Annual Report 2020 3

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Three Red Lines” Policy

Real Estate Developers with High Leverage to See Inventory Quality Tested Under Broader “Three Red Lines” Policy October 28, 2020 In our view, the widening of regulations aimed at controlling real estate developers’ interest- ANALYSTS bearing debt would further reduce the industry’s overall credit risk in the long term. However, the nearer term may see less headroom for highly leveraged developers to finance in the capital Xiaoliang Liu, CFA market, pushing them to sell off inventory to ease liquidity pressure. Beijing +86-10-6516-6040 The People’s Bank of China said in September that measures aimed at monitoring the funding [email protected] and financial management of key real estate developers will steadily be expanded. Media reports suggest that the new regulations would see a cap of 15% on annual growth of interest-bearing Jin Wang debt for all property developers. Developers will be assessed against three indicators, which are Beijing called “red lines”: whether asset liability ratios (excluding advance) exceeded 70%; whether net +86-10-6516-6034 gearing ratio exceeded 100%; whether cash to short-term debt ratios went below 1.0. Developers [email protected] which breached all three red lines won’t be allowed to increase their debt. If only one or two of the red lines are breached, such developers would have their interest-bearing debt growth capped at 5% and 10% respectively. The first half of the year saw debt grow rapidly among developers. In a sample of 87 real estate developers that we are monitoring, more than 40% saw their interest-bearing debt grow at a faster rate than 15% year over year as of the end of June (see the chart below). -

Global Offering

(Incorporated in the Cayman Islands with limited liability) Stock Code: Global Offering Joint Sponsors, Joint Global Coordinators, Joint Bookrunners and Joint Leadad ManagersManagers (in alphabetical order) Other Joint Global Coordinator, Joint Bookrunner and Joint Lead Manager Other Joint Bookrunners and Joint Lead Managers (in alphabetical order) Project A_PPTUS cover(Eng) Cover size: 210 x 280mm / Open size: 445.3 x 280mm / Spine width: 25.3mm IMPORTANT If you are in any doubt about any of the contents of this prospectus, you should obtain independent professional advice. (Incorporated in the Cayman Islands with limited liability) GLOBAL OFFERING Number of Offer Shares under : 550,000,000 Shares (subject to the Over- the Global Offering allotment Option) Number of Hong Kong Offer Shares : 27,500,000 Shares (subject to reallocation) Number of International Offer Shares : 522,500,000 Shares (including 55,000,000 Reserved Shares under the Preferential Offering) (subject to reallocation and the Over-allotment Option) Maximum Offer Price : HK$22.30 per Share plus brokerage of 1.0%, SFC transaction levy of 0.0027% and the Hong Kong Stock Exchange trading fee of 0.005% (payable in full on application, subject to refund) Nominal value : US$0.00001 per Share Stock code : 1209 Joint Sponsors, Joint Global Coordinators, Joint Bookrunners and Joint Lead Managers (in alphabetical order) Other Joint Global Coordinator, Joint Bookrunner and Joint Lead Manager Other Joint Bookrunners and Joint Lead Managers (in alphabetical order) Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibility for the contents of this prospectus, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this prospectus. -

China Reits Property Landlords to Shine 19

SECTOR BRIEFING number DBS Asian Insights DBS Group59 Research • May 2018 China REITs Property Landlords to Shine 19 DBS Asian Insights SECTOR BRIEFING 59 02 China REITs Property Landlords to Shine Ken HE Equity Analyst DBS (Hong Kong) [email protected] Carol WU Head of Greater China Research DBS (Hong Kong) [email protected] Danielle WANG CFA Equity Analyst DBS (Hong Kong) [email protected] Derek TAN Equity Analyst DBS Group Research [email protected] Jason LAM Equity Analyst DBS (Hong Kong) [email protected] Produced by: Asian Insights Office • DBS Group Research go.dbs.com/research @dbsinsights [email protected] Goh Chien Yen Editor-in-Chief Jean Chua Managing Editor Martin Tacchi Art Director 19 DBS Asian Insights SECTOR BRIEFING 59 03 04 Executive Summary 08 China REITs Are Lagging Edging Towards Onshore REITs Major Obstacles in Fostering 18 an Onshore REIT Regime CMBS/CMBNs Are Growing Faster C-REITs Are Imminent Which Asset Type Will Benefit 28 More? Modern Logistics Properties The Rise of Active Property Asset Management Which Developer Will Benefit From the Establishment of C-REITs? 49 Appendix DBS Asian Insights SECTOR BRIEFING 59 04 Executive Summary No REIT regime yet he real estate investment trust (REIT) has become an important investment vehicle as evidenced by its separation from the financial sector in the Global Industry Classification Standard as a sector on its own. Major Asian countries/regions have joined western countries to kickstart local versions of REITs, leaving China the last Tbig economy that has yet to have such an investment vehicle. Two major technical In our view, removing legislative obstacles (publicly traded funds are not allowed to obstacles hold commercial properties) is the first step that the government needs to take towards establishing a modern REIT regime. -

