Pursuing New Opportunities for Growth

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Top 100 Retailers in Asia 2020

Top 100 Retailers in Asia 2020 DEEPIKA CHANDRASEKAR AND CLARE LEE Not to be distributed without permission. The data included in this document is accurate according to Passport, Euromonitor International’s market research database, at time of publication: May 2020 Top 100 Retailers in Asia 2020 DEEPIKA CHANDRASEKAR CLARE LEE CONNECT WITH US © 2020 Euromonitor International Contents 1 Asia Pacific as an Innovation Hub 2 The Asian Landscape: Top 100 Retailers in Asia Pacific 5 Key Retailing Categories 11 Regional Spotlight: Southeast Asia 14 Country Profiles 26 Coronavirus: Outlook of Asia Pacific’s Retailing Industry on the Back of the Pandemic 28 Definitions 33 About the Authors 34 How Can Euromonitor International Help? © Euromonitor International Asia Pacific as an Innovation Hub 2019 was another year of growth for the retailing industry in Asia Pacific. What set the region apart from other markets was the proliferation of new types of brick-and-mortar and e-commerce retailing formats and new brands experimenting with various innovations in order to win the local young, and increasingly tech-savvy, population. The rapid uptake of social media in Asia Pacific, thanks to consumer segments such as millennials and Generation Z, has been a major factor in the rise of social commerce. The Asia Pacific region offers businesses great growth opportunities and profitability, due to its large working-age population, a critical mass of highly-educated people, an expanding middle class and modernisation efforts, all of which are boosting consumer expenditure and increasing demand for online retailing and e-commerce. Demographic dividend and fast-paced digital connectivity are key differentiators allowing the region to surpass other countries by paving the way for more innovative accessible services, customised products and experiences as well as creating unique digital marketplaces in the region. -

List of Payment Centers (As of January 2016)

List of Payment Centers (as of January 2016) BRANCH NAME LOCATION NAME LOCATION ADDRESS CUBAO DEPARTMENT STORE SM Cubao Bldg., Araneta Center, Socorro Cubao, Quezon City SAVEMORE NEPA Q. MART SAVEMORE NEPA Q. MART Savemore Market Nepa Q-Mart, G/F & 2F 770 St., Rose Bldg. Edsa cor K-G St. West Kamias, Q.C. SAVEMORE P. TUAZON SAVEMORE P. TUAZON Savemore Market P. Tuazon A.D. Legaspi St.,cor P. Tuazon Blvd., Marilag,Proj 4, Q.C. 1109 SAVEMORE ARANETA SAVEMORE ARANETA Savemore Market COD Cubao Gen Romulo St., Araneta Center Cubao Quezon City SAVEMORE ANONAS SAVEMORE ANONAS Savemore Market Anonas, Maamo St. Road, Lot 30 V. Luna and Anonas Extn. Sikatuna, Q.C. 1101 HYPERMARKET CUBAO HYPERMARKET CUBAO SM Hypermarket Cubao, Main Ave cor EDSA, Quezon QUIAPO DEPARTMENT STORE SM Quiapo , MDC Bldg., C. Palanca St., Quiapo, Manila SAVEMORE STA. CRUZ SAVEMORE STA. CRUZ Savemore Market Sta Cruz 665 Rizal Avenue, Jennet & Lord Theater, Sta Cruz, Manila MAKATI DEPARTMENT STORE SM Makati Building Ayala Center, Brgy. San Lorenzo Village, Makati City SAVEMORE PASONG TAMO SAVEMORE PASONG TAMO Savemore-Market Pasong Tamo, 2256 Chino Roces Ave.,Ext EDSA, Brgy. Magallanes, Makati City 1231 SAVEMORE MARKET PLACE SAVEMORE MARKET PLACE SM Marketplace A Venue Hall, Antel Lifestyle City, 7829, Makati Avenue, Poblacion, Makati City HYPERMARKET JAZZ HYPERMARKET JAZZ SM Hypermarket Jazz Nicanor Garcia corner Jupiter Street, Brgy Bel Air, Makati City SAVEMORE LIGHT RESIDENCES SAVEMORE LIGHT RESIDENCES Savemore Market Light Residences Edsa Cor. Madison St. Brgy. Barranca, Mandaluyong City HARRISON DEPARTMENT STORE SM Harrison Plaza Complex, Malate, Manila 1004 HYPERMARKET ADRIATICO DEPARTMENT STORE SM Hypermart Adriatico M.H. -

