Phoenix Unit Trust Managers Manager's Interim Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Monks Investment Trust

WhatSupplement February 2021 Investment TRUST A ONCE IN A LIFETIME CHANCE Nine opportunities to pick up promising trusts that you will not want to miss out on Gresham House’s Richard Staveley talks investment philosophy; and TEMIT’s Chetan Sehgal on innovative EMs THINK: GROWTH If you’re thinking about your future, • 3 long-term growth trends drive our research think Martin Currie Global Portfolio Trust. • World-class sustainability ratings Our specialist team hand pick stocks with a focus on Find out more at martincurrieglobal.com long-term growth drivers, offering investors access to a Capital at risk. Values can go up and down. We do not target diversified portfolio of between 25 and 40 of the world’s particular sustainability outcomes. leading companies. Sustainability Rating: Martin Currie Investment Management Limited, registered in Scotland (no SC066107). Registered office: Saltire Court, 20 Castle Terrace, Edinburgh EHES. Authorised and regulated by the Financial Conduct Authority. Please note that calls to the above number may be recorded. Tel: 0808 100 2125 www.martincurrie.com © 2020 Morningstar, Inc. All rights reserved. Morningstar Rating as of 22-12-20. GPTpressAds2021.indd 2 05/01/2021 10:47 THINK: GROWTH If you’re thinking about your future, • 3 long-term growth trends drive our research think Martin Currie Global Portfolio Trust. • World-class sustainability ratings Our specialist team hand pick stocks with a focus on Find out more at martincurrieglobal.com long-term growth drivers, offering investors access to a Capital at risk. Values can go up and down. We do not target > diversified portfolio of between 25 and 40 of the world’s particular sustainability outcomes. -

Annual Report and Audited Financial Statements

Annual report and audited financial statements BlackRock Charities Funds • BlackRock Armed Forces Charities Growth & Income Fund • BlackRock Catholic Charities Growth & Income Fund • BlackRock Charities Growth & Income Fund • BlackRock Charities UK Bond Fund • BlackRock Charities UK Equity ESG Fund • BlackRock Charities UK Equity Fund • BlackRock Charities UK Equity Index Fund For the financial period ended 30 June 2020 Contents General Information 2 About the Trust 3 Charity Authorised Investment Fund 4 Charity Trustees’ Investment Responsibilities 4 Fund Manager 4 Significant Events 4 Investment Report 5 Report on Remuneration 15 Accounting and Distribution Policies 21 Financial Instruments and Risks 24 BlackRock Armed Forces Charities Growth & Income Fund 37 BlackRock Catholic Charities Growth & Income Fund 56 BlackRock Charities Growth & Income Fund 74 BlackRock Charities UK Bond Fund 95 BlackRock Charities UK Equity ESG Fund 111 BlackRock Charities UK Equity Fund 125 BlackRock Charities UK Equity Index Fund 138 Statement of Manager’s and Trustee’s Responsibilities 162 Independent Auditor’s Report 165 Supplementary Information 169 1 General Information Advisory Committee Members - BlackRock manager of the Funds, each of which is an alternative Armed Forces Charities Growth & Income investment fund for the purpose of the Alternative Fund: Investment Fund Managers Directive. Mr Michael Baines (Chairman) Mr Guy Davies Directors of the Manager Major General A Lyons CBE G D Bamping* Major General Ashley Truluck CB, CBE M B Cook Colonel -

