Protecting Workers from Unlawful Interference with Their Jobs PROTECTING WORKERS from UNLAWFUL INTERFERENCE with THEIR JOBS

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Notes and Sources for Evil Geniuses: the Unmaking of America: a Recent History

Notes and Sources for Evil Geniuses: The Unmaking of America: A Recent History Introduction xiv “If infectious greed is the virus” Kurt Andersen, “City of Schemes,” The New York Times, Oct. 6, 2002. xvi “run of pedal-to-the-medal hypercapitalism” Kurt Andersen, “American Roulette,” New York, December 22, 2006. xx “People of the same trade” Adam Smith, The Wealth of Nations, ed. Andrew Skinner, 1776 (London: Penguin, 1999) Book I, Chapter X. Chapter 1 4 “The discovery of America offered” Alexis de Tocqueville, Democracy In America, trans. Arthur Goldhammer (New York: Library of America, 2012), Book One, Introductory Chapter. 4 “A new science of politics” Tocqueville, Democracy In America, Book One, Introductory Chapter. 4 “The inhabitants of the United States” Tocqueville, Democracy In America, Book One, Chapter XVIII. 5 “there was virtually no economic growth” Robert J Gordon. “Is US economic growth over? Faltering innovation confronts the six headwinds.” Policy Insight No. 63. Centre for Economic Policy Research, September, 2012. --Thomas Piketty, “World Growth from the Antiquity (growth rate per period),” Quandl. 6 each citizen’s share of the economy Richard H. Steckel, “A History of the Standard of Living in the United States,” in EH.net (Economic History Association, 2020). --Andrew McAfee and Erik Brynjolfsson, The Second Machine Age: Work, Progress, and Prosperity in a Time of Brilliant Technologies (New York: W.W. Norton, 2016), p. 98. 6 “Constant revolutionizing of production” Friedrich Engels and Karl Marx, Manifesto of the Communist Party (Moscow: Progress Publishers, 1969), Chapter I. 7 from the early 1840s to 1860 Tomas Nonnenmacher, “History of the U.S. -

The SEC and the Failure of Federal, Takeover Regulation

Florida State University Law Review Volume 34 Issue 2 Article 2 2007 The SEC and the Failure of Federal, Takeover Regulation Steven M. Davidoff [email protected] Follow this and additional works at: https://ir.law.fsu.edu/lr Part of the Law Commons Recommended Citation Steven M. Davidoff, The SEC and the Failure of Federal, Takeover Regulation, 34 Fla. St. U. L. Rev. (2007) . https://ir.law.fsu.edu/lr/vol34/iss2/2 This Article is brought to you for free and open access by Scholarship Repository. It has been accepted for inclusion in Florida State University Law Review by an authorized editor of Scholarship Repository. For more information, please contact [email protected]. FLORIDA STATE UNIVERSITY LAW REVIEW THE SEC AND THE FAILURE OF FEDERAL TAKEOVER REGULATION Steven M. Davidoff VOLUME 34 WINTER 2007 NUMBER 2 Recommended citation: Steven M. Davidoff, The SEC and the Failure of Federal Takeover Regulation, 34 FLA. ST. U. L. REV. 211 (2007). THE SEC AND THE FAILURE OF FEDERAL TAKEOVER REGULATION STEVEN M. DAVIDOFF* I. INTRODUCTION.................................................................................................. 211 II. THE GOLDEN AGE OF FEDERAL TAKEOVER REGULATION.................................. 215 A. The Williams Act (the 1960s) ..................................................................... 215 B. Going-Privates (the 1970s)......................................................................... 219 C. Hostile Takeovers (the 1980s)..................................................................... 224 1. SEC Legislative -

Rethinking the Federal Securities Laws

Florida International University College of Law eCollections Faculty Publications Faculty Scholarship 2003 Accountants Make Miserable Policemen: Rethinking the Federal Securities Laws Jerry W. Markham Florida International University College of Law Follow this and additional works at: https://ecollections.law.fiu.edu/faculty_publications Part of the Banking and Finance Law Commons Recommended Citation Jerry W. Markham, Accountants Make Miserable Policemen: Rethinking the Federal Securities Laws, 28 N.C.J. Int'l L. & Com. Reg. 725, 812 (2003). This Article is brought to you for free and open access by the Faculty Scholarship at eCollections. It has been accepted for inclusion in Faculty Publications by an authorized administrator of eCollections. For more information, please contact [email protected]. +(,121/,1( Citation: Jerry W. Markham, Accountants Make Miserable Policemen: Rethinking the Federal Securities Laws, 28 N.C.J. Int'l L. & Com. Reg. 725 (2003) Provided by: FIU College of Law Content downloaded/printed from HeinOnline Tue May 1 11:26:02 2018 -- Your use of this HeinOnline PDF indicates your acceptance of HeinOnline's Terms and Conditions of the license agreement available at https://heinonline.org/HOL/License -- The search text of this PDF is generated from uncorrected OCR text. -- To obtain permission to use this article beyond the scope of your HeinOnline license, please use: Copyright Information Use QR Code reader to send PDF to your smartphone or tablet device Accountants Make Miserable Policemen: Rethinking the Federal -