2015 SMPHI Annual Report

SUSTAINING GROWTH, DELIVERING VALUE 10th Floor, OneE-com Center Harbor Drive, Mall of Asia Complex Pasay City 1300, Philippines Email: [email protected] www.sminvestments.com 2 IFC Our Business Philosophy 2 Business Highlights & Impact 6 Financial Highlights 7 Shareholder Value SM INVESTMENTS CORPORATION SM INVESTMENTS OUR BUSINESS PHILOSOPHY 8 Ten-Year Performance Overview 10 Our Business Footprint 12 Message to Shareholders SM Investments Corporation is the Philippines’ largest 14 President’s Report publicly-listed holding company that holds a group of sustainable businesses in retail, property and financial services. The Group thrives on leadership, innovation 18 RETAIL OPERATIONS and highly synergistic operations. • THE SM STORE Our Vision is to build world-class businesses that are • SM Markets catalysts for development in the communities we serve. Our long history of sustained growth is an indication of our ability to deliver value for all our stakeholders through sound financial management, leadership, innovation, long-term sustainability efforts and a comprehensive development program for all our host communities. Through our interests and activities, Our Mission is to strive to be a good corporate citizen by partnering with our host communities in providing consistently high standards of service to our customers, look after the welfare of our employees, and deliver sustainable returns to our shareholders at all times, upholding the highest standards of corporate governance in all our businesses. 28 PROPERTY Over the years, we have been committed to sustaining • Malls our growth, in creating value and delivering quality • Residences products and services that our millions of customers aspire for. We are here to serve. -

List of Participating Branches in Mindanao for Balance Transfer As of August 2018

List of Participating Branches in Mindanao for Balance Transfer As of August 2018 Branch Area Branch Name Address Code Davao Davao - Agdao 324 Lapu-lapu St., 8000 Agdao, Davao City Davao Davao - Bangoy 325 R. Magsaysay Avenue corner C. Bangoy St., 8000 Davao City KSS Bldg., Buhangin Road cor. Olive St., Brgy. Buhangin, Davao Davao Davao – Buhangin 1141 City Davao – Buhangin C.P. Garcia Davao 279 Carlos P. Garcia Highway, Buhangin Diversion Road, Davao City Highway WTKC Realty Bldg., Davao-Bukidnon National Highway, Brgy. Davao Davao - Calinan 1099 Calinan, Davao City Davao Davao - Claveria 715 BDO Building No. 30 C.M. Recto Ave., Poblacion, Davao City Davao Davao - C.M. Recto 270 383 Claro M. Recto St., Davao City Davao Davao - Felcris Centrale 1025 Felcris Centrale, Quimpo Boulevard, Brgy. Bucana, Davao City SJRDC Bldg., Insular Village 1 Commercial Area, Lanang, Davao Davao Davao - Lanang Insular Village 244 City Ramon Magsaysay Avenue corner Lizada St., 8000 Davao City, Davao Davao - Lizada 375 Davao del Sur Davao Davao - Mati 373 Rizal corner Mabini St., 8200 Mati, Davao Oriental Davao Davao - Monteverde 187 G/F Sequoia Inn, Monteverde Avenue, Davao City Davao Davao - Narra 676 Tomas Monteverde Avenue corner Narra St., Davao City Davao Davao - Panabo 1023 National Highway, Brgy. Sto. Niño, Panabo City, Davao del Norte Davao Davao - Quirino Avenue 326 Nicolas I Bldg., Quirino Avenue, 8000 Davao City Davao Davao - Rizal 194 Caritas Bldg. Rizal St. corner Pelayo St. Davao City Davao Davao - Sta. Ana 337 Monteverde corner F. Bangoy St., 8000 Davao City, Davao del Sur Davao Davao - Sta. Ana Gempesaw 837 Sta. -