Dean's List Australia

THE OHIO STATE UNIVERSITY Dean's List AUTUMN SEMESTER 2019 Australia Data as of January 15, 2020 Sorted by Zip Code, City and Last Name Student Name (Last, First, Middle) City State Zip Nothdurft, Alexandra Eloise Brisbane 4075 THE OHIO STATE UNIVERSITY OSAS - Analysis and Reporting January 15, 2020 Page 1 of 133 Contact: [email protected] THE OHIO STATE UNIVERSITY Dean's List AUTUMN SEMESTER 2019 Bahamas Data as of January 15, 2020 Sorted by Zip Code, City and Last Name Student Name (Last, First, Middle) City State Zip Campbell, Caronique Leandra Nassau THE OHIO STATE UNIVERSITY OSAS - Analysis and Reporting January 15, 2020 Page 2 of 133 Contact: [email protected] THE OHIO STATE UNIVERSITY Dean's List AUTUMN SEMESTER 2019 Bangladesh Data as of January 15, 2020 Sorted by Zip Code, City and Last Name Student Name (Last, First, Middle) City State Zip Sajid, A s m Dhaka 1212 THE OHIO STATE UNIVERSITY OSAS - Analysis and Reporting January 15, 2020 Page 3 of 133 Contact: [email protected] THE OHIO STATE UNIVERSITY Dean's List AUTUMN SEMESTER 2019 Belgium Data as of January 15, 2020 Sorted by Zip Code, City and Last Name Student Name (Last, First, Middle) City State Zip Lallemand, Martin Victor D Orp-le-grand 1350 THE OHIO STATE UNIVERSITY OSAS - Analysis and Reporting January 15, 2020 Page 4 of 133 Contact: [email protected] THE OHIO STATE UNIVERSITY Dean's List AUTUMN SEMESTER 2019 Brazil Data as of January 15, 2020 Sorted by Zip Code, City and Last Name Student Name (Last, First, Middle) City State Zip Marotta Gudme, Erik Rio De Janeiro -

The Lonely Diplomats Club Meet the Micro-Ambassadors Dining at the World’S Largest Table

P earl R iver D elta THE LONELY DIPLOMATS CLUB MEET THE MICRO-AMBASSADORS DINING AT THE WORLD’S LARGEST TABLE Follow Us on WeChat Now Advertising Hotline 400 820 8428 Nice Tats 城市漫步珠三角 英文版 7 月份 Girls Getting Inked Up 国内统一刊号: CN 11-5234/GO China Intercontinental Press Ice, Ice, Baby 07 Cool Off with Skating Spectacular Pole Dancing JULY 2014 No Tips Please, We’re Athletes 《城市漫步》珠江三角洲 英文月刊 主管单位 : 中华人民共和国国务院新闻办公室 Supervised by the State Council Information Office of the People's Republic of China 主办单位 : 五洲传播出版社 地址 : 北京市海淀区北三环中路 31 号生产力大楼 B 座 7 层 邮编 100088 B-721 Shengchanli Building, No. 31 Beisanhuan Zhonglu, Haidian District, Beijing 100088, PRC http://www.cicc.org.cn 社长 President: 李红杰 Li Hongjie 期刊部负责人 Supervisor of Magazine Department: 邓锦辉 Deng Jinhui Chief Editor Tom Lee Deputy Editor Jane Kent Shenzhen Editor Gary Maidment Events and Web Editor Will Wu Editorial Assistant Van Fan Contributors Marianna Cerini, Andrew Chin, Lena Gidwani, Christine Gilbert, Oscar Holland, Monica Liau, Trevor Marshallsea, S. E. Smith, Zoey Zha Urbanatomy Media Shanghai (Head office) 上海和舟广告有限公司 上海市澳门路 872 弄 10 号 邮政编码 : 200050 No.10, Lane 872, Aomen Lu, Shanghai 200050 电话 : 021-2213 9018 传真 : 021-2213 9010 Guangzhou 上海和舟广告有限公司广州分公司 广州市麓苑路 42 号大院 2 号楼 610 室 邮政编码 : 510095 Rm. 610, No. 2 Building, Area 42, Lu Yuan Lu, Guangzhou 510095 电话 : 020-8358 6125 传真 : 020-8357 3859 - 816 Shenzhen 深圳业务 电话 : 0755-8623 3220 传真 : 0755-6406 8538 Beijing 北京联络处 北京市东城区东直门外大街 48 号东方银座 C 座 G9 室 邮政编码 : 100027 9G, Block C, Ginza Mall, No.48 Dongzhimen Wai Dajie, Dongcheng District, -

