A World of Entertainment Entertainment One Ltd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

RAPPORTO Il Mercato E L’Industria Del Cinema in Italia 2008

RAPPORTO Il Mercato e l’Industria del Cinema in Italia 2008 fondazione ente dello spettacolo RAPPORTO Il Mercato e l’Industria del Cinema in Italia 2008 In collaborazione con CINECITTA’ LUCE S.p.A. Con il sostegno di Editing e grafica: PRC srl - Roma fondazione ente Realizzazione a cura di: Area Studi Ente dello Spettacolo Consulenza: Redento Mori dello spettacolo Presentazione el panorama della pubblicistica italiana sul cinema, è mancata fino ad oggi una sintesi che consentisse una visione organica del settore e tale da misurare il peso di una realtà produttiva che per qualità e quantità rappresenta una delle voci più significative Ndell’intera economia. Il Rapporto 2008 su “Il Mercato e l’Industria del Cinema in Italia” ha lo scopo primario di colmare questa lacuna e di offrire agli operatori e agli analisti un quadro più ampio possibile di un universo che attraversa la cultura e la società del nostro Paese. Il Rapporto è stato realizzato con questo spirito dalla Fondazione Ente dello Spettacolo in collaborazione con Cinecittà Luce S.p.A., ed è il frutto della ricerca condotta da un’équipe di studiosi sulla base di una pluralità di fonti e di dati statistici rigorosi. Questo rigore si è misurato in alcuni casi con la relativa indeterminatezza di informazioni provocata dall’assenza di dati attualizzati (ad esempio, per i bilanci societari) e dalla fluidità di notizie in merito a soggetti che operano nel settore secondo una logica a volte occasionale e temporanea. La Fondazione Ente dello Spettacolo opera dal 1946. Finora si è conosciuto molto del cinema italiano soprattutto in termini di È una realtà articolata e multimediale, impegnata nella diffusione, promozione consumo. -

Eone Annual Report 2019

2019 Annual Report and Accounts Unlocking the power & value of creativity We are focused on building the leading talent-driven, platform- agnostic entertainment company in the world. Through our deep creative relationships we are able to produce the highest quality content for the world’s markets. We are powered by global reach, scale and local market knowledge to generate maximum value for this content. Strategic Report SR Governance G Financial Statements FS Unlocking the Unlocking the value of originality power & value p.10 of creativity Unlocking the power of creativity p.12 Strategic report Governance 02 At a glance 66 Corporate governance 04 Chairman’s statement 68 Board of Directors 06 Chief Executive Officer’s review 70 Corporate governance report 10 Unlocking the power 78 Audit Committee report & value of creativity Unlocking the 86 Nomination Committee report value of direction 20 Market Review 90 Directors’ Remuneration report p.14 22 Business Model 118 Directors’ report: 24 Strategy additional information 26 Key performance indicators Financial statements Business review 122 Independent auditor’s report 28 Family & Brands 127 Consolidated financial statements 36 Film, Television & Music 131 Notes to the consolidated financial statements Unlocking the 46 Finance review power of storytelling 51 Principal risks and uncertainties Visit our website: entertainmentone.com p.16 58 Corporate responsibility Unlocking the value of talent p.18 entertainmentone.com 1 AT A GLANCE Performance highlights Strong growth in underlying EBITDA -

