Annual Report 2019 02

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Uni-Fuel System, a Simple and Modern Way to Improve Fuel Consumption and Energy Generating Costs - the Sulzer S20 Diesel Engine As a Basic Model

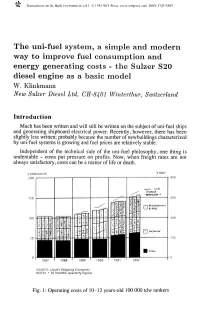

Transactions on the Built Environment vol 1, © 1993 WIT Press, www.witpress.com, ISSN 1743-3509 The uni-fuel system, a simple and modern way to improve fuel consumption and energy generating costs - the Sulzer S20 diesel engine as a basic model W. Klinkmann New Sulzer Diesel Ltd, CH-8401 Winterthur, Switzerland Introduction Much has been written and will still be written on the subject of uni-fuel ships and generating shipboard electrical power. Recently, however, there has been slightly less written; probably because the number of newbuildings characterized by uni-fuel systems is growing and fuel prices are relatively stable. Independent of the technical side of the uni-fuel philosophy, one thing is undeniable - costs put pressure on profits. Now, when freight rates are not always satisfactory, costs can be a matter of life or death. S'OOO* 600 200 1987 1988 1990 SOURCE: Lloyd's Shipping Economist NOTES: * 30 months; quarterly figures Fig. 1: Operating costs of 10-12 years-old 100 000 tdw tankers 12 8 MarinTransactionse Engineerin on the Built Environmentg vol 1, © 1993 WIT Press, www.witpress.com, ISSN 1743-3509 The Principal Economic Parameter Shipping and related activities are risky businesses with high investments and market environments which are highly volatile. The output of ships (tonne-miles) only takes place when vessels are at sea. Reliability of ships and their machinery are therefore of eminent economical importance. The following formula gives us a good basis for judging the influence which different parameters have on -

Contract Specifications for Futures Contracts and Eurex14 Options Contracts at Eurex Deutschland and Stand March 2831, 2008 Eurex Zürich Seite 1

Contract Specifications for Futures Contracts and Eurex14 Options Contracts at Eurex Deutschland and Stand March 2831, 2008 Eurex Zürich Seite 1 [....] Annex A in relation to subsection 1.6 of the contract specifications: Futures on Shares of Produkt- Group Cash Contract Minimum Currency ID ID** Market- Size Price ID** Change* Julius Bär Holding AG - N. BAEG CH01 XSWX 50 0.0010.01 CHF BB Biotech AG BIOF CH01 XSWX 50 0.0010.01 CHF Logitech International S.A. - N. LOGF CH01 XSWX 100 0.00010.01 CHF Pargesa Holding S.A. PARF CH01 XSWX 10 0.0010.01 CHF Sonova Holding AG - N. PHBF CH01 XSWX 50 0.0010.01 CHF PSP Swiss Property AG - N. PSPF CH01 XSWX 50 0.0010.01 CHF Schindler Holding AG SINF CH01 XSWX 50 0.0010.01 CHF Straumann Holding AG STMF CH01 XSWX 10 0.0010.01 CHF Swatch Group AG, The - N. UHRF CH01 XSWX 100 0.00010.01 CHF Valiant Holding AG - N. VATF CH01 XSWX 10 0.0010.01 CHF ABB Ltd. ABBF CH02 XVTX 100 0.00010.01 CHF Adecco S.A. - N. ADEF CH02 XVTX 100 0.0010.01 CHF Actelion Ltd. - N. ATLG CH02 XVTX 50 0.0010.01 CHF Bâloise Holding AG BALF CH02 XVTX 100 0.0010.01 CHF Compagnie Financière Richemont AG CFRH CH02 XVTX 100 0.0010.01 CHF Ciba Spezialitätenchemie Holding AG - N. CIBF CH02 XVTX 10 0.0010.01 CHF Clariant AG - N. CLNF CH02 XVTX 100 0.00010.01 CHF Credit Suisse Group - N. CSGG CH02 XVTX 100 0.00010.01 CHF Geberit AG - N. -

Switzerland Fund A-CHF for Investment Professionals Only FIDELITY FUNDS MONTHLY PROFESSIONAL FACTSHEET SWITZERLAND FUND A-CHF 31 AUGUST 2021

pro.en.xx.20210831.LU0054754816.pdf Switzerland Fund A-CHF For Investment Professionals Only FIDELITY FUNDS MONTHLY PROFESSIONAL FACTSHEET SWITZERLAND FUND A-CHF 31 AUGUST 2021 Strategy Fund Facts The Portfolio Managers are bottom-up investors who believe share prices are Launch date: 13.02.95 correlated to earnings, and that strong earners will therefore outperform. They look to Portfolio manager: Andrea Fornoni, Alberto Chiandetti invest in companies where the market underestimates earnings because their Appointed to fund: 01.03.18, 01.08.11 sustainability is not fully appreciated. They also look for situations where the impact Years at Fidelity: 7, 15 company changes will have on earnings has not been fully recognised by the market. Fund size: CHF366m They aim to achieve a balance of different types of companies, so they can deliver Number of positions in fund*: 36 performance without adding undue risk. Fund reference currency: Swiss Franc (CHF) Fund domicile: Luxembourg Fund legal structure: SICAV Management company: FIL Investment Management (Luxembourg) S.A. Capital guarantee: No Portfolio Turnover Cost (PTC): 0.01% Portfolio Turnover Rate (PTR): 28.92% *A definition of positions can be found on page 3 of this factsheet in the section titled “How data is calculated and presented.” Objectives & Investment Policy Share Class Facts • The fund aims to provide long-term capital growth with the level of income expected Other share classes may be available. Please refer to the prospectus for more details. to be low. • The fund will invest at least 70% in Swiss company shares. Launch date: 13.02.95 • The fund has the freedom to invest outside its principal geographies, market sectors, industries or asset classes. -

Keyinvest Return Monitor Systematically Selected UBS Barrier Reverse Convertibles

Structured investment products for clients in Switzerland KeyInvest Return Monitor Systematically selected UBS Barