Poly Property Group Co., Limited 保利置業集團有限公司 (Incorporated in Hong Kong with Limited Liability) (Stock Code: 119)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

5G for Trains

5G for Trains Bharat Bhatia Chair, ITU-R WP5D SWG on PPDR Chair, APT-AWG Task Group on PPDR President, ITU-APT foundation of India Head of International Spectrum, Motorola Solutions Inc. Slide 1 Operations • Train operations, monitoring and control GSM-R • Real-time telemetry • Fleet/track maintenance • Increasing track capacity • Unattended Train Operations • Mobile workforce applications • Sensors – big data analytics • Mass Rescue Operation • Supply chain Safety Customer services GSM-R • Remote diagnostics • Travel information • Remote control in case of • Advertisements emergency • Location based services • Passenger emergency • Infotainment - Multimedia communications Passenger information display • Platform-to-driver video • Personal multimedia • In-train CCTV surveillance - train-to- entertainment station/OCC video • In-train wi-fi – broadband • Security internet access • Video analytics What is GSM-R? GSM-R, Global System for Mobile Communications – Railway or GSM-Railway is an international wireless communications standard for railway communication and applications. A sub-system of European Rail Traffic Management System (ERTMS), it is used for communication between train and railway regulation control centres GSM-R is an adaptation of GSM to provide mission critical features for railway operation and can work at speeds up to 500 km/hour. It is based on EIRENE – MORANE specifications. (EUROPEAN INTEGRATED RAILWAY RADIO ENHANCED NETWORK and Mobile radio for Railway Networks in Europe) GSM-R Stanadardisation UIC the International -

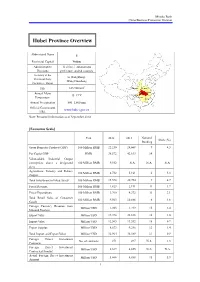

Hubei Province Overview

Mizuho Bank China Business Promotion Division Hubei Province Overview Abbreviated Name E Provincial Capital Wuhan Administrative 12 cities, 1 autonomous Divisions prefecture, and 64 counties Secretary of the Li Hongzhong; Provincial Party Wang Guosheng Committee; Mayor 2 Size 185,900 km Shaanxi Henan Annual Mean Hubei Anhui 15–17°C Chongqing Temperature Hunan Jiangxi Annual Precipitation 800–1,600 mm Official Government www.hubei.gov.cn URL Note: Personnel information as of September 2014 [Economic Scale] Unit 2012 2013 National Share (%) Ranking Gross Domestic Product (GDP) 100 Million RMB 22,250 24,668 9 4.3 Per Capita GDP RMB 38,572 42,613 14 - Value-added Industrial Output (enterprises above a designated 100 Million RMB 9,552 N.A. N.A. N.A. size) Agriculture, Forestry and Fishery 100 Million RMB 4,732 5,161 6 5.3 Output Total Investment in Fixed Assets 100 Million RMB 15,578 20,754 9 4.7 Fiscal Revenue 100 Million RMB 1,823 2,191 11 1.7 Fiscal Expenditure 100 Million RMB 3,760 4,372 11 3.1 Total Retail Sales of Consumer 100 Million RMB 9,563 10,886 6 4.6 Goods Foreign Currency Revenue from Million USD 1,203 1,219 15 2.4 Inbound Tourism Export Value Million USD 19,398 22,838 16 1.0 Import Value Million USD 12,565 13,552 18 0.7 Export Surplus Million USD 6,833 9,286 12 1.4 Total Import and Export Value Million USD 31,964 36,389 17 0.9 Foreign Direct Investment No. -