Summit Guide Guide Du Sommet Guía De La Cumbre Contents/Sommaire/Sumario

New Frontiers for Creators in the Marketplace 9-10 June 2009 – Ronald Reagan Center – Washington DC, USA www.copyrightsummit.com Summit Guide Guide du Sommet Guía de la Cumbre Contents/Sommaire/Sumario Page Welcome 1 Conference Programme 3 What’s happening around the Summit? 11 Additional Summit Information 12 Page Bienvenue 14 Programme des conférences 15 Autres événements autour du sommet ? 24 Informations supplémentaires du sommet 25 Página Bienvenidos 27 Programa de las Conferencias 28 ¿Lo que pasa alrededor del conferencia? 38 Información sobre el conferencia 39 Page Sponsor & Advisory Committee Profiles 41 Partner Organization Profiles 44 Media Partner Profiles 49 Speaker Biographies 53 9-10 June 2009 – Ronald Reagan Center – Washington DC, USA New Frontiers for Creators in the Marketplace Welcome Welcome to the World Copyright Summit! Two years on from our hugely successful inaugural event in Brussels it gives me great pleasure to welcome you all to the 2009 World Copyright Summit in Washington, DC. This year’s slogan for the Summit – “New Frontiers for Creators in the Marketplace” – illustrates perfectly what we aim to achieve here: remind to the world that creators’ contributions are fundamental for cultural, economic and social development but also that creators – and those who represent them – face several daunting challenges in this new digital economy. It is imperative that we bring to the forefront of political debate the creative industries’ future and where we, creators, fit into this new landscape. For this reason we have gathered, under the CISAC umbrella, all the stakeholders involved one way or another in the creation, production and dissemination of creative works. -

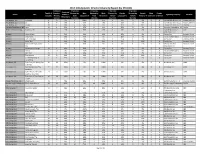

2017 DGA Episodic Director Diversity Report (By STUDIO)

2017 DGA Episodic Director Diversity Report (by STUDIO) Combined # Episodes # Episodes # Episodes # Episodes Combined Total # of Female + Directed by Male Directed by Male Directed by Female Directed by Female Male Female Studio Title Female + Signatory Company Network Episodes Minority Male Caucasian % Male Minority % Female Caucasian % Female Minority % Unknown Unknown Minority % Episodes Caucasian Minority Caucasian Minority A+E Studios, LLC Knightfall 2 0 0% 2 100% 0 0% 0 0% 0 0% 0 0 Frank & Bob Films II, LLC History Channel A+E Studios, LLC Six 8 4 50% 4 50% 1 13% 3 38% 0 0% 0 0 Frank & Bob Films II, LLC History Channel A+E Studios, LLC UnReal 10 4 40% 6 60% 0 0% 2 20% 2 20% 0 0 Frank & Bob Films II, LLC Lifetime Alameda Productions, LLC Love 12 4 33% 8 67% 0 0% 4 33% 0 0% 0 0 Alameda Productions, LLC Netflix Alcon Television Group, Expanse, The 13 2 15% 11 85% 2 15% 0 0% 0 0% 0 0 Expanding Universe Syfy LLC Productions, LLC Amazon Hand of God 10 5 50% 5 50% 2 20% 3 30% 0 0% 0 0 Picrow, Inc. Amazon Prime Amazon I Love Dick 8 7 88% 1 13% 0 0% 7 88% 0 0% 0 0 Picrow Streaming Inc. Amazon Prime Amazon Just Add Magic 26 7 27% 19 73% 0 0% 4 15% 1 4% 0 2 Picrow, Inc. Amazon Prime Amazon Kicks, The 9 2 22% 7 78% 0 0% 0 0% 2 22% 0 0 Picrow, Inc. Amazon Prime Amazon Man in the High Castle, 9 1 11% 8 89% 0 0% 0 0% 1 11% 0 0 Reunion MITHC 2 Amazon Prime The Productions Inc. -

Catalogue-2018 Web W Covers.Pdf

A LOOK TO THE FUTURE 22 years in Hollywood… The COLCOA French Film this year. The French NeWave 2.0 lineup on Saturday is Festival has become a reference for many and a composed of first films written and directed by women. landmark with a non-stop growing popularity year after The Focus on a Filmmaker day will be offered to writer, year. This longevity has several reasons: the continued director, actor Mélanie Laurent and one of our panels will support of its creator, the Franco-American Cultural address the role of women in the French film industry. Fund (a unique partnership between DGA, MPA, SACEM and WGA West); the faithfulness of our audience and The future is also about new talent highlighted at sponsors; the interest of professionals (American and the festival. A large number of filmmakers invited to French filmmakers, distributors, producers, agents, COLCOA this year are newcomers. The popular compe- journalists); our unique location – the Directors Guild of tition dedicated to short films is back with a record 23 America in Hollywood – and, of course, the involvement films selected, and first films represent a significant part of a dedicated team. of the cinema selection. As in 2017, you will also be able to discover the work of new talent through our Television, Now, because of the continuing digital (r)evolution in Digital Series and Virtual Reality selections. the film and television series industry, the life of a film or series depends on people who spread the word and The future is, ultimately, about a new generation of foreign create a buzz. -

