4 Stocks with the Right Ingredients

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Description Iresscode Exchange Current Margin New Margin 3I

Description IRESSCode Exchange Current Margin New Margin 3I INFRASTRUCTURE PLC 3IN LSE 20 20 888 HOLDINGS PLC 888 LSE 20 20 ASSOCIATED BRITISH ABF LSE 10 10 ADMIRAL GROUP PLC ADM LSE 10 10 AGGREKO PLC AGK LSE 20 20 ASHTEAD GROUP PLC AHT LSE 10 10 ANTOFAGASTA PLC ANTO LSE 15 10 ASOS PLC ASC LSE 20 20 ASHMORE GROUP PLC ASHM LSE 20 20 ABERFORTH SMALLER COM ASL LSE 20 20 AVEVA GROUP PLC AVV LSE 20 20 AVIVA PLC AV LSE 10 10 ASTRAZENECA PLC AZN LSE 10 10 BABCOCK INTERNATIONAL BAB LSE 20 20 BARR PLC BAG LSE 25 20 BARCLAYS PLC BARC LSE 10 10 BRITISH AMERICAN TOBA BATS LSE 10 10 BAE SYSTEMS PLC BA LSE 10 10 BALFOUR BEATTY PLC BBY LSE 20 20 BARRATT DEVELOPMENTS BDEV LSE 10 10 BARING EMERGING EUROP BEE LSE 50 100 BEAZLEY PLC BEZ LSE 20 20 BH GLOBAL LIMITED BHGG LSE 30 100 BOWLEVEN PLC BLVN LSE 60 50 BANKERS INVESTMENT BNKR LSE 20 20 BUNZL PLC BNZL LSE 10 10 BODYCOTE PLC BOY LSE 20 20 BP PLC BP LSE 10 10 BURBERRY GROUP PLC BRBY LSE 10 10 BLACKROCK WORLD MININ BRWM LSE 20 65 BT GROUP PLC BT-A LSE 10 10 BRITVIC PLC BVIC LSE 20 20 BOVIS HOMES GROUP PLC BVS LSE 20 20 BROWN GROUP PLC BWNG LSE 25 20 BELLWAY PLC BWY LSE 20 20 BIG YELLOW GROUP PLC BYG LSE 20 20 CENTRAL ASIA METALS PLC CAML LSE 40 30 CLOSE BROTHERS GROUP CBG LSE 20 20 CARNIVAL PLC CCL LSE 10 10 CENTAMIN PLC CEY LSE 20 20 CHARIOT OIL & GAS LTD CHAR LSE 100 100 CHEMRING GROUP PLC CHG LSE 25 20 CONYGAR INVESTMENT CIC LSE 50 40 CALEDONIA INVESTMENTS CLDN LSE 25 20 CARILLION PLC CLLN LSE 100 100 COMMUNISIS PLC CMS LSE 50 100 CENTRICA PLC CNA LSE 10 10 CAIRN ENERGY PLC CNE LSE 30 30 COBHAM PLC -

The Sectors Which Recover Quickest from a Sell-Off

VOL 21 / ISSUE 43 / 31 OCTOBER 2019 / £4.49 BOUNCING BACK THE SECTORS WHICH RECOVER QUICKEST FROM A SELL-OFF... AND STAND TALLEST IN A DOWNTURN GLAXOSMITHKLINE WHY ALTERNATIVE FUNDS EXPOSED TRANSFORMED BY ASSETS ARE IN TO HIGH-RISK NEW STRATEGY DEMAND DIVIDENDS EDITOR’S VIEW Why stewardship really matters with investing A new code draws the spotlight on how big investors engage with companies he introduction of a new UK Stewardship in the eyes of the wider public has to be a good Code by the Financial Reporting Council thing, particularly if it opens people’s eyes to the T will look to raise the bar on how big opportunities provided by putting their cash to investors hold the companies in which they invest work in the markets. to account. A lot of the headlines around the news focused DON’T LOSE SIGHT OF UK STRENGTHS on the climate change angle but there is more to In fairness, if it wanted to distract from its own the code than environmental concerns, including shortcomings, the investment world could easily how institutions make their decisions and what point to failures of stewardship among the political they are doing about issues such as governance class in the UK. and diversity. As we write the country remains mired in a Brexit Fundamentally this is about recognising that stalemate with the potential joys of a Christmas investors are part-owners of a business. Even big election. Companies and markets are still denied asset managers are sometimes guilty of buying the clarity on the UK’s future relationship with the shares and seeing their work as done. -