Evergrande Real Estate Group Limited 恒 大 地 產 集 團 有 限 公 司 (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 3333)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. Evergrande Real Estate Group Limited 恒 大 地 產 集 團 有 限 公 司 (Incorporated in the Cayman Islands with limited liability) (Stock Code: 3333) DISCLOSEABLE TRANSACTION The Board announces that on 2 December 2015, Shengyu (BVI) Limited, a wholly-owned subsidiary of the Company, as the purchaser, entered into three agreements respectively with the Vendor, pursuant to which the Purchaser agreed to acquire the interests in the relevant shares in and loans to the target companies held by the Vendor. These target companies hold the interests in the Haikou Project, the Huiyang Project and two projects located in Wuhan. Since the Vendor is the seller in these three agreements, such agreements will be aggregated in accordance with Rule 14.22 of the Listing Rules. As the applicable percentage ratios for the Acquisition exceed 5% but are less than 25%, the Acquisition constitutes a discloseable transaction for the Company under Chapter 14 of the Listing Rules and is subject to the reporting and announcement requirements under Chapter 14 of the Listing Rules. 1. INTRODUCTION The Board announces that on 2 December 2015, Shengyu (BVI) Limited, a wholly-owned subsidiary of the Company, as the purchaser, entered into three agreements respectively with the Vendor, pursuant to which the Purchaser agreed to acquire the interests in the relevant shares in and loans to the target companies held by the Vendor. -

High Speed Rail: Wuhan Urban Garden 5-Day Trip

High Speed Rail: Wuhan Urban Garden 5-Day Trip Day 1 Itinerary Suggested Transportation Hong Kong → Wuhan High Speed Rail [Hong Kong West Kowloon Station → Wuhan Railway Station] To hotel: Recommend to stay in a hotel by the river in Wuchang District. Metro: From Wuhan Railway Hotel for reference: Station, take Metro Line 4 The Westin Wuhan Wuchang Hotel towards Huangjinkou. Address: 96 Linjiang Boulevard, Wuchang District, Wuhan Change to Line 2 at Hongshan Square Station towards Tianhe International Airport. Get off at Jiyuqiao Station and walk for about 7 minutes. (Total travel time about 46 minutes) Taxi: About 35 minutes. Enjoy lunch near the hotel On foot: Walk for about 5 minutes Restaurant for reference: Zhen Bafang Hot Pot from the hotel. Address: No. 43 & 44, Building 12-13, Qianjin Road, Wanda Plaza, Jiyu Bridge, Wuchang District, Wuhan Stand the Test of Time: Yellow Crane Tower Bus: Walk for about 4 minutes from the restaurant to Jiyuqiao Metro Station. Take bus 804 towards Nanhu Road Jiangnan Village. Get off at Yue Ma Chang Station and walk for about 6 minutes. (Total travel time about 37 minutes) Taxi: About 15 minutes. Known as “The No. 1 Tower in the World”, the Yellow Crane Tower is a landmark for Wuhan City and Hubei Province and a must-see attraction. The tower was built in the Three Kingdoms era and was named after its erection on Huangjiji, a submerged rock. Well-known ancient characters such as Li Bai, Bai Juyi, Lu You and Yue Fei had all referenced the tower in their poetry works. -

Use Style: Paper Title

2019 4th International Conference on Education and Social Development (ICESD 2019) ISBN: 978-1-60595-621-3 Wuhan Subway Economic Development in the Perspective of "Innovation, Coordination, Green, Open, Sharing" Concept 1,a 2,b, Fang WANG and Xiao-sheng LEI * 1Hubei University of Traditional Chinese Medicine, Wuhan, Hubei, China 2Hubei University of Traditional Chinese Medicine, Wuhan, Hubei, China [email protected], [email protected] *Corresponding author Keywords: Development Concept, Wuhan, Subway Economy. Abstract. Since the 18th congress of the communist party of China, the "innovation, coordination, green, open and shared" development concept has been a profound change in the overall situation of China's development. In this context, the Wuhan Metro has developed rapidly, This paper analyzes the current situation, characteristics and influence of the development of subway economy in Wuhan from the perspective of development concept, and puts forward some suggestions for the future development of subway economy. Introduction For a long time, China has faced problems such as uneven, inadequate, uncoordinated and unsustainable development, and it has already faced the "ceiling dilemma". In recent years, China is facing the downward pressure of the economy. In order to change the development mode and solve the development problems, the 18th National Congress put forward five development concepts of “innovation, coordination, green, openness and sharing”, which have important guidance for the future development of social economy. Xiong'an New District is an innovative, coordinated, green ecological, open and co-constructed shared future urban model. Wuhan, following the glory of history, is becoming a reactivated city, and it must follow this development philosophy. -