Alemany, Ricard

1 As I finished my first year of the MBA, one of my mentor’s advice was to read. Used to reading case studies, the question really was “what books should I read?”. After two years at IESE, and experiencing first hand the breadth and depth of knowledge shared from IESE Faculty, I thought the most valuable advice on what to read was right in front of me. How could I continue to learn from professors beyond the classroom, once the MBA path comes to an end. I thought a reading list from IESE Faculty could serve not just me, but my whole class and perhaps future IESE graduates, as a guide to continue learning. Therefore, I asked professors for book recommendations that would inspire and guide us in our future endeavors. The document that follows is the result of it. I hope you find this document insightful and useful. I would like to thank all the participating professors for their recommendations and participation in the project and for sharing their knowledge not only in class, but also beyond it. Additionally, I am grateful for the help and patience of Eduardo Pérez (IESE MBA 2019), the creative genius, who has given shape of the document that I here present to you. Antonio Recio Sanromán. " Our brain is like our body: it needs exercise. If you don’t read at least one good book every month, you will lose most of the good intellectual and analytical shape you got during the MBA reading every day case after case… So, don’t stop reading. -

The New Investor Tom C.W

The New Investor Tom C.W. Lin EVIEW R ABSTRACT A sea change is happening in finance. Machines appear to be on the rise and humans on LA LAW LA LAW the decline. Human endeavors have become unmanned endeavors. Human thought and UC human deliberation have been replaced by computerized analysis and mathematical models. Technological advances have made finance faster, larger, more global, more interconnected, and less human. Modern finance is becoming an industry in which the main players are no longer entirely human. Instead, the key players are now cyborgs: part machine, part human. Modern finance is transforming into what this Article calls cyborg finance. This Article offers one of the first broad, descriptive, and normative examinations of this sea change and its wide-ranging effects on law, society, and finance. The Article begins by placing the rise of artificial intelligence and computerization in finance within a larger social context. Next, it explores the evolution and birth of a new investor paradigm in law precipitated by that rise. This Article then identifies and addresses regulatory dangers, challenges, and consequences tied to the increasing reliance on artificial intelligence and computers. Specifically, it warns of emerging financial threats in cyberspace, examines new systemic risks linked to speed and connectivity, studies law’s capacity to govern this evolving financial landscape, and explores the growing resource asymmetries in finance. Finally, drawing on themes from the legal discourse about the choice between rules and standards, this Article closes with a defense of humans in an uncertain financial world in which machines continue to rise, and it asserts that smarter humans working with smart machines possess the key to better returns and better futures. -

Americans for Tax Fairness Selected Opinion Pieces on Corporate Inversions

AMERICANS FOR TAX FAIRNESS SELECTED OPINION PIECES ON CORPORATE INVERSIONS As of October 1, 2014 NATIONAL Fortune – Positively un-American Tax Dodgers, Allan Sloan, July 7, 2014 “Undermining the finances of the federal government by inverting helps undermine our economy. And that’s a bad thing, in the long run, for companies that do business in America.” Fortune – Foreign Tax Ploys Raise a Question: What is an American Company?, Allan Sloan, June 2, 2014 “But in the past few years, as the world has become more global and other countries have cut their corporate rates, a new exodus wave has started. ‘For the past 20 years, there’s been an arms race between the companies on the one hand and the IRS and Congress on the other, and the companies always seem to come up with better weapons,’ says tax expert Bob Willens.” The New York Times – Cracking Down on Corporate Tax Games, The Editorial Board, September 23, 2014 “New rules from the Treasury Department[2] are likely to slow the offensive practice that allows American companies to avoid taxes by merging with foreign rivals. Known as corporate inversions, these are complex, modern variations on the practices of yesteryear, when companies dodged their taxes by moving their addresses to post office boxes in the Caribbean.” The New York Times – At Walgreen, Renouncing Corporate Citizenship, Andrew Ross Sorkin, June 30, 2014 “In Walgreen’s case, an inversion would be an affront to United States taxpayers. The company, which also owns the Duane Reade chain in New York, reaps almost a quarter of -

