Financial Statements Investor Information

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Description Iresscode Exchange Current Margin New Margin 3I

Description IRESSCode Exchange Current Margin New Margin 3I INFRASTRUCTURE PLC 3IN LSE 20 20 888 HOLDINGS PLC 888 LSE 20 20 ASSOCIATED BRITISH ABF LSE 10 10 ADMIRAL GROUP PLC ADM LSE 10 10 AGGREKO PLC AGK LSE 20 20 ASHTEAD GROUP PLC AHT LSE 10 10 ANTOFAGASTA PLC ANTO LSE 15 10 ASOS PLC ASC LSE 20 20 ASHMORE GROUP PLC ASHM LSE 20 20 ABERFORTH SMALLER COM ASL LSE 20 20 AVEVA GROUP PLC AVV LSE 20 20 AVIVA PLC AV LSE 10 10 ASTRAZENECA PLC AZN LSE 10 10 BABCOCK INTERNATIONAL BAB LSE 20 20 BARR PLC BAG LSE 25 20 BARCLAYS PLC BARC LSE 10 10 BRITISH AMERICAN TOBA BATS LSE 10 10 BAE SYSTEMS PLC BA LSE 10 10 BALFOUR BEATTY PLC BBY LSE 20 20 BARRATT DEVELOPMENTS BDEV LSE 10 10 BARING EMERGING EUROP BEE LSE 50 100 BEAZLEY PLC BEZ LSE 20 20 BH GLOBAL LIMITED BHGG LSE 30 100 BOWLEVEN PLC BLVN LSE 60 50 BANKERS INVESTMENT BNKR LSE 20 20 BUNZL PLC BNZL LSE 10 10 BODYCOTE PLC BOY LSE 20 20 BP PLC BP LSE 10 10 BURBERRY GROUP PLC BRBY LSE 10 10 BLACKROCK WORLD MININ BRWM LSE 20 65 BT GROUP PLC BT-A LSE 10 10 BRITVIC PLC BVIC LSE 20 20 BOVIS HOMES GROUP PLC BVS LSE 20 20 BROWN GROUP PLC BWNG LSE 25 20 BELLWAY PLC BWY LSE 20 20 BIG YELLOW GROUP PLC BYG LSE 20 20 CENTRAL ASIA METALS PLC CAML LSE 40 30 CLOSE BROTHERS GROUP CBG LSE 20 20 CARNIVAL PLC CCL LSE 10 10 CENTAMIN PLC CEY LSE 20 20 CHARIOT OIL & GAS LTD CHAR LSE 100 100 CHEMRING GROUP PLC CHG LSE 25 20 CONYGAR INVESTMENT CIC LSE 50 40 CALEDONIA INVESTMENTS CLDN LSE 25 20 CARILLION PLC CLLN LSE 100 100 COMMUNISIS PLC CMS LSE 50 100 CENTRICA PLC CNA LSE 10 10 CAIRN ENERGY PLC CNE LSE 30 30 COBHAM PLC -

The Art of Investing in Smaller Companies – P 30

www.whatinvestment.co.ukWhat FOR Investment A WEALTHIER FUTURE Issue 424 July 2018 £4.50 The art of investing in smaller companies – P 30 Emerging Profit from Wine Markets How looking beyond the China and India are catching blockbuster vintages can the US, but are they worth deliver corking returns investing in? – Page 36 – Page 50 WI.JULY.2018.Cover.indd 1 21/06/2018 16:07 NEED INVESTMENT GUIDANCE? Why not join thousands of investors and benefi t from all our independent analysis and insight? Subscribe www.whatinvestment.co.ukWhat FOR Investment A WEALTHIER FUTURE Issue 423 June 2018 £4.50 and get Britain’s Buffetts issues How can you profit 12 from the UK managers inspired by the legendary American investor for the price – P 14 of 10 > Unit Trusts 1 | >| The Last Word | Peter Elston behaviour of, say, numbers or Hubris is the greatest challenge planets or elementary particles or rocks or plants or people. Our new columnist argues that being a non- Successful investing, on the other conformist and not following the crowd can be hand, necessitates disagreement. The Aging bull The Empire Trust For me to give myself a chance uncomfortable but can also produce good returns of beating my competitors, and thus the market, the last thing I should do is agree with them. I The bull market might be The British Empire Trust I am not exactly sure how I have one was just lucky. Probably seek out where they are huddled ended up as a chief investment best to assume you were lucky. -

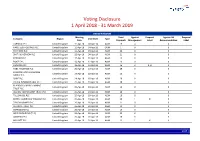

Global Voting Activity Report to March 2019

Voting Disclosure 1 April 2018 - 31 March 2019 UNITED KINGDOM Meeting Total Against Proposal Against ISS Proposal Company Region Vote Date Type Date Proposals Management Label Recommendation Label CARNIVAL PLC United Kingdom 11-Apr-18 04-Apr-18 AGM 19 0 0 HANSTEEN HOLDINGS PLC United Kingdom 11-Apr-18 04-Apr-18 OGM 1 0 0 RIO TINTO PLC United Kingdom 11-Apr-18 04-Apr-18 AGM 22 0 0 SMITH & NEPHEW PLC United Kingdom 12-Apr-18 04-Apr-18 AGM 21 0 0 PORVAIR PLC United Kingdom 17-Apr-18 10-Apr-18 AGM 15 0 0 BUNZL PLC United Kingdom 18-Apr-18 12-Apr-18 AGM 19 0 0 HUNTING PLC United Kingdom 18-Apr-18 12-Apr-18 AGM 16 2 3, 8 0 HSBC HOLDINGS PLC United Kingdom 20-Apr-18 13-Apr-18 AGM 29 0 0 LONDON STOCK EXCHANGE United Kingdom 24-Apr-18 18-Apr-18 AGM 26 0 0 GROUP PLC SHIRE PLC United Kingdom 24-Apr-18 18-Apr-18 AGM 20 0 0 CRODA INTERNATIONAL PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 18 0 0 BLACKROCK WORLD MINING United Kingdom 25-Apr-18 19-Apr-18 AGM 15 0 0 TRUST PLC ALLIANZ TECHNOLOGY TRUST PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 10 0 0 TULLOW OIL PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 16 0 0 BRITISH AMERICAN TOBACCO PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 20 1 8 0 TAYLOR WIMPEY PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 21 0 0 ALLIANCE TRUST PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 13 0 0 SCHRODERS PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 19 0 0 WEIR GROUP PLC (THE) United Kingdom 26-Apr-18 20-Apr-18 AGM 23 0 0 AGGREKO PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 20 0 0 MEGGITT PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 22 1 4 0 1/47 -

FTSE Factsheet

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Axiom European Financial Debt Fund AXI Closed End Investments — GBP 0.975 at close 20 April 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 21-Apr-2015 1D WTD MTD YTD Absolute - - - - Rel.Sector - - - - Rel.Market - - - - VALUATION Data unavailable Trailing PE 52.7 EV/EBITDA 25.0 PB 1.0 PCF 24.7 Div Yield 6.6 Price/Sales +ve Net Debt/Equity 0.0 Div Payout +ve ROE 1.8 DESCRIPTION Data unavailable The Company is a closed-ended investment company registered and incorporated in Guernsey and managed by Axiom Alternative Investments SARL. Past performance is no guarantee of future results. Please see the final page for important legal disclosures. 1 of 4 FTSE COMPANY REPORT: Axiom European Financial Debt Fund 20 April 2021 Valuation Metrics Price to Earnings (PE) EV to EBITDA Price to Book (PB) 31-Mar-2021 31-Mar-2021 31-Mar-2021 60 25 1.15 1.1 50 +1SD 20 1.05 40 1 15 0.95 Avg 30 0.9 10 +1SD 20 +1SD 0.85 -1SD 5 Avg 0.8 10 Avg 0.75 0 ‖ ‖ 0 ‖ ‖ -1SD 0.7 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Murray International Trust (Ord) 120.0 Murray International Trust (Ord) 100.0 CVC Credit Partners European Opportunities (GBP) 2.3 European Opportunities Trust 120.0 European Opportunities Trust 100.0 Hipgnosis Songs Fund 2.2 Law Debenture Corp 120.0 Law Debenture Corp 100.0 Pacific Horizon Investment Trust 2.0 HICL Infrastructure -

