Scheme Booklet Supplement This Booklet Contains a Copy of the Independent Expert’S Report, Investigating Accountant’S Report and the Scheme Implementation Agreement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report and Financial Statements 2018 Sainsbury’S Group Helping Customers Live Well for Less Has Been at the Heart of What We Do Since 1869

Live Well For Less Annual Report and Financial Statements 2018 Sainsbury’s Group Helping customers live well for less has been at the heart of what we do since 1869. We employ over 185,000 colleagues who work hard every day to make our customers’ lives easier and to provide them with great products, quality and service whenever and wherever it is convenient to access them. Food Our strategic focus is to help 608 our customers live well for less. Sainsbury’s supermarkets We offer customers quality and convenience as well as great value. Our distinctive ranges and innovative 102 partnerships differentiate stores offering Same Day our offer. More customers delivery to 40 per cent are shopping with us than of the UK population ever before and our share of customer transactions has increased. See more on page 12 General Merchandise 191 and Clothing Argos stores in Sainsbury’s We are one of the largest general supermarkets merchandise and clothing retailers in the UK, offering a wide range of products across our Argos, Sainsbury’s Home and 16 Habitat brands, in stores and Habitat stores and online. We are a market leader in Click & Collect available toys, electricals and technology in over 2,300 locations and Tu clothing offers high street style at supermarket prices. See more on page 14 Financial Services Financial Services are an 3.9m integral part of our business. Active customers Sainsbury’s Bank offers at Sainsbury’s Bank and accessible products such as Argos Financial Services credit cards, insurance, travel money and personal loans that reward loyalty. -

December 2017 Month in Review Contents

December 2017 Month in Review Contents Feature – 2017 The year in review 3 QS corner 4 Commercial - Retail 6 Residential 23 Rural 62 Market Indicators 74 Disclaimer This publication presents a generalised overview regarding the state of Australian property markets using property market risk-ranking scales. It is not a guide to individual property assessments and should not be relied upon. Herron Todd White accepts no responsibility for any reliance placed on the commentary and generalised information. Contact Herron Todd White to obtain formal, specific property advice on any matters of interest arising from this publication. All rights reserved. This report can not be reproduced or distributed without written permission of Herron Todd White. Month in Review December 2017 2017 - The year in review We’re about to bring down the shutters on a year full of action. Most of us hoped world events in 2017 would The surprise dark horse in the mix was probably This is also the time of year when we ask our offices provide of less surprises compared to its tumultuous Hobart. Our Apple Isle capital was rediscovered to look back at their hit predictions from February’s predecessor. We’re not sure 2017 delivered in terms by buyers as high yields and beautiful properties, “Year Ahead” issue and tell us how they went. As of a quiet one, but perhaps the new normal has set in coupled with a general economic strengthening, usual, some will be hits – but others will be misses. and we’re all recalibrating our compass. The year still united. The city saw substantial gains in both growth Why not read through and check out each office’s had its moments of tension, brinkmanship and awe and yields in 2017. -

Kaufland Australia Proposed Store Mornington, Melbourne Economic Impact Assessment

Kaufland Australia Proposed store Mornington, Melbourne Economic Impact Assessment November 2018 Prepared by: Anthony Dimasi, Managing Director – Dimasi & Co [email protected] Prepared for Kaufland Australia Table of contents Executive summary 1 Introduction 5 Section 1: The supermarket sector – Australia and Victoria 6 Section 2: Kaufland Australia – store format and offer 13 Section 3: Economic Impact Assessment 20 3.1 Site location and context 21 3.2 Trade area analysis 23 3.3 Competition analysis 27 3.4 Estimated sales potential 28 3.5 Economic impacts 30 3.6 Net community benefit assessment 43 Executive summary The Supermarkets & Grocery Stores category is by far the most important retail category in Australia. Total sales recorded by Supermarkets & Grocery Stores as measured by the Australian Bureau of Statistics have increased from $64.5 billion at 2007 to $103.7 billion at 2017, recording average annual growth of 4.9% per annum – despite the impacts of the global financial crisis (GFC). Over this past decade the category has also increased its share of total Australian retail sales from 31.3% to 33.7%. For Victoria, similar trends are evident. Supermarkets and grocery stores’ sales have increased over the past decade at a similar rate to the national average – 4.5% versus 4.9%. The share of total retail sales directed to supermarkets and grocery stores by Victorians has also increased over this period, from 31.6% at 2007 to 32.8% at 2017. Given the importance of the Supermarkets & Grocery Stores category to both the Victorian retail sector and Victorian consumers, the entry of Kaufland into the supermarket sector brings with it enormous potential for significant consumer benefits, as well as broader economic benefits. -