A Business Lawyer's Bibliography: Books Every Dealmaker Should Read

585 A Business Lawyer’s Bibliography: Books Every Dealmaker Should Read Robert C. Illig Introduction There exists today in America’s libraries and bookstores a superb if underappreciated resource for those interested in teaching or learning about business law. Academic historians and contemporary financial journalists have amassed a huge and varied collection of books that tell the story of how, why and for whom our modern business world operates. For those not currently on the front line of legal practice, these books offer a quick and meaningful way in. They help the reader obtain something not included in the typical three-year tour of the law school classroom—a sense of the context of our practice. Although the typical law school curriculum places an appropriately heavy emphasis on theory and doctrine, the importance of a solid grounding in context should not be underestimated. The best business lawyers provide not only legal analysis and deal execution. We offer wisdom and counsel. When we cast ourselves in the role of technocrats, as Ronald Gilson would have us do, we allow our advice to be defined downward and ultimately commoditized.1 Yet the best of us strive to be much more than legal engineers, and our advice much more than a mere commodity. When we master context, we rise to the level of counselors—purveyors of judgment, caution and insight. The question, then, for young attorneys or those who lack experience in a particular field is how best to attain the prudence and judgment that are the promise of our profession. For some, insight is gained through youthful immersion in a family business or other enterprise or experience. -

Economic Principals \273 Blog Archive \273 a Normal Professor

Economic Principals » Blog Archive » A Normal Professor http://www.economicprincipals.com/issues/2008.06.01/320.html Home June 1, 2008 David Warsh, Proprietor About Archives previous | contents | next Books A Normal Professor Receive the Bulldog Edition Perhaps, now that Harvard’s Russia scandal is receding into the past, Andrei Shleifer, 47, will take it easy. He has a steady stream of students, presides over a growing literature in comparative economics, and has developed an interesting sideline in the economics of persuasion. His wife, Nancy Zimmerman , runs a hedge fund that has seen explosive growth, today managing more than $3 billion for institutional clients; together the pair, through their start-ups, may have Economic Blogosphere amassed net worth of $40 million or more. (A columnist for Economics Portfolio magazine’s website subsequently estimated that Roundtable the figure may be closer to $1 bullion.) Their children are Economists View growing, his energetic parents live nearby, he superintends a steady stream of visitors to his villa in the south of France, and he keeps a hand in with developments in Russia. Economic Journalists For example, when Anders Aslund , of Washington’s Peterson Allan Sloan institute for International Economics, was in Cambridge, Amity Shlaes Mass. last winter, to celebrate the publication of How Andrew Leonard Capitalism Was Built: The Transformation of Central and Binyamin Appelbaum Eastern Europe, Russia, and Central Asia and Russia’s Bruce Bartlett Capitalist Revolution: Why Market Reform Succeeded and Carl Bialik Democracy Failed , Shleifer, the author of A Normal Catherine Rampell Country: Russia After Communism , threw a party for him at Charles Duhigg his spacious home on unpaved Bracebridge Road in suburban Christopher Caldwell Newton. -

Insider Trading

Brooklyn Law School BrooklynWorks Faculty Scholarship 9-1998 Outsider Trading on Confidential Information: A Breech in Search of a Duty Roberta S. Karmel Brooklyn Law School, [email protected] Follow this and additional works at: https://brooklynworks.brooklaw.edu/faculty Part of the Other Law Commons, and the Securities Law Commons Recommended Citation 20 Cardozo L. Rev. 83 (1998-1999) This Article is brought to you for free and open access by BrooklynWorks. It has been accepted for inclusion in Faculty Scholarship by an authorized administrator of BrooklynWorks. OUTSIDER TRADING ON CONFIDENTIAL INFORMATION-A BREACH IN-SEARCH OF A DUTY Roberta S. Karmel* INTRODUCTION Insider trading cases are a key part of the enforcement pro- gram of the Securities and Exchange Commission ("SEC").1 Many prosecutions of insider trading, however, do not involve true in- sider trading. Rather, they involve trading by outsiders, that is, persons who are not employed by the issuer whose securities are traded, and who trade on nonpublic market information. A fre- quent type of outsider trading is trading in anticipation of a tender offer not yet announced. Because of the egregious facts underly- ing these cases, the SEC has been able to prosecute hundreds of cases without formulating a reasoned analysis of the legal and policy issues involved. Also, despite the large number of articles discussing insider trading, a general consensus among commenta- tors has not developed as to why insider trading is unlawful.2 * Professor and Co-Director of the Center for the Study of International Business Law at Brooklyn Law School. The author is also of counsel to Kelley Drye & Warren LLP. -