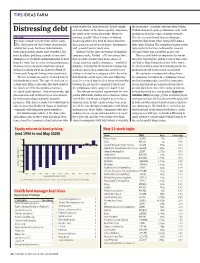

Distressing Debt Seek out Shares in the Lowest Quality Companies; Verdad Compared Equity Performance with Credit the Worst-Of-The-Worst, If You Like

TIPS IDEAS FARM want to play the ‘dash for trash’ should simply the issue price. A similar story was found when Distressing debt seek out shares in the lowest quality companies; Verdad compared equity performance with credit the worst-of-the-worst, if you like. However, quality based on the scores of rating agencies. ALGY HALL ignoring ‘quality’ when it comes to buying Here the research found share performance t’s been a tough time for short sellers lately. beaten-up stocks (the kind of shares found on started to deteriorate when ratings fell below a IThe ‘dash for trash’ that I wrote about in this these pages in our tables of shorts, downgrades high single B rating. The annualised equity return column last week, has been indiscriminate. and 52-week lows) is rarely wise. from stocks in the least creditworthy category Even real no-hoper shares have benefited. The Intrigued by the price movement of bankrupt- (CC and below) was a negative 34 per cent. most headline-grabbing example of investors’ company stocks, Verdad – a US investment firm This research holds an important lesson for willingness to overlook all fundamentals in their that specialises in investing in the shares of investors targeting the grubbier end of this recov- hunt for ‘trash’ has been the strong performance cheap, indebted, smaller companies – trawled its ery. Rather than buying the worst-of-the-worst, of shares in US companies that have already database. It looked for the long-term relationship it’s the best-of-the-worst that should provide the declared bankruptcy or are about to (Hertz, JC between share price performance and the level optimal trade-off between risk and reward. -

UK Investment Trusts Index This Listing Aims to Help Readers to Locate an Investment Trust in the AIC Sectors

UK Investment Trusts Index This listing aims to help readers to locate an investment trust in the AIC sectors. Funds are presented in alphabetical order by provider. Fund name Sector Fund name Sector Fund name Sector 3i Group Plc Private Equity Blackstone/GSO Loan Financing Limited Debt - Structured Finance Energiser Investments PLC Unclassified 3I Infrastructure Plc Infrastructure Blue Planet Investment Trust PLC ORD 1P Global High Income EP Global Opportunities Trust PLC Global Aberdeen Asian Income LTd Asia Pacific Income Blue Star Capital PLC Unclassified EPE Special Opportunities Unclassified Ab Div Inc & Grw Trt Flexible Investment Bluefield Solar Income Limited Renewable Energy Infrastructure European Assets Trust PLC European Smaller Companies AbrEmrMrInvCmpLtd Global Emerging Markets BMO Cap & Inc IT PLC UK Equity Income F&C Investment Trust Plc Global Abr Frn Mr Inv CmpLtd Global Emerging Markets BMO Commercial Property Trust Limited Property - UK Commercial F&C UK Real Estate Investments Limited Property - UK Commercial Aberdeen Japan IT PLC Japan BMO Global Smaller Companies Plc Global Smaller Companies Fair Oaks Income Limited 2017 SHS Debt - Structured Finance Aberdeen Latin American Income Ltd Latin America BMO Managed Portfolio Trust Plc Growth Flexible Investment FastForward Innovations Limited Ord 1P Private Equity Abrdn New Dawn IT PLC Asia Pacific BMO Managed Portfolio Trust Plc Inc Flexible Investment Fidelity Asian Values PLC Asia Pacific Aberdeen New Ind IT PLC Ord Country Specialist: Asia Pacific ex Jap BMO Private -

