Haversham Holdings

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

DATABANK INSIDE the CITY SABAH MEDDINGS the WEEK in the MARKETS the ECONOMY Consumer Prices Index Current Rate Prev

10 The Sunday Times November 11, 2018 BUSINESS Andrew Lynch LETTERS “The fee reflects the cleaning out the Royal Mail Send your letters, including food sales at M&S and the big concessions will be made for Delia’s fingers burnt by online ads outplacement amount boardroom. Don’t count on it SIGNALS full name and address, supermarkets — self-service small businesses operating charged by a major company happening soon. AND NOISE . to: The Sunday Times, tills. These are hated by most retail-type operations, but no Delia Smith’s website has administration last month for executives at this level,” 1 London Bridge Street, shoppers. Prices are lower at such concessions would been left with a sour taste owing hundreds of says Royal Mail, defending London SE1 9GF. Or email Lidl and other discounters, appear to be available for after the collapse of Switch thousands of pounds to its the Spanish practice. BBC friends [email protected] but also you can be served at businesses occupying small Concepts, a digital ad agency clients. Delia, 77 — no You can find such advice Letters may be edited a checkout quickly and with a industrial workshop or that styled itself as a tiny stranger to a competitive for senior directors on offer reunited smile. The big supermarkets warehouse units. challenger to Google. game thanks to her joint for just £10,000 if you try. Eyebrows were raised Labour didn’t work in the have forgotten they need Trevalyn Estates owns, Delia Online, a hub for ownership of Norwich FC — Quite why the former recently when it emerged 1970s, and it won’t again customers. -

STOXX UK 180 Last Updated: 02.10.2017

STOXX UK 180 Last Updated: 02.10.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) GB0005405286 0540528 HSBA.L 040054 HSBC GB GBP Y 171.2 1 1 GB0002875804 0287580 BATS.L 028758 BRITISH AMERICAN TOBACCO GB GBP Y 121.6 2 2 GB00B03MLX29 B09CBL4 RDSa.AS B09CBL ROYAL DUTCH SHELL A GB EUR Y 115.3 3 3 GB0007980591 0798059 BP.L 013849 BP GB GBP Y 107.0 4 4 GB0009252882 0925288 GSK.L 037178 GLAXOSMITHKLINE GB GBP Y 83.1 5 5 GB0009895292 0989529 AZN.L 098952 ASTRAZENECA GB GBP Y 71.2 6 9 GB0002374006 0237400 DGE.L 039600 DIAGEO GB GBP Y 70.1 7 6 GB00B10RZP78 B10RZP7 ULVR.L 091321 UNILEVER PLC GB GBP Y 64.2 8 7 GB00BH4HKS39 BH4HKS3 VOD.L 071921 VODAFONE GRP GB GBP Y 63.2 9 8 GB0008706128 0870612 LLOY.L 087061 LLOYDS BANKING GRP GB GBP Y 55.3 10 12 GB0007099541 0709954 PRU.L 070995 PRUDENTIAL GB GBP Y 52.4 11 11 GB00B24CGK77 B24CGK7 RB.L 072769 RECKITT BENCKISER GRP GB GBP Y 51.9 12 10 GB0007188757 0718875 RIO.L 071887 RIO TINTO GB GBP Y 47.4 13 13 JE00B4T3BW64 B4T3BW6 GLEN.L GB10B3 GLENCORE PLC GB GBP Y 47.0 14 14 JE00B2QKY057 B2QKY05 SHP.L 079980 SHIRE GB GBP Y 39.4 15 16 GB00BDR05C01 BDR05C0 NG.L 024282 NATIONAL GRID GB GBP Y 35.9 16 15 GB0031348658 3134865 BARC.L 007820 BARCLAYS GB GBP Y 35.1 17 19 GB0004544929 0454492 IMB.L 045449 IMPERIAL BRANDS GB GBP Y 34.6 18 18 GB0000566504 0056650 BLT.L 005666 BHP BILLITON GB GBP Y 31.5 19 17 GB00BD6K4575 BD6K457 CPG.L 053315 COMPASS GRP GB GBP Y 28.6 20 20 GB0030913577 3091357 BT.L 014084 BT GRP GB GBP Y 28.2 21 21 GB0002162385 0216238 AV.L -

TIME to ‘RESET and RESTART’ – SAYS ROBINS & DAY CHIEF EXECUTIVE JAMES WESTON AS HIS TEAM RESPONDS to the CHALLENGES POSED by COVID-19 / P18 Adrocket