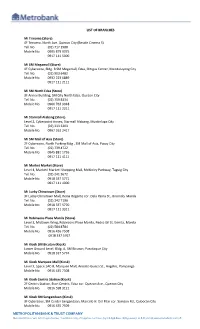

Metropolitan Bank & Trust Company List

LIST OF BRANCHES Mi Trinoma (Store) 4F Trinoma, North Ave. Quezon City (Beside Cinema 5) Tel. No. (02) 717 1980 Mobile No. 0995 879 9075 0917 111 5000 Mi SM Megamall (Store) 4F Cyberzone, Bldg. B SM Megamall, Edsa, Ortigas Center, Mandaluyong City Tel. No. (02) 903 6482 Mobile No. 0932 223 6889 0917 111 2111 Mi SM North Edsa (Store) 3F Annex Building, SM City North Edsa, Quezon City Tel. No. (02) 759 8334 Mobile No. 0966 763 9048 0917 111 2211 Mi Starmall Alabang (Store) Level 2, Cyberpoint Annex, Starmall Alabang, Muntinlupa City Tel. No. (02) 333 3203 Mobile No. 0967 262 2417 Mi SM Mall of Asia (Store) 2F Cyberzone, North Parking Bldg., SM Mall of Asia, Pasay City Tel. No. (02) 739 4722 Mobile No. 0945 881 1726 0917 111 4111 Mi Market Market (Store) Level 4, Market! Market! Shopping Mall, McKinley Parkway, Taguig City Tel. No. (02) 241 3672 Mobile No. 0918 337 5771 0917 111 4000 Mi Lucky Chinatown (Store) 3F Lucky Chinatown Mall, Reina Regente cor. Dela Reina St., Binondo, Manila Tel. No. (02) 242 7190 Mobile No. 0918 337 5770 0917 111 3311 Mi Robinsons Place Manila (Store) Level 3, Midtown Wing, Robinsons Place Manila, Pedro Gil St. Ermita, Manila Tel. No. (02) 584 8784 Mobile No. 0916 436 7508 0918 337 5767 Mi Kiosk SM Bicutan (Kiosk) Lower Ground Level, Bldg. A, SM Bicutan, Parañaque City Mobile No. 0918 337 5774 Mi Kiosk Marquee Mall (Kiosk) Level 3, Space 1AC-8, Marquee Mall, Aniceto Gueco St., Angeles, Pampanga Mobile No. 0916 435 7508 Mi Kiosk Centris Station (Kiosk) 2F Centris Station, Eton Centris, Edsa cor. -

