Efiled: May 31 2016 08:30PM EDT Filing ID 59078052 Case Number 157,2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

How Uber Won the Rideshare Wars and What Comes Next

2/18/2020 How Uber Won The Rideshare Wars and What Comes Next CUSTOMER EXPERIENCE | HOW UBER WON THE RIDESHARE WARS AND WHAT COMES NEXT How Uber Won The Rideshare Wars and What Comes Next How Uber won the first phase of the rideshare war and how cabs, competitors, and car companies are battling back. BY ELYSE DUPRE — AUGUST 29, 2016 VIEW GALLERY https://www.dmnews.com/customer-experience/article/13035536/how-uber-won-the-rideshare-wars-and-what-comes-next 1/18 2/18/2020 How Uber Won The Rideshare Wars and What Comes Next View Gallery In 2011, two University of Michigan alums Adrian Fortino and Jahan Khanna partnered with venture capitalist Sunil Paul to revolutionize how people got from point A to point B quickly without having to do much. The company was Sidecar, and the idea was simple: “We're going to replace your car with your iPhone,” Fortino explains. Sidecar did not lack competition. Around this time, the taxi industry was experimenting with new ways to make it easier for individuals to summon cars. And entrepreneurs, frustrated with wait times, imagined new ways to hire someone to drive them around. Multiple companies formed to solve this need, including one that is now considered a global powerhouse: Uber. By the time Sidecar went into beta testing in February 2012, Uber, or UberCab as it was originally known when it was founded in 2009, had raised at least $37.5 million at a $330 million post-money valuation, according to VentureBeat. Lyft followed shortly after when it went into beta in mid 2012, boasting more than $7 million in funding, according to TechCrunch's figures. -

Reinventing Transportation in Our Connected World September 7-11, 2014 | Cobo Center | Detroit, Michigan, USA

Preliminary Program Registration Open Reinventing Transportation in our Connected World September 7-11, 2014 | Cobo Center | Detroit, Michigan, USA Hosted by: Co-hosts: www.itsworldcongress.org | #ITSWC14 2 21st World Congress on Intelligent Transport Systems Contents Welcome ----------------------------------------------------------------------- 4 & 5 Congress Format -------------------------------------------------------------- 6 Special Features --------------------------------------------------------------- 8 The 2014 ITS World Congress Mobile App ----------- 11 Registration ---------------------------------------------------------------------- 13 Travel & Transportation Information ----------------------- 18 Accommodation Information ------------------------------------- 20 General Information ------------------------------------------------------- 21 ITS America Leadership Circle -------------------------------- 22 Session Tracks ---------------------------------------------------------------- 23 Schedule at a Glance ---------------------------------------------------- 27 Keynote Speakers ---------------------------------------------------------- 28 High Level Policy Roundtable ------------------------------------ 30 Town Hall Sessions -------------------------------------------------------- 31 Plenary Sessions ------------------------------------------------------------ 32 CTO Summit Sessions -------------------------------------------------- 34 Executive Sessions -------------------------------------------------------- 38 Special -