Description Iresscode Exchange Current Margin New Margin 3I

Description IRESSCode Exchange Current Margin New Margin 3I INFRASTRUCTURE PLC 3IN LSE 20 20 888 HOLDINGS PLC 888 LSE 20 20 ASSOCIATED BRITISH ABF LSE 10 10 ADMIRAL GROUP PLC ADM LSE 10 10 AGGREKO PLC AGK LSE 20 20 ASHTEAD GROUP PLC AHT LSE 10 10 ANTOFAGASTA PLC ANTO LSE 15 10 ASOS PLC ASC LSE 20 20 ASHMORE GROUP PLC ASHM LSE 20 20 ABERFORTH SMALLER COM ASL LSE 20 20 AVEVA GROUP PLC AVV LSE 20 20 AVIVA PLC AV LSE 10 10 ASTRAZENECA PLC AZN LSE 10 10 BABCOCK INTERNATIONAL BAB LSE 20 20 BARR PLC BAG LSE 25 20 BARCLAYS PLC BARC LSE 10 10 BRITISH AMERICAN TOBA BATS LSE 10 10 BAE SYSTEMS PLC BA LSE 10 10 BALFOUR BEATTY PLC BBY LSE 20 20 BARRATT DEVELOPMENTS BDEV LSE 10 10 BARING EMERGING EUROP BEE LSE 50 100 BEAZLEY PLC BEZ LSE 20 20 BH GLOBAL LIMITED BHGG LSE 30 100 BOWLEVEN PLC BLVN LSE 60 50 BANKERS INVESTMENT BNKR LSE 20 20 BUNZL PLC BNZL LSE 10 10 BODYCOTE PLC BOY LSE 20 20 BP PLC BP LSE 10 10 BURBERRY GROUP PLC BRBY LSE 10 10 BLACKROCK WORLD MININ BRWM LSE 20 65 BT GROUP PLC BT-A LSE 10 10 BRITVIC PLC BVIC LSE 20 20 BOVIS HOMES GROUP PLC BVS LSE 20 20 BROWN GROUP PLC BWNG LSE 25 20 BELLWAY PLC BWY LSE 20 20 BIG YELLOW GROUP PLC BYG LSE 20 20 CENTRAL ASIA METALS PLC CAML LSE 40 30 CLOSE BROTHERS GROUP CBG LSE 20 20 CARNIVAL PLC CCL LSE 10 10 CENTAMIN PLC CEY LSE 20 20 CHARIOT OIL & GAS LTD CHAR LSE 100 100 CHEMRING GROUP PLC CHG LSE 25 20 CONYGAR INVESTMENT CIC LSE 50 40 CALEDONIA INVESTMENTS CLDN LSE 25 20 CARILLION PLC CLLN LSE 100 100 COMMUNISIS PLC CMS LSE 50 100 CENTRICA PLC CNA LSE 10 10 CAIRN ENERGY PLC CNE LSE 30 30 COBHAM PLC -

Hipgnosis Songs Fund Limited

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt as to the action you should take or the contents of this Prospectus, you are recommended to seek your own independent financial advice immediately from your stockbroker, bank, solicitor, accountant, or other appropriate independent financial adviser, who is authorised under the Financial Services and Markets Act 2000 (the “FSMA”) if you are in the United Kingdom, or from another appropriately authorised independent financial adviser if you are in a territory outside the United Kingdom. A copy of this document, which comprises a prospectus relating to Hipgnosis Songs Fund Limited (the “Company”) in connection with the issue of Issue Shares in the Company and their admission to trading on the Main Market and to listing on the premium listing category of the Official List, prepared in accordance with the Prospectus Rules of the FCA made pursuant to section 73A of the FSMA, has been filed with the Financial Conduct Authority in accordance with Rule 3.2 of the Prospectus Rules. The Prospectus has been approved by the FCA, as competent authority under the Prospectus Regulation and the FCA only approves this Prospectus as meeting the standards of completeness, comprehensibility and consistency imposed by the Prospectus Regulation. Accordingly, such approval should not be considered as an endorsement of the issuer, or of the quality of the securities, that are the subject of this Prospectus; investors should make their own assessment as to the suitability of investing in the Issue Shares. The Issue Shares are only suitable for investors: (i) who understand the potential risk of capital loss and that there may be limited liquidity in the underlying investments of the Company; (ii) for whom an investment in the Issue Shares is part of a diversified investment programme; and (iii) who fully understand and are willing to assume the risks involved in such an investment programme. -