Download Paper

Variations in supplier relations operating within voluntary groups; historical perspectives on relationships and social justice in the independent retail sector . Keith Jackson, Doctoral Candidate, University of Cumbria Professor Helen Woodruffe-Burton, Newcastle Business School, Northumbria University Abstract The convenience store sector evolved from the variety of small retailers operating in the 1950’s and is still dominated (in store numbers) by SMEs operating smaller stores (usually smaller than 3,000 sq ft.); trading extended hours; with a base around confectionary, tobacco and news (CTN) and off licence. In the 1980s as more independent retailers adopted the new convenience format the convenience sector spread geographically to fill the increasing demand for local stores with extended hours. Once geographic saturation was reached the main independent supply chains within the convenience sector adopted either a broadly coordinated embedded network through voluntary symbol groups or a broadly cooperative supply chain through cash and carries and delivered wholesalers. Various writers have argued that networking and the building of social capital (as in the voluntary symbol groups) is vital for SME growth whilst Jack and Anderson (2002) have demonstrated that entrepreneurs embedding themselves within a network may be sacrificing their entrepreneurial capabilities. Around 2000, the major retail multiples and the COOP entered the convenience sector. By using their extensive knowledge of Supply Chain Management (SCM) they were able to gain commercial advantage over the existing supply chains which focused these chains on the need for economic efficiency. This meant that the businesses within the voluntary groups had to choose between the mechanisms highlighted by Payan (2000) of economic efficiency with increased dependence on the centre and the mechanisms of social justice within the group that allowed independent actions within the group. -

Supermarket Refrigeration Going Natural

cover story >>> SEAN McGOWAN REPORTS Supermarket refrigeration going natural In 2005, Coles Supermarkets opened its first ‘environmental concept’ supermarket featuring a cascade carbon dioxide refrigeration system. Two years on the technology has undergone significant improvement to better serve the local market, while internationally it promises to receive widespread adoption by the world’s retail heavyweights, as Sean McGowan reports. Supermarket refrigeration accounts for a significant 1% of Australia’s total electricity consumption, and this figure is reported to be higher in Europe and the United States. Therefore, its not surprising to find supermarket chains worldwide clamoring to adopt new technology which promises to cut their energy costs, while at the same time, address their corporate responsibilities to the environment and the communities who shop with them. The knight in shining armour looks set to be carbon dioxide (CO2) refrigeration systems, which are often used in a cascade design with fluorocarbon refrigerants such as R507 or R134a. A cascade system using ammonia is also on the agenda according to one of Australia’s leading supermarket refrigeration specialists, Frigrite Refrigeration. “We have traveled the world investigating system design and have developed solutions that best suit the Australian market. We installed the first CO2 systems in Australia, with another four systems installed in new supermarkets since,” says Andrew Reid, national account manager for Frigrite. “Due to economic constraints, the cascade CO2 systems installed in Australia best suit the energy and environmental expectations, however, further development is underway in finding improvements to the current concepts, which may involve a fundamental system design change and alternate refrigerants to those currently being used.” Reid says supermarket chains have acknowledged the importance of meeting environmental and community expectations as the general awareness of these two aspects increases. -

