Effect of Chapter 11 Bankruptcy Protection on Airfares in the U.S

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

WORLD AVIATION Yearbook 2013 EUROPE

WORLD AVIATION Yearbook 2013 EUROPE 1 PROFILES W ESTERN EUROPE TOP 10 AIRLINES SOURCE: CAPA - CENTRE FOR AVIATION AND INNOVATA | WEEK startinG 31-MAR-2013 R ANKING CARRIER NAME SEATS Lufthansa 1 Lufthansa 1,739,886 Ryanair 2 Ryanair 1,604,799 Air France 3 Air France 1,329,819 easyJet Britis 4 easyJet 1,200,528 Airways 5 British Airways 1,025,222 SAS 6 SAS 703,817 airberlin KLM Royal 7 airberlin 609,008 Dutch Airlines 8 KLM Royal Dutch Airlines 571,584 Iberia 9 Iberia 534,125 Other Western 10 Norwegian Air Shuttle 494,828 W ESTERN EUROPE TOP 10 AIRPORTS SOURCE: CAPA - CENTRE FOR AVIATION AND INNOVATA | WEEK startinG 31-MAR-2013 Europe R ANKING CARRIER NAME SEATS 1 London Heathrow Airport 1,774,606 2 Paris Charles De Gaulle Airport 1,421,231 Outlook 3 Frankfurt Airport 1,394,143 4 Amsterdam Airport Schiphol 1,052,624 5 Madrid Barajas Airport 1,016,791 HE EUROPEAN AIRLINE MARKET 6 Munich Airport 1,007,000 HAS A NUMBER OF DIVIDING LINES. 7 Rome Fiumicino Airport 812,178 There is little growth on routes within the 8 Barcelona El Prat Airport 768,004 continent, but steady growth on long-haul. MostT of the growth within Europe goes to low-cost 9 Paris Orly Field 683,097 carriers, while the major legacy groups restructure 10 London Gatwick Airport 622,909 their short/medium-haul activities. The big Western countries see little or negative traffic growth, while the East enjoys a growth spurt ... ... On the other hand, the big Western airline groups continue to lead consolidation, while many in the East struggle to survive. -

ALPA Los Angeles Field Office Records

Air Line Pilots Association Los Angeles Field Office 1955-1989 (Predominately 70s & 80s) 18 Storage Boxes 1 Manuscript Box Accession #247 Provenance The papers of the Airline Pilots Association of the Los Angeles Field Office were deposited to the Walter P. Reuther Library in 1976 and have been added to over the years since that time. Last addition was in 1991. Collection Information This is composed mainly of correspondence, minutes, reports and statistic concerning various airlines. The largest represented airlines include Continental Airlines, Flying Tiger Line, Trans World Airlines and Western Airlines. Important Subjects Air Safety Forum Airworthiness Review Briefs of Accidents Continental Airlines (CAL) Delta Airlines (DAL) Engineering & Air Safety Flying Tiger Line (FTL) LAX Area Safety Master Executive Council (MEC) Pan American World Airways (PAA) Trans World Airlines (TWA) United Airlines (UAL) Western Airlines (WAL) Important Correspondence Continental Airlines (CAL) Flying Tiger Line (FTL) Master Executive Council (MEC) Pan American World Airways (PAA) Trans World Airlines (TWA) United Airlines (UAL) Western Airlines (WAL) Box 1 1-1. AAH; Agreement; 1977 1-2. AAH; Amendment to Agreement; 1975 1-3. AAH; B 737 Crew Complement; 1971 1-4. Accident Investigation Committee; 1979 1-5. Active Grievances; 1966-1967 1-6. Age; Wage Analysis; 1974-1979 1-7. Air Safety Forum; 1955 1-8. Air Safety Forum; 1956 1-9. Air Safety Forum; 1957 1-10. Air Safety Forum; 1964 1-11. Air Safety Forum; 1968 1-12. Air Safety Forum; 1969 1-13. Air Safety Forum; 1972 1-14. Air Safety; General; 1967-1973 1-15. Air Safety Newsletter; 1958-1959 1-16. -