In the Court of Chancery of the State of Delaware

IN THE COURT OF CHANCERY OF THE STATE OF DELAWARE THOMAS SANDYS, Derivatively on Behalf of ) ZYNGA INC., ) ) Plaintiff, ) ) v. ) C.A. No. 9512-CB ) MARK J. PINCUS, REGINALD D. DAVIS, ) CADIR B. LEE, JOHN SCHAPPERT, DAVID M. ) WEHNER, MARK VRANESH, WILLIAM ) GORDON, REID HOFFMAN, JEFFREY ) KATZENBERG, STANLEY J. MERESMAN, ) SUNIL PAUL and OWEN VAN NATTA, ) ) Defendants, ) ) and ) ) ZYNGA INC., a Delaware Corporation, ) ) Nominal Defendant. ) MEMORANDUM OPINION Date Submitted: November 17, 2015 Date Decided: February 29, 2016 Norman M. Monhait and P. Bradford deLeeuw, ROSENTHAL, MONHAIT & GODDESS, P.A., Wilmington, Delaware; Jeffrey S. Abraham and Philip T. Taylor, ABRAHAM, FRUCHTER & TWERSKY, LLP, New York, New York; Attorneys for Plaintiff. Elena C. Norman, Nicholas J. Rohrer and Paul J. Loughman, YOUNG CONAWAY STARGATT & TAYLOR, LLP, Wilmington, Delaware; Jordan Eth, Anna Erickson White and Kevin A. Calia, MORRISON & FOERSTER LLP, San Francisco, California; Attorneys for Defendants Mark J. Pincus, Reginald D. Davis, Cadir B. Lee, John Schappert, David M. Wehner, Mark Vranesh, Owen Van Natta, and Nominal Defendant Zynga Inc. Bradley D. Sorrels and Jessica A. Montellese, WILSON SONSINI GOODRICH & ROSATI, P.C., Wilmington, Delaware; Steven M. Schatz, Nina Locker and Benjamin M. Crosson, WILSON SONSINI GOODRICH & ROSATI, P.C., Palo Alto, California; Attorneys for Defendants William Gordon, Reid Hoffman, Jeffrey Katzenberg, Stanley J. Meresman and Sunil Paul. BOUCHARD, C. A stockholder of Zynga Inc. brings this derivative suit to recover damages the company allegedly suffered because the Zynga board approved exceptions to lockup agreements and other trading restrictions that allowed certain directors and officers to sell some of their Zynga shares in an April 2012 secondary offering. -

Report of the Special Litigation Committee of the Board of Directors of Zynga Inc

REPORT OF THE SPECIAL LITIGATION COMMITTEE OF THE BOARD OF DIRECTORS OF ZYNGA INC. February 27, 2018 TABLE OF CONTENTS INTRODUCTION ........................................................................................... 1 SUMMARY OF THE STOCKHOLDER DERIVATIVE ACTIONS ........... 5 A. The Three Derivative Lawsuits ................................................................ 7 B. The Nominal Defendant .........................................................................11 C. The Defendants ......................................................................................12 D. The Allegations ......................................................................................15 1. Allegations that Defendants Breached the Fiduciary Duty of Loyalty ....................................................................................17 a) Allegations Relating to Knowledge of Material, Adverse Information .........................................................19 b) Allegations Relating to Director Conflicts........................25 2. Allegations that Defendants Breached the Fiduciary Duty of Care .........................................................................................26 E. Timeline of the Derivative Lawsuits .....................................................28 FORMATION OF THE SPECIAL LITIGATION COMMITTEE .............. 31 A. The Members of the SLC .......................................................................34 B. Compensation ........................................................................................36 -

Organizing Manual National Homeless Persons' Memorial Day

22000099 OOrrggaanniizziinngg MMaannuuaall NATIONAL HOMELESS PERSONS’ MEMORIAL DAY MANUAL 2009 Organizing Manual National Homeless Persons’ Memorial Day December 21, 2009 Homeless people will die in your community this year. Plan to memorialize them on December 21, the first day of Winter, the longest night of the year. In 2008, over 120 communities participated in the 18th Annual National Homeless Persons’ Memorial Day; surpassing last years’ number of communities by more than 30. Let’s make 2009 a year of more awareness by organizing even more memorial services for the homeless throughout the nation. The National Coalition National Health Care for National Consumer for the Homeless the Homeless Council Advisory Board 2201 P St NW PO Box 60427 PO Box 60427 www.nationalhomeless.org Nashville, TN 37206 Nashville, TN 37206 Washington, DC 20037 www.nhchc.org www.nhchc.org Phone: 202.462.4822 Phone: (615) 226-2292 Phone: (615) 226-2292 Fax: 202.462.4823 Fax: (615) 226-1656 Fax: (615) 226-1656 [email protected] [email protected] [email protected] THE FIRST DAY OF WINTER. THE LONGEST NIGHT OF THE YEAR. ii NATIONAL HOMELESS PERSONS’ MEMORIAL DAY MANUAL 2009 Table of Contents 1 An Overview 2 Organizing an Event to Commemorate National Homeless Persons’ Memorial Day 4 2008 Memorial Day Event Locations 6 Sample Flyers and Agendas 10 Sample Press Releases 14 Sample State Proclamations 16 Sample City/County Resolutions 20 Highlights of 2008 Memorial Day Events 42 List of Homeless Deaths in 2008 72 “Bloggers Unite” 73 Street Sense article, March 2009 St. Louis Memorial Service, Dec. 21, 2008. -

