City • Westgate Center,Muntinlupa City • Prism Plaza, TwoEcom Center Building Mall of Asia Complex, Pasay City • Estancia Mall Capitol Commons, Pasig City Alchemy - Bistro • 4893 Durban St. Poblacion Makati Bari Uma Ramen • Ground Floor Serendra, Bonifacio High Street, BGC • Ayala Center Cebu Burgoo • The Block, North Edsa • SM City Marikina • The District Imus • Solenad 3, Nuvali • Robinsons Galleria • SM Mall of Asia • Gateway Mall • SM Southmall • Fairview Terraces • Vista Mall, Taguig Butamaru • West Gate Center, Alabang, Muntinlupa City • Technopoint Bldg, Pasig Chairman Wang's • Molito Lifestyle Bldg, Alabang Chotto Matte • Net Park, 5th Avenue, Bonifacio Global City, Taguig City Gumbo • SM Mall of Asia • Mega Atrium, Megamall • Robinsons Magnolia Hatsu Hana Tei • Herald Suites, Don Chino Roces Avenue, Makati City Ikomai & Tochi • ACI Group Building Makati City Izakaya Sensu • Net Park Building Bonifacio, Global City Kichitora • Bonifacio Highstreet Central, Bonifacio Global City • SM Megamall La Cabrera • Ayala Business Center, 6750 Ayala Avenue Mireio • 1 Raffles Drive Makati Avenue, Makati City Motto Motto • Ground Floor, Serendra, Bonifacio Global City, Taguig City Txanton • Alegria Alta Building,Makati City Wooden Horse Steakhouse • Molito Complex Alabang Yanagi • Midas Hotel Roxas Blvd, Pasay Yoshinoya • Glorietta Mall • SMCity Cebu North • Robinsons, Cybergate -

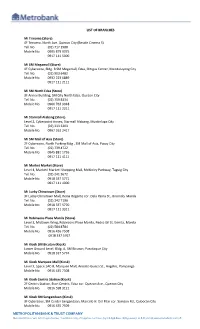

Metropolitan Bank & Trust Company List

LIST OF BRANCHES Mi Trinoma (Store) 4F Trinoma, North Ave. Quezon City (Beside Cinema 5) Tel. No. (02) 717 1980 Mobile No. 0995 879 9075 0917 111 5000 Mi SM Megamall (Store) 4F Cyberzone, Bldg. B SM Megamall, Edsa, Ortigas Center, Mandaluyong City Tel. No. (02) 903 6482 Mobile No. 0932 223 6889 0917 111 2111 Mi SM North Edsa (Store) 3F Annex Building, SM City North Edsa, Quezon City Tel. No. (02) 759 8334 Mobile No. 0966 763 9048 0917 111 2211 Mi Starmall Alabang (Store) Level 2, Cyberpoint Annex, Starmall Alabang, Muntinlupa City Tel. No. (02) 333 3203 Mobile No. 0967 262 2417 Mi SM Mall of Asia (Store) 2F Cyberzone, North Parking Bldg., SM Mall of Asia, Pasay City Tel. No. (02) 739 4722 Mobile No. 0945 881 1726 0917 111 4111 Mi Market Market (Store) Level 4, Market! Market! Shopping Mall, McKinley Parkway, Taguig City Tel. No. (02) 241 3672 Mobile No. 0918 337 5771 0917 111 4000 Mi Lucky Chinatown (Store) 3F Lucky Chinatown Mall, Reina Regente cor. Dela Reina St., Binondo, Manila Tel. No. (02) 242 7190 Mobile No. 0918 337 5770 0917 111 3311 Mi Robinsons Place Manila (Store) Level 3, Midtown Wing, Robinsons Place Manila, Pedro Gil St. Ermita, Manila Tel. No. (02) 584 8784 Mobile No. 0916 436 7508 0918 337 5767 Mi Kiosk SM Bicutan (Kiosk) Lower Ground Level, Bldg. A, SM Bicutan, Parañaque City Mobile No. 0918 337 5774 Mi Kiosk Marquee Mall (Kiosk) Level 3, Space 1AC-8, Marquee Mall, Aniceto Gueco St., Angeles, Pampanga Mobile No. 0916 435 7508 Mi Kiosk Centris Station (Kiosk) 2F Centris Station, Eton Centris, Edsa cor. -