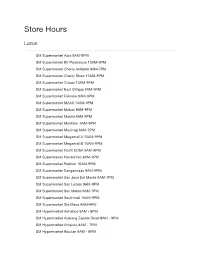

SM MARKETS STORE HOURS Aug 2021

Store Hours Luzon _____________________________________________________________________________________ SM Supermarket Aura 9AM-9PM SM Supermarket BF Paranaque 10AM-9PM SM Supermarket Cherry Antipolo 9AM-7PM SM Supermarket Cherry Shaw 10AM-9PM SM Supermarket Cubao 10AM-9PM SM Supermarket East Ortigas 9AM-9PM SM Supermarket Fairview 9AM-9PM SM Supermarket MAAX 10AM-9PM SM Supermarket Makati 9AM-9PM SM Supermarket Manila 9AM-9PM SM Supermarket Marikina 9AM-9PM SM Supermarket Masinag 9AM-7PM SM Supermarket Megamall A 10AM-9PM SM Supermarket Megamall B 10AM-9PM SM Supermarket North EDSA 9AM-9PM SM Supermarket Novaliches 8AM-9PM SM Supermarket Podium 10AM-9PM SM Supermarket Sangandaan 9AM-9PM SM Supermarket San Jose Del Monte 9AM-7PM SM Supermarket San Lazaro 9AM-9PM SM Supermarket San Mateo 9AM-7PM SM Supermarket Southmall 10AM-9PM SM Supermarket Sta Mesa 9AM-9PM SM Hypermarket Adriatico 8AM - 8PM SM Hypermarket Alabang Zapote Road 8AM - 9PM SM Hypermarket Antipolo 8AM - 7PM SM Hypermarket Bicutan 9AM - 9PM SM Hypermarket Cainta 8AM - 7PM SM Hypermarket Cherry Congressional 9AM - 9PM SM Hypermarket Cubao 8AM - 9PM SM Hypermarket Deca Mall 8AM - 8PM SM Hypermarket Eton Centris 10AM - 8PM SM Hypermarket Fairview 9AM - 9PM SM Hypermarket FTI, Taguig 8AM - 8PM SM Hypermarket Jazz Residences 9AM - 9PM SM Hypermarket Las Piñas 9AM - 9PM SM Hypermarket Makati 8AM - 9PM SM Hypermarket Mall of Asia 9AM - 9PM SM Hypermarket Mandaluyong 8AM - 9PM SM Hypermarket Monumento 8AM - 9PM SM Hypermarket Muntinlupa 9AM - 9PM SM Hypermarket North Edsa 9AM - 9PM SM Hypermarket Novaliches 8AM - 9PM SM Hypermarket Pasig 9AM - 9PM SM Hypermarket Sucat 9AM - 9PM SM Hypermarket Sucat Lopez 9AM - 9PM SM Hypermarket Sun Residences 10AM - 9PM SM Hypermarket Taytay 9AM - 7PM SM Hypermarket The Village Square Alabang 8AM - 8PM SM Hypermarket Valenzuela 10AM - 9PM Free Choice Mart (7AM - 9PM) SavemoreAmang Rodriguez (7AM - 9PM ) Savemore Market Anonas (7AM - 9PM) Savemore Market Acacia (7AM - 9PM) Marketplace A. -

MEMO EXPRESS.Pdf

MERCHANT BRANCHES MEMO EXPRESS SM SOUTHMALL ALABANG ZAPOTE RD ALMANZA UNO LAS PINAS CITY 1740 MEMO EXPRESS CYBERZONE SM CITY FAIRVIEW REGALADO AVE. GREATER LAGRO QUEZON CITY 1100 MEMO EXPRESS UNIT CZ24 SM CITY BF D.A.S.A COR PRES AVE BRGY BF HOMES PARANAQUE CITY 1700 MEMO EXPRESS 345 ALABANG ZAPOTE RD ROBINSON PLACE LAS PINAS BRGY TALON LAS PINAS CITY 1740 MEMO EXPRESS UNIT 303 2F ARCADIA BLDG SANTA ROSA TAGAYTAY ROAD DON JOSE STA. ROSA CITY LAGUNA 4026 MEMO EXPRESS CZ234 SM CITY BACOLOD RECLAMATION ARE BACOLOD CITY 6100 MEMO EXPRESS SM CENTER ANGONO MANILA EAST ROAD SAN ISIDRO ANGONO RIZAL 1930 MEMO EXPRESS SM MEGA CENTER MELENCIO SAN ROQUE CABANATUAN CITY NUEVA ECIJA 3100 MEMO EXPRESS CY 20 SM CITY GENSAN CORNER SANTIAGO BLVD SAN MIGUEL ST. LAGAO GEN SANTOS CITY 9500 MEMO EXPRESS SPACE 3-052 3F NEW GLORIETTA 2 AYALA CENTER SAN LORENZO MAKATI CITY 1224 MEMO EXPRESS L3-341 ROBINSONS NORTH ABUCAY BRGY 91 TACLOBAN CITY 6500 MEMO EXPRESS L2 2019 ROBINSON PLACE ORMOC CHRYSANTHEMUM SUBD. COGON ORMOC CITY 6541 MEMO EXPRESS CZ 3008 17 SM CITY LEGAZPI TAHAO ROAD LEGAZPI CITY ALBAY 4500 MEMO EXPRESS RM 814 PACIFIC LAND CTR BLDG QUITIN PAREDES ST. BRGY 289 ZONE 027 DIST 111 BINONDO MANILA 1006 MEMO EXPRESS SPACE 3111 ABREEZA MALL JP LAUREL AVE DAVAO CITY 8000 MEMO EXPRESS THE DISTRICT MALL AGUINALDO HIWAY COR. DAANG HARI ROAD ANABU II D CITY OF IMUS CAVITE 4103 MEMO EXPRESS L3 ROBINSON PLACE SANTIAGO MABINI SANTIAGO CITY 3311 MEMO EXPRESS 239 SM CITY CAUAYAN MAHARLIKA HIGHWAY DISTRICT 2 CAUAYAN CITY ISABELA 3305 MEMO EXPRESS CENTRIO MALL CM RECTO AVENUE BRGY 24 CAGAYAN DE ORO CITY 9000 MEMO EXPRESS L3-338 ROBINSON PLACE MALOLOS SUMAPANG MATANDA CITY MALOLOS BULACAN 3300 MEMO EXPRESS 3RD LEVEL SPACE 3029A FAIRVIEW TERRACES QUIRINO HIGHWAY PASONG PUTIK QUEZON CITY 1012 MEMO EXPRESS SPACE 2 02448 ROBINSON PLACE PUEBLO DE PANAY LAWAAN ROXAS CITY 5800 MEMO EXPRESS CZ 015 25 SM CITY SAN JOSE DEL MONTE BRGY TUNGKONG MANGGA CITY OF SAN JOSE DEL MONTE BULACAN 3023 MEMO EXPRESS UNIT 326 3RD FLR AYALA MALLS LEGAZPI RIZAL ST. -