The Art of Investing in Smaller Companies – P 30

www.whatinvestment.co.ukWhat FOR Investment A WEALTHIER FUTURE Issue 424 July 2018 £4.50 The art of investing in smaller companies – P 30 Emerging Profit from Wine Markets How looking beyond the China and India are catching blockbuster vintages can the US, but are they worth deliver corking returns investing in? – Page 36 – Page 50 WI.JULY.2018.Cover.indd 1 21/06/2018 16:07 NEED INVESTMENT GUIDANCE? Why not join thousands of investors and benefi t from all our independent analysis and insight? Subscribe www.whatinvestment.co.ukWhat FOR Investment A WEALTHIER FUTURE Issue 423 June 2018 £4.50 and get Britain’s Buffetts issues How can you profit 12 from the UK managers inspired by the legendary American investor for the price – P 14 of 10 > Unit Trusts 1 | >| The Last Word | Peter Elston behaviour of, say, numbers or Hubris is the greatest challenge planets or elementary particles or rocks or plants or people. Our new columnist argues that being a non- Successful investing, on the other conformist and not following the crowd can be hand, necessitates disagreement. The Aging bull The Empire Trust For me to give myself a chance uncomfortable but can also produce good returns of beating my competitors, and thus the market, the last thing I should do is agree with them. I The bull market might be The British Empire Trust I am not exactly sure how I have one was just lucky. Probably seek out where they are huddled ended up as a chief investment best to assume you were lucky. -

FTSE Factsheet

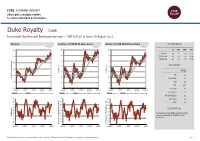

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Duke Royalty DUKE Investment Banking and Brokerage Services — GBP 0.4125 at close 10 August 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 10-Aug-2021 10-Aug-2021 10-Aug-2021 0.45 140 140 1D WTD MTD YTD Absolute -2.4 -1.2 -1.8 35.2 130 130 0.4 Rel.Sector -2.4 -0.5 -3.6 25.9 Rel.Market -2.8 -1.7 -3.7 20.9 120 120 0.35 VALUATION 110 110 0.3 Trailing 100 100 Relative Price Relative Price Relative 0.25 PE -ve Absolute Price (local (local currency) AbsolutePrice 90 90 EV/EBITDA -ve 0.2 80 80 PB 2.0 PCF 28.1 0.15 70 70 Div Yield 4.6 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Price/Sales -ve Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.2 90 90 90 Div Payout -ve 80 80 80 ROE -ve 70 70 70 Share Index) Share Share Sector) Share - 60 - 60 60 DESCRIPTION 50 50 50 40 40 The Company is a globally focused investment 40 RSI RSI (Absolute) 30 30 company specialising in diversified royalty investment. -

Global Voting Activity Report to March 2019

Voting Disclosure 1 April 2018 - 31 March 2019 UNITED KINGDOM Meeting Total Against Proposal Against ISS Proposal Company Region Vote Date Type Date Proposals Management Label Recommendation Label CARNIVAL PLC United Kingdom 11-Apr-18 04-Apr-18 AGM 19 0 0 HANSTEEN HOLDINGS PLC United Kingdom 11-Apr-18 04-Apr-18 OGM 1 0 0 RIO TINTO PLC United Kingdom 11-Apr-18 04-Apr-18 AGM 22 0 0 SMITH & NEPHEW PLC United Kingdom 12-Apr-18 04-Apr-18 AGM 21 0 0 PORVAIR PLC United Kingdom 17-Apr-18 10-Apr-18 AGM 15 0 0 BUNZL PLC United Kingdom 18-Apr-18 12-Apr-18 AGM 19 0 0 HUNTING PLC United Kingdom 18-Apr-18 12-Apr-18 AGM 16 2 3, 8 0 HSBC HOLDINGS PLC United Kingdom 20-Apr-18 13-Apr-18 AGM 29 0 0 LONDON STOCK EXCHANGE United Kingdom 24-Apr-18 18-Apr-18 AGM 26 0 0 GROUP PLC SHIRE PLC United Kingdom 24-Apr-18 18-Apr-18 AGM 20 0 0 CRODA INTERNATIONAL PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 18 0 0 BLACKROCK WORLD MINING United Kingdom 25-Apr-18 19-Apr-18 AGM 15 0 0 TRUST PLC ALLIANZ TECHNOLOGY TRUST PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 10 0 0 TULLOW OIL PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 16 0 0 BRITISH AMERICAN TOBACCO PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 20 1 8 0 TAYLOR WIMPEY PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 21 0 0 ALLIANCE TRUST PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 13 0 0 SCHRODERS PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 19 0 0 WEIR GROUP PLC (THE) United Kingdom 26-Apr-18 20-Apr-18 AGM 23 0 0 AGGREKO PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 20 0 0 MEGGITT PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 22 1 4 0 1/47 -