Hypermarket Lessons for New Zealand a Report to the Commerce Commission of New Zealand

Hypermarket lessons for New Zealand A report to the Commerce Commission of New Zealand September 2007 Coriolis Research Ltd. is a strategic market research firm founded in 1997 and based in Auckland, New Zealand. Coriolis primarily works with clients in the food and fast moving consumer goods supply chain, from primary producers to retailers. In addition to working with clients, Coriolis regularly produces reports on current industry topics. The coriolis force, named for French physicist Gaspard Coriolis (1792-1843), may be seen on a large scale in the movement of winds and ocean currents on the rotating earth. It dominates weather patterns, producing the counterclockwise flow observed around low-pressure zones in the Northern Hemisphere and the clockwise flow around such zones in the Southern Hemisphere. It is the result of a centripetal force on a mass moving with a velocity radially outward in a rotating plane. In market research it means understanding the big picture before you get into the details. PO BOX 10 202, Mt. Eden, Auckland 1030, New Zealand Tel: +64 9 623 1848; Fax: +64 9 353 1515; email: [email protected] www.coriolisresearch.com PROJECT BACKGROUND This project has the following background − In June of 2006, Coriolis research published a company newsletter (Chart Watch Q2 2006): − see http://www.coriolisresearch.com/newsletter/coriolis_chartwatch_2006Q2.html − This discussed the planned opening of the first The Warehouse Extra hypermarket in New Zealand; a follow up Part 2 was published following the opening of the store. This newsletter was targeted at our client base (FMCG manufacturers and retailers in New Zealand). -

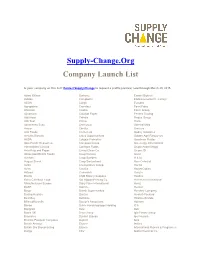

Supply-Change.Org Company Launch List

Supply-Change.Org Company Launch List Is your company on this list? Contact Supply Change to request a profile preview, now through March 25, 2015. Adani Wilmar Burberry Emami Biotech Adidas Campbell's Etablissements Fr. Colruyt AEON Cargill Eurostar Agropalma Carrefour Farm Frites Ahlstrom Casino Fazer Group Ajinomoto Catalyst Paper Ferrero Trading Aldi Nord Cefetra Findus Group Aldi Sud Cémoi Florin Almacenes Exito Cencosud General Mills Amcor Cérélia Ginsters Arla Foods Coca-Cola Godrej Industries Arnott's Biscuits Coles Supermarkets Golden Agri-Resources ASDA Colgate-Palmolive Goodman Fielder Asia Pacific Resources Compass Group Greenergy International International Limited ConAgra Foods Grupo André Maggi Asia Pulp and Paper Co-op Clean Co. Grupo JD Associated British Foods Coop Norway Gucci Auchan Coop Sweden H & M August Storck Coop Switzerland Hain Celestial Aviko Co-operative Group Haribo Avon CostCo HarperCollins Axfood Cranswick Harry's Barilla CSM Bakery Supplies Hasbro Barry Callebaut Food Dai Nippon Printing Co. Heineken International Manufacturers Europe Dairy Farm International Heinz BASF Danone Henkel Bayer Dansk Supermarked Hershey Company Beijing Hualian Danzer Hewlett-Packard Best Buy Delhaize Hillshire Brands BillerudKorsnäs Doctor's Associates Holmen Bimbo Dohle Handelsgruppe Holding ICA Bongrain Dow IGA Boots UK Drax Group Iglo Foods Group Brambles Dunkin' Brands Igor Novara Brioche Pasquier Cerqueux Dupont Ikea British Airways Ecover Inditex British Sky Broadcasting Elanco International Flavors & Fragrances Bunge -

