382820Settleme101official0u

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Financial System That Creates Economic Opportunities Nonbank Financials, Fintech, and Innovation

U.S. DEPARTMENT OF THE TREASURY A Financial System That Creates Economic Opportunities A Financial System That T OF EN TH M E A Financial System T T R R A E P A E S That Creates Economic Opportunities D U R E Y H T Nonbank Financials, Fintech, 1789 and Innovation Nonbank Financials, Fintech, and Innovation Nonbank Financials, Fintech, TREASURY JULY 2018 2018-04417 (Rev. 1) • Department of the Treasury • Departmental Offices • www.treasury.gov U.S. DEPARTMENT OF THE TREASURY A Financial System That Creates Economic Opportunities Nonbank Financials, Fintech, and Innovation Report to President Donald J. Trump Executive Order 13772 on Core Principles for Regulating the United States Financial System Steven T. Mnuchin Secretary Craig S. Phillips Counselor to the Secretary T OF EN TH M E T T R R A E P A E S D U R E Y H T 1789 Staff Acknowledgments Secretary Mnuchin and Counselor Phillips would like to thank Treasury staff members for their contributions to this report. The staff’s work on the report was led by Jessica Renier and W. Moses Kim, and included contributions from Chloe Cabot, Dan Dorman, Alexan- dra Friedman, Eric Froman, Dan Greenland, Gerry Hughes, Alexander Jackson, Danielle Johnson-Kutch, Ben Lachmann, Natalia Li, Daniel McCarty, John McGrail, Amyn Moolji, Brian Morgenstern, Daren Small-Moyers, Mark Nelson, Peter Nickoloff, Bimal Patel, Brian Peretti, Scott Rembrandt, Ed Roback, Ranya Rotolo, Jared Sawyer, Steven Seitz, Brian Smith, Mark Uyeda, Anne Wallwork, and Christopher Weaver. ii A Financial System That Creates Economic -

China Insurance Sector

China / Hong Kong Industry Focus China Insurance Sector Refer to important disclosures at the end of this report DBS Group Research . Equity 1 Nov 2017 Multi-year value growth ahead HSI: 28,336 • Strong growth potential back by C-ROSS, favourable policy direction, and structural drivers ANALYST • Favourable asset/liability mismatch position Ken SHIH +852 2820 4920 [email protected] bodes well under a rising rate environment; China lifers’ book value is set to rise Keith TSANG CFA, +852 2971 1935 nd [email protected] • Impact from 2 phase of auto insurance pricing reform expected to be more severe; online insurers considered to be a disruptive force Recommendation & valuation • Initiating coverage on China Insurance sector. Top picks: China Taiping (966 HK), CPIC (2601 HK), and C losing Targe t FY17F Ping An (2318 HK). Top SELLs: PICC P&C (2328 HK), Stock Ticker Rating Price Price PB Yield ROE and China Re (1508 HK) (HKD) (HK D) (X) (%) (% ) Spotlight on value enhancement: We believe China’s low Ping A n - H 2318 H K BUY 68. 1 86. 0 2.4 1.5 17.8 insurance coverage, launch of China Risk-Oriented Solvency C hina Life - H 2628 H K BUY 25. 8 32. 0 1.9 1.8 9.6 System (C-ROSS), and policy guidance will continue to direct China Taiping 966 HK BUY 25.1 38.0 1.4 1.1 8.9 China life insurers to refocus on traditional life products and C hina Pacific - H 2601 HK BUY 37. 7 54. 0 2.0 2.8 11.1 value enhancement. -

CUGN Academic Catalog Contains Current Information Regarding the Academic Calendar, Admissions, Degree Requirements, Fees, Regulations, and Course Offerings