Midas Investments Research Retail Industry This Report Is Published for Educational Purposes Only by Students Competing in the CFA Institute Research Challenge

s Services Sector Midas Investments Research Retail Industry This report is published for educational purposes only by students competing in the CFA Institute Research Challenge. Puregold Price Club, Inc. 29 November 2012 Ticker: PGOLD Recommendation: BUY Price: PHP 32.20 (USD 0.79) Price Target: PHP 40.16 (USD 1.00) Exchange Rate Pure consumer play outpacing market on defensive USD/PHP: 40.88 growth Figure 1: Share Price Performance We recommend a BUY for PGOLD, the Philippines‟ fastest growing grocery retailer and the only pure, direct and broad-based domestic consumer play in the market, at a price 35 target of Php 40.16, a 24.72% upside from current price of P32.20. Our positive outlook is 30 based on growing and resilient domestic consumption that is captured by an EDLP (Every 25 Day Low Prices) Strategy targeting low to middle-income consumers bringing in traffic of 20 18 million each week. Through the Tindahan ni Aling Puring (TNAP) reseller program, it 15 is the only major retailer to focus on the widely popular traditional sari-sari store. By 10 acquiring membership shopping club S&R, it also captures a growing niche of high-income 5 consumer spending. With aggressive store expansion underway, we forecast sustainable long-term growth for this defensive stock. 0 Focus on domestic consumption driving resilient earnings against volatile global financial system: As the only pure direct and broad-based domestic consumer play on 5-Jul-12 5-Jan-12 5-Jun-12 5-Oct-11 5-Oct-12 5-Feb-12 5-Sep-12 5-Apr-12 5-Dec-11 5-Mar-12 5-Nov-11 5-Aug-12 5-Nov-12 5-May-12 the local market, PGOLD‟s stock price has outpaced the Philippine stock market by PGOLD PSEi (rebased) MSCI (rebased) 77.2% (see Figure 1) driven by revenue growth of 39.69% (2012E) on the back of 16% growth in domestic consumption. -