Los Angeles Mission 2019

EC7.7 REPORT FOR ACTION Los Angeles Mission 2019 Date: August 13, 2019 To: Economic and Community Development Committee From: General Manager, Economic Development and Culture Wards: All SUMMARY On May 9, 2019, Mayor John Tory, alongside Deputy Mayor Michael Thompson, Councillor Paula Fletcher and key City staff led a delegation of 30 Toronto screen industry companies and organizations to Los Angeles to strengthen existing relationships and foster new ones with Los Angeles’ leading film, television and digital media companies in order to secure more investment in Toronto. The delegation, the largest to date for this mission, presented a unified voice for the jurisdiction and showcased Toronto’s commitment to growing the industry beyond the $2 billion it contributed to the city in 2018. Messaging from Mayor Tory, Deputy Mayor Thompson, Councillor Fletcher, City staff and delegates was focused on infrastructure growth, workforce development and customer service during this unprecedented golden age of content creation. This report provides an overview of the Mayor’s Los Angeles Mission including key activities and outcomes. RECOMMENDATIONS The General Manager, Economic Development and Culture recommends that: 1. City Council receive this report for information. FINANCIAL IMPACT The total cost of the trade mission was $152,822.42. The net cost after sponsorship contributions of $133,193.16 was $19,629.26. This amount was included in Economic Development and Culture's 2019 Approved Operating Budget, under the Film and Entertainment Industries activity. Future investments in Toronto by companies met in Los Angeles will result in benefits to the City. Los Angeles Mission 2019 Page 1 of 9 The Chief Financial Officer and Treasurer has reviewed this report and agrees with the financial impact information. -

Hasbro Annual Report 2020

Hasbro Annual Report 2020 Form 10-K (NASDAQ:HAS) Published: February 27th, 2020 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 29, 2019 Commission file number 1-6682 Hasbro, Inc. (Exact Name of Registrant As Specified in its Charter) Rhode Island 05-0155090 (State of Incorporation) (I.R.S. Employer Identification No.) 1027 Newport Avenue Pawtucket, Rhode Island 02861 (Address of Principal Executive Offices) (Zip Code) Registrant’s telephone number, including area code (401) 431-8697 Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol(s) Name of each exchange on which registered Common Stock HAS The NASDAQ Global Select Market Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ or No ☐. Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ or No ☒. Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Making Great Things Happen N G

M a k i Making great things happen n g g Corus Entertainment 2007 Annual Report r e a t t h i n g s h a p p e n C o r u s E n t e r t a i n m e n t I n c . 2 0 0 7 A n n u a l R e p o r t “Our Core Values give us clarity, focus and drive – we are proud to live them each day. ” Cheryl Bechtel, Controller, Corus Radio and a 2007 Corus Samurai Award winner Initiative Innovation Teamwork Accountability Knowledge We empower employees to We are committed to We believe the greatest We do what we say We believe in continuous make great things happen creative thinking that leads value is realized when we we’ll do – no excuses learning and the sharing of to breakthrough ideas and work together our insights and ideas superior results www.corusent.com Revenues Segment profit (in millions) (in millions) 768.7 240.9 726.3 666.8 683.1 214.1 643.9 195.3 165.3 90.4 0304050607 0304050607 Financial highlights (millions of Canadian dollars except per share amounts) 2007 2006 2005 2004 2003 REVENUES 768.7 726.3 683.1 666.8 643.9 SEGMENT PROFIT 1 240.9 214.1 195.3 90.4 165.3 NET INCOME (LOSS) 107.0 35.5 71.1 (23.1) 40.0 EARNINGS (LOSS) PER SHARE Basic $2.53 $0.84 $1.66 $(0.54) $0.94 Diluted $2.47 $0.82 $1.65 $(0.54) $0.94 Total assets 1,937.0 1,842.2 1,928.4 1,871.9 1,940.6 Total long-term financial liabilities 673.8 666.4 660.4 690.9 693.5 CASH DIVIDENDS DECLARED PER SHARE Class A Voting $1.00250 $0.4525 $0.065 $0.04 – Class B Non-Voting $1. -