2012 ACADEMIC CATALOG CHRISTIAN UNIVERSITY GLOBALNET 2013-14 ACADEMIC CATALOG www.cugn.org Table of Contents Introduction . 3 Academic Policies . .60 Welcome . 4 Drop/Add Procedures . 60 From the President . .. 4 Appeals Process . 60 From the Academic Dean . 5 Honesty/Cheating/Plagiarism . 61 Contacting Us . 6 Student IDs . 61 About CUGN . 7 Bible Competency Exam and Advanced Placement . 61 History . 7 Repeating a Course . 62 Academic Programs . 7 GPA Scale . .. 62 What We Believe . 8 Pass-Fail and Course Validation in Core 1 . 62 Endorsements and Testimonials . 9 Special Student Needs/Accommodations . 63 General Endorsements . 9 CUGN Email Account/Google Docs . 63 Faculty Endorsements . 10 Incompletes . 63 Mission and Vision . .11 Extensions . 63 Academic Calendar / Enrollment Deadlines . 12 Academic Probation . 64 2013 . 12 Dismissal . .. 64 2014 . 13 Transfer Credit . 64 2015 . 14 Part-time, Full-time, Noncredit Students . 65 Curriculum Description . .15 Discussion Forum Guidelines . 65 Summary Chart of Program Requirements . 16 Requirements for Success . 66 M.A.R. Thesis-Project . 19 Tutorials and Learning Management System (LMS) . 66 M.A.R. Concentrations . .20 Bible Competency Exam . 66 Choosing Your M .A .R . Concentration . 20 English Proficiency . 66 Master of Arts in Ministry Studies (accredited) . 23 Computer/Internet/Software Requirements . 66 Certificate Programs . 24 Student Records . 67 Transfer Credit Courses . 26 Mentor Requirements . 67 Course Lists Per Semester . 27 Graduation Procedures . .67 Undergraduate Degree Options . 30 Online Library / Resources . 67 Course Descriptions . 32 Tuition and Financial Aid . 68 Old Testament . 33 Tuition Costs . 68 New Testament . 37 Tuition Payments . 68 Systematic Theology . 41 Refunds . 68 Church History . 42 Financial Assistance . -

Universidad Apec

UNIVERSIDAD APEC ESCUELA DE GRADUADOS Trabajo Final Para Optar Por El Titulo De: MAESTRÍA EN GERENCIA Y PRODUCTIVIDAD Tema: “Mejoras para la Optimización de la Funcionalidad en la Red de Cajeros Automáticos. Caso: Banco Popular Año 2011” Sustentante: Glenny W. Serrata García 2009-1883 Asesora: Ivelisse Comprés, MA, MsC, MBA. Santo Domingo, D.N. Agosto, 2011 “Mejoras para la Optimización de la Funcionalidad en la Red de Cajeros Automáticos. Caso: Banco Popular Año 2011” INDICE Págs. RESUMEN ..................................................................................................... ii DEDICATORIA ............................................................................................ iv INTRODUCCION ........................................................................................ 02 CAPITULO I: GENERALIDADES DE LA BANCA ELECTRÓNICA 1.1 Historia de los Cajeros Automáticos .......................................................... 06 1.1.2 Definición de Cajeros Automáticos ................................................... 08 1.1.3 Funcionalidad de los ATM ............................................................... 08 1.1.4 Diseño y Tipos de Cajeros Automáticos............................................ 10 1.1.5 Regulaciones de los ATMs ............................................................... 11 1.2 Nueva Tecnología en Cajeros Automáticos ................................................ 12 1.2.1 Cajero Automáticos de Autoservicio ................................................. 12 1.2.2 Primer Cajero Biométrico -

Financial Crisis Report Written and Edited by David M

PUBLISHED BY MIYOSHI LAW July 2018 INTERNATIONAL & EST ATE LAW PRACTICE Volume 1, Issue 81 Financial Crisis Report Written and Edited by David M. Miyoshi Advancing in a Time of Crisis Words of Wisdom: "You can succeed at anything, as long as you don’t Inside this issue: care who takes the credit” Ronald Reagan 1. Historic Singapore Meeting 2. Go West Young Man Historic Singapore Meeting and suggested that it may ease its sanctions on 3. Wedding IRS Loves North Korea prior to complete denuclearization 4. Cryptocurrency Geo-Political Weap- its Aftermath and that it will halt U.S.-South Korea military on exercises. 5. Is Harvard Racist? Except for the Great Depression, we are experiencing the most By affirming that "mutual confidence building economically unstable period in can promote the denuclearization of the Korean the history of the modern world. Peninsula," the statement indicated that the This period will be marked with United States is willing to accept the phased extreme fluctuations in the stock, approach to denuclearization that North Korea commodity and currency markets accompanied by severe and some- desires. In a phased approach, both sides would times violent social disruptions. offer incentives along the way to denucleariza- As is typical of such times, many tion, rather than the United States waiting until fortunes will be made and lost the process is complete before offering any during this period. After talking tradeoffs. For the time being, Trump empha- with many business owners, sized that sanctions would remain in effect, but executives, professionals and he said they could be removed when North government officials from around n June 12, President Trump and the world, the writer believes that Korea makes a certain degree of progress in its Kim Jong Un leader of North Korea denuclearization. -