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

Company Engagement Report

BAILLIE GIFFORD Company Engagement on Environmental, Social and Governance Issues Quarter 3: 1 July 2020 – 30 September 2020 Baillie Gifford Company Engagement on Environmental, Social and Governance Issues Company Engagement on Environmental, Social and Governance Issues Company Country Engagement Topic(s) 10x Genomics, Inc. United States Environmental/Social Abcam plc United Kingdom Corporate Governance Abiomed, Inc. United States Corporate Governance Addtech AB (publ.) Sweden AGM or EGM Proposals ADLER Group S.A. Germany AGM or EGM Proposals Ain Holdings Inc. Japan AGM or EGM Proposals Alphabet Inc. United States Environmental/Social Amazon.com, Inc. United States Environmental/Social Ashtead Group plc United Kingdom AGM or EGM Proposals Aumann AG Germany AGM or EGM Proposals AVEVA Group plc United Kingdom AGM or EGM Proposals Beijer Ref AB (publ) Sweden Environmental/Social BHP Group Plc United Kingdom Corporate Governance Environmental/Social boohoo group plc United Kingdom Environmental/Social British Land Company Plc United Kingdom AGM or EGM Proposals Burberry Group plc United Kingdom Executive Remuneration Calbee, Inc. Japan AGM or EGM Proposals 1 Baillie Gifford Company Engagement on Environmental, Social and Governance Issues Company Engagement on Environmental, Social and Governance Issues Company Country Engagement Topic(s) Calbee, Inc. Japan Environmental/Social Chegg, Inc. United States Environmental/Social Cisco Systems, Inc. United States Environmental/Social Discovery Limited South Africa Environmental/Social DP Aircraft I Limited United Kingdom AGM or EGM Proposals Ecolab Inc. United States Environmental/Social EnQuest PLC United Kingdom Corporate Governance Executive Remuneration Exact Sciences Corporation United States AGM or EGM Proposals Experian plc United Kingdom AGM or EGM Proposals First Derivatives plc United Kingdom Executive Remuneration First Republic Bank United States Environmental/Social GREE, Inc. -

The Art of Investing in Smaller Companies – P 30

www.whatinvestment.co.ukWhat FOR Investment A WEALTHIER FUTURE Issue 424 July 2018 £4.50 The art of investing in smaller companies – P 30 Emerging Profit from Wine Markets How looking beyond the China and India are catching blockbuster vintages can the US, but are they worth deliver corking returns investing in? – Page 36 – Page 50 WI.JULY.2018.Cover.indd 1 21/06/2018 16:07 NEED INVESTMENT GUIDANCE? Why not join thousands of investors and benefi t from all our independent analysis and insight? Subscribe www.whatinvestment.co.ukWhat FOR Investment A WEALTHIER FUTURE Issue 423 June 2018 £4.50 and get Britain’s Buffetts issues How can you profit 12 from the UK managers inspired by the legendary American investor for the price – P 14 of 10 > Unit Trusts 1 | >| The Last Word | Peter Elston behaviour of, say, numbers or Hubris is the greatest challenge planets or elementary particles or rocks or plants or people. Our new columnist argues that being a non- Successful investing, on the other conformist and not following the crowd can be hand, necessitates disagreement. The Aging bull The Empire Trust For me to give myself a chance uncomfortable but can also produce good returns of beating my competitors, and thus the market, the last thing I should do is agree with them. I The bull market might be The British Empire Trust I am not exactly sure how I have one was just lucky. Probably seek out where they are huddled ended up as a chief investment best to assume you were lucky. -

Changing Times INVESTING for a NEW WORLD ORDER?

SUMMER 2018 Changing times INVESTING FOR A NEW WORLD ORDER? alliancetrustsavings.co.uk Welcome to the latest edition of Taking Stock. Changing times If this edition had a theme tune it might be something like Bob Dylan’s 1960s classic The Times They Are A-Changin’. Or at least that’s how it feels to many of us. US protectionism, Trump-style diplomacy, North Korea, Iran, Syria, Russia, China, Brexit, Facebook, Cambridge Analytica. These have all been headline makers for 2018 so far, and some have undoubtedly been implicated in increased market volatility. Around the world the political and economic power of nation states has always ebbed and flowed. Alliances are made and undone. And the fortunes of individual corporations rise and fall. But the question for investors today is, are we just looking at a variation on a theme of business as usual for the world’s established economic power base? Or is something else going on? Are we on the cusp of some more fundamental change in the world economic order? Keeping ahead of the curve Views on this matter because searching for growth necessarily involves looking ahead and understanding where the longer-term opportunities and threats are likely to be. In this edition of Taking Stock our expert contributors explore the potential implications of the developing picture. From how it’s influencing investment decisions today, to steps any investor can take to make the most of their money in uncertain times. As always, I hope you will find it an informative read. If you have any feedback or suggestions for future editions, please get in touch. -