Item List for Location ZE for the Item Groups You Selected

10:14 AM 1/24/2018 Item List for Location ZE For The Item Groups You Selected Call Number Title Author Publisher Pub. Date Barcode 613.7 Bey (VHS) Beyond basic yoga for dummies Dragonfly Productions[unknown] Inc. 33246001206861 613.7046 AM (DVD) AM PM yoga for beginners Lions Gate Entertainment,[2012] 33246002326791 941.83508 Lew Secret child : Lewis, Gordon. Harper Element, [2015] 33246002313112 (ON TRACE) BBC DVD FICMI-5, MI-5 volume (s.7) 07 BBC Video ; [2010] 33246002010338 (ON TRACE) DVD FIC Eight8 movie family adventure collection Echo Bridge Home Entertainment,[2013] 33246002290732 (ON TRACE) DVD FIC NothiNothing in common Tri Star, [2002] 33246001431956 (ON TRACE) DVD FIC RedRed Magnolia Home Entertainment,[2008] 33246002179083 (ON TRACE) DVD FIC StarStar trek XI Paramount, [2009] 33246001904911 BBC DVD FIC Above (s.2)Above suspicion, set 2 ITV Studios Home Entertainment[2012] ;33246002162659 BBC DVD FIC Agath (M. Agatha7 & 12) Christie's Marple, set 1, volume 2 : A&E Television Networks[2006] : 33246001875970 BBC DVD FIC Agath (M. Agatha8 & 9) Christie's Marple, set 1, volume 1 : A&E Television Networks[2006] : 33246001875962 BBC DVD FIC Agath (T. 2)Agatha Christie's Partners in Crime, set 2 distributed exclusively[2004]. by Acorn Media,33246002226959 BBC DVD FIC Balle Ballet shoes BFS Video, [2000] 33246001613892 BBC DVD FIC Berke Berkeley square, the complete series / BFS, [2011] 33246002256402 BBC DVD FIC Broad (s.1)Broadchurch, season 1 / Entertainment One (New[2014] Releases), 2013.33246002277978 BBC DVD FIC Broke (s. 3)The Brokenwood mysteries, series 3 Acorn, [2017] 33246002396141 BBC DVD FIC Danie Daniel Deronda BBC Video ; [2003] c2002.33246001980986 BBC DVD FIC Death (s.2)Death in paradise, season 2 BBC ; [2013] 33246002248862 BBC DVD FIC Death (s.3)Death in paradise, season 3 BBC Worldwide., [2014] 33246002356111 BBC DVD FIC Death (s.5)Death in paradise, season 5 BBC Video, [2016] 33246002313419 BBC DVD FIC Downt (DowntonDownton Abbey Abbey, s. -

UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 __________________ FORM 10-Q __________________ (Mark One) ☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended June 27, 2021 or ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission File Number 1-6682 __________________ HASBRO, INC. (Exact name of registrant as specified in its charter) Rhode Island 05-0155090 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.) 1027 Newport Avenue Pawtucket, Rhode Island 02861 (Address of Principal Executive Offices) (Zip Code) (401) 431-8697 Registrant's telephone number, including area code Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol(s) Name of each exchange on which registered Common Stock, $0.50 par value per share HAS The NASDAQ Global Select Market Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [x] No [ ] Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). -