Banking-Sched-Dec-30-2019.Pdf

BANKING SCHEDULES FOR THE HOLIDAY SEASON Banking Schedule of Selected Branches December 30,2019 Selected Regular Branches A. Regular Opening Hours Up to 3:00 PM LUZON Abra - Bangued Albay - Daraga Albay - Tabaco Angeles - Balibago Angeles - Miranda Antipolo - Circumferential Rd. Aurora Blvd. - Broadway Centrum Baguio - Bokawkan Road Baguio - Harrison Road Baguio - Kennon Road Baguio - Legarda Baguio - Leonard Wood Road Baguio - Luneta Baguio - Marcos Highway Balsigan Baguio - Marcos Highway Centerpoint Baguio - Session Road Balanga - Capitol Drive Baliwag - JP Rizal Balubaran - MacArthur Highway Batangas - Balayan Batangas - Bauan Batangas - Diego Silang Batangas - Gulod Batangas - Nasugbu Batangas City - Rizal Avenue Benguet - La Trinidad Bocaue - MacArthur Highway Bulacan - Bocaue Bulacan - Hagonoy Bulacan - Obando Bulacan - Primark Plaridel Bulacan - San Jose Del Monte Bulacan - San Miguel Bulacan - San Rafael Bulacan - Sapang Palay Bulacan Sta. Maria - Bagbaguin Bulacan Sta. Maria - M.G. de Leon Cagayan - Aparri Caloocan - Primark Deparo Carmen Planas Cavite - Congressional Road Cavite - Dasmariñas Salawag Cavite - Gen Trias San Francisco Cavite - Imus Aguinaldo Highway Cavite - Naic Cavite - P. Burgos Cavite - Silang Aguinaldo Highway Cavite - Trece Martires Cavite Imus - The District Clark - Philexcel Business Park Dagupan - Tapuac Eastwood City - IBM Plaza Echague EDSA - East Caloocan Ilocos Norte - Batac Ilocos Sur - Cabugao Ilocos Sur - Candon Ilocos Sur - Narvacan Iriga City Isabela - Ilagan Isabela - Primark Cordon Isabela - -

Download Rate 82 Sessions Conducted 526 Childcare Leaves Credited 81% Access Rate 42% Activated Accounts Vs

Integrated Report 2020 1 Our Story Inspiring Resilience Integrated Report 2020 2 Integrated Report 2020 Our Story About this Report (102-46, 102-47, 102-49, 102-50, 102-51, 102-54) SM Prime Holdings, Inc. presents the first annual Integrated Report and the ninth edition following the Global Reporting Initiative (GRI) Framework. This Integrated Report features the International Integrated Reporting Council (IIRC) framework that uses the economic, environment, social and governance pillars of sustainability in combination with the six capitals: Financial, Manufactured, Intellectual, Environment, Human and Social and Relationship. The financial and non-financial information contained herein covers reporting from January to December 2020 and discusses SM Prime’s assets where the business has an organizational boundary. The report shares the performance and consolidated data of its malls, residences, leisure resorts, offices, hotels and convention centers. This report has been prepared in accordance with the GRI Standards: Core Option and the Task Force on Climate-related Financial Disclosures alongside multiple internationally recognized frameworks such as the UN Sustainable Development Goals, UN Global Compact and the Sendai Framework for Disaster Risk Reduction (2015-2030). This report is entitled Inspiring Resilience to describe the year in terms of the Company’s strength, dedication and response to Cover Photo: any challenge. SM Mall of Asia’s iconic globe reflects a public health and safety message in line with #SafeMallingatSM. The online version of the 2020 SM Prime Integrated Report is Next Page: available at the SM Prime website (www.smprime.com). Part of the Bike-Friendly SM program, commuters ply the new bike lane at the Feedback on the report may be sent to [email protected]. -