Title: Aviation Collection Reference Code: Mss-1969 Inclusive Dates

Title: Aviation Collection Reference Code: Mss-1969 Inclusive Dates: 1920 – ongoing Quantity: 1.2 cu. ft. total Location: BV 097-098 (0.8 cu. ft.) RC9, Sh. 007 & 015 (0.4 cu. ft.) Scope and Content: This collection contains general aviation documents on the local, state and national level as well as files on more specific subjects such as Hamilton Field and the EAA. In addition, this collection includes pamphlets from various airlines. Access and Use: No restrictions Language: English Notes: The collection was processed by Jeewon Schally, April 1993, and added to multiple times by Steve Daily and Kevin Abing. Arrangement: Folder Heading Box # File # Hamilton Field (1926) 1 1 Experimental Aircraft Association (EAA) (1971-1990) 1 2 Aviators 1 3 - Clara Adams (1939) - Charles A. Lindbergh (1920, 1927-1928) [Includes letter re Lindbergh’s Special Air Mail flight from Milwaukee-Chicago-St. Louis) - Richard Ira Bong - Douglas Corrigan Milwaukee 1 4 - "National Transportation Week" by The Milwaukee Journal (1966) - "On the Move" by The Milwaukee Sentinel (1966) - Badger Jaycee National Air Show Program (1966) - Jaycee Aero Space Exposition (1965) - Post card from Midwest Airways, Inc., depicting the "sister-ship" of Lindbergh's "Spirit of St. Louis," ca. 1927 - Newspaper clipping, "What Could Have Been," on Alfred Lawson, 1991 - "America's First Airliner," by Francis J. Allen, Air Classics, November 1984 - Program/menu honoring Capt. Wolfgang Von Gronau, 1932 - “Milwaukee County’s First Airport” by George Hardie - “Milwaukee’s First Airliner” by George Hardie - Membership Application/Information Card for Aero Club of Wisconsin - Program, Air Force Association Billy Mitchell Award, ca. -

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

G410020002/A N/A Client Ref

Solicitation No. - N° de l'invitation Amd. No. - N° de la modif. Buyer ID - Id de l'acheteur G410020002/A N/A Client Ref. No. - N° de réf. du client File No. - N° du dossier CCC No./N° CCC - FMS No./N° VME G410020002 G410020002 RETURN BIDS TO: Title – Sujet: RETOURNER LES SOUMISSIONS À: PURCHASE OF AIR CARRIER FLIGHT MOVEMENT DATA AND AIR COMPANY PROFILE DATA Bids are to be submitted electronically Solicitation No. – N° de l’invitation Date by e-mail to the following addresses: G410020002 July 8, 2019 Client Reference No. – N° référence du client Attn : [email protected] GETS Reference No. – N° de reference de SEAG Bids will not be accepted by any File No. – N° de dossier CCC No. / N° CCC - FMS No. / N° VME other methods of delivery. G410020002 N/A Time Zone REQUEST FOR PROPOSAL Sollicitation Closes – L’invitation prend fin Fuseau horaire DEMANDE DE PROPOSITION at – à 02 :00 PM Eastern Standard on – le August 19, 2019 Time EST F.O.B. - F.A.B. Proposal To: Plant-Usine: Destination: Other-Autre: Canadian Transportation Agency Address Inquiries to : - Adresser toutes questions à: Email: We hereby offer to sell to Her Majesty the Queen in right [email protected] of Canada, in accordance with the terms and conditions set out herein, referred to herein or attached hereto, the Telephone No. –de téléphone : FAX No. – N° de FAX goods, services, and construction listed herein and on any Destination – of Goods, Services, and Construction: attached sheets at the price(s) set out thereof. -

Domestic Airline Competition, Legacy Carrier Consolidation and the Rise of the Low-Cost Carrier

DOMESTIC AIRLINE COMPETITION, LEGACY CARRIER CONSOLIDATION AND THE RISE OF THE LOW-COST CARRIER A Thesis submitted to the Faculty of the Graduate School of Arts and Sciences of Georgetown University in partial fulfillment of the requirements for the degree of Master of Public Policy in Public Policy By Christian T. Ueland, B.S. Washington, DC April 13, 2017 Copyright 2017 by Christian T. Ueland All Rights Reserved ii The research and writing of this thesis is dedicated to my family and friends. Many thanks, Christian Ueland iii DOMESTIC AIRLINE COMPETITION, LEGACY CARRIER CONSOLIDATION AND THE RISE OF THE LOW-COST CARRIER Christian T. Ueland, B.S. Thesis Advisor: Terry Kennedy, Ph.D. ABSTRACT In the past eight years, the airline market in the United States has gone through a string of bankruptcies, some brought on by the severe economic recession in 2008 and 2009. These financial difficulties provided the impetus for four giant airline mergers, causing concern that market concentration had exceeded a healthy limit. This paper examines the competitive landscape of domestic air travel through an analysis of the relationship between airline fares and different levels of competition in the domestic airline market. Taking US Department of Transportation data from 2008 and 2016, I use an ordinary least squares (OLS) regression model to determine the relationship between average market fares and the type/number of competing airlines in each airport-pair market. The results for each year represent the strength of competitive forces, which I then compare to determine the manner in which competition has changed over the eight-year period. -