Photo Release -- Zynga Appoints John Doerr to Board of Directors

April 5, 2013 Photo Release -- Zynga Appoints John Doerr to Board of Directors SAN FRANCISCO, April 5, 2013 (GLOBE NEWSWIRE) -- Zynga Inc. (Nasdaq:ZNGA), the world's leading social game developer, announced today that John Doerr, General Partner of Kleiner Perkins Caufield & Byers, joined the company's board of directors. A photo accompanying this release is available at http://www.globenewswire.com/newsroom/prs/?pkgid=17973. "John has been a supporter of Zynga since our early days, and truly understands our core values and mission," said Mark Pincus, CEO and Founder, Zynga. "John has worked with some of the most well-known companies in the world at every stage imaginable and his experience helping teams innovate at scale will be a tremendous asset for our leadership team. I'm personally looking forward to working closer with John, a true pioneer in the consumer internet space, and welcoming him to the board as a trusted advisor through this pivotal, transition year. John inspired us all to pursue creating internet treasures. He is a true missionary and will deepen and strengthen our DNA." "In just five years Zynga has connected hundreds of millions of people to their friends for fun. What's exciting is this is still day zero — just the beginning -- of social gaming's potential," said John Doerr, General Partner, Kleiner Perkins Caufield & Byers. "With its deep talent and multi-platform technology, and millions of happy customers, Zynga will engage more of us wherever we play — whether on the web, phones or tablets. I'm excited about working with Mark and the Zynga team in its next chapters of growth." John Doerr, general partner at Doerr joined KPCB in 1980, and has backed some of the world's most successful Kleiner Perkins Caufield & companies, including Google Inc. -

Innovalue #Payments

Innovalue #payments INSIGHT | OPINION Vol 6 • Q1 2014 Host Card Emulation: The wings of NFC payments Mirko Krauel, Both approaches are currently not have to be commercially orchestrated, and Principal broadly successful in the market due to a (4) the different players “fight” for the custom- number of reasons. The following article will er ownership. Erik Heimbächer, focus on mobile payment solutions based on The above-mentioned challenges are Associate traditional schemes and will describe how especially true between Mobile Network HCE could revitalize this strategic approach. Operators (MNOs) and issuers since MNOs are gate keepers with reference to the SIM. Issuers The non-breakthrough of Mobile Payments who intend on getting a payment card into For a rather long time already, companies with Bone of contention: the secure element the mobile phone have to arrange coopera- diverse industry backgrounds have worked on Mobile payment solutions based on tradition- tion with multiple telecommunication enabling mobile payments using smartphones al payment schemes are currently storing sen- providers. For granting access to the SIM, at the point of sale (POS). In this context, two sitive payment data on a tamper resistant lo- often MNOs expect e.g. revenue shares or blue-print strategies can be observed in the cation, broadly known as the secure element. customer access. market: (1) the set-up of proprietary, self-con- Different types of secure elements are possi- tained mobile payment ecosystems, and (2) ble (e.g. smartphone embedded, microSD "HCE has the potential to the set-up of mobile payment solutions based card, SIM card), but in fact the secure ele- unlock innovation in the NFC on traditional schemes. -