FTSE Factsheet

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Axiom European Financial Debt Fund AXI Closed End Investments — GBP 0.975 at close 20 April 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 21-Apr-2015 1D WTD MTD YTD Absolute - - - - Rel.Sector - - - - Rel.Market - - - - VALUATION Data unavailable Trailing PE 52.7 EV/EBITDA 25.0 PB 1.0 PCF 24.7 Div Yield 6.6 Price/Sales +ve Net Debt/Equity 0.0 Div Payout +ve ROE 1.8 DESCRIPTION Data unavailable The Company is a closed-ended investment company registered and incorporated in Guernsey and managed by Axiom Alternative Investments SARL. Past performance is no guarantee of future results. Please see the final page for important legal disclosures. 1 of 4 FTSE COMPANY REPORT: Axiom European Financial Debt Fund 20 April 2021 Valuation Metrics Price to Earnings (PE) EV to EBITDA Price to Book (PB) 31-Mar-2021 31-Mar-2021 31-Mar-2021 60 25 1.15 1.1 50 +1SD 20 1.05 40 1 15 0.95 Avg 30 0.9 10 +1SD 20 +1SD 0.85 -1SD 5 Avg 0.8 10 Avg 0.75 0 ‖ ‖ 0 ‖ ‖ -1SD 0.7 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Murray International Trust (Ord) 120.0 Murray International Trust (Ord) 100.0 CVC Credit Partners European Opportunities (GBP) 2.3 European Opportunities Trust 120.0 European Opportunities Trust 100.0 Hipgnosis Songs Fund 2.2 Law Debenture Corp 120.0 Law Debenture Corp 100.0 Pacific Horizon Investment Trust 2.0 HICL Infrastructure -

Distressing Debt Seek out Shares in the Lowest Quality Companies; Verdad Compared Equity Performance with Credit the Worst-Of-The-Worst, If You Like

TIPS IDEAS FARM want to play the ‘dash for trash’ should simply the issue price. A similar story was found when Distressing debt seek out shares in the lowest quality companies; Verdad compared equity performance with credit the worst-of-the-worst, if you like. However, quality based on the scores of rating agencies. ALGY HALL ignoring ‘quality’ when it comes to buying Here the research found share performance t’s been a tough time for short sellers lately. beaten-up stocks (the kind of shares found on started to deteriorate when ratings fell below a IThe ‘dash for trash’ that I wrote about in this these pages in our tables of shorts, downgrades high single B rating. The annualised equity return column last week, has been indiscriminate. and 52-week lows) is rarely wise. from stocks in the least creditworthy category Even real no-hoper shares have benefited. The Intrigued by the price movement of bankrupt- (CC and below) was a negative 34 per cent. most headline-grabbing example of investors’ company stocks, Verdad – a US investment firm This research holds an important lesson for willingness to overlook all fundamentals in their that specialises in investing in the shares of investors targeting the grubbier end of this recov- hunt for ‘trash’ has been the strong performance cheap, indebted, smaller companies – trawled its ery. Rather than buying the worst-of-the-worst, of shares in US companies that have already database. It looked for the long-term relationship it’s the best-of-the-worst that should provide the declared bankruptcy or are about to (Hertz, JC between share price performance and the level optimal trade-off between risk and reward. -

Good and Bad News for Investors

STOCKS | FUNDS | INVESTMENT TRUSTS | PENSIONS AND SAVINGS VOL 19 / ISSUE 46 / 23 NOVEMBER 2017 / £4.49 SHARES WE MAKE INVESTING EASIER CAN YOUR HOME FUND YOUR RETIREMENT? Good and bad news for investors WHY DO 5 QUESTIONS COMPANIES DIGITAL DISRUPTION RAISED BY BUY BACK HOW TO INVEST IN GAME ZPG’S MOVE ON SHARES? CHANGING COMPANIES GOCOMPARE Fundsmith LLP (“Fundsmith”) is authorised and regulated by The Fundsmith Emerging Equities Trust the Financial Conduct Authority and only acts for the funds (FEET) research team searches the world to to whom it provides regulated investment management and find companies that make their money from a transaction arrangement services. Fundsmith does not act for or advise potential investors in connection with acquiring large number of everyday, repeat, predictable shares in Fundsmith Emerging Equities Trust plc and will not transactions and will benefit from the rise of the be responsible to potential investors for providing them with protections afforded to clients of Fundsmith. consumer in developing economies. Prospective investors are strongly advised to take their own For example, Indofood sold 9 billion packets of legal, investment and tax advice from independent and suitably qualified advisers. The value of investments may Indomie noodles last year, Magnit welcomed 11 million go up as well as down. Past performance is not a guide to shoppers a day, MercadoLibre sold over 50 million future performance. items on its website last quarter and Dabur’s Hajmola FEET Performance, % Total Return tablets were taken 26 million times a day in India. Year ending 31st August 2017 2016 2015 Since inception You may never have heard of them, despite their FEET Share Price +3.6 +21.5 -16.2 +15.5 scale, but all can be found in the FEET portfolio. -