MPLC Studioliste Juli21-2.Pdf

MPLC ist der weltweit grösste Lizenzgeber für öffentliche Vorführrechte im non-theatrical Bereich und in über 30 Länder tätig. Ihre Vorteile + Einfache und unkomplizierte Lizenzierung + Event, Title by Title und Umbrella Lizenzen möglich + Deckung sämtlicher Majors (Walt Disney, Universal, Warner Bros., Sony, FOX, Paramount und Miramax) + Benutzung aller legal erworbenen Medienträger erlaubt + Von Dokumentar- und Independent-, über Animationsfilmen bis hin zu Blockbustern ist alles gedeckt + Für sämtliche Vorführungen ausserhalb des Kinos Index MAJOR STUDIOS EDUCATION AND SPECIAL INTEREST TV STATIONS SWISS DISTRIBUTORS MPLC TBT RIGHTS FOR NON THEATRICAL USE (OPEN AIR SHOW WITH FEE – FOR DVD/BLURAY ONLY) WARNER BROS. FOX DISNEY UNIVERSAL PARAMOUNT PRAESENS FILM FILM & VIDEO PRODUCTION GEHRIG FILM GLOOR FILM HÄSELBARTH FILM SCHWEIZ KOTOR FILM LANG FILM PS FILM SCHWEIZER FERNSEHEN (SRF) MIRAMAX SCM HÄNSSLER FIRST HAND FILMS STUDIO 100 MEDIA VEGA FILM COCCINELLE FILM PLACEMENT ELITE FILM AG (ASCOT ELITE) CONSTANTIN FILM CINEWORX DCM FILM DISTRIBUTION (SCHWEIZ) CLAUSSEN+PUTZ FILMPRODUKTION Label Anglia Television Animal Planet Productions # Animalia Productions 101 Films Annapurna Productions 12 Yard Productions APC Kids SAS 123 Go Films Apnea Film Srl 20th Century Studios (f/k/a Twentieth Century Fox Film Corp.) Apollo Media Distribution Gmbh 2929 Entertainment Arbitrage 365 Flix International Archery Pictures Limited 41 Entertaiment LLC Arclight Films International 495 Productions ArenaFilm Pty. 4Licensing Corporation (fka 4Kids Entertainment) Arenico Productions GmbH Ascot Elite A Asmik Ace, Inc. A Really Happy Film (HK) Ltd. (fka Distribution Workshop) Astromech Records A&E Networks Productions Athena Abacus Media Rights Ltd. Atlantic 2000 Abbey Home Media Atlas Abot Hameiri August Entertainment About Premium Content SAS Avalon (KL Acquisitions) Abso Lutely Productions Avalon Distribution Ltd. -

Oppdatert Liste Samarbeidspartnere 2015

OPPDATERT LISTE Baby Cow Productions Cannon Pictures SAMARBEIDSPARTNERE Bandai Visual Co. Ltd Captured Light Distribution LLC Banijay International Ltd Carey Films Ltd 2015/2016 Bankside Films Cargo Film & Releasing Bard Entertainment Carnaby Sales and Distribution Ltd 12 Yard Productions Bardel Distribution Carrere Group D.A. 2929 Entertainment LLC BBC Worldwide Cartoon Network 3DD Entertainment BBL Distribution Inc. Cartoon One 9 Story Enterprises BBP Music Publishing c/o Black Bear Caryn Mandabach Productions A&E Channel Home Video Pictures Casanova Multimedia Abduction Films Ltd Beacon Communications Cascade Films Pty Ltd Acacia Becker Group Ltd. Castle Hill Productions ACC Action Concept Cinema GmbH & Beijing Asian Union Culture and Media Cats and Docs SAS Co. KG Investment CCI Releasing ACI Bejuba Entertainment CDR Communications Acorn Group Bell Phillip Television Productions Inc. Celador Productions ACORN GROUP INC Benaroya Pictures Celestial Filmed Entertainment Ltd. Acorn Media Bend it Like Beckham Productions Celluloid Dreams Actaeon Films Bentley Productions Celsius Entertainment Action Concept Berlin Animation Film Gmbh Celsius Film Sales Action Concept Film und Best Film and Video Central Independent Television Stuntproduktion GmbH Best Picture Show Central Park Media Action Image GmbH & Co. KG Betty TV Channel 4 Learning Adness Entertainment Co. Ltd. Beyond International Ltd Chapter 2 Adult Swim Productions Big Bright House of Tunes Chatsworth Enterprises After Dark Films Big Idea Entertainment Children's Film And Television Ager Film Big Light Productions Foundation AIM Group LLC. Big Talk Productions Chorion Plc Akkord Film Produktion GmBH Billy Graham Evangelistic Association / Christian Television Association Alain Siritzky Productions World Wide Pictures Ciby 2000 Alameda Films Bio Channel Cineflix International Media Albachiara S.r.l.