FTSE Russell Publications

2 FTSE Russell Publications 19 August 2021 FTSE 250 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Infrastructure 0.43 UNITED Bytes Technology Group 0.23 UNITED Edinburgh Investment Trust 0.25 UNITED KINGDOM KINGDOM KINGDOM 4imprint Group 0.18 UNITED C&C Group 0.23 UNITED Edinburgh Worldwide Inv Tst 0.35 UNITED KINGDOM KINGDOM KINGDOM 888 Holdings 0.25 UNITED Cairn Energy 0.17 UNITED Electrocomponents 1.18 UNITED KINGDOM KINGDOM KINGDOM Aberforth Smaller Companies Tst 0.33 UNITED Caledonia Investments 0.25 UNITED Elementis 0.21 UNITED KINGDOM KINGDOM KINGDOM Aggreko 0.51 UNITED Capita 0.15 UNITED Energean 0.21 UNITED KINGDOM KINGDOM KINGDOM Airtel Africa 0.19 UNITED Capital & Counties Properties 0.29 UNITED Essentra 0.23 UNITED KINGDOM KINGDOM KINGDOM AJ Bell 0.31 UNITED Carnival 0.54 UNITED Euromoney Institutional Investor 0.26 UNITED KINGDOM KINGDOM KINGDOM Alliance Trust 0.77 UNITED Centamin 0.27 UNITED European Opportunities Trust 0.19 UNITED KINGDOM KINGDOM KINGDOM Allianz Technology Trust 0.31 UNITED Centrica 0.74 UNITED F&C Investment Trust 1.1 UNITED KINGDOM KINGDOM KINGDOM AO World 0.18 UNITED Chemring Group 0.2 UNITED FDM Group Holdings 0.21 UNITED KINGDOM KINGDOM KINGDOM Apax Global Alpha 0.17 UNITED Chrysalis Investments 0.33 UNITED Ferrexpo 0.3 UNITED KINGDOM KINGDOM KINGDOM Ascential 0.4 UNITED Cineworld Group 0.19 UNITED Fidelity China Special Situations 0.35 UNITED KINGDOM KINGDOM KINGDOM Ashmore -

The Hard Sell Recent Years Has Been Downwards

TIPS IDEAS FARM the general trajectory of the share price over subsequent build-up in shorts underpinned The hard sell recent years has been downwards. This our confidence in the sell case and encour- emphasises the importance of taking the kind aged us to restate the call. Shorts peaked ALGY HALL of external prompts we monitor in the Ideas at 12.5 per cent in May last year, by which ome stock ideas just keep on giving. While Farm as a reason to undertake further research time the shares were already down to 774p. Sthis is a principle often associated with rather than a call to blindly follow suit. Negative bets fell to 5 per cent a year ago, but buy-and-hold investments, the same can But on this occasion, we think the have been riding high again for much of the apply to popular shorts (bets that a share prospects for Sainsbury may be more akin to past 12 months. The shares hit a 66p low in price will fall). Indeed, over recent weeks, two of the other serial short favourites when March and currently trade at 95p. four of the top five stocks in our most-shorted- they’ve previously experienced short surges: Shorts aside, our view of both Cineworld shares table are names that have flirted with Cineworld and Metro Bank. and Metro Bank when we moved to sell boiled top spots on the list in the past. In the case of cinema chain Cineworld, down to the fact they looked vulnerable to the Of the top five,Cineword (CINE), Metro it was a combination of sharply rising short dreaded combination of an ongoing decline Bank (MTRO), J Sainsbury (SBRY) and interest and broker downgrades that attracted in profit coupled with an overstretched bal- Premier Oil (PMO) all have historical form as our attention to the shares in September ance sheet. -