UK Investment Trusts Index This Listing Aims to Help Readers to Locate an Investment Trust in the AIC Sectors

UK Investment Trusts Index This listing aims to help readers to locate an investment trust in the AIC sectors. Funds are presented in alphabetical order by provider. Fund name Sector Fund name Sector Fund name Sector 3i Group Plc Private Equity Blackstone/GSO Loan Financing Limited Debt - Structured Finance Energiser Investments PLC Unclassified 3I Infrastructure Plc Infrastructure Blue Planet Investment Trust PLC ORD 1P Global High Income EP Global Opportunities Trust PLC Global Aberdeen Asian Income LTd Asia Pacific Income Blue Star Capital PLC Unclassified EPE Special Opportunities Unclassified Ab Div Inc & Grw Trt Flexible Investment Bluefield Solar Income Limited Renewable Energy Infrastructure European Assets Trust PLC European Smaller Companies AbrEmrMrInvCmpLtd Global Emerging Markets BMO Cap & Inc IT PLC UK Equity Income F&C Investment Trust Plc Global Abr Frn Mr Inv CmpLtd Global Emerging Markets BMO Commercial Property Trust Limited Property - UK Commercial F&C UK Real Estate Investments Limited Property - UK Commercial Aberdeen Japan IT PLC Japan BMO Global Smaller Companies Plc Global Smaller Companies Fair Oaks Income Limited 2017 SHS Debt - Structured Finance Aberdeen Latin American Income Ltd Latin America BMO Managed Portfolio Trust Plc Growth Flexible Investment FastForward Innovations Limited Ord 1P Private Equity Abrdn New Dawn IT PLC Asia Pacific BMO Managed Portfolio Trust Plc Inc Flexible Investment Fidelity Asian Values PLC Asia Pacific Aberdeen New Ind IT PLC Ord Country Specialist: Asia Pacific ex Jap BMO Private -

Stoxx® Europe Total Market Financial Services Index

STOXX® EUROPE TOTAL MARKET FINANCIAL SERVICES INDEX Components1 Company Supersector Country Weight (%) LONDON STOCK EXCHANGE Financial Services GB 10.21 DEUTSCHE BOERSE Financial Services DE 9.72 INVESTOR B Financial Services SE 8.23 PARTNERS GRP HLDG Financial Services CH 5.46 3I GROUP PLC. Financial Services GB 4.58 STANDARD LIFE ABERDEEN Financial Services GB 3.39 EXOR NV Financial Services IT 2.91 INVESTOR A Financial Services SE 2.82 GRP BRUXELLES LAMBERT Financial Services BE 2.74 M&G Financial Services GB 2.63 HARGREAVES LANSDOWN Financial Services GB 2.32 INTERMEDIATE CAPITAL GRP Financial Services GB 2.01 KINNEVIK B Financial Services SE 1.93 SCHRODERS Financial Services GB 1.68 AMUNDI Financial Services FR 1.54 EURONEXT Financial Services FR 1.41 INDUSTRIVARDEN A Financial Services SE 1.37 INDUSTRIVARDEN C Financial Services SE 1.32 INVESTEC Financial Services GB 1.24 WENDEL Financial Services FR 1.20 QUILTER Financial Services GB 1.17 ACKERMANS & VAN HAAREN Financial Services BE 1.14 SOFINA Financial Services BE 1.09 IG GRP HLDG Financial Services GB 1.08 MAN GRP Financial Services GB 1.04 PARGESA Financial Services CH 1.01 TP ICAP Financial Services GB 0.98 EURAZEO Financial Services FR 0.98 ASHMORE GRP Financial Services GB 0.97 BOLSAS Y MERCADOS ESPANOLES Financial Services ES 0.93 GRENKE N Financial Services DE 0.92 AZIMUT HLDG Financial Services IT 0.84 ONESAVINGS BANK Financial Services GB 0.80 JUPITER FUND MANAGEMENT Financial Services GB 0.79 JOHN LAING GROUP Financial Services GB 0.78 LATOUR INVESTMENT B Financial -