Service Provider Name Region AOC Date Assessor DESV

A company’s name appears on this Compliant Service Provider List if (i) Mastercard has received a copy of an Attestation of Compliance (AOC) by a Qualified Security Assessor (QSA) reflecting validation of the company being PCI DSS compliant and (ii) Mastercard records reflect the company is registered as a Service Provider by one or more Mastercard Customers. The date of the AOC and the name of the QSA are also provided. Each AOC is valid for one year. Mastercard receives copies of AOCs from various sources. This Compliant Service Provider List is provided solely for the convenience of Mastercard Customers and any Customer that relies upon or otherwise uses this Compliant Service Provider list does so at the Customer’s sole risk. While Mastercard endeavors to keep the list current as of the date set forth in the footer, Mastercard disclaims any and all warranties of any kind, including any warranty of accuracy or completeness or fitness for any particular purpose. Mastercard disclaims any and all liability of any nature relating to or arising in connection with the use of or reliance on the Compliant Service Provider List or any part thereof. Each Mastercard Customer is obligated to comply with Mastercard Rules and other Standards pertaining to use of a Service Provider. As a reminder, an AOC by a QSA provides a “snapshot” of security controls in place at a point in time. Compliant Service Provider 1-60 Days Past AOC Due Date 61-90 Days Past AOC Due Date Service Provider Name Region AOC Date Assessor DESV “BPC Processing”, LLC Europe 03/31/2017 Informzaschita 1&1 Internet SE (1&1, 1&1 ipayment, Europe 05/08/2017 Security Research & Consulting GmbH ipayment.de) 1Shoppingcart.com (Web.com Group, lnc.) US 04/29/2017 SecurityMetrics 2138617 Ontario Inc. -

Attachment I

ATTACHMENT I PROPERTY INSURANCE Schedule of Values Exposure Information VALUED AS OF JULY 1, 2017 JEFFERSON COUNTY PUBLIC SCHOOLS LOUISVILLE, KENTUCKY i Thl le%rsoii County Board of Education, Louisville, KY I ?- Sdsx l Shap?rq the Future l 2017-2018 Statement of lnsurable Values Loc # r r g Building Name Address r Constr Class Description ? Building Contents l TotalByCampus 1 STONESTREETELEMENTARY 10007 STONESTREET ROAD %onry N6n-Combustible - j00 % J '? 1 r r r W 'Mu4,lSal 9,070q ffl T r l r r l l 1 J?RDAiE HIGH SCHOOL Q 40118 Fire Resistive - 100 % J Y l o ffi W W 1 i 2'JRDALEVC)CATIONAL Ji00l FAIRDALE RD %:rv xon-combustibie - 100 % Y o J W Q 1 J?RDAiE OFFICE BUILDING (BUS) liOl FAIRDALE RD J40ljfe - 100 % Y o '? 1 2 FAIRLDALEWEIGHTRMBUILDING W ?01 FAilRDALE RD lLlol18 dbUaible-100% Y o 7 20,851i 2 iLOC.SubtOtal l T ffi T 46.370,6021 '6,477,9SSi j l T l T r l l 1 F,ENGELHARD ELEMENTARY 1004 SOUTH FIRST STRa- 4nry Non-combustible - 100 % {J94 i 8,432,30IJ 2.2i5,034i 1 r r r l l Q W W Th l T r r r 1 I?SOuTHliH PARK PARK?? TA?P 1010 NEIGHBORHOOD PLACE J4%nrv Non-Combustible - 100 % J J i,szi,sssJ 1 r r r s:q Q Q r r r r r T r l s FAIRDALE EIEMENTARY 10104 MITCHELL HILL ROAD 40118 llflasonry Non-Combustible - 100 % Y o J W 1 s FAIRDALEELEMENTARYSCHOOL-AD[)ITION 981,842i 10104 MITCHELL HILL ROAD %nry Non-Combustible - 100 % Y N pIs l 2,158,994T 'm,sasi 1 s Loc.Subtotal r r r l s,soo,o'4 1,202,688 i '? r r l r r 1 f'?l?LEY HIGH 'iCHOOL Jm200'DIXIEHIGHWlAY 4*;ea p*re Resistive - too s Y 100 1 6 VAILY'HIGHSCHOOL,1.C.CANTRELLGYM J W J }10200 DIXIE HIGHWAY J40272Jj?nry Non-Combustible - 100 % Y o J 2Q m? 1 6 Loc. -