(Anti) Social Media

Facing down Facebook Reclaiming democracy in the age of (anti) social media a Report for the office of molly scott cato mep by tom scott FOREWORD BY MOLLY SCOTT CATO MEP 2 3.2 INVESTIGATION INTO THE USE OF DATA ANALYTICS IN POLITICAL CAMPAIGNS BY contents EXECUTIVE SUMMARY 3 THE UK INFORMATION COMMISSIONER’S 1.0 INTRODUCTION 5 OFFICE 29 2.0 FACEBOOK’S RISE TO GLOBAL 3.2.1 BACKGROUND 29 DOMINANCE 8 3.2.2 TRANSPARENCY 29 2.1 MOVE FAST AND BREAK THINGS’ 8 3.2.3 USES OF DATA FOR POLITICAL ADVERTISING 30 2.2 RHETORIC OF OPENNESS AND 3.2.4 OUTCOMES AND CONCLUSIONS 30 INCLUSIVITY 9 3.3 DEMOCRACY UNDER THREAT: RISKS AND 2.3 MONETISING PERSONAL DATA 10 SOLUTIONS IN THE ERA OF DISINFORMATION 2.4 THE SOCIAL GRAPH: TURNING AND DATA MONOPOLY. REPORT OF THE PEOPLE INTO ‘INVENTORY’ 10 STANDING COMMITTEE ON ACCESS 2.5 PRIVACY ISSUES PROLIFERATE 12 TO INFORMATION, PRIVACY AND ETHICS OF THE CANADIAN 2.6 TRUST US, WE’VE CHANGED 13 PARLIAMENT 31 2.7 THE ‘OPEN GRAPH’ AND THE 3.3.1 BACKGROUND 31 GROWING BACKLASH 14 3.3.2 AGGREGATEIQ AND FACEBOOK DATA 32 2.8 THE ‘INSIDER PIG PILE’: FACEBOOK GOES PUBLIC 16 3.3.3 STRUCTURAL PROBLEMS IN THE ‘INFORMATION ECOSYSTEM’ 32 2.9 INSATIABLE DEMAND FOR GROWTH 17 3.3.4 TRANSPARENCY IN ONLINE 2.10 TRUST US, THIS TIME WE’VE REALLY ADVERTISING 33 CHANGED 19 3.3.5 ALGORITHMIC TRANSPARENCY AND 2.11 TRADING DATA FOR REVENUE 19 RESPONSIBILITY FOR CONTENT 33 2.12 BIGGER THAN ANY RELIGION 20 3.3.6 REGULATION OF MONOPOLY POWER 34 3.0 THE ATTACK ON DEMOCRACY: 3.3.7 INADEQUACY OF SELF-REGULATION 34 RECENT FINDINGS 22 3.4 FACEBOOK SCRUTINISED BY EU 3.1. -

Reality Check Facebook, Inc

Reality Check Facebook, Inc. NASDAQ: FB January 24, 2019 “unequivocally wrong” “completely wrong” “not based on any facts or research” —Facebook, Inc. Author Aaron Greenspan Disclosures Aaron Greenspan owns FB put options in his personal capacity. He entered into a confidential settlement with Mark Zuckerberg and Facebook, Inc. in 2009. Legal Notices Copyright © 2018-2019 Think Computer Corporation. All Rights Reserved. PlainSite is a registered trademark of Think Computer Corporation. This report is not legal or investment advice. Trade at your own risk. About PlainSite® PlainSite is a legal research initiative jointly run by Think Computer Corporation, a for-profit computer software company, and Think Computer Foundation, a 501(c)(3) non-profit organization. The PlainSite website at https://www.plainsite.org hosts information regarding over eleven million court dockets, as well as millions of documents and government records from federal and state entities. Think Computer Foundation, which also sponsors activities for individuals with disabilities in the Cleveland area, is funded in part by donations from Think Computer Corporation. Visit the Facebook, Inc. PlainSite profile at https://www.plainsite.org/profiles/facebook-inc/. Read our other Reality Check reports at http://www.plainsite.org/realitycheck/. Contact For PlainSite Pro Investor paid early access to future reports, questions, or comments, contact us by e-mail at [email protected]. Executive Summary On paper, Facebook, Inc. (NASDAQ: FB) is one of the most successful companies in history. With a market capitalization that peaked at over $600 billion, Facebook has been the envy of blue chip executives, entrepreneurs, and FB Price Per Share venture capitalists since it exploded onto the global stage. -