The More Things Change, the More They Stay the Same

YEARS 2003-2013 Issue 15 × 2013 September 28 - October 10 YOUR FREE COPY THE ESSENTIAL GUIDE TO LIFE, TRAVEL & ENTERTAINMENT IN ICELAND NEWS POLITICS FILM MUSIC TRAVEL Jóhanna The gender-based Lots and lots of Bam brings us We let fish suck on Sigurðardóttir wage gap widens :( RIFF! “Random Hero” our toes… SPEAKS! 5 year anniversary of the collapse 2008- 2013 THE MORE THINGS CHANGE, THE MORE THEY STAY THE SAME... Complete Lots of Download the FREE Grapevine Appy Hour app! Reykjavík Listings cool events Every happy hour in town in your pocket. + Available on the App store and on Android Market. The Reykjavík Grapevine Issue 15 — 2013 2 Editorial | Anna Andersen TRACK OF THE ISSUE ICELANDISTAN 5.0 Anna’s 32nd Editorial have wreaked more havoc on this country than land in the foreign media. anything that’s not directly caused by a natural So much emphasis has been put on this (only disaster. Our economy has been reduced to the possible) course of action that Icelanders them- standards of Eastern Europe at end of the Cold selves have perhaps forgotten what else the new War. As a nation, we are more or less bankrupt.” government has done to stem the rippling effects Almost overnight, our tiny island nation in the of the crash, not to mention all of the events that middle of the North Atlantic became the poster- led up to it. This would at least explain why Ice- child for the global economic crisis—a shiny ex- landers recently returned to power the very same ample of how to do everything wrong. -

Kaupthing Bank

Kaupthing Bank - COMPANY UPDATE - HOLD Rating Summary and Conclusions Equity value 223,7 bn.ISK Kaupthing Bank acquires FIH Price 407,9 Kaupthing Bank (KB banki) has reached an agreement with Forenings Sparbanken (Swedbank) to Closing price 23.06.2004 429,5 purchase FI Holding, the holding company of the Danish corporate bank FIH. The purchase price amounts to ISK 84 billion (EUR 1,000 million), in addition to which Swedbank will retain part of Contents FIH's own equity. The acquisition will be financed with the issue of new share capital to holders of pre-emptive rights, as well as through subordinated debt. The price-to-book ratio for the Summary and Conclusions.........................................................1 transaction is 1.6. Kaupthing Bank acquires FIH....................................................2 Payment..................................................................................2 FIH is the third-largest bank in Danmark, with total assets close to ISK 800 bn at the end of Q1. It Financing.........................................................................2 was established in 1954 by the Danish state to encourage growth and development of Danish FIH...............................................................................................2 industry. FIH's activities are almost exclusively corporate lending. It holds a 17% share of the Danish Effect on group operations and value...................................3 corporate market and has around 5,000 customers, half of whom have been dealing with the -

“Art Is in Our Heart”

“ART IS IN OUR HEART”: TRANSNATIONAL COMPLEXITIES OF ART PROJECTS AND NEOLIBERAL GOVERNMENTALITY _____________________________________________ A Dissertation Submitted to the Temple University Graduate Board _____________________________________________ in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy _____________________________________________ By G.I Tinna Grétarsdóttir January, 2010 Examining Committee Members: Dr. Jay Ruby, Advisory Chair, Anthropology Dr. Raquel Romberg, Anthropology Dr. Paul Garrett, Anthropology Dr. Roderick Coover, External Member, Film and Media Arts, Temple University. i © Copyright 2010 by G.I Tinna Grétarsdóttir All Rights Reserved ii ABSTRACT “ART IS IN OUR HEART”: TRANSNATIONAL COMPLEXITIES OF ART PROJECTS AND NEOLIBERAL GOVERNMENTALITY By G.I Tinna Grétarsdóttir Doctor of Philosophy Temple University, January 2010 Doctoral Advisory Committee Chair: Dr. Jay Ruby In this dissertation I argue that art projects are sites of interconnected social spaces where the work of transnational practices, neoliberal politics and identity construction take place. At the same time, art projects are “nodal points” that provide entry and linkages between communities across the Atlantic. In this study, based on multi-sited ethnographic fieldwork in Canada and Iceland, I explore this argument by examining ethnic networking between Icelandic-Canadians and the Icelandic state, which adopted neoliberal economic policies between 1991 and 2008. The neoliberal restructuring in Iceland was manifested in the implementation of programs of privatization and deregulation. The tidal wave of free trade, market rationality and expansions across national borders required re-imagined, nationalized accounts of Icelandic identity and society and reconfigurations of the margins of the Icelandic state. Through programs and a range of technologies, discourses, and practices, the Icelandic state worked to create enterprising, empowered, and creative subjects appropriate to the neoliberal project. -