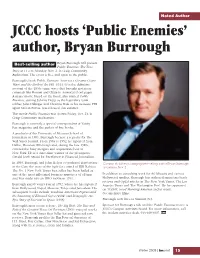

JCCC Hosts 'Public Enemies' Author, Bryan Burrough

Noted Author JCCC hosts ‘Public Enemies’ author, Bryan Burrough Best-selling author Bryan Burrough will present Public Enemies: The True Story at 11 a.m. Monday, Nov. 2, in Craig Community Auditorium. The event is free and open to the public. Burrough’s book Public Enemies: America’s Greatest Crime Wave and the Birth of the FBI, 1933-34 is the definitive account of the 1930s crime wave that brought notorious criminals like Bonnie and Clyde to America’s front pages. A major movie based on the book, also named Public Enemies, starring Johnny Depp as the legendary bank robber John Dillinger and Christian Bale as his nemesis, FBI agent Melvin Purvis, was released this summer. The movie Public Enemies was shown Friday, Oct. 23, in Craig Community Auditorium. Burrough is currently a special correspondent at Vanity Fair magazine and the author of five books. A graduate of the University of Missouri School of Journalism in 1983, Burrough became a reporter for The Wall Street Journal. From 1983 to 1992, he reported from Dallas, Houston, Pittsburgh and, during the late 1980s, covered the busy mergers and acquisitions beat in New York. He is a three-time winner of the prestigious Gerald Loeb Award for Excellence in Financial Journalism. In 1990, Burrough and John Helyar co-authored Barbarians Campus Activities is bringing best-selling author Bryan Burrough at the Gate, the story of the fight for control of RJR Nabisco. to campus Nov. 2. The No. 1 New York Times best-seller has been hailed as one of the most influential business narratives of all time In addition to consulting work for 60 Minutes and various and was made into an HBO movie in 1993. -

2018 Audio Catalog on Demand Getting Ahead of ADHD Joel T

CONTENTS NEW TITLE INDEX CONTENTS NEW TITLE INDEX SELLING MANAGEMENT General Selling Skills.......................................................... 2 On Demand The Coaching Habit Michael Bungay Stanier...................... 12 Pharmaceutical Selling ....................................................... 7 On Demand Collaboration Begins... Ken Blanchard .................................... 12 MANAGEMENT Both Move Your Bus Ron Clark ............................................ 22 General Management Skills................................................ 9 On Demand The Servant Ames C. Hunter .................................. 24 On Demand The Vibrant Workplace Paul White .......................................... 28 Personal Development...................................................... 29 NEW TITLE INDEX BUSINESS Marketing .......................................................................... 38 PERSONAL DEVELOPMENT Entrepreneurship .............................................................. 41 On Demand The Go-Giver Bob Burg, John David Mann ............. 32 Business Concepts ........................................................... 42 On Demand Leader’s Bookshelf R. Manning Ancel ............................... 33 Financial............................................................................ 53 On Demand Overcoming Bias Tiffany Jana, Matthew Freeman ........ 35 Future................................................................................ 57 On Demand The Power Of Moments Chip and Dan Heath........................... -

J. Edgar Hoover and the Anti-Interventionists

J. Edgar Hoover and the Anti-interventionists J. Edgar Hoover and the Anti-interventionists FBI Political Surveillance and the Rise of the Domestic Security State, 1939–1945 Douglas M. Charles THE OHIo STATE UNIVERSITY PREss • COLUMBUS Copyrght © 2007 by The Oho State Unversty. All rghts reserved. Library of Congress Catalogng-n-Publcaton Data Charles, Douglas M. J. Edgar Hoover and the ant-nterventonsts : FBI poltcal survellance and the rse of the domestc securty state, 1939–1945 / Douglas M. Charles. p. cm. Includes bblographcal references and index. ISBN-13: 978-0-8142-1061-1 (cloth : alk. paper) ISBN-10: 0-8142-1061-9 (cloth : alk. paper) ISBN-13: 978-0-8142-9140-5 (cd-rom) ISBN-10: 0-8142-9140-6 (cd-rom) 1. Hoover, J. Edgar (John Edgar), 1895–1972. 2. Roosevelt, Frankln D. (Frankln Delano), 1882–1945. 3. Unted States. Federal Bureau of Investgaton—History. 4. World War, 1939–1945—Unted States. 5. Intellgence servce—Unted States— History—20th century. 6. Internal securty—Unted States—History—20th cen- tury. 7. Dssenters—Government polcy—Unted States—History—20th century. 8. Neutralty—Unted States—History—20th century. 9. Unted States—History—1933– 1945. 10. Unted States—Foregn relatons—1933–1945—Publc opnon. I. Ttle. HV8144.F43C43 2007 940.53'160973—dc22 2006102680 Cover desgn by Janna Thompson-Chordas Typeset in Adobe Minon Pro Typesettng by Julet Wllams Prnted by Thomson-Shore The paper used in ths publcaton meets the mnmum requrements of the Amercan Natonal Standard for Informaton Scences—Permanence of Paper for Prnted Library