Issue Country of Domicile GICS Sector Portfolio Weight (%) AJ BELL United

Issue Country of domicile GICS sector Portfolio weight (%) AJ BELL United Kingdom Financials 3.35% AVAST United Kingdom Information Technology 2.45% CAPITAL FOR COLLEAGUES United Kingdom Financials 0.03% CERES POWER HOLDINGS United Kingdom Industrials 0.76% COMPASS GROUP United Kingdom Consumer Discretionary 1.73% COUNTRYSIDE PROPERTIES United Kingdom Consumer Discretionary 3.84% CREST NICHOLSON HOLDINGS United Kingdom Consumer Discretionary 1.84% DFS FURNITURE United Kingdom Consumer Discretionary 3.08% DISTRIBUTION FINANCE CAPITAL United Kingdom Financials 0.70% ETHICAL PROPERTY CO United Kingdom Real Estate 0.06% FIRST DERIVATIVES United Kingdom Information Technology 2.00% GB GROUP United Kingdom Information Technology 2.58% GENUIT GROUP United Kingdom Industrials 1.04% GREENCOAT UK WIND United Kingdom Utilities 0.96% GYM GROUP United Kingdom Consumer Discretionary 2.75% HALMA United Kingdom Information Technology 2.74% HARGREAVES LANSDOWN United Kingdom Financials 3.53% HELIOS TOWERS United Kingdom Communication Services 2.93% HOME REIT United Kingdom Consumer Discretionary 0.88% INTERTEK GROUP United Kingdom Industrials 3.23% KINGSPAN GROUP Ireland Industrials 2.52% LEARNING TECHNOLOGIES GROUP United Kingdom Information Technology 4.01% LEGAL & GENERAL GROUP United Kingdom Financials 3.72% LONDON STOCK EXCHANGE GROUP United Kingdom Financials 3.78% MORTGAGE ADVICE BUREAU HOLDINGS United Kingdom Financials 1.57% NATIONAL EXPRESS GROUP United Kingdom Industrials 3.35% NATIONAL GRID United Kingdom Utilities 1.30% OXFORD INSTRUMENTS -

DECA Lunch Menu

Date | January 4 Price | All you can eat buffet $10.00 Mongolian Grill Taco Bar Garbage Plates Chicken, Beef & Vegetarian Taco on Corn, Hamburgers, Cheeseburgers, Hot Dogs, Macaroni Salad, White or Wholegrain Tortilla Homefries, Baked Beans, Hot Sauce Spanish Beans, Cilantro Rice, Romaine, Tomatoes, Olives, Jalapeños, Sour Cream, Guacamole, Pepper Jack Ched- Pizza dar Cheese Blend, Ranch Taco Sauce, Homemade Pico de Gallo & Chipotle Picante Sauce Sheet Pizzas Pepperoni / Cheese / Sausage & Mushroom Grill Angus Beef or Halal Burgers Pasta Bar Grilled Chicken Barilla Regular & Wholegrain Pasta Toppings: Italian Chicken, Italian Tofu, Steamed Broccoli, Zwiegel’s Hot Dog Seasonal Vegetable, Meatballs Chicken Fingers Tomato Sauce & Alfredo Sauce Grilled Cheese Deli Fried Fish Fillet Sandwiches Boca Burger (vegan) White or Wheat Sub Roll, Wraps, Variety of Breads Black Bean Burger (vegan) Turkey, Ham, Roast Beef, Regular & Lite Tuna Salad, Gardenburger Original (vegetarian) Chicken, Hummus Toppings: Bacon, American Cheese, Lettuce, Tomato, Bacon, Tomato, Lettuce, Onion, Banana Peppers, Onions, Onion, Relish & Tartar Sauce Pickles, Cucumbers Sides: French Fries, Cheese Sauce American, Swiss, Cheddar, Provolone, Mozzarella Cheeses Condiments: Mayonnaise, Reduced Fat Mayonnaise, Caesar, Yellow Mustard, Spicy Brown Mustard, Honey Salad Bar Mustard, Italian Dressing Romaine Salad Mix Baby Spinach Toppings Toppings: Chopped Egg, Edamame, Chicken, Tuna, Olives, Broccoli, Baby Carrots, Cucumbers, Grape Tomatoes, Peppers, Cottage Cheese, Pepper Jack Cheddar Cheese, Asiago Cheese, Greek Yogurt, Cut Fruit, Canned Fruit, Assorted Dressings, Croutons, Bacon Bits, & Sunower Seeds Assorted Desserts, Ice Cream & Beverages.