Notice Concerning Property Acquisition and Disposition

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vision for Coastal Area

In Formulating the Vision Vision for Coastal Area About 100 years ago, the Kawasaki coastal area was created by Soichiro - The Ideal Image of Kawasaki Coastal Area - Asano, the pioneer of entrepreneurs, through landfilling projects and corporate invitations and has made great strides in the post-war high economic growth period by supporting the Japanese economy. After that, in the process of experiencing the hollowing out of industry due to environmental issues and globalization, the entire area, mainly compa- nies, has repeatedly replaced the old with the new and has progressively advanced the R&D function and accumulation of logistics facilities. At present, efforts to strengthen the competitiveness of key industries and business collaborations utilizing the strength of an industrial complex have emerged. In addition, the Tonomachi International Strategic Base, King Skyfront, was formed, and efforts using hydrogen were developed. The movement to create new industries is also accelerating. For the sustainable development of the Kawasaki coastal area even in the continued turbulent world and aiming not only to support citizen services and employment as the center of the creation of a strong indus- trial city but also to become a global model area as an industrial base, we have formulated Vision For Coastal Area looking ahead 30 years with various related parties, including companies, this time. In the Vision, as the ideal image in 30 years that the Kawasaki coastal area is aiming for, industries that realize the affluence are in full play as required in a new era and an area where diverse human resources and cultures resonate by utilizing the climate of the Kawasaki coastal area were set. -

Inage Kaigan Area 5 Chiba Minato Area 2 Makuhari New Urban Center

1 Chiba City 市内全域略図 A B C D E Katsutadai Keisei-oowada Sakura Sakura Takanodai CC Ibaraki Sawara Yachiyodai Saitama Katsutagawa River Tsukuba Express Costco Wholesale Kashiwa Japan 2 幕張新都心エリア Higashikanto Express way Narita Makuhari New Urban Center Area Choshi Matsudo Narita Sakura Airport A B C D Yokodo Akihabara Kaihin To Tokyo 1 1 Shinjuku Keiyo Express way Chiba Togane Express way makuhari Naruto Tokyo N AEON MALL Chiba Tokyo Maihama Chiba MAKUHARI-SHINTOSHIN Soga City Mimomi Miharuno Strawberry Farm To Tokyo Hamada Nokyo-maeHaneda Oami Keisei Main Line Monoi Driver's License Center To Tokyo Airport Kotehasidanchi Kanagawa Tokyo Bay Aqualine Keisei-Ookubo Iriguchi Yotsukaido IC Naganuma-Funabashi road Hanashima koen (park) Kayabasidai Chiba Makuhari Messe Parking Area Kashiwai Leisure Farm Yokohama Yotsukaido-Kamishizu road Tateyama Express way Sapporo License Center Tenpuku-ji (Temple) Kisarazu Railway Naha 1 Hamadagawa green space Tanjyo Farm Road Toyosuna Amadodai Higashi Kanto Expressway Messe Ohashi Furusato Farm Otaki Ohara Choin-ji Hamadagawa River Seiko Instruments (Temple) Kotehashi Onsui Pool Kazusa To Tokyo Kameyama Onjuku Anagawa-Amado road Anagawa-Amado Makuharihongo road Anagawa-Amado Chiba Kita Police Station Hamadagawa-dori St. ACCESS Hanamigawa River MARINES MUSEUM Tokyo Gas Makuhari PA Chibakita IC Katsuura Fujitsu SHARP FAMY INN MAKUHARI Tokyo STARTS To Tokyo Takeishi IC Awa Kyoto KITZ Chiba H Kamogawa Osaka Nagoya Kotehasi Kaizuka Shimada Family's Buildings Fukuoka Koyasu-Jinja (shell mound) Park nakase 2 (Shrine) Naganuma (Late Edo Period) Business-dori St. Business-dori Houdou-ji (Temple) (National historic site) Tateyama QVC Marine Field Keiyo Road Yotsukaido Cannon MJ Komamori-Jinja (Shrine) Miyanogi Sports Center Messe-odori St. -