Poly Property Group Co., Limited 保利置業集團有限公司 (Incorporated in Hong Kong with Limited Liability) (Stock Code: 119)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. Poly Property Group Co., Limited 保利置業集團有限公司 (Incorporated in Hong Kong with limited liability) (Stock code: 119) RESULTS ANNOUNCEMENT FOR THE YEAR ENDED 31ST DECEMBER, 2017 RESULTS The directors (the “Directors”) of Poly Property Group Co., Limited (the “Company”) presented the audited consolidated financial statements of the Company and its subsidiaries (the “Group”) for the year ended 31st December, 2017, together with the independent auditor’s report issued by BDO Limited, as follows: – 1 – INDEPENDENT AUDITOR’S REPORT TO THE MEMBERS OF POLY PROPERTY GROUP CO., LIMITED (incorporated in Hong Kong with limited liability) Opinion We have audited the consolidated financial statements of Poly Property Group Co., Limited and its subsidiaries (together “the Group”) set out on pages 9 to 120, which comprise the consolidated statement of financial position as at 31st December, 2017, the consolidated statement of profit or loss, the consolidated statement of comprehensive income, the consolidated statement of changes in equity and the consolidated statement of cash flows for the year then ended and notes to the consolidated financial statements, including a summary of significant accounting policies. In our opinion, the consolidated financial statements give a true and fair view of the consolidated financial position of the Group as at 31st December, 2017 and of its consolidated financial performance and its consolidated cash flows for the year then ended in accordance with Hong Kong Financial Reporting Standards (“HKFRSs”) issued by the Hong Kong Institute of Certified Public Accountants (“HKICPA”) and have been properly prepared in compliance with the Hong Kong Companies Ordinance. -

5G for Trains

5G for Trains Bharat Bhatia Chair, ITU-R WP5D SWG on PPDR Chair, APT-AWG Task Group on PPDR President, ITU-APT foundation of India Head of International Spectrum, Motorola Solutions Inc. Slide 1 Operations • Train operations, monitoring and control GSM-R • Real-time telemetry • Fleet/track maintenance • Increasing track capacity • Unattended Train Operations • Mobile workforce applications • Sensors – big data analytics • Mass Rescue Operation • Supply chain Safety Customer services GSM-R • Remote diagnostics • Travel information • Remote control in case of • Advertisements emergency • Location based services • Passenger emergency • Infotainment - Multimedia communications Passenger information display • Platform-to-driver video • Personal multimedia • In-train CCTV surveillance - train-to- entertainment station/OCC video • In-train wi-fi – broadband • Security internet access • Video analytics What is GSM-R? GSM-R, Global System for Mobile Communications – Railway or GSM-Railway is an international wireless communications standard for railway communication and applications. A sub-system of European Rail Traffic Management System (ERTMS), it is used for communication between train and railway regulation control centres GSM-R is an adaptation of GSM to provide mission critical features for railway operation and can work at speeds up to 500 km/hour. It is based on EIRENE – MORANE specifications. (EUROPEAN INTEGRATED RAILWAY RADIO ENHANCED NETWORK and Mobile radio for Railway Networks in Europe) GSM-R Stanadardisation UIC the International -