WINNERW I N N E R OFO F NEWSPRESSN E W S P R E S S AWARDS’AWA R D S ’ AUTOMOTIVEA U T O M O T I V E BUSINESSB U S I N E S S PUBLICATIONP U B L I C AT I O N 20202 0 2 0 BACKLASH FOR BCA / P6 Revised cinch platform makes it a competitor, says retailers WWHATHAT NNEXTEXT FFOROR LLEVC?EVC? / P22 The maker of London tax cabs is branching out into electric vans www.am-online.com NovemberNovember 22020020 ££8.008.00 DEALER TECHNOLOGY GUIDE / P31 A 31-page guide to suppliers at the cutting edge TIME TO ‘RESET AND RESTART’ – SAYS ROBINS & DAY CHIEF EXECUTIVE JAMES WESTON AS HIS TEAM RESPONDS TO THE CHALLENGES POSED BY COVID-19 / P18 adRocket FP_AM_9781CCPAM2id4396297.pdf 10.16.2020 10:33 EDITOR’S LETTER fter the lull of this year’s second quarter, hasn’t quarter four turned into a race for everyone? The pressure is on to finish the year as strongly as possible and keep that confidence sustained into 2021 as we all continually adjust to the changing restrictions. To help keep you inspired and up-to-date with the latest best practice, and to help you see what your peers have been up to, AM has two virtual events scheduled for November and December, which you’ll be able to log on to from your PC or phone. First, there will be a webinar for this year’s AM100 on A November 18, in association with BDO, where we’ll reveal the latest trends and highlights of the UK’s biggest motor retailers. -

Automotive Aftermarket

INVESTMENT BANKING 247 / 150 / 70 Parts Retailers 0 / 176 / 80 Suppliers Automotive Aftermarket JEFFERIES WEEKLY GLOBAL AUTOMOTIVE AFTERMARKET REPORT April 21, 2017 0 / 112 / 192 General Twelve Month Price Performance Suppliers Parts Retailers & Distributors Retail Service Providers Collision 255 / 204 / 0 Automotive Aftermarket Equity JEF Automotive Aftermarket Index S&P 500 Retail Service Index Returns 150% Providers 1 Week 1 Month 140% S&P 500 0.8% 0.2% 130% 255 / 0 / 0 JEF Automotive Aftermarket Index 3.5% 0.9% 120% 113.2% 112.3% Dealers Suppliers 3.1% 2.0% 110% 106.1% 102.9% 101.6% Parts Retailers & Distributors 4.4% 0.1% 100% 99.8% Retail Service Providers (0.3%) (1.8%) 0 / 176 / 240 90% Collision 2.0% (2.8%) 80% Collision Source: Capital IQ Suppliers: AXTA, CTB, DORM, GT, HZN, MPAA, SMP, SNA, VVV; Parts Retailers & Distributors: AAP, AZO, GPC, LKQ, ORLY, PRTS, SNA, UNS; Retail Service Providers: BYD.UN; 128 / 100 / 162 MNRO, VVV; Collision: BYD.UN, CPRT, FENX, KAR, LKQ AA Index LTM Trading Multiples Suppliers Parts Retailers & Distributors (EV / LTM EBITDA) Retail Service Providers Collision JEF Automotive Aftermarket Index Automotive Aftermarket 16.0x Trading Multiples 15.0x 4/21/2017 1 Year Ago 14.0x 13.5x 13.0x 13.2x JEF Automotive Aftermarket Index 11.5x 12.3x 12.0x 12.0x 11.5x Suppliers 9.6x 9.8x 11.0x Parts Retailers & Distributors 12.0x 13.6x 10.0x 9.6x Retail Service Providers 13.2x 15.0x 9.0x 8.0x Collision 13.5x 13.5x Source: Capital IQ MILES TRAVELED AND AVERAGE GASOLINE PRICE PER GALLON 8.0% $2.90 PerPriceGallon Average Gasoline Year - 6.0% 5.0% $2.70 Over - 4.5% 3.6% $2.50 4.0% 3.0% 2.7% $2.30 2.2% 1.8% Change) 1.6% 1.3% 2.0% 0.9% $2.10 0.7% 0.5% $1.90 0.0% $1.70 (0.2%) Vehicle Miles Traveled (Year VehicleMilesTraveled (2.0%) $1.50 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Source: Miles Traveled – U.S. -

DATABANK INSIDE the CITY RACHEL MILLARD the WEEK in the MARKETS the ECONOMY Consumer Prices Index Current Rate Prev