The Fiscal Conditions and Prefectural Bonds of Chiba Prefecture

IR document The Fiscal Conditions and Prefectural Bonds of Chiba Prefecture October 2014 Chiba Prefecture Table of Contents Page 1. Outline of Chiba Prefecture (1) State of Population in Chiba Prefecture ・・・ 2 (2) Economical State in Chiba Prefecture Viewed from Report on ・・・ 3 Prefectural Accounts (3) Characteristics of Industry in Chiba Prefecture ・・・ 4 (4) Chiba Prefecture in the National Ranking ・・・ 5 2. Status of Budget and Accounts (1) General Account Budget (Revenue) After Revision in September, ・・・ 6 FY2014 (2) General Account Budget (Expenditure) After Revision in September, ・・・ 7 FY2014 (3) Major Projects in the Original Budget ・・・ 8 (4) Balance of Settled General Accounts ・・・ 10 (5) [Revenue Related] Prefectural Tax Revenue ・・・ 11 (6) [Expenditures] Transition of Personnel Expenses ・・・ 12 (7) Transition of Fund Balance ・・・ 13 (8) Transition of Prefectural Bonds Issuance ・・・ 14 (9) Transition of Outstanding of Prefectural Bonds ・・・ 15 (10)Financial Indicators (General Account) ・・・ 16 (11)Overview of FY2013 General and Special Accounts ・・・ 18 (12)Local Public Corporations Management Results ・・・ 19 (13)Joint Third Sectors Results and Prefecture Financial Support ・・・ 20 (14)FY 2012 Balance Sheet ・・・ 21 3. Administrative and Financial Reforms Made So Far 22 4. Chiba Prefecture Financial Soundness Plan (FY2013 - 24 FY2016) 5. Chiba Prefectural Bonds (1) Prefectural bonds issuance by funds (General Account) ・・・ 26 (2) Prefectural bonds outstanding by funds (General Account) ・・・ 26 (3) Prefectural bonds outstanding by account ・・・ 27 (4) FY2014 Public Offering Bond Issuance Plan ・・・ 27 (5) Prefectural Bond Redemption ・・・ 28 (6) Security of Local Municipal Bonds ・・・ 29 1. Outline of Chiba Prefecture Although Chiba Prefecture is located in the national capital region, it is blessed with rich nature, and has a lot of treasures and potential, including Narita International Airport as the gateway to the sky in Japan. -

Measurement of Radiation Dose for Air in the Ports Measurement Of

Measurement of Radiation Dose for Air in the Ports (the Pacific side of Northeast Japan) http://www.mlit.go.jp/kowan/kowan_fr1_000041.html Annual exposure Measurement points H29.1.12 H29.1.19 H29.1.26 calculation Distance from Fukushima Daiichi Nuclear Power Station ① Port of Tokyo Oi Wharf 0.03 μSv/h 0.05 μSv/h 0.05 μSv/h = 0.00005 mSv/h 0.44 mSv Port of Honmoku Wharf ② 0.04 μSv/h 0.04 μSv/h 0.04 μSv/h = 0.00004 mSv/h 0.35 mSv Yokohama (BC gate) Kawasaki Environment Synthesis ③ Port of Kawasaki Laboratory 0.02 μSv/h 0.02 μSv/h 0.02 μSv/h = 0.00002 mSv/h 0.18 mSv ⑩ <4km from the port> (AM8:00) (AM8:00) (AM8:00) Chiba Prefectural Port of Chiba Environmental Research Center μSv/h μSv/h μSv/h = 0.00003 mSv/h mSv ④ 0.03 (AM8:00) 0.03 0.03 0.26 <9km from the port> (AM8:00) (AM8:00) ⑤ Port of Kashima Bureau of Port of Kashima - μSv/h - μSv/h - μSv/h = - mSv/h - mSv (AM8:00) (AM8:00) (AM8:00) ⑥ Port of Onahama Fujiwara Wharf - μSv/h - μSv/h - μSv/h = - mSv/h - mSv ⑨ (AM) (AM) (AM) ⑧ ⑦ Port of Souma No.2 Wharf - μSv/h - μSv/h - μSv/h = - mSv/h - mSv (AM) (AM) (AM) ⑦ Port of Sendai- μSv/h μSv/h μSv/h = - mSv/h mSv Fukushima Daiichi ⑧ shiogama Takasago Container Terminal - - - - Nuclear Power Station 100km ⑥ Port of μSv/h - μSv/h μSv/h = - mSv/h mSv ⑨ Ishinomaki Nakajima Wharf - - - 150km Research Institute for Environmental Sciences ⑩ Port of Kuji 0.02 μSv/h 0.02 μSv/h 0.02 μSv/h = 0.00002 mSv/h 0.18 mSv and Public Health (AM) (AM) (AM) 200km ⑤ ① ①Source: Bureau of Port and Harbor Tokyo Metropolitan Government ③ ④ http://www.kouwan.metro.tokyo.jp/jishin_kouwankyoku_oshirase/measurement/> -