Glossary of Key Sharing Economy Terms

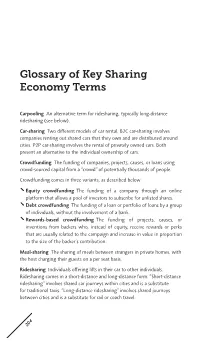

Glossary of Key Sharing Economy Terms Carpooling An alternative term for ridesharing, typically long-distance ridesharing (see below). Car-sharing Two different models of car rental. B2C car-sharing involves companies renting out shared cars that they own and are distributed around cities. P2P car-sharing involves the rental of privately owned cars. Both present an alternative to the individual ownership of cars. Crowdfunding The funding of companies, projects, causes, or loans using crowd-sourced capital from a “crowd” of potentially thousands of people. Crowdfunding comes in three variants, as described below. Equity crowdfunding The funding of a company through an online platform that allows a pool of investors to subscribe for unlisted shares. Debt crowdfunding The funding of a loan or portfolio of loans by a group of individuals, without the involvement of a bank. Rewards-based crowdfunding The funding of projects, causes, or inventions from backers who, instead of equity, receive rewards or perks that are usually related to the campaign and increase in value in proportion to the size of the backer’s contribution. Meal-sharing The sharing of meals between strangers in private homes, with the host charging their guests on a per seat basis. Ridesharing Individuals offering lifts in their car to other individuals. Ridesharing comes in a short-distance and long-distance form. “Short-distance ridesharing” involves shared car journeys within cities and is a substitute for traditional taxis. “Long-distance ridesharing” involves shared journeys between cities and is a substitute for rail or coach travel. 204 Glossary of Key Sharing Economy Terms 205 Sharing economy (condensed version) The value in taking underutilized assets and making them accessible online to a community, leading to a reduced need for ownership of those assets. -

Facebookfrom Wikipedia, the Free Encyclopediajump To: Navigation, Search This Article Is About the Website

FacebookFrom Wikipedia, the free encyclopediaJump to: navigation, search This article is about the website. For the collection of photographs of people after which it is named, see Facebook (directory(directory).). Facebook, Inc. Type Private Founded Cambridge, MassachusettsMassachusetts[1][1] (2004 (2004)) Founder Mark Zuckerberg Eduardo Saverin Dustin Moskovitz Chris Hughes HeadquarterHeadquarterss Palo Alto, California, U.S., will be moved to MenMenlolo Park, California, U.S. in June 2011 Area served Worldwide Key people Mark Zuckerberg (CEO) Chris Cox (VP of Product) Sheryl Sandberg (COO) Donald E. Graham (Chairman) Revenue US$800 mmillionillion (2009 est.)[2] Net income N/A This website stores data such as cookies to enableEmployees essential 2000+(2011)[3] site functionality, as well as marketing, personalization,Website and analytics. facebook.com You may change your settings at any time or accept theIPv6 default support settings. www.v6.fawww.v6.facebook.comcebook.com Alexa rank 2 (Ma(Marchrch 2011[upda2011[update][4])te][4]) Privacy Policy Type of site Social networking service Marketing PersonalizationAdvertising Banner ads, referral marketing, casual games AnalyticsRegistration Required Save Accept All Users 600 million[5][6] (active in January 2011) Available in Multilingual Launched February 4, 2004 Current status Active Screenshot[show] Screenshot of Facebook's homepage Facebook (stylized facebook) is a social networking service and website launched in February 2004, operated and privately owned by Facebook, Inc.[1] As of January 2011[update], Facebook has more than 600 million active users.[5][6] Users may create a personal profile, add other users as friends, and exchange messages, including automatic notifications when they update their profile. -

Transportation Network Companies

Transportation Network Companies Testimony of Ginger Goodin, P.E. Senior Research Engineer and Director, Transportation Policy Research Center and Maarit Moran Associate Transportation Researcher Texas A&M Transportation Institute to the Texas Senate Committee on Business and Commerce March 14, 2017 Introduction Chairman Hancock and Members, I am Ginger Goodin, Director of the Texas A&M Transportation Institute Policy Research Center, and I am joined today by Maarit Moran, TTI Associate Transportation Researcher and Principal Investigator of the research to be discussed at this hearing. In your briefing material is a map summarizing the nationwide legislation enacted to authorize and regulate transportation network companies through March 1, 2017. Background Since 2010, a number of private companies have entered the transportation services market by offering new travel options that use digital technology to provide an on-demand and highly automated private ride service. The most well-known of the transportation network companies, or TNCs, as these companies are frequently classified, may be Uber and Lyft, although there are many companies operating in this arena. TNCs have expanded rapidly in cities worldwide. However, they do not fit neatly into current regulatory schemes and have caused some disruption in the transportation marketplace. We take no position regarding any desirability or lack thereof of regulating TNCs at any level of government. Our purpose is to help policy makers navigate the inherent policy considerations. To that end, we examined laws and lawmaking efforts in other states as well as regulatory efforts in a number of Texas cities, and we compiled the state-level information into an easily accessed interactive online map.