Development of High-Speed Rail in the People's Republic of China

ADBI Working Paper Series DEVELOPMENT OF HIGH-SPEED RAIL IN THE PEOPLE’S REPUBLIC OF CHINA Pan Haixiao and Gao Ya No. 959 May 2019 Asian Development Bank Institute Pan Haixiao is a professor at the Department of Urban Planning of Tongji University. Gao Ya is a PhD candidate at the Department of Urban Planning of Tongji University. The views expressed in this paper are the views of the author and do not necessarily reflect the views or policies of ADBI, ADB, its Board of Directors, or the governments they represent. ADBI does not guarantee the accuracy of the data included in this paper and accepts no responsibility for any consequences of their use. Terminology used may not necessarily be consistent with ADB official terms. Working papers are subject to formal revision and correction before they are finalized and considered published. The Working Paper series is a continuation of the formerly named Discussion Paper series; the numbering of the papers continued without interruption or change. ADBI’s working papers reflect initial ideas on a topic and are posted online for discussion. Some working papers may develop into other forms of publication. Suggested citation: Haixiao, P. and G. Ya. 2019. Development of High-Speed Rail in the People’s Republic of China. ADBI Working Paper 959. Tokyo: Asian Development Bank Institute. Available: https://www.adb.org/publications/development-high-speed-rail-prc Please contact the authors for information about this paper. Email: [email protected] Asian Development Bank Institute Kasumigaseki Building, 8th Floor 3-2-5 Kasumigaseki, Chiyoda-ku Tokyo 100-6008, Japan Tel: +81-3-3593-5500 Fax: +81-3-3593-5571 URL: www.adbi.org E-mail: [email protected] © 2019 Asian Development Bank Institute ADBI Working Paper 959 Haixiao and Ya Abstract High-speed rail (HSR) construction is continuing at a rapid pace in the People’s Republic of China (PRC) to improve rail’s competitiveness in the passenger market and facilitate inter-city accessibility. -

Pengyuan Credit Rating (Hong Kong) Co.,Ltd

Property China Credit profiles to improve on lower land acquisitions and solid sales Contents Summary Summary ............................................ 1 Overall policy stance on property industry remains unchanged: we expect the Chinese governments will continue its tight control policies on Property sales ..................................... 2 property industry in 2019 to avoid unwanted overheating in the industry. In Land acquisition .................................. 4 our view, the governments will continue to clamp down the shadow banking financing in the industry and encourage the credit growth through more Property funding ................................. 6 regulated financing channels. On the other hand, with property price under Working capital efficiency ................... 7 control and inventory came off from its peak, a further severe tightening on the industry is unlikely, in our opinion. Industry consolidation ......................... 8 Residential property sales momentum likely to continue but at a slightly Profitability and Cash Flow ................. 9 softer pace: residential property sales value was better than the market Leverage .......................................... 10 expected in the first nine months of 2018, with property sales value rising 16% year over year, according to National Bureau of Statistics (NBS). We Sampled Property Issuers ................ 11 expect to see residential property sales value to grow around 10-15% in the Glossary ........................................... 13 fourth quarter of 2018, and continue to grow at around 10% in 2019, with 3- 4% growth in sales volume and 5-6% growth in average selling price (ASP). Land acquisitions to slow down further and market sentiment unlikely to rebound: we expect the land acquisition activities to continue slow down noticeably in 2019, with the land sale value to grow at around low teen level over the next 12 months. -

At the Forefront of China Property Dec 31, 2020

December 31, 2020 December Issue At the Forefront of China Property Opportunities emerging in Property Management Sector We believe value is emerging among small cap property management China Property companies. We believe Aoyuan Healthy Life is underappreciated by the Coverage Summary market, especially considering the recent completion of their major M&A Ticker Name Rating 0832.HK Central China Buy of the year (Easy Life). For Property Developers, Powerlong, Yuzhou and 3883.HK China Aoyuan Buy Redsun under our coverage have already achieved >96% of sales target. 1238.HK Powerlong Buy 3662.HK Aoyuan Healthy Life Buy Valuations Diverging among Property Management Companies 9983.HK Central China New Life Buy The flurry of new listings of property management companies in the last 2 0035.HK Far East Buy months have seen a major correction in the property management sector. 0017.HK New World Dev Buy Sector’s valuation has now retreated to 24.5x 12M Fwd P/E, below the 3-year 1996.HK Redsun Buy 1628.HK Yuzhou Buy historical mean. We believe market is struggling to differentiate the value 0095.HK LVGEM Buy proposition of different names and thus been sticking to large cap companies 6111.HK Dafa Hold backed by big name developers. This has resulted in a widening valuation gap 0230.HK Minmetals Hold between large-cap (47.7x P/E) and small-cap companies (19.5x P/E), offering Source: Company data, AMTD Research attractive investment opportunities. Fundamentals of some of these small-cap property management companies are unchanged, and the annual results in 30-city GFA growth momentum declined '000 sqm 30-city 7-day moving sum of GFA sold and YoY March 2021 will be positive catalysts to drive a re-rating, in our view. -