3I Bioscience, 212 3I European Technology Trust, 205, 212 3I Group, 13, 14, 32, 45, 46, 70, 120, 121, 128, 162, 202, 204, 219, 2

INVESTMENT TRUSTS – A COMPLETE GUIDE Index Aberforth Split Level Income, 42, 97 3 Aberforth Split Level Trust, 202, 209 Absolute Return Trust, 217 3i Bioscience, 212 Abtrust Scotland, 199, 205 3i European Technology Trust, 205, 212 AcenciA Debt Strategies, 213 3i Group, 13, 14, 32, 45, 46, 70, 120, 121, 128, Ackman, Bill, 35 162, 202, 204, 219, 231 Acorn Income Fund, 204, 210, 214, 232 3i Infrastructure, 117, 149, 150, 171, 194, 215, Active Capital Trust, 211 219, 224, 235, 243 Adams, Andy, 41, 196, 207 3i Smaller Quoted Companies Trust, 212 Adamson, Donald, 164 3PC Investment Trust, 207, 210 Advance Developing Markets, 201, 205, 219, 220, 226, 232 A Advance UK, 200, 201, 202, 221 Aberdeen All Asia Investment Trust, 227 AEW Long Lease REIT, 97 Aberdeen Asian Income Fund, 87, 213 AEW UK REIT, 138, 194 Aberdeen Asian Smaller Companies, 225, 230 AIC, 13, 14, 16, 17, 23, 24, 52, 53, 70, 72, 73, Aberdeen Convertible Income, 212 76, 81, 84, 86, 87, 89, 114, 115, 116, 117, Aberdeen Emerging Economies, 208 118, 119, 121, 131, 132, 133, 136, 145, 153, Aberdeen Emerging Markets Company, 91, 155, 156, 191, 192, 194, 214, 215, 216, 217, 240 218, 220, 223, 224, 225, 227, 230, 233, 238, Aberdeen Emerging Markets Smaller 241 Companies Trust, 223 AIM Trust, 204, 207, 209, 210 Aberdeen European, 201, 202 AJ Bell, 76, 144 Aberdeen High Income, 209 Albany Investment Trust, 107, 225 Aberdeen Japan Investment Trust, 57, 177, Alliance Trust, 16, 17, 35, 45, 46, 58, 86, 129, 178, 227, 229, 231 133, 146, 155, 176, 202, 212, 214, 215, 218, Aberdeen Latin American, -

Marten & Co / Quoted Data Word Template

QuotedData Quarterly report | Investment companies April 2019 First Quarter of 2019 All investment companies QuotedData news median discount Through the first quarter of 2019, global equities Time period 01/04/2018 to 31/03/2019 largely clawed back the losses suffered over the final -4.5 -5.0 weeks of 2018. How much longer this ten-year bull -5.5 market can sustain itself is the subject of much -6.0 debate. US interest rate rises have stalled, reflecting -6.5 growing cautiousness. Elsewhere, many of the -7.0 Premium/discount (%) headwinds that ruffled markets late last year, including -7.5 Apr/18 Jul/18 Oct/18 Jan/19 the US/China trade negotiations, continue to lurk in Source: Morningstar, Marten & Co the background. The UK remains in gridlock, with no Discounts are higher than they were this time sign of a resolution to Brexit. last year, reflecting mounting uncertainty. This may pause the longer-term trend towards a tightening of the median discount New research to NAV. Over the quarter, we published notes on Henderson Diversified Global income moves to Income, Premier Global Infrastructure, Geiger Counter, John Laing premium Environmental Assets, Aberdeen Standard European Logistics Income, Montanaro European Smaller Companies, International Time period 01/04/2018 to 31/03/2019 Biotechnology, Civitas Social Housing, Herald Investment Trust, 3 Bluefield Solar Income, JPMorgan Russian Securities and 2 1 BlackRock Throgmorton Trust. You can read all these notes by 0 clicking on the links above or by visiting www.quoteddata.com. -1 -2 In this issue -3 Premium/discount (%) -4 Performance Data – It was notable that China-focused funds had a -5 good quarter while the rebound in technology benefitted Allianz Apr-18 Jul-18 Oct-18 Jan-19 Technology and Edinburgh Worldwide. -