List of Accredited Clinic

LIST OF ACCREDITED CLINIC LUZON ADVANCED LAB SOLUTIONS BY HI- PRECISION DIAGNOSTICS NATIONAL CAPITAL REGION (NCR) 9th Floor Centuria Medical Makati, Kalayaan Ave., Cor Salamanca St., Brgy. Poblacion, Makati City CALOOCAN CITY Tel no.: (02)7938611 THE MEDICAL CITY CLINIC – VICTORY ASSOCIATED MEDICAL SERVICES MALL 3/F, Kalayaan Building, cor. Salcedo & Dela Rosa 3F Victory Mall, Rizal Ave, Monumento, Caloocan Sts., Legaspi Village, Makati Tel no.: (02) 351.4978, 351.4987 Tel no.: (02) 892.5906 Mon-Sun 8am-8pm Fax no.:(02) 892.5906 Mon - Fri 8:00am-4:00pm Sat 8:00am-11:30am THE PERLAS POLYCLINIC AND SPECIALIST CENTER AVENTUS MEDICAL CARE INC – MAKATI 171 4th Ave. cor Roxas St. Grace park 2nd & 4th Floor Beneficial PNB Life Bldg 166 Tel no.: (02) 364.8731, 442.3295 Salcedo St, Legaspi Village Fax no.: (02) 367.3895 Tel no.: (02) 817.1464 Mon – Sat 8:00am – 5:00pm Fax no.: (02) 817.2715 Mon – Sat 8:00am – 5:00pm LAS PINAS FORTMED MEDICAL CLINICS MAKATI, INC 3rd/ F Crown Center, 158 Jupiter cor N. Garcia Sts. ALABANG MEDICAL CLINIC – ALMANZA Tel no.: (02) 897-1111 to 19 2/ F Susana Arcade # 476 Real St. Almanza, Las Fax no.: (02) 890.9957 Piñas City Mon – Sat 8:00am – 6:00pm Tel no.:(02) 801.4535, (02) 800.3840 Fax no.: (02) 800.3831 GREPALIFE MEDICAL AND DIAGNOSTIC CENTER ALABANG MEDICAL CLINIC - TALON Mezzanine Floor, Tower 2 RCBC Plaza 6819 Ayala Alabang- Zapote Road, cor. Mendoza St., Pelayo Ave. Village, Talon, Las Piñas City Tel no.: (02) 886 6586, (02) 843.5063 Tel no.: (02) 873.6464, (02) 874.0164 Fax no.: (02) 886.6587 (02) 874.2506 Mon – Sat 7:30am – 5:00pm Fax no.: (02) 873.1288 HEALTHLAB, INC CASA MEDICA - SOUTHMALL Unit 802 and 1601 Medical Plaza, Amorsolo, Makati G/F SM Southmall, Casa Medica Incorporated, City Alabang-Zapote Road, Zapote Tel no.: (02) 867.1140 (02) 817.8606 Tel: (02) 806.7851,(02) 806.7855;(02) 806.6863 Fax no.: (02) 867.1141 Mon – Sun 10:00am – 7:00pm HEALTH PROTECT MEDICAL CLINIC HI-PRECISION DIAGNOSTIC CENTER – LAS SYSTEM PIÑAS Dela Rosa cor Amorsolo St. -

Tion Doing Business with Academy

tion Doing Business with Academy January 2019 All information contained in this publication is proprietary. No reproduction, distribution or use of the material is permitted without the express permission of Academy Sports + Outdoors. © 2019 Academy, Ltd. All rights reserved. Private and Confidential - Do Not Distribute 1 Table Of Contents Product Safety & Compliance………………………………………….……………………………………………..……….…….45 Supplier Onboarding Guide Federal Regulations……………………………………………………………………………………..…….50 State Regulations………………………………………………………………………………………….……..51 About Academy Sports + Outdoors 3 Product Recall/Corrective Actions…………………………….…………………………....52 Brand Management and Packaging……………………………………………………………………..…………………….4 Legal……………………………………………………………………………………..………………………………………………………………………….57 FCPA……………………………………………………………………………………………………………………………...59 Vendor Management………………………………………………………………………………………………….………………………..6 Ethics and Code of Conduct Policy & New Supplier Set-up……………………………………………..………......................................7 Vendor Code of Conduct…………………………..………………………………………..……….. 70 EDI…………………………………………………………………………………………………………………….……….…...8 Quality Assurance 75 Risk Management………………………………………………………………….……………………………………………….………………9 Product Testing…………………………………………………………………….……………………………….77 PLI…………………………………………………………………………………….…………………………………………….10 Business Rules…..........................................................................................................83 Inspections……………………………………………………………………………………………………………….92 Factory Compliance……………………………………………………………………………………………………………….……………..15