Ports of Japan

PORTS OF JAPAN Report Details of Japanese Ports and their value in Submitted to Sir Pacific ocean Sohail Bashir Author: S.M.Misbah Ce-063 1 PORTS OF JAPAN Table of Content 1. Introduction 2 2. Background 3 3. Port Infrastructure 5 4. Details of Major Japanese Ports 6 5. References 19 Ports of Japan 2 Introduction: Japan is a long, narrow island nation in East Asia. Located in the Pacific Ocean, it lies to the east of the Sea of Japan, China, North Korea, South Korea and Russia, stretching from the Sea of Okhotsk in the north to the East China Sea and Taiwan in the south. Japan has a large industrial capacity, and is home to some of the largest and most technologically advanced producers of motor vehicles, electronics, machine tools, steel and nonferrous metals, ships, chemical substances, textiles, and processed foods. Agricultural businesses in Japan cultivate 13 percent of Japan's land, and Japan accounts for nearly 15 percent of the global fish catch. Japan's exports amounted to US$4,210 per capita in 2005. Its main imports are machinery and equipment, fossil fuels, foodstuffs (in particular beef), chemicals, textiles and raw materials for its industries. By market share measures, domestic markets are the least open of any OECD country. Junichiro Koizumi's administration began some pro-competition reforms, and foreign investment in Japan has soared. Trade with other nations stimulated cultural development in Japan, and the limited amount of space prompted a national policy establishing foreign trade early on. The development of ports and harbors has therefore been particularly important to the economy, and the Japanese government plays a leading role in maintaining the country's ports, as well as its shipping. -

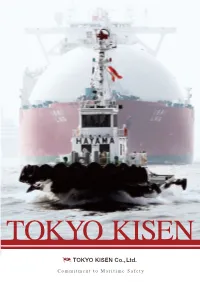

Commitment to Maritime Safety Greetings

TOKYO KISEN Commitment to Maritime Safety Greetings Ensuring Maritime Safety: Tokyo Kisen’s constant mission. Tokyo Kisen, as a towage company, considers maritime safety to be its Tokyo Kisen’s Service Areas primary mission. Since first being established in 1947 as Japan’ s first commercial tugboat operator we have been assisting with the navigational Port of Tokyo safety of ships throughout Tokyo Bay, the center of Japanese maritime transportation, and one of the busiest global sea traffic areas. Our company services are available 24 hours every day of the year in Port of Chiba thereby flexibly accommodating the maritime safety needs of clients. We provide a wide range of towage services from harbor towage in which we Port of Kawasaki assist ships to safely berth and unberth at ports in Tokyo Bay, an escort tug service that safeguards the routes of large ships transporting hazardous materials along the Uraga Channel-Nakanose route, a Port of Yokohama disaster-prevention service that includes berth patrols and providing assistance with oil-spills, and emergency support services that include Nakanose route Port of Kisarazu immediately responding to the need for ships to be rescued and life-saving operations in the event of an accident occurring in Tokyo Bay and the surrounding area. Fundamental to our business is undertaking to Port of Yokosuka fulfill any possible request involving tugboats. Tugboats equipped with state-of-the-art technology as well as Uraga channel route extremely experienced crews allow us to perform these towage services in a safe and reliable manner. Our onshore support system also enables swift action to be taken in the event of emergencies and disasters at sea. -

Eco Airport Eco Airport Eco Airport

English 2017 What is ECO AIRPORT As an eco-airport, ■Becoming an Airport with the World's Highest Standards Narita International Airport has served a total of 1 billion passengers as of July 2017. Thanks Narita Airport will promote to the understanding and cooperation of many people including local residents, Narita Airport has played signicant roles in Japan’s economic development and international exchanges as an international hub airport that places the highest priority on safety while our environmental initiatives responding to international aviation demand in the Tokyo Metropolitan Region. As founder and administrator of the airport, Narita International Airport Corporation (NAA) looking to the future pursues to achieve stable airport operations with the world’s highest standards while providing high-quality service to passengers, reinforcing aviation networks, and taking environmental countermeasures and deepening the partnership with the local community for coexistence with the aim of becoming an airport with the world’s highest standards. We are currently making preparations at Narita Airport to welcome, with the highest levels of hospitality, athletes and others traveling for the 2020 Tokyo Olympic and Paralympic Games, which will attract global attention. To respond to aviation demand in the Tokyo metropolitan area, which is expected to continue increasing even after the Olympics, we are working in collaboration with local residents and other stakeholders regarding the further functional improvements at Narita Airport, such as the construction of an additional runway. We will respond in a timely manner to changes in the airport environment and take measures to achieve greater harmony and mutual prosperity between the airport and local communities. -