10 The Sunday Times August 4, 2019 BUSINESS Liam Kelly LETTERS dating (the company, you Send your letters, including Arcadia, Intu initially resisted — there’s a need for women- Rothschild banker’s 23.5-carat boast understand, not the board No accounting SIGNALS full name and address, giving in to Sir Philip Green’s only workspaces”, July 21). itself ) because it could use AND NOISE . to: The Sunday Times, demands because it feared Recent academic research Readers of the London the 1,000-year-old petrified the same technology as the for top Tory 1 London Bridge Street, stable tenants would request studied the types of networks Magazine were treated to a wood tables, the rare online property portal. Ben Elliot was named joint London SE1 9GF. Or email: parity. It would seem that that men and women benefit glimpse inside a grade II- artworks by Sakti Burman, Instead of pictures of houses, Conservative chairman after [email protected] Intu had a point that was lost from. One difference was that listed pile last summer, and the 23.5 carat gold used it would show singletons’ Boris’s brutal reshuffle. But Letters may be edited on its fellow landlords. women benefit from having a tastefully refurbished in to decorate an alcove photos and descriptions. He the nephew of the Duchess As a retired architect distinctive inner circle of luxurious Indian style. containing a Burmese had, in effect, imagined a of Cornwall — founder of Money-hungry owners can specialising in retail, I wrote a close female contacts. Giving The home on Heath Drive Buddha (“24 carat is too prehistoric Tinder. -

Investment Company Report

Investment Company Report Meeting Date Range: 01-Jul-2019 - 30-Sep-2019 Report Date: 03-Oct-2019 Page 1 of 721 BlackRock ABIOMED, INC. Security: 003654100 Agenda Number: 935053607 Ticker: ABMD Meeting Type: Annual ISIN: US0036541003 Meeting Date: 07-Aug-19 Prop. # Proposal Proposed Proposal Vote For/Against by Management's Recommendation 1. DIRECTOR 1 Michael R. Minogue Mgmt For For 2 Martin P. Sutter Mgmt For For 2. Approval, by non-binding advisory vote, of the Mgmt Against Against compensation of our named executive officers. 3. Ratify the appointment of Deloitte & Touche Mgmt For For LLP as our independent registered public accounting firm for the fiscal year ending March 31, 2020. Investment Company Report Meeting Date Range: 01-Jul-2019 - 30-Sep-2019 Report Date: 03-Oct-2019 Page 2 of 721 BlackRock ANADARKO PETROLEUM CORPORATION Security: 032511107 Agenda Number: 935062531 Ticker: APC Meeting Type: Special ISIN: US0325111070 Meeting Date: 08-Aug-19 Prop. # Proposal Proposed Proposal Vote For/Against by Management's Recommendation 1. To adopt the Agreement and Plan of Merger, Mgmt For For dated as of May 9, 2019, by and among Occidental Petroleum Corporation, Baseball Merger Sub 1, Inc. and Anadarko Petroleum Corporation ("Anadarko"). 2. To approve, on a non-binding advisory basis, Mgmt Against Against the compensation that may be paid or become payable to Anadarko's named executive officers that is based on or otherwise related to the proposed transactions. Investment Company Report Meeting Date Range: 01-Jul-2019 - 30-Sep-2019 Report Date: 03-Oct-2019 Page 3 of 721 BlackRock BB&T CORPORATION Security: 054937107 Agenda Number: 935057629 Ticker: BBT Meeting Type: Special ISIN: US0549371070 Meeting Date: 30-Jul-19 Prop. -

2020 Annual Review 8.63MB

About the BVRLA Established in 1967, the BVRLA is the UK trade body for companies engaged in vehicle rental, leasing and fleet management. BVRLA members register around 50% of all new cars, vans and trucks sold each year and are responsible for a combined fleet of over five million vehicles, that’s 1-in-8 cars, 1-in-5 vans and 1-in-4 trucks operating on UK roads. These fleets are leading the charge to decarbonise road transport. The BVRLA’s Plug-in Pledge will see the sector registering 400,000 battery electric vehicles (BEVs) per year by 2025, making it responsible for 80% of new battery electric car and van sales. On behalf of its 1,000+ member organisations, the BVRLA works with governments, public sector agencies, industry associations and key business influencers across a wide range of road transport, environmental, taxation, technology and finance-related issues. The vehicle rental and Transport Secretary of State, leasing industry supports over 465,000 jobs, adds Grant Shapps MP £7.6bn in tax revenues and contributes £49bn to the UK economy each year. BVRLA membership provides customers with “ The UK vehicle rental and leasing industry is the reassurance that the company they are an important part of our economy and will dealing with adheres to the highest standards of professionalism and fairness. remain so in the future. The industry not only BVRLA ANNUAL REVIEW 2020 REVIEW BVRLA ANNUAL The association achieves this by maintaining industry standards and regulatory compliance via directly employs tens of thousands of people its mandatory Codes of Conduct, inspection and and generates significant value in GDP terms governance programme and government-approved Alternative Dispute Resolution service. -