F&C Managed Portfolio Trust

F&C Managed Portfolio Trust Initiation of coverage Diverse exposure with income and growth options Investment trusts 22 March 2017 F&C Managed Portfolio Trust (FMPT), launched in 2008, comprises two listed investment portfolios – an income portfolio (FMPI) and a growth FMPI; FMPG portfolio (FMPG) – this is a differentiated structure for an investment trust. Price 136.0p; 177.0p These portfolios provide investors with a long-term savings vehicle. Both Market cap £57m; £60m portfolios hold at least 25 investments (currently concentrated portfolios of c 40 investment companies); they are benchmarked against the FTSE AUM £59m; £60m All-Share index, however, there are no maximum levels set for underlying NAV* 132.0p; 179.0p exposures to geographic regions or sectors. A unique feature of FMPT is Premium(+)/discount(-) to NAV +3.0%; -1.1% that any net income generated by FMPG is transferred to FMPI in exchange NAV** 132.9p; 179.0p for capital, which benefits the income prospects for FMPI and potential Premium(+)/discount(-) to NAV +2.4%; -1.1% capital growth prospects for FMPG. NAV total returns for both portfolios *Excluding income. **Including income. As at 17 March 2017. have outperformed the benchmark over one, three and five years. Yield 3.9%; 0.0% Ordinary shares in issue 41.6m; 33.7m 12 months FMPI share FMPI NAV FMPG share FMPG NAV FTSE All-Share Code FMPI; FMPG ending price (%) (%) price (%) (%) (%) 28/02/13 18.7 18.4 17.0 17.6 14.1 Primary exchange LSE 28/02/14 13.6 10.3 19.4 17.8 13.3 AIC sector Global Equity Income; Global 28/02/15 8.7 8.4 7.0 5.0 5.6 29/02/16 (7.7) (7.2) (4.7) (3.9) (7.3) FMPI one-year performance 28/02/17 24.7 24.9 22.1 23.7 22.8 140 4 Note: Twelve-month rolling discrete total return performance. -

Wheat from Chaff Way to Address Its Debt and Pension Issues While Sheet and Operations Are in an Altogether Different Reinvigorating Growth

TIPS IDEAS FARM could prove wrong and the company may find a That said, the quality of this company’s balance Wheat from chaff way to address its debt and pension issues while sheet and operations are in an altogether different reinvigorating growth. There would certainly be and superior category to that of AA. Our view ALGY HALL plenty of potential valuation upside if it did, but here is based more on our concerns about over n last week’s column I looked at research from our opinion is that this is unlikely and the risks in optimism in the trading outlook (see page 41). Iquant firm Verdad that illustrated what poor the opposite direction are currently unpalatable. Fashion retailer Joules (JOUL) is another returns investors tend to get from buying shares Helping to inform the question about case where our tables nave hinted that some- in companies with distressed debt. In this the group’s prospects are the objective clues thing interesting may be happening. Last week week’s tip section our writers have been trying from both our table of most shorted stocks the company appeared to have experienced to sort some of the wheat from the chaff. and broker downgrades. While AA shares strong broker forecast upgrades over the prior When a rising market lifts all boats, it can have been significantly more shorted in the month. This followed significant downgrades feel like an opportunity to exit poorly performing past, short interest has ticked up over the when lockdown began. Importantly, the positions that have proved a source of misery in past month, although as can be seen in the company’s business model looks good, the the recent past.