Close Encounter Chanel’S Mobile Art Mother Ship Has Landed in Central Park

▲ NEWS: ▲ Ann FASHION: ▲ RETAIL: Taylor Contemporary ▲ NEWS: Topshop taps brands Susan goes design, feel the Sokol bigger in store squeeze, to exit Tokyo, heads, page 9. Vera page 3. Wang, page 3. page 3. WWDWomen’s Wear Daily • TheTHURSDAY Retailers’ Daily Newspaper • October 16, 2008 • $3.00 Sportswear Close Encounter Chanel’s Mobile Art mother ship has landed in Central Park. The futuristic, Zaha Hadid-designed pavilion, which houses 18 modern artists’ odes to the iconic Chanel 2.55 handbag, will open to the public on Monday. For more on the installation, see pages 6 and 7. Bleak House: Retail Shares Dive Again as Outlook Darkens By David Moin and Evan Clark On a day marked by disappointments in which it has issued them, and the Credit jitters have given way to on several fronts, the Commerce weakness recently seen in retail shares holiday dread. Department reported declines in swept over the vendor community, led by The severity of the retail downturn nearly every category of retail sales in a nearly 30 percent drop in the price of was on full display Wednesday, in the September, including department and Jones Apparel Group Inc. shares. Jones process further depressing already specialty stores; the National Retail reduced its earnings estimates for the downtrodden stocks and anemic Federation issued its lowest forecast year after the market closed Tuesday. holiday expectations. for holiday spending in the seven years See More, Page 17 PHOTO BY TALAYA CENTENO TALAYA PHOTO BY WWD.COM WWDTHURSDAY Sportswear FASHION 6 Karl Lagerfeld and Zaha Hadid’s Space-Age spin ™ on portable structures, Chanel’s Mobile Art pavil- ion, has touched down in Central Park. -

1 Background

1 Background 1.1 Introduction There has been significant public concern regarding the competitiveness of retail prices in the grocery industry in Australia and the pricing of household grocery products. In particular there is concern that Australia has a highly concentrated grocery industry, and while inflation has been low in Australia over the last few years, grocery food prices have increased at a significantly higher rate than the headline inflation rate. In response to these concerns, the Assistant Treasurer and Minister for Competition Policy and Consumers Affairs wrote to the Australian Competition and Consumer Commission (ACCC) on 22 January 2008, directing the ACCC to hold a public inquiry under Part VIIA of the Trade Practices Act 1974 (the Act) into the competitiveness of retail prices for standard groceries. A copy of this letter is at appendix A. 1.2 Terms of reference The instrument attached to the Assistant Treasurer and Minister for Competition Policy and Consumers Affairs’ letter stated: I, Chris Bowen, Assistant Treasurer and Minister for Competition Policy and Consumer Affairs, pursuant to section 95H(2) the Trade Practices Act 1974, hereby require the Australian Competition and Consumer Commission to hold an inquiry into the competitiveness of retail prices for standard groceries. Matters to be taken into consideration by the inquiry shall include, but not be restricted to: • the current structure of the grocery industry at the supply, wholesale and retail levels including mergers and acquisitions by the national retailers