MEMO EXPRESS.Pdf

MERCHANT BRANCHES MEMO EXPRESS SM SOUTHMALL ALABANG ZAPOTE RD ALMANZA UNO LAS PINAS CITY 1740 MEMO EXPRESS CYBERZONE SM CITY FAIRVIEW REGALADO AVE. GREATER LAGRO QUEZON CITY 1100 MEMO EXPRESS UNIT CZ24 SM CITY BF D.A.S.A COR PRES AVE BRGY BF HOMES PARANAQUE CITY 1700 MEMO EXPRESS 345 ALABANG ZAPOTE RD ROBINSON PLACE LAS PINAS BRGY TALON LAS PINAS CITY 1740 MEMO EXPRESS UNIT 303 2F ARCADIA BLDG SANTA ROSA TAGAYTAY ROAD DON JOSE STA. ROSA CITY LAGUNA 4026 MEMO EXPRESS CZ234 SM CITY BACOLOD RECLAMATION ARE BACOLOD CITY 6100 MEMO EXPRESS SM CENTER ANGONO MANILA EAST ROAD SAN ISIDRO ANGONO RIZAL 1930 MEMO EXPRESS SM MEGA CENTER MELENCIO SAN ROQUE CABANATUAN CITY NUEVA ECIJA 3100 MEMO EXPRESS CY 20 SM CITY GENSAN CORNER SANTIAGO BLVD SAN MIGUEL ST. LAGAO GEN SANTOS CITY 9500 MEMO EXPRESS SPACE 3-052 3F NEW GLORIETTA 2 AYALA CENTER SAN LORENZO MAKATI CITY 1224 MEMO EXPRESS L3-341 ROBINSONS NORTH ABUCAY BRGY 91 TACLOBAN CITY 6500 MEMO EXPRESS L2 2019 ROBINSON PLACE ORMOC CHRYSANTHEMUM SUBD. COGON ORMOC CITY 6541 MEMO EXPRESS CZ 3008 17 SM CITY LEGAZPI TAHAO ROAD LEGAZPI CITY ALBAY 4500 MEMO EXPRESS RM 814 PACIFIC LAND CTR BLDG QUITIN PAREDES ST. BRGY 289 ZONE 027 DIST 111 BINONDO MANILA 1006 MEMO EXPRESS SPACE 3111 ABREEZA MALL JP LAUREL AVE DAVAO CITY 8000 MEMO EXPRESS THE DISTRICT MALL AGUINALDO HIWAY COR. DAANG HARI ROAD ANABU II D CITY OF IMUS CAVITE 4103 MEMO EXPRESS L3 ROBINSON PLACE SANTIAGO MABINI SANTIAGO CITY 3311 MEMO EXPRESS 239 SM CITY CAUAYAN MAHARLIKA HIGHWAY DISTRICT 2 CAUAYAN CITY ISABELA 3305 MEMO EXPRESS CENTRIO MALL CM RECTO AVENUE BRGY 24 CAGAYAN DE ORO CITY 9000 MEMO EXPRESS L3-338 ROBINSON PLACE MALOLOS SUMAPANG MATANDA CITY MALOLOS BULACAN 3300 MEMO EXPRESS 3RD LEVEL SPACE 3029A FAIRVIEW TERRACES QUIRINO HIGHWAY PASONG PUTIK QUEZON CITY 1012 MEMO EXPRESS SPACE 2 02448 ROBINSON PLACE PUEBLO DE PANAY LAWAAN ROXAS CITY 5800 MEMO EXPRESS CZ 015 25 SM CITY SAN JOSE DEL MONTE BRGY TUNGKONG MANGGA CITY OF SAN JOSE DEL MONTE BULACAN 3023 MEMO EXPRESS UNIT 326 3RD FLR AYALA MALLS LEGAZPI RIZAL ST. -

Melco International Development Limited

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult your licensed securities dealer or other registered dealer in securities, bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Melco International Development Limited, you should at once hand this circular to the purchaser or transferee or to the bank, the licensed securities dealer or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. Melco International Development Limited (Incorporated in Hong Kong with limited liability) Website: www.melco-group.com (Stock Code: 200) MAJOR TRANSACTION MELCO RESORTS & ENTERTAINMENT LIMITED NEW SHARE REPURCHASE PROGRAM A letter from the Board is set out on pages 3 to 11 of this circular. 25 April 2019 CONTENTS Page DEFINITIONS ................................................................ 1 LETTER FROM THE BOARD ................................................... 3 APPENDIX I – FINANCIAL INFORMATION OF THE GROUP ................. 12 APPENDIX II – FINANCIAL INFORMATION OF MELCO RESORTS ............ 15 APPENDIX III – UNAUDITED PRO FORMA FINANCIAL INFORMATION OF THE GROUP ......................................... 256 APPENDIX IV – GENERAL INFORMATION.................................. 263 This circular is printed on environmentally friendly paper. -

7-Eleven Partner Locations Nationwide for Cash-In & Loan Repayment Transactions Only