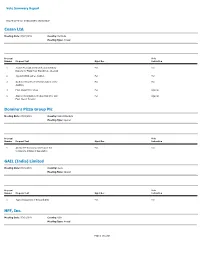

Vote Summary Report

Vote Summary Report Reporting Period: 07/01/2019 to 09/30/2019 Cosan Ltd. Meeting Date: 07/01/2019 Country: Bermuda Meeting Type: Annual Proposal Vote Number Proposal Text Mgmt Rec Instruction 1 Accept Financial Statements and Statutory For For Reports for Fiscal Year Ended Dec. 31, 2018 2 Appoint KPMG LLP as Auditors For For 3 Authorize Board to Fix Remuneration of the For For Auditors 4 Elect Class III Directors For Against 5 Approve Resignation of Class I Director and For Against Elect Class I Director Domino's Pizza Group Plc Meeting Date: 07/01/2019 Country: United Kingdom Meeting Type: Special Proposal Vote Number Proposal Text Mgmt Rec Instruction 1 Amend the Borrowing Limit Under the For For Company's Articles of Association GAIL (India) Limited Meeting Date: 07/01/2019 Country: India Meeting Type: Special Proposal Vote Number Proposal Text Mgmt Rec Instruction 1 Approve Issuance of Bonus Shares For For HFF, Inc. Meeting Date: 07/01/2019 Country: USA Meeting Type: Annual Page 1 of 1,208 Vote Summary Report Reporting Period: 07/01/2019 to 09/30/2019 HFF, Inc. Proposal Vote Number Proposal Text Mgmt Rec Instruction 1 Approve Merger Agreement For For 2 Advisory Vote on Golden Parachutes For For 3.1 Elect Director Deborah H. McAneny For For 3.2 Elect Director Steven E. Wheeler For For 4 Ratify Ernst & Young LLP as Auditors For For 5 Advisory Vote to Ratify Named Executive For Against Officers' Compensation Shanxi Xishan Coal & Electricity Power Co., Ltd. Meeting Date: 07/01/2019 Country: China Meeting Type: Special Proposal Vote Number -

Asset Listing for the New York State Common Retirement Fund As of March 31, 2019

New York State Common Retirement Fund Asset Listing as of March 31, 2019 Domestic and International Equity 1 - 75 Commingled Stock Funds 76 Global Fixed Income 77 - 94 Mortgage Holdings 95 - 99 Real Estate Investments 100 - 101 SHort-Term Investments 102 - 103 Alternative Investments Assets: Private Equity Investments 104 - 107 Private Equity Investments / Fund of Funds Listing 108 - 113 Absolute Return Strategy / Fund of Funds Listing 114 Opportunistic Funds 115 Real Assets 116 DOMESTIC AND INTERNATIONAL EQUITY As of March 31, 2019 Security Description Shares Cost Fair Value 1-800-FLOWERS.COM INC - CLASS A 27,600 $ 280,598 $ 503,148 1ST CONSTITUTION BANCORP 8,100 177,876 143,937 1ST SOURCE CORP 19,531 655,207 877,137 21VIANET GROUP INC - ADR 3,854 36,373 30,601 22ND CENTURY GROUP INC 94,600 231,770 161,766 2U INC 122,062 10,177,125 8,648,093 3D SYSTEMS CORP 110,800 1,533,420 1,192,208 3I GROUP PLC 353,685 3,715,939 4,538,640 3M COMPANY 1,438,900 115,229,822 298,974,642 58.COM INC - ADR 54,646 3,068,505 3,589,149 77 BANK LTD/THE 123,100 2,864,838 1,720,519 8X8 INC 95,700 1,045,763 1,933,140 A&D COMPANY LTD 16,900 159,271 116,499 A.O. SMITH CORP 531,747 22,320,398 28,352,750 A10 NETWORKS INC 36,500 247,343 258,785 A2 MILK COMPANY LTD 285,501 2,694,919 2,762,213 AA LTD 1,708,209 7,267,192 2,025,552 AAC HOLDINGS INC 9,300 340,886 17,112 AAK AB 81,073 1,276,127 1,212,166 AAON INC 40,500 673,141 1,870,290 AAR CORP 31,900 832,868 1,037,069 AAREAL BANK AG 28,659 1,322,302 884,300 AARONS INC - CLASS A 226,943 8,724,323 11,937,202 ABBOTT LABORATORIES -