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

Airline Business & Law: Aircraft Acquisition, Finance & Leasing

Airline Business & Law: Aircraft Acquisition, Finance & Leasing Airline Business & Law (ASPL 614) McGill Institute of Air & Space Law Mark Lessard Pillsbury Winthrop Shaw Pittman LLP Table of Contents 1. Introduction: Aircraft as Investments 2. The Principal Players a. Aircraft Operators b. The Metal-Heads c. Sources of Finance 3. Aircraft Acquisition Process a. Selecting Equipment b. OEM Aircraft Purchase Agreements c. Pre-Delivery Payments and Financing d. Secondary Market 4. The Aircraft Leasing Industry a. Operating Leasing vs. Finance Leasing b. Asset Risk Arbitrage vs. Credit Arbitrage c. Depreciation Table of Contents 5. Aircraft Financing Methods a. Airline Credit vs. Asset Values b. Commercial Bank Lending c. Export Credit Agencies d. Capital Markets 6. Legal and Contractual Protections a. Perfecting Security in Aircraft b. Operation, Maintenance and Return Conditions c. Insurance 7. Default and Remedies a. Lease and Loan Defaults b. Airline Bankruptcies c. Foreclosure and Repossession d. Transition and Deficiency 8. Conclusion: Risk and Reward Introduction: Aircraft as Investments Q: What is the surest way to become a millionaire? A: Become a billionaire and start an airline… - Richard Branson Introduction: 10 Reasons for Investor Caution 1. Danger and liability = highly regulated industry (SAFETY!) 2. Variable operating costs, mainly driven by fuel and personnel 3. Highly mobile, crossing national borders and subject to expropriation 4. Expensive to maintain even when not in use 5. Value dependent on maintenance status, variant, upgrades, engine type, operating conditions, line number etc… 6. Highl y cycli cal i nd ust ry (GDP growth necessary b u t not suffi c ien t) 7. Long-dated asset (30 + years) 8. -

Appendix 25 Box 31/3 Airline Codes

March 2021 APPENDIX 25 BOX 31/3 AIRLINE CODES The information in this document is provided as a guide only and is not professional advice, including legal advice. It should not be assumed that the guidance is comprehensive or that it provides a definitive answer in every case. Appendix 25 - SAD Box 31/3 Airline Codes March 2021 Airline code Code description 000 ANTONOV DESIGN BUREAU 001 AMERICAN AIRLINES 005 CONTINENTAL AIRLINES 006 DELTA AIR LINES 012 NORTHWEST AIRLINES 014 AIR CANADA 015 TRANS WORLD AIRLINES 016 UNITED AIRLINES 018 CANADIAN AIRLINES INT 020 LUFTHANSA 023 FEDERAL EXPRESS CORP. (CARGO) 027 ALASKA AIRLINES 029 LINEAS AER DEL CARIBE (CARGO) 034 MILLON AIR (CARGO) 037 USAIR 042 VARIG BRAZILIAN AIRLINES 043 DRAGONAIR 044 AEROLINEAS ARGENTINAS 045 LAN-CHILE 046 LAV LINEA AERO VENEZOLANA 047 TAP AIR PORTUGAL 048 CYPRUS AIRWAYS 049 CRUZEIRO DO SUL 050 OLYMPIC AIRWAYS 051 LLOYD AEREO BOLIVIANO 053 AER LINGUS 055 ALITALIA 056 CYPRUS TURKISH AIRLINES 057 AIR FRANCE 058 INDIAN AIRLINES 060 FLIGHT WEST AIRLINES 061 AIR SEYCHELLES 062 DAN-AIR SERVICES 063 AIR CALEDONIE INTERNATIONAL 064 CSA CZECHOSLOVAK AIRLINES 065 SAUDI ARABIAN 066 NORONTAIR 067 AIR MOOREA 068 LAM-LINHAS AEREAS MOCAMBIQUE Page 2 of 19 Appendix 25 - SAD Box 31/3 Airline Codes March 2021 Airline code Code description 069 LAPA 070 SYRIAN ARAB AIRLINES 071 ETHIOPIAN AIRLINES 072 GULF AIR 073 IRAQI AIRWAYS 074 KLM ROYAL DUTCH AIRLINES 075 IBERIA 076 MIDDLE EAST AIRLINES 077 EGYPTAIR 078 AERO CALIFORNIA 079 PHILIPPINE AIRLINES 080 LOT POLISH AIRLINES 081 QANTAS AIRWAYS -