FTSE Factsheet

FTSE COMPANY REPORT Share price analysis relative to sector and index performance BB Healthcare Trust BBH Closed End Investments — GBP 1.964 at close 20 April 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 21-Apr-2015 1D WTD MTD YTD Absolute - - - - Rel.Sector - - - - Rel.Market - - - - VALUATION Data unavailable Trailing PE 6.0 EV/EBITDA 5.4 PB 1.1 PCF -ve Div Yield 2.6 Price/Sales 5.7 Net Debt/Equity 0.0 Div Payout 15.4 ROE 21.6 DESCRIPTION Data unavailable The Company is a closed-ended investment company which to invest in a concentrated portfolio of listed or quoted equities in the global healthcare industry. Past performance is no guarantee of future results. Please see the final page for important legal disclosures. 1 of 4 FTSE COMPANY REPORT: BB Healthcare Trust 20 April 2021 Valuation Metrics Price to Earnings (PE) EV to EBITDA Price to Book (PB) 31-Mar-2021 31-Mar-2021 31-Mar-2021 25 25 1.5 1.4 20 20 +1SD 1.3 +1SD +1SD 1.2 Avg 15 15 1.1 Avg Avg -1SD 1 10 10 0.9 -1SD -1SD 5 5 0.8 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Murray International Trust (Ord) 120.0 Murray International Trust (Ord) 100.0 CVC Credit Partners European Opportunities (GBP) 2.3 European Opportunities Trust 120.0 European Opportunities Trust 100.0 Hipgnosis Songs Fund 2.2 Law Debenture Corp 120.0 Law Debenture Corp 100.0 Pacific Horizon Investment Trust 2.0 HICL Infrastructure 64.6 HICL Infrastructure 64.5 Scottish -

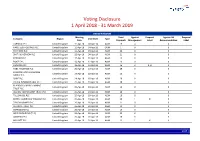

Global Voting Activity Report to March 2019

Voting Disclosure 1 April 2018 - 31 March 2019 UNITED KINGDOM Meeting Total Against Proposal Against ISS Proposal Company Region Vote Date Type Date Proposals Management Label Recommendation Label CARNIVAL PLC United Kingdom 11-Apr-18 04-Apr-18 AGM 19 0 0 HANSTEEN HOLDINGS PLC United Kingdom 11-Apr-18 04-Apr-18 OGM 1 0 0 RIO TINTO PLC United Kingdom 11-Apr-18 04-Apr-18 AGM 22 0 0 SMITH & NEPHEW PLC United Kingdom 12-Apr-18 04-Apr-18 AGM 21 0 0 PORVAIR PLC United Kingdom 17-Apr-18 10-Apr-18 AGM 15 0 0 BUNZL PLC United Kingdom 18-Apr-18 12-Apr-18 AGM 19 0 0 HUNTING PLC United Kingdom 18-Apr-18 12-Apr-18 AGM 16 2 3, 8 0 HSBC HOLDINGS PLC United Kingdom 20-Apr-18 13-Apr-18 AGM 29 0 0 LONDON STOCK EXCHANGE United Kingdom 24-Apr-18 18-Apr-18 AGM 26 0 0 GROUP PLC SHIRE PLC United Kingdom 24-Apr-18 18-Apr-18 AGM 20 0 0 CRODA INTERNATIONAL PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 18 0 0 BLACKROCK WORLD MINING United Kingdom 25-Apr-18 19-Apr-18 AGM 15 0 0 TRUST PLC ALLIANZ TECHNOLOGY TRUST PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 10 0 0 TULLOW OIL PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 16 0 0 BRITISH AMERICAN TOBACCO PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 20 1 8 0 TAYLOR WIMPEY PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 21 0 0 ALLIANCE TRUST PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 13 0 0 SCHRODERS PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 19 0 0 WEIR GROUP PLC (THE) United Kingdom 26-Apr-18 20-Apr-18 AGM 23 0 0 AGGREKO PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 20 0 0 MEGGITT PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 22 1 4 0 1/47 -

FTSE Factsheet

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Axiom European Financial Debt Fund AXI Closed End Investments — GBP 0.975 at close 20 April 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 21-Apr-2015 1D WTD MTD YTD Absolute - - - - Rel.Sector - - - - Rel.Market - - - - VALUATION Data unavailable Trailing PE 52.7 EV/EBITDA 25.0 PB 1.0 PCF 24.7 Div Yield 6.6 Price/Sales +ve Net Debt/Equity 0.0 Div Payout +ve ROE 1.8 DESCRIPTION Data unavailable The Company is a closed-ended investment company registered and incorporated in Guernsey and managed by Axiom Alternative Investments SARL. Past performance is no guarantee of future results. Please see the final page for important legal disclosures. 1 of 4 FTSE COMPANY REPORT: Axiom European Financial Debt Fund 20 April 2021 Valuation Metrics Price to Earnings (PE) EV to EBITDA Price to Book (PB) 31-Mar-2021 31-Mar-2021 31-Mar-2021 60 25 1.15 1.1 50 +1SD 20 1.05 40 1 15 0.95 Avg 30 0.9 10 +1SD 20 +1SD 0.85 -1SD 5 Avg 0.8 10 Avg 0.75 0 ‖ ‖ 0 ‖ ‖ -1SD 0.7 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Murray International Trust (Ord) 120.0 Murray International Trust (Ord) 100.0 CVC Credit Partners European Opportunities (GBP) 2.3 European Opportunities Trust 120.0 European Opportunities Trust 100.0 Hipgnosis Songs Fund 2.2 Law Debenture Corp 120.0 Law Debenture Corp 100.0 Pacific Horizon Investment Trust 2.0 HICL Infrastructure -

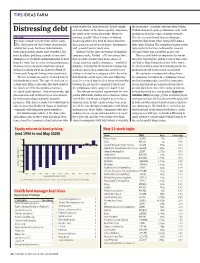

Distressing Debt Seek out Shares in the Lowest Quality Companies; Verdad Compared Equity Performance with Credit the Worst-Of-The-Worst, If You Like

TIPS IDEAS FARM want to play the ‘dash for trash’ should simply the issue price. A similar story was found when Distressing debt seek out shares in the lowest quality companies; Verdad compared equity performance with credit the worst-of-the-worst, if you like. However, quality based on the scores of rating agencies. ALGY HALL ignoring ‘quality’ when it comes to buying Here the research found share performance t’s been a tough time for short sellers lately. beaten-up stocks (the kind of shares found on started to deteriorate when ratings fell below a IThe ‘dash for trash’ that I wrote about in this these pages in our tables of shorts, downgrades high single B rating. The annualised equity return column last week, has been indiscriminate. and 52-week lows) is rarely wise. from stocks in the least creditworthy category Even real no-hoper shares have benefited. The Intrigued by the price movement of bankrupt- (CC and below) was a negative 34 per cent. most headline-grabbing example of investors’ company stocks, Verdad – a US investment firm This research holds an important lesson for willingness to overlook all fundamentals in their that specialises in investing in the shares of investors targeting the grubbier end of this recov- hunt for ‘trash’ has been the strong performance cheap, indebted, smaller companies – trawled its ery. Rather than buying the worst-of-the-worst, of shares in US companies that have already database. It looked for the long-term relationship it’s the best-of-the-worst that should provide the declared bankruptcy or are about to (Hertz, JC between share price performance and the level optimal trade-off between risk and reward.