Nissin Corporation Was Founded in 1938 As a Domestic In-Harbor Transport Dec

Corporate Profile Brief History of the Company Nissin Welcomes You Nissin Corporation was founded in 1938 as a domestic in-harbor transport Dec. 1938 Established as Nissin Transport Co., Ltd. company in Yokohama, Japan’s main gateway to the world. It has since Mar. 1946 Changed company name to Nissin Trading Co., Ltd. expanded to cater to the logistics needs of the Ports of Kobe, Osaka and Nov. 1948 Established Kobe Branch Office Chiba. As Japan developed into a world economic power and its Jan. 1950 Changed company name to Nissin Transportation & Warehousing Co., Ltd. transportation needs became more advanced and complex, Nissin faced the Apr. 1950 Listed on First Section of the Tokyo Stock Exchange. rising need to improve both its systems and facilities. In 1968 it began Apr. 1950 Harbor transportation began in port of Yokohama. offering comprehensive global logistics services, an entirely new category of Nov. 1954 Established Tokyo Branch Office service, and it now operates in Japan and 23 other countries. May 1958 Established Osaka Branch Office Aug. 1961 Completed Kanagawa Pier and started operations as Nissin Pier Our name, Nissin, is derived from the Chinese literature classic “Great Apr. 1969 Established Chiba Branch Office Learning,” combining two characters meaning ‘day’ and ‘new’ to reflect the May 1973 Listed on First Section of the Osaka Stock Exchange company spirit of encouraging effort to improve daily. This spirit drives Nissin Dec. 1973 Established Nissin International Transport U.S.A. as local subsidiary in Los Angeles, U.S.A. to respond to change proactively so tomorrow is always better than today as Jan. -

CHIBA PREFECTURE Latest Update: August 2013

www.EUbusinessinJapan.eu CHIBA PREFECTURE Latest update: August 2013 Prefecture’s flag Main City: Chiba Population: 6,192,000 people, ranking 6/47 prefecture (2013) [1] Area: 5,156.15 km² [2] Geographical / Landscape description Chiba Prefecture is located in the Kanto region and the Greater Tokyo Area. With the exception of the large-scale Keiyo Industrial Zone in the northeast, the entirety of the coast of Chiba Prefecture is protected as two quasi-national parks and one prefectural natural park under the national park system of Japan. As of 1 April 2012, 6% of the total land area of the prefecture was designated as Natural Parks. [2] Climate Chiba Prefecture has a warm oceanic climate that is mild in winter and relatively cool in summer, as it is surrounded on three sides by the sea. [2] Time zone GMT +7 in summer (+8 in winter) International dialling code: 0081 Recent history, culture Chiba's culture flourished in particular under the Edo Shogunate (1603-1867), when the centre of power of Japan lay just next to Chiba. Sawara (presently part of Katori City), a commerce town, prospered so much from the flow of goods along the Tonegawa River that it was said to rival Edo. Against this backdrop, Chiba made its own mark on Japanese culture. [3] Economic overview Chiba Prefecture has the advantage of being located adjacent to Tokyo, the national capital, and it is the site of both Narita International Airport, which handles international airline passengers and freight from around the world, and the Port of Chiba, which boasts one of the largest volume of freight handled in Japan. -