Javid's Plan Set for Next Wednesday

Get more from your holiday money BUSINESS WITH PERSONALITY WEDNESDAY 28 AUGUST 2019 ISSUE 3,444 CITYAM.COM FREE Javid’s plan set for next Wednesday CATHERINE NEILAN BIG TOBACCO @CatNeilan PHILIP MORRIS AND ALTRIA ENTER CHANCELLOR Sajid Javid has brought forward his debut TALKS OVER $210BN MEGA-MERGER spending review to next Wednes day, fuelling speculation AS MARLBORO-MAKERS SEEK TO of an autumn General Election. Javid was due to give his first LIGHT UP ALTERNATIVE PRODUCTS major speech since becoming chancellor this morning, before it was cancelled yesterday. AUGUST GRAHAM Altria already plans to market PMI’s The Treasury said the Iqos – a heated tobacco product which spending review would “cover @AugustGraham won US approval in April – to American the themes and priorities he ONE OF the world’s most hotly consumers. was due to outline”. anticipated mega-mergers kicked off Meanwhile, Altria bought a 35 per One source told City A.M. the yesterday as tobacco giants Philip cent stake in popular vape pen maker decision to pull the speech had Morris International (PMI) and Altria Juul for $12.8bn late last year. come from Number 10. said they were in talks to form a Bonnie Herzog, managing director at Javid is expected to announce $210bn (£170bn) behemoth. Wells Fargo Securities, said ahead of significant spending hikes. The deal would reunite two the announcement that PMI would be companies that split up in 2008 amid an ideal partner to help the younger regulatory pressures at the time. Juul expand beyond the US. In recent years, both businesses Elliott said: “The combined entity – have put alternative nicotine products Philip Morris 2.0 – could present a such as e-cigarettes at the front and united front” on alternative products, Home Office centre of their strategies. -

How Telematics Is Set to Shape the Way We Buy, Drive and Maintain Cars

www.motorfinanceonline.com Issue 177 / august 2019 REMOTE CONTROL HOW TELEMATICS IS SET TO SHAPE THE WAY WE BUY, DRIVE AND MAINTAIN CARS FEATURE ANALYSIS COMMENT Car manufacturers are As dealers sell more online, Surprising statistics about doubling down as consumer the race is on for full millennials’ attitudes, and appetite for EVs grows omnichannel adoption what they mean for dealers MF August 177.indd 1 01/08/2019 10:46:26 contents this month COVER STORY NEWS 14 05 / EDITOR’S LETTER 06 / DIGEST • Barclays Partner Finance withdraws from motor finance • Car dealer group Lookers under FCA investigation • Blue to collaborate with Lloyds for instant payments • Northridge signs white-label deal with SsangYong • SMMT: new car registrations drop for fourth consecutive month • Pendragon CEO to depart role • FCA launches review of credit information market • TDR Capital, BCA Marketplace agree £1.9bn acquisition • Getaround acquires Nordic firm for $12m • FCA launches consultation on customer treatment TELEMATICS • Pre-registrations return a ‘sign of difficulties’ Editor: News Desk: Publishing Assistant: Brian Cantwell +44 (0)20 7406 6538 Asena Değirmenci 24 / DATABANK +44 (0)20 7406 6705 +44 (0)20 3096 2633 Group Editorial Director: [email protected] [email protected] Ana Gyorkos Senior Reporter: +44 (0)20 7406 6707 Director of Events: Chris Lemmon [email protected] Ray Giddings +44 (0)20 7406 3723 +44 (0)20 3096 2585 Sub-editor: [email protected] [email protected] Nick Midgley Reporter: +44 (0)161 359 5829 Head of Subscriptions: Christopher Marchant [email protected] Alex Aubrey +44 (0)20 7406 6709 +44 (0)20 3096 2603 Sub-editor: [email protected] [email protected] Sophia Bell 07 Customer Services: +44 (0)20 3096 2603 or +44 (0)20 3096 2636, [email protected] Financial News Publishing, 2012. -

CDP's List of Official Samples 2019

CDP’s List of Official Samples 2019 This document contains a list of companies by sample that are requested to respond to CDP’s climate change, forests and water security questionnaires for 2019. Contents CDP’s List of Official Samples 2019 ................................................................................................ 1 Introduction ................................................................................................................................. 4 CDP Climate Change 2019 ............................................................................................................. 5 Worldwide ................................................................................................................................... 6 Emerging Markets .................................................................................................................... 6 FTSE All-World ...................................................................................................................... 12 Global 500 ............................................................................................................................. 17 Americas ................................................................................................................................... 21 Brazil...................................................................................................................................... 21 Canada .................................................................................................................................