Assessing Payments Systems in Latin America

Assessing payments systems in Latin America An Economist Intelligence Unit white paper sponsored by Visa International Assessing payments systems in Latin America Preface Assessing payments systems in Latin America is an Economist Intelligence Unit white paper, sponsored by Visa International. ● The Economist Intelligence Unit bears sole responsibility for the content of this report. The Economist Intelligence Unit’s editorial team gathered the data, conducted the interviews and wrote the report. The author of the report is Ken Waldie. The findings and views expressed in this report do not necessarily reflect the views of the sponsor. ● Our research drew on a wide range of published sources, both government and private sector. In addition, we conducted in-depth interviews with government officials and senior executives at a number of financial services companies in Latin America. Our thanks are due to all the interviewees for their time and insights. May 2005 © The Economist Intelligence Unit 2005 1 Assessing payments systems in Latin America Contents Executive summary 4 Brazil 17 The financial sector 17 Electronic payments systems 7 Governing institutions 17 Electronic payment products 7 Banks 17 Conventional payment cards 8 Clearinghouse systems 18 Smart cards 8 Electronic payment products 18 Stored value cards 9 Credit cards 18 Internet-based Payments 9 Debit cards 18 Payment systems infrastructure 9 Smart cards and pre-paid cards 19 Clearinghouse systems 9 Direct credits and debits 19 Card networks 10 Strengths and opportunities 19 -

Absa Bank (South Africa)

The Companies Listed under the Consortium for Next Gen ATMs ABA (American Bankers Association) Absa Bank (South Africa) Access Cash General Partnership (EZEE ATM) ACG ACI Worldwide ATEFI AIB (Allied Irish Banks) Akbank (Turkey) Altron Bytes Managed Solutions Aman (Palestine) ANZ Argotechno ATB Financial ATEFI ATM24 ATM CLUB Atima ATMIA ATM Security Association Auriga Australian Technology Management Pty Ltd Axis Communications AB 1 Bank of America Bank of Hawaii Bank of Montreal Bank of South Pacific Bank Permata BANTAS A.S Banktech (Australia) Barclays Bank BBVA Belfius Bank & Verzekeringen Bitstop Blanda Marketing & Public Relations BMO Financial Group BOSACH Technologies & Consulting Pvt. Ltd. BVK Capital One Cashflows Cashway Technology Co., Ltd. Capital One Bank Capitec Bank Cardtronics Cash and Card World Ltd Cash Connect® – ATM Solutions by WSFS Bank Cash Infrastructure Projects and Services GmbH Cashware Cecabank CIBC (Canadian Imperial Bank of Commerce) Citibank Citizens Bank CMS Analytics Coast Capital Savings Credit Union 2 Columbus Data Comerica Bank Commonwealth Bank of Australia Convergint Technologies CO-OP Financial Services CR2 Culiance Cummins Allison Cyttek Group Desjardins Dgiworks Technology (Turkey) Diebold-Nixdorf dormakaba USA Inc DPL Eastern Carolina ATM Eastman Credit Union EFTA Elan Financial Services Electronic Payment & Services (Pty) Ltd Embry Consulting, LLC Emirates NBD Euronet Worldwide EuroTechzam S.A. EVERTEC, Inc – US EVERI EVO Payments Faradis Alborz Corp First American Payment Systems First Data First National Bank of South Africa FISERV 3 FIS Global (Fidelity National Information Services) Fujitsu Ten España G4S GCB Bank (Ghana) General Dynamics Mission Systems Genmega GMR GMV Gorham Savings Bank GPT Great Southern Bank GRG Banking Gunnebo Gunnebo India Private Ltd Heritage Bank Hitachi Europe Hitachi-Omron Terminal Solutions, Corp. -