Tohoku Earthquake & Tsunami Event Recap Report

Impact Forecasting Tohoku Earthquake & Tsunami Event Recap Report August 30, 2011 Proprietary & Confidential Table of Contents Executive Summary 2 Introduction 3 Seismological Recap 4 Human Casualty Effects 8 Tsunami Impacts 9 Property Effects 13 Commercial Effects 17 Utility Effects 19 Energy Effects 20 Nuclear Power Plants 21 Infrastructure Effects 23 Economic Impacts 26 Appendix A: Regions and prefectures of Japan 27 Appendix B: Lists of historical earthquakes since 1900 28 Appendix C: Additional Japan tsunami inland inundation maps 29 Appendix D: Additional recorded tsunami wave heights 30 Appendix E: Additional photos from IF on-site visit 31 Appendix F: Glossary of earthquake and tsunami terminology 34 Impact Forecasting | Tohoku Earthquake and Tsunami Event Recap Report 1 Executive Summary A mega-earthquake and tsunami struck the northeastern coast of Japan on March 11, 2011, killing and injuring thousands of people and causing extensive damage. As of this writing, the death toll was 15,776 and expected to possibly reach 20,000. At least 5,929 others were injured and more than 4,225 people were officially listed as missing. The main magnitude-9.0 earthquake struck at 2:46 PM local time (5:46 UTC) with an epicenter 129 kilometers (80 miles) east of Sendai, Japan. The Tohoku earthquake is the largest known tremor to have struck Japan. This mega-thrust event occurred in an area where the Pacific Plate is thrust beneath the Eurasian and North American Plates, and ruptured an area 400 kilometers (249 miles) long and 50 kilometers (30 miles) wide. The ensuing tsunami was triggered as typically seen in cases of subduction zone events. -

March Weekender Full.Pdf

tokyo weekenderJapan’s premier English language magazine MARCH 2013 CHIBA is The GreAT outdoors riGht neXT door? J-POP THE CURSE OF IDOL CULTURE TRAVEL & ART NAoshiMA And the inlAnd ISLANDS + setouchi triennAle RETURNS ALSO IN THIS ISSUE: Top news from Asia Daily Wire, “Rami-chan” looks forward to the new baseball season, movies, events and more... Tokyo weekender- subat ilan.pdf 1 24.01.2013 10:39 C M Y CM MY CY CMY K Tokyo weekender- subat ilan.pdf 1 24.01.2013 10:39 C M Y CM MY CY CMY K Away on business or leisure, find comfort in a familiar environment — luxurious in Oakwood Premier, elegant in Oakwood Residence or stylish in Oakwood Apartments. Come home to the ease of Oakwood living in Asia. Oakwood offers a choice of 7 hot spot locations in Asia's most cosmopolitan city, Tokyo — Aoyama, Akasaka, Azabujyuban, Midtown, Roppongi and Shirokane. For further details, please visit our website or call (81-3) 5412 3131 or email us [email protected]. March 2013 CONTENTS 18 NOKOGIRI-YAMA Hiking up the saw tooth mountain, just over the Aqua-Line into Chiba. 14 33 35 CHIBA’S SURPRISES SETOUCHI TRIENNALE AGENDA Festivals, surfing spots, sake, peanuts and A world class art festival on Naoshima The best goings on this month, including more than we ever thought there was. and surrounding islands. an intimate gig from Grimes (above). 9 Asia Daily Wire 22 Kamogawa Style 38 Baseball A roundup of all the top APAC news of the This was the first place in Japan to see Ahead of the 2013 season we met with past month. -

Circular Dated 6 April 2018

CIRCULAR DATED 6 APRIL 2018 MAPLETREE GREATER CHINA COMMERCIAL TRUST THIS CIRCULAR IS IMPORTANT AND (Constituted in the Republic of Singapore pursuant to a Trust Deed dated 14 February 2013 REQUIRES YOUR IMMEDIATE ATTENTION (as amended)) CIRCULAR TO UNITHOLDERS IN RELATION TO THE PROPOSED ACQUISITION OF THE JAPAN PORTFOLIO (COMPRISING SIX FREEHOLD COMMERCIAL PROPERTIES) Singapore Exchange Securities Trading Limited (the “SGX-ST”) takes may not be offered or sold within the United States except pursuant no responsibility for the accuracy of any statements or opinions made, to an exemption from, or transactions not subject to, the registration or reports contained, in this Circular. If you are in any doubt as to the requirements of the Securities Act and in compliance with any applicable action you should take, you should consult your stockbroker, bank state securities laws. The Manager does not intend to conduct a public manager, solicitor, accountant or other professional adviser immediately. offering of any securities of MGCCT in the United States. If you have sold or transferred all your units in Mapletree Greater China IMPORTANT DATES AND TIMES FOR UNITHOLDERS Commercial Trust (“MGCCT”, and the units in MGCCT, the “Units”), you should immediately forward this Circular, together with the Notice of Last date and time for 21 April 2018 (Saturday) at Extraordinary General Meeting and the accompanying Proxy Form in lodgement of Proxy Forms 3.30 p.m. this Circular, to the purchaser or transferee or to the bank, stockbroker or other agent through whom the sale or transfer was effected for Date and time of 24 April 2018 (Tuesday) at onward transmission to the purchaser or transferee.