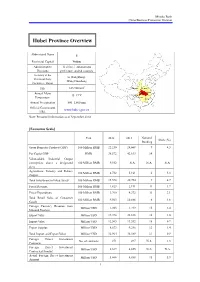

Hubei Province Overview

Mizuho Bank China Business Promotion Division Hubei Province Overview Abbreviated Name E Provincial Capital Wuhan Administrative 12 cities, 1 autonomous Divisions prefecture, and 64 counties Secretary of the Li Hongzhong; Provincial Party Wang Guosheng Committee; Mayor 2 Size 185,900 km Shaanxi Henan Annual Mean Hubei Anhui 15–17°C Chongqing Temperature Hunan Jiangxi Annual Precipitation 800–1,600 mm Official Government www.hubei.gov.cn URL Note: Personnel information as of September 2014 [Economic Scale] Unit 2012 2013 National Share (%) Ranking Gross Domestic Product (GDP) 100 Million RMB 22,250 24,668 9 4.3 Per Capita GDP RMB 38,572 42,613 14 - Value-added Industrial Output (enterprises above a designated 100 Million RMB 9,552 N.A. N.A. N.A. size) Agriculture, Forestry and Fishery 100 Million RMB 4,732 5,161 6 5.3 Output Total Investment in Fixed Assets 100 Million RMB 15,578 20,754 9 4.7 Fiscal Revenue 100 Million RMB 1,823 2,191 11 1.7 Fiscal Expenditure 100 Million RMB 3,760 4,372 11 3.1 Total Retail Sales of Consumer 100 Million RMB 9,563 10,886 6 4.6 Goods Foreign Currency Revenue from Million USD 1,203 1,219 15 2.4 Inbound Tourism Export Value Million USD 19,398 22,838 16 1.0 Import Value Million USD 12,565 13,552 18 0.7 Export Surplus Million USD 6,833 9,286 12 1.4 Total Import and Export Value Million USD 31,964 36,389 17 0.9 Foreign Direct Investment No. -

THE OHIO STATE UNIVERSITY Dean's List AUTUMN SEMESTER 2016 Australia Data As of January 19, 2017 Sorted by Zip Code, City and Last Name

THE OHIO STATE UNIVERSITY Dean's List AUTUMN SEMESTER 2016 Australia Data as of January 19, 2017 Sorted by Zip Code, City and Last Name Student Name (Last, First, Middle) City State Zip Bailey, Meg Elizabeth Merewether 2291 Caudle, Emily May Canberra 2609 Davis, Sarah Kate Canberra 2615 Thek, Hannah Louise Surrey Hills 3127 Engel, Rachel Olivia Glen Iris 3146 Taig, Darcy Lachlan Melbourne 3166 THE OHIO STATE UNIVERSITY Enrollment Services - Analysis and Reporting January 19, 2017 Page 1 of 119 Contact: [email protected] THE OHIO STATE UNIVERSITY Dean's List AUTUMN SEMESTER 2016 Bangladesh Data as of January 19, 2017 Sorted by Zip Code, City and Last Name Student Name (Last, First, Middle) City State Zip Bari, Rizvi Dhaka 1215 THE OHIO STATE UNIVERSITY Enrollment Services - Analysis and Reporting January 19, 2017 Page 2 of 119 Contact: [email protected] THE OHIO STATE UNIVERSITY Dean's List AUTUMN SEMESTER 2016 Brazil Data as of January 19, 2017 Sorted by Zip Code, City and Last Name Student Name (Last, First, Middle) City State Zip Rodrigues Franklin, Ana Beatriz Rio de Janeiro 22241 Gomes Pereira Painhas, Henrique Curitiba 80240 Sprintzin, Leonardo Curitiba 80240 Missell, Daniel Caxias do Sul 95020 THE OHIO STATE UNIVERSITY Enrollment Services - Analysis and Reporting January 19, 2017 Page 3 of 119 Contact: [email protected] THE OHIO STATE UNIVERSITY Dean's List AUTUMN SEMESTER 2016 Canada Data as of January 19, 2017 Sorted by Zip Code, City and Last Name Student Name (Last, First, Middle) City State Zip Lu, George Shizhou Vancouver -

Evergrande Real Estate Group Limited 恒 大 地 產 集 團 有 限 公 司 (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 3333)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. Evergrande Real Estate Group Limited 恒 大 地 產 集 團 有 限 公 司 (Incorporated in the Cayman Islands with limited liability) (Stock Code: 3333) DISCLOSEABLE TRANSACTION The Board announces that on 2 December 2015, Shengyu (BVI) Limited, a wholly-owned subsidiary of the Company, as the purchaser, entered into three agreements respectively with the Vendor, pursuant to which the Purchaser agreed to acquire the interests in the relevant shares in and loans to the target companies held by the Vendor. These target companies hold the interests in the Haikou Project, the Huiyang Project and two projects located in Wuhan. Since the Vendor is the seller in these three agreements, such agreements will be aggregated in accordance with Rule 14.22 of the Listing Rules. As the applicable percentage ratios for the Acquisition exceed 5% but are less than 25%, the Acquisition constitutes a discloseable transaction for the Company under Chapter 14 of the Listing Rules and is subject to the reporting and announcement requirements under Chapter 14 of the Listing Rules. 1. INTRODUCTION The Board announces that on 2 December 2015, Shengyu (BVI) Limited, a wholly-owned subsidiary of the Company, as the purchaser, entered into three agreements respectively with the Vendor, pursuant to which the Purchaser agreed to acquire the interests in the relevant shares in and loans to the target companies held by the Vendor. -