Inclusión Financiera Y Medios De Pago Electrónicos

Inclusión Financiera y Medios de Pago Electrónicos Informe preparado por la Mesa de Trabajo integrada por los Ministerios de Desarrollo Social, Economía, Hacienda, y Transporte y Telecomunicaciones, en el marco de la Agenda de Impulso Competitivo. Abril 2013 Ministerio de Economía, Fomento y Turismo Ministerio de Desarrollo Social Ministerio de Hacienda Ministerio de Transporte y Telecomunicaciones ÍNDICE 1. Resumen Ejecutivo 4 2. Glosario 9 3. Introducción 10 4. Mercado de Tarjetas de Crédito y Débito 12 4.1 Consideraciones Generales 12 4.2 Experiencia Extranjera 16 4.3 Mercado Chileno 20 4.3.1 Antecedentes Generales 20 4.3.2 Medios de Pago 24 4.3.3 Tarjetas Bancarias 26 4.3.4 Tarjetas de Crédito No Bancarias 31 4.3.5 Cuadro Comparativo 33 4.3.6 Transbank 33 4.3.7 Nexus 38 4.3.8 Redbanc 39 4.3.9 Redes Transaccionales Instaladas 41 4.4 Regulación Aplicable 45 4.5 Sociedades de Apoyo al Giro 48 4.6 Consideraciones Finales 49 5. Sistemas de Prepago o Valor Almacenado 53 5.1 Consideraciones Generales 53 5.2 Experiencia y Regulación Extranjera 56 5.3 Chile 59 5.4 Recomendaciones para Chile 60 2 Inclusión Financiera y Medios de Pago Electrónicos 6. Pagos Móviles 63 6.1 Mercado Móvil 63 6.2 Distintos Modelos de Negocios de Pagos Móviles 64 6.3 Tipos de Pagos Móviles en el Mundo 65 6.3.1 Dispositivos Móviles como POS 65 6.3.2 Mensaje de Texto Tradicional - SMS 65 6.3.3 SMS para Transferencias Electrónicas de Dinero 66 6.3.4 USSD para Transferencias Electrónicas de Dinero 67 6.3.5 M-Banking (Uso de la Banca a través de Internet Móvil) 68 6.3.6 Near Field Communication - NFC 68 6.3.7 Quick Responde Code - QR 69 6.4 Regulación de la Industria de Telecomunicaciones Aplicables 69 a los Pagos Móviles 6.5 Consideraciones Finales 70 7. -

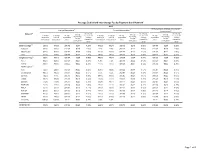

Average Debit Card Interchange Fee by Payment Card Network1

Average Debit Card Interchange Fee by Payment Card Network1 2015 All transactions (exempt and covered Exempt transactions 3 Covered transactions 4 transactions) 5 2 Interchange Interchange Interchange Network Average Average Average % of total % of total Average fee as % of % of total % of total Average fee as % of Average fee as % of interchange interchange interchange number of value of transaction average number of value of transaction average transaction average fee per fee per fee per transactions6 transactions6 value7 transaction transactions10 transactions10 value7 transaction value7 transaction transaction8 transaction8 transaction8 value9 value9 value9 11 Dual-message 38.2% 37.0% $36.49 $0.51 1.39% 61.8% 63.0% $38.38 $0.23 0.60% $37.66 $0.34 0.89% Discover 99.6% 99.5% $41.67 $0.65 1.56% 0.4% 0.5% $43.38 $0.24 0 55% $41.67 $0.65 1.55% MasterCard 50.8% 50.3% $37.98 $0.57 1.50% 49.2% 49.7% $38.77 $0.24 0.61% $38.37 $0.41 1.06% Visa 34.2% 32.7% $35.77 $0.48 1.34% 65.8% 67.3% $38.29 $0.23 0 59% $37.43 $0.31 0.84% Single-message12 35.2% 35.1% $39.04 $0.26 0.65% 64.8% 64.9% $39.36 $0.24 0.60% $39.25 $0.24 0.62% Accel 93.2% 92.8% $43.26 $0.21 0.48% 6.8% 7.2% $45.66 $0.24 0 53% $43.43 $0.21 0.49% AFFN 88.3% 86.9% $34.55 $0.25 0.72% 11.7% 13.1% $39.48 $0.21 0 54% $35.12 $0.25 0.70% Alaska Option13 ATH 14.2% 20.0% $50.58 $0.25 0.50% 85.8% 80.0% $33.44 $0.19 0 57% $35.87 $0.20 0.56% Credit Union 99.5% 99.5% $48.17 $0.23 0.47% 0.5% 0.5% $42.93 $0.20 0.47% $48.14 $0.23 0.47% Interlink 10.2% 9.4% $35.43 $0.35 0.99% 89.8% 90.6% $38.95 $0.24 -

December 31, 2015 Complete Financial Statements in IFRS Itaú Unibanco Holding S.A

December 31, 2015 Complete Financial Statements in IFRS Itaú Unibanco Holding S.A. Report of independent auditors on the consolidated financial statements To the Board of Directors and Stockholders of Itaú Unibanco Holding S.A. We have audited the accompanying consolidated financial statements of Itaú Unibanco Holding S.A. and its subsidiaries (the "Institution"), which comprise the consolidated balance sheet as at December 31, 2015 and the consolidated statements of income, comprehensive income, changes in equity and cash flows for the year then ended, and a summary of significant accounting policies and other explanatory information. Management's responsibility for the consolidated financial statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with the International Financial Reporting Standards (IFRS), and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. Auditor's responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with Brazilian and International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error.