7-ELEVEN PARTNER LOCATIONS NATIONWIDE as of March 2021 FOR CASH-IN & LOAN REPAYMENT TRANSACTIONS ONLY REGION TOWN/CITY BRGY. PARTNER OUTLET TYPE ADDRESS REGION XIII AGUSAN DEL Brgy. 25 CAPITOL DRIVE Cash-in and NATIONAL HIGHWAY, 54 RABE NORTE Loan Repayment SUBDIVISION, TAGUM CITY REGION XIII AGUSAN DEL Brgy. 3 BUENAVISTA Cash-in and MDC BUILDING, DAHICAN, NORTE Loan Repayment NATIONAL HIGHWAY, MATI CITY, DAVAO ORIENTAL REGION XIII AGUSAN DEL Brgy. 4 (Poblacion) NASIPIT CENTRO Cash-in and AJT GAS STATION, KINGKING NORTE Loan Repayment PANTUKAN, COMPOSTELA VALLEY PROVINCE REGION XIII AGUSAN DEL Brgy. 8 CPI CABADBARAN Cash-in and OJEDA AVENUE, CORNER ASIS NORTE Loan Repayment STREET, CABADBARAN CITY, AGUSAN DEL NORTE REGION XIII AGUSAN DEL Brgy. Diego Silang PRINCE HOTEL Cash-in and PRK. SAMPAGUITA, VISAYAN NORTE Loan Repayment VILLAGE, TAGUM CITY, DAVAO DEL NORTE REGION XIII AGUSAN DEL Brgy. Doongan BUTUAN DOCTORS Cash-in and CROSSING MANIKLING, SAN NORTE Loan Repayment ISIDRO, DAVAO ORIENTAL REGION XIII AGUSAN DEL Brgy. Kananga UNI-V SOUTH MONTILLA Cash-in and RIZAL ST., CORNER ZAMORA ST., NORTE Loan Repayment BRGY. CENTRAL, MATI CITY, DAVAO ORIENTAL REGION XIII AGUSAN DEL Brgy. Libertad CPI LIBERTAD Cash-in and EIGHT HORSES ENTERPRISES II NORTE Loan Repayment BLDG., BRGY. POBLACION, LUPON, DAVAO ORIENTAL REGION XIII AGUSAN DEL Brgy. Mabini CABADBARAN TERMINAL Cash-in and NATIONAL HIGHWAY, POBLACION, NORTE Loan Repayment BANAYBANAY, DVAO ORIENTAL REGION XIII AGUSAN DEL Brgy. Mangagoy SHELL MANGAGOY Cash-in and EIGHT HORSES ENTERPRISES II NORTE Loan Repayment BLDG., BRGY. POBLACION, LUPON, DAVAO ORIENTAL REGION XIII AGUSAN DEL Brgy. Montilla SJIT MONTILLA Cash-in and CAMP UTLEY AVE., APOKON, NORTE Loan Repayment TAGUM CITY, DAVAO DEL NORTE CIMB Bank Philippines 28th Floor, Ore Central Tower, 9th Avenue corner 31st Street, Bonifacio Global City, Taguig City (+632) 85800100 www.cimbbank.com.ph Page 1 REGION XIII AGUSAN DEL Brgy. -

Banking-Sched-Dec-30-2019.Pdf

BANKING SCHEDULES FOR THE HOLIDAY SEASON Banking Schedule of Selected Branches December 30,2019 Selected Regular Branches A. Regular Opening Hours Up to 3:00 PM LUZON Abra - Bangued Albay - Daraga Albay - Tabaco Angeles - Balibago Angeles - Miranda Antipolo - Circumferential Rd. Aurora Blvd. - Broadway Centrum Baguio - Bokawkan Road Baguio - Harrison Road Baguio - Kennon Road Baguio - Legarda Baguio - Leonard Wood Road Baguio - Luneta Baguio - Marcos Highway Balsigan Baguio - Marcos Highway Centerpoint Baguio - Session Road Balanga - Capitol Drive Baliwag - JP Rizal Balubaran - MacArthur Highway Batangas - Balayan Batangas - Bauan Batangas - Diego Silang Batangas - Gulod Batangas - Nasugbu Batangas City - Rizal Avenue Benguet - La Trinidad Bocaue - MacArthur Highway Bulacan - Bocaue Bulacan - Hagonoy Bulacan - Obando Bulacan - Primark Plaridel Bulacan - San Jose Del Monte Bulacan - San Miguel Bulacan - San Rafael Bulacan - Sapang Palay Bulacan Sta. Maria - Bagbaguin Bulacan Sta. Maria - M.G. de Leon Cagayan - Aparri Caloocan - Primark Deparo Carmen Planas Cavite - Congressional Road Cavite - Dasmariñas Salawag Cavite - Gen Trias San Francisco Cavite - Imus Aguinaldo Highway Cavite - Naic Cavite - P. Burgos Cavite - Silang Aguinaldo Highway Cavite - Trece Martires Cavite Imus - The District Clark - Philexcel Business Park Dagupan - Tapuac Eastwood City - IBM Plaza Echague EDSA - East Caloocan Ilocos Norte - Batac Ilocos Sur - Cabugao Ilocos Sur - Candon Ilocos Sur - Narvacan Iriga City Isabela - Ilagan Isabela - Primark Cordon Isabela - -