Airline Schedules

Airline Schedules This finding aid was produced using ArchivesSpace on January 08, 2019. English (eng) Describing Archives: A Content Standard Special Collections and Archives Division, History of Aviation Archives. 3020 Waterview Pkwy SP2 Suite 11.206 Richardson, Texas 75080 [email protected]. URL: https://www.utdallas.edu/library/special-collections-and-archives/ Airline Schedules Table of Contents Summary Information .................................................................................................................................... 3 Scope and Content ......................................................................................................................................... 3 Series Description .......................................................................................................................................... 4 Administrative Information ............................................................................................................................ 4 Related Materials ........................................................................................................................................... 5 Controlled Access Headings .......................................................................................................................... 5 Collection Inventory ....................................................................................................................................... 6 - Page 2 - Airline Schedules Summary Information Repository: -

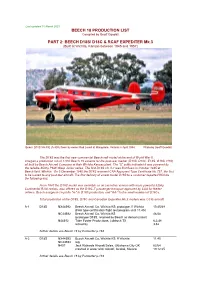

BEECH D18S/ D18C & RCAF EXPEDITER Mk.3 (Built at Wichita, Kansas Between 1945 and 1957)

Last updated 10 March 2021 BEECH 18 PRODUCTION LIST Compiled by Geoff Goodall PART 2: BEECH D18S/ D18C & RCAF EXPEDITER Mk.3 (Built at Wichita, Kansas between 1945 and 1957) Beech D18S VH-FIE (A-808) flown by owner Rod Lovell at Mangalore, Victoria in April 1984. Photo by Geoff Goodall The D18S was the first new commercial Beechcraft model at the end of World War II. It began a production run of 1,800 Beech 18 variants for the post-war market (D18S, D18C, E18S, G18S, H18), all built by Beech Aircraft Company at their Wichita Kansas plant. The “S” suffix indicated it was powered by the reliable 450hp P&W Wasp Junior series. The first D18S c/n A-1 was first flown in October 1945 at Beech field, Wichita. On 5 December 1945 the D18S received CAA Approved Type Certificate No.757, the first to be issued to any post-war aircraft. The first delivery of a new model D18S to a customer departed Wichita the following day. From 1947 the D18C model was available as an executive version with more powerful 525hp Continental R-9A radials, also offered as the D18C-T passenger transport approved by CAA for feeder airlines. Beech assigned c/n prefix "A-" to D18S production, and "AA-" to the small number of D18Cs. Total production of the D18S, D18C and Canadian Expediter Mk.3 models was 1,035 aircraft. A-1 D18S NX44592 Beech Aircraft Co, Wichita KS: prototype, ff Wichita 10.45/48 (FAA type certification flight test program until 11.45) NC44592 Beech Aircraft Co, Wichita KS 46/48 (prototype D18S, retained by Beech as demonstrator) N44592 Tobe Foster Productions, Lubbock TX 6.2.48 retired by 3.52 further details see Beech 18 by Parmerter p.184 A-2 D18S NX44593 Beech Aircraft Co, Wichita KS: ff Wichita 11.45 NC44593 reg. -

Global Aviation Holdings: the KERP Is Back

Portfolio Media. Inc. | 860 Broadway, 6th Floor | New York, NY 10003 | www.law360.com Phone: +1 646 783 7100 | Fax: +1 646 783 7161 | [email protected] Global Aviation Holdings: The KERP Is Back Law360, New York (August 06, 2012, 1:11 PM ET) -- In a recent decision[1] involving Global Aviation Holdings Inc. and its affiliated debtors (collectively, the “debtors”), the United States Bankruptcy Court for the Eastern District of New York granted the debtors' motion for approval of a key employee retention plan (the “KERP motion”) pursuant to Sections 363(b) and 503(c)(3) of Title 11 of the United States Code over the objections of both the United States Trustee for Region 2 (the “UST”) and the official committee of unsecured creditors (the “committee”). In the objections, the committee and the UST argued the debtors were seeking to pay bonuses to insiders without satisfying the requirements set forth in Section 503(c)(1) of the Bankruptcy Code. The committee and the UST also argued, that to the extent the key employee retention plan recipients turned out to be non-insiders, the debtors did not establish whether the proposed key employee retention plan payments were “justified by the facts and circumstances of the case” as required by Section 503(c)(3) of the Bankruptcy Code. The debtors operate two airlines: North American Airlines Inc. and World Airways Inc. From the outset of their bankruptcy cases, the debtors planned to move North American’s headquarters from JFK International Airport in Jamaica, N.Y., to World’s headquarters in Peachtree City, Ga., in order to consolidate operations.