At the Forefront of China Property Fully Recovered from COVID-19, Back to the New Normal

November 27, 2020 November Issue At the Forefront of China Property Fully Recovered From COVID-19, Back to the New Normal We believe the property industry has fully recovered from the COVID-19 China Property impact by all measures. Property austerity measures such as price Coverage Summary restrictions, financing restrictions will limit growth and profitability, but Ticker Name Rating 0832.HK Central China Buy the industry is generating healthy cash flows which we believe is positive 3883.HK China Aoyuan Buy for credit. Aoyuan, Powerlong and CCRE are our top picks of the sector. 1238.HK Powerlong Buy 3662.HK Aoyuan Healthy Life Buy Returning back to the Property Austerity New Normal 9983.HK Central China New Life Buy We believe the termination of reorganization between Evergrande (3333 HK, 0035.HK Far East Buy NR) and Shenzhen Real Estate (000029 SZ, NR) during the past month 0017.HK New World Dev Buy reinforces the policy stance to contain developers’ debt and equity financing to 1996.HK Redsun Buy 1628.HK Yuzhou Buy prevent an overheated property market. Moreover, we have also noted that 0095.HK LVGEM Buy some cities have also tightened regulations on pre-approved new home prices 6111.HK Dafa Hold and pre-sale requirements to curb price growth momentum. This has resulted 0230.HK Minmetals Hold in 70-city new residential property price MoM growth to narrow to 0.2% in Nov Source: Company data, AMTD Research from 0.3% in Oct and 0.6% in Sep. YTD industry FCF YoY growth recorded positive Industry has fully recovered from COVID-19 impact 2017-2020 FCF YTD YoY 400% YTD industry cash flow YoY growth has returned to positive (+2.0%) for the 300% first time this year amid the pick-up in national contracted sales. -

Design Contest for Conceptual City in Northern Region of Guishan (Turtle Hill)

WUHAN City of history (the center for civilization of Yangtze River) Design contest for conceptual city in northern region of Guishan (Turtle Hill) THE HEART OF THE YANGTZE RIVER CIVILIZATION PRELIMINARY STUDY ON THE PLANNING Wuhan Land Resource and Planning Bureau April in 2018 Geographical Location of Wuhan Wuhan is briefly called “Han” and it is also named “riverside city”, being the capital of Hubei Province and the only sub-provincial division and megalopolis in six central provinces; it is the center city in Chinese central area, core city of Yangtze River Economic Zone, important national industrial base, scientific and educational base and comprehensive transportation junction and Wuhan combined service force guarantee base under Central Military Commission. The city has 13 municipal districts, three national development zones with a total area of 8494.41 square kilometers, and the number of permanent resident people was 10.7662 million and the urbanization rate of the city is 79.77% in 2016. Planning Background Wuhan is one of the second batch of national famous historical and cultural cities announced by State Council in 1986, and the city history can date back to Panlong City in Shang Dynasty 3500 years ago; it has a long history with many ancient relics and historical sites of modern times. Preparation and implementation for protection planning of famous historical and cultural Wuchang city has very important significance to enhance national cultural confidence, carry forward civilization of Yangtze River and revive the great -