Grade 7 OFFICIAL Results for CHINA 2014-2015 School Year

2014-2015 CONTEST SCORE REPORT SUMMARY FOR GRADE 7 Summary of Results 7th Grade Contests – Math League China Regional Standing This Contest took place on Jan 3, 2015. Top 60 Students in 7th Grade Contests (Perfect Score = 200) Rank Student School Town Score 1 Chuanyang Jin Nanjing 200 1 Zhaoyi Zhou Shanghai 200 1 Honghan Huang Shanghai 200 4 Tianyue Cao Beijing 195 4 Yuxiao Xie Shenzhen Middle School Shenzhen 195 4 Keming Qian Nanjing Foreign Language School Nanjing 195 4 Yuxing Chen Shanghai 195 8 Junqiu Hu Shenzhen Middle School Shenzhen 190 8 Haozhe Chi Shenzhen Middle School Shenzhen 190 8 Huatai Zou Shenzhen Middle School Shenzhen 190 8 Ziang Wei Nanjing 190 8 Jiale Liu Nanjing 190 8 Xinyuan Wu Nanjing 190 8 Kaibo Tang Shanghai 190 8 Jianhua Wu Shanghai 190 8 Yiyang Fan Shanghai 190 17 Liangdong Hu Beijing 185 17 Weiyuan Chen Shenzhen Middle School Shenzhen 185 17 Yiyang Cao Nanjing 185 Shanghai Foreign Language School Affiliated To Shanghai International 17 Yuqing Liu Shanghai 185 Studies University 17 Yingcheng Cai Shanghai 185 17 Junxiong Chen Shanghai 185 17 Yili Lu Shanghai 185 17 Yikun Ji Shanghai 185 17 Junhao Zhu Shanghai 185 26 Yongle Zhou Beijing 180 26 Songyi Huang Middle School Attached To Guangzhou University Guangzhou 180 26 Zuning Ye Guangzhou 180 26 Xiaotian Lin Shenzhen Middle School Shenzhen 180 Summary of Results 7th Grade Contests – Math League China Regional Standing This Contest took place on Jan 3, 2015. Top 60 Students in 7th Grade Contests (Perfect Score = 200) (Continued) Rank Student School Town Score 26 -

High Speed Rail: Wuhan Urban Garden 5-Day Trip

High Speed Rail: Wuhan Urban Garden 5-Day Trip Day 1 Itinerary Suggested Transportation Hong Kong → Wuhan High Speed Rail [Hong Kong West Kowloon Station → Wuhan Railway Station] To hotel: Recommend to stay in a hotel by the river in Wuchang District. Metro: From Wuhan Railway Hotel for reference: Station, take Metro Line 4 The Westin Wuhan Wuchang Hotel towards Huangjinkou. Address: 96 Linjiang Boulevard, Wuchang District, Wuhan Change to Line 2 at Hongshan Square Station towards Tianhe International Airport. Get off at Jiyuqiao Station and walk for about 7 minutes. (Total travel time about 46 minutes) Taxi: About 35 minutes. Enjoy lunch near the hotel On foot: Walk for about 5 minutes Restaurant for reference: Zhen Bafang Hot Pot from the hotel. Address: No. 43 & 44, Building 12-13, Qianjin Road, Wanda Plaza, Jiyu Bridge, Wuchang District, Wuhan Stand the Test of Time: Yellow Crane Tower Bus: Walk for about 4 minutes from the restaurant to Jiyuqiao Metro Station. Take bus 804 towards Nanhu Road Jiangnan Village. Get off at Yue Ma Chang Station and walk for about 6 minutes. (Total travel time about 37 minutes) Taxi: About 15 minutes. Known as “The No. 1 Tower in the World”, the Yellow Crane Tower is a landmark for Wuhan City and Hubei Province and a must-see attraction. The tower was built in the Three Kingdoms era and was named after its erection on Huangjiji, a submerged rock. Well-known ancient characters such as Li Bai, Bai Juyi, Lu You and Yue Fei had all referenced the tower in their poetry works.