Cebu-Ebook.Pdf

About Cebu .........................................................................................................................................2 Sinulog festival....................................................................................................................................3 Cebu Facts and Figures .....................................................................................................................4 Cebu Province Towns & Municipalities...........................................................................................5 Sites About Cebu and Cebu City ......................................................................................................6 Cebu Island, Malapascus, Moalboal Dive Sites...............................................................................8 Cebu City Hotels...............................................................................................................................10 Lapu Lapu Hotels.............................................................................................................................13 Mactan Island Hotels and Resorts..................................................................................................14 Safety Travel Tips ............................................................................................................................16 Cebu City ( Digital pdf Map ) .........................................................................................................17 Mactan Island ( Digital -

Pharmacy Branch Location City Mercury ANTIPOLO CITY POBLACION M.L

MERCURY STORES Pharmacy Branch Location City Mercury ANTIPOLO CITY POBLACION M.L. QUEZON ST. CORNER ANTIPOLO Mercury ANTIPOLO-MASINAG MARCOS HIGHWAY,BO.MAYAMOT ANTIPOLO Mercury ANTIPOLO COGEO-MARCOS HIGHWAY LOTS 14,15 AND 16,MARCOS HWY. ANTIPOLO Mercury ANTIPOLO CATHEDRAL P. OLIVEROS ST. ANTIPOLO Mercury RIZAL ANTIPOLO CITY MALL ANCHOR A,BUILDING A,LOWER ANTIPOLO Mercury Q PLAZA CAINTA IMELDA AVENUE CORNER BARAS Mercury CAINTA-A. BONIFACIO 69 A. BONIFACIO AVENUE BARAS Mercury CAINTA-ORTIGAS AVE. EXT. ORTIGAS AVENUE EXTENSION BARAS Mercury STA. LUCIA MALL CAINTA STA.LUCIA EAST GRANDMALL BARAS Mercury CAINTA RUBLOU MARKET PLACE SPACES G02 AND G03,RUBLOU BARAS Mercury KALOOKAN-9TH AVENUE AURELIO BLDG., CALOOCAN Mercury KALOOKAN-MONUMENTO BONIFACIO MONUMENT CALOOCAN Mercury KALOOKAN-11TH AVENUE RIZAL AVE. COR. 11TH AVE. CALOOCAN Mercury KALOOKAN-MAYPAJO J.P. RIZAL COR. JALA-JALA CALOOCAN Mercury KALOOKAN-PLAZA MABINI ST. COR. P. CALOOCAN Mercury KALOOKAN-SAMSON SAPPHIRE 33 BLDG., CALOOCAN Mercury KALOOKAN-BAGONG SILANG PH2, PCG1,BLK2, LOT 3 CALOOCAN Mercury KALOOKAN C-3 A. MABINI ST.,COR. C-3 RD CALOOCAN Mercury QUEZON CITY ROBINSONS NOVA MARKET BRANCH ROBINSONS PLACE CALOOCAN Mercury ZABARTE TOWN CENTER KALOOKAN ZABARTE TOWN CENTER 588 CALOOCAN Mercury KALOOKAN MONUMENTO GEN. SIMON DYTRONIX BLDG.,CORNER CALOOCAN Mercury KALOOKAN 5TH AVENUE RIZAL AVENUE EXTENSION CALOOCAN Mercury LAS PINAS-ZAPOTE OLD ALABANG HIGHWAY LAS PINAS Mercury LAS PINAS-PHILAM LIFE PHILAM LIFE AVENUE LAS PINAS Mercury LAS PINAS-TALON TALON II, NATIONAL HWY LAS PINAS Mercury LAS PINAS PERPETUAL ALABANG ZAPOTE ROAD LAS PINAS Mercury LAS PINAS-ALMANZA ALABANG-ZAPOTE ROAD LAS PINAS Mercury LAS PINAS CITY PUREGOLD COMMERCIAL UNITS G1-G3 LAS PINAS Mercury LAS PINAS CITY CASIMIRO CASIMIRO COMMERCIAL BLDG.