METROS/U-BAHN Worldwide

METROS DER WELT/METROS OF THE WORLD STAND:31.12.2020/STATUS:31.12.2020 ّ :جمهورية مرص العرب ّية/ÄGYPTEN/EGYPT/DSCHUMHŪRIYYAT MISR AL-ʿARABIYYA :القاهرة/CAIRO/AL QAHIRAH ( حلوان)HELWAN-( المرج الجديد)LINE 1:NEW EL-MARG 25.12.2020 https://www.youtube.com/watch?v=jmr5zRlqvHY DAR EL-SALAM-SAAD ZAGHLOUL 11:29 (RECHTES SEITENFENSTER/RIGHT WINDOW!) Altamas Mahmud 06.11.2020 https://www.youtube.com/watch?v=P6xG3hZccyg EL-DEMERDASH-SADAT (LINKES SEITENFENSTER/LEFT WINDOW!) 12:29 Mahmoud Bassam ( المنيب)EL MONIB-( ش ربا)LINE 2:SHUBRA 24.11.2017 https://www.youtube.com/watch?v=-UCJA6bVKQ8 GIZA-FAYSAL (LINKES SEITENFENSTER/LEFT WINDOW!) 02:05 Bassem Nagm ( عتابا)ATTABA-( عدىل منصور)LINE 3:ADLY MANSOUR 21.08.2020 https://www.youtube.com/watch?v=t7m5Z9g39ro EL NOZHA-ADLY MANSOUR (FENSTERBLICKE/WINDOW VIEWS!) 03:49 Hesham Mohamed ALGERIEN/ALGERIA/AL-DSCHUMHŪRĪYA AL-DSCHAZĀ'IRĪYA AD-DĪMŪGRĀTĪYA ASCH- َ /TAGDUDA TAZZAYRIT TAMAGDAYT TAỴERFANT/ الجمهورية الجزائرية الديمقراطيةالشعبية/SCHA'BĪYA ⵜⴰⴳⴷⵓⴷⴰ ⵜⴰⵣⵣⴰⵢⵔⵉⵜ ⵜⴰⵎⴰⴳⴷⴰⵢⵜ ⵜⴰⵖⴻⵔⴼⴰⵏⵜ : /DZAYER TAMANEỴT/ دزاير/DZAYER/مدينة الجزائر/ALGIER/ALGIERS/MADĪNAT AL DSCHAZĀ'IR ⴷⵣⴰⵢⴻⵔ ⵜⴰⵎⴰⵏⴻⵖⵜ PLACE DE MARTYRS-( ع ني نعجة)AÏN NAÂDJA/( مركز الحراش)LINE:EL HARRACH CENTRE ( مكان دي مارت بز) 1 ARGENTINIEN/ARGENTINA/REPÚBLICA ARGENTINA: BUENOS AIRES: LINE:LINEA A:PLACA DE MAYO-SAN PEDRITO(SUBTE) 20.02.2011 https://www.youtube.com/watch?v=jfUmJPEcBd4 PIEDRAS-PLAZA DE MAYO 02:47 Joselitonotion 13.05.2020 https://www.youtube.com/watch?v=4lJAhBo6YlY RIO DE JANEIRO-PUAN 07:27 Así es BUENOS AIRES 4K 04.12.2014 https://www.youtube.com/watch?v=PoUNwMT2DoI -

Finance Project

MASTER OF SCIENCE IN FINANCE MASTERS FINAL WORK PROJECT EQUITY RESEARCH: CHINA VANKE CO., LTD SANG JINLAMU APRIL 2019 MASTER OF SCIENCE IN FINANCE MASTERS FINAL WORK PROJECT EQUITY RESEARCH: CHINA VANKE CO., LTD SANG JINLAMU SUPERVISOR: JOÃO CARVALHO DAS NEVES APRIL 2019 Abstract The Residential Housing Market in China has more than 30 years of development history. Due to the reform and liberalization in 1980’s, Deng Xiaoping started to define real estate as commodity in China. In 1987, Shenzhen conducted the first public land auction, symbolizing the official commercialization of Chinese real estate. Vanke, one year later, entered the real estate industry. After more than 20 years, it has become the largest residential developer in China, and is known as the “city real estate and service provider”. From Vanke, we can see the epitome of development of all Chinese real estate companies. The economic downturn and the changing world pattern are the major concerns for Chinese real estate developers in the recent years. These concerns are reflected by Vanke, which is the reason why I choose Vanke for Master Final Work equity research. This report adopts the research report format recommended by the CFA Institute. The full text includes 8 parts including Research Snapshot, Business Description and Management and Corporate Governance. It analyzes finance and management of Vanke in the past four years and forecasts the operations for the next five years. Generally, Vanke's operational development is stable. Persisting in high asset turnover strategy, it has about 20% ROE on the period analyzed. In terms of leverage, in the past two years, Vanke has increased its debt level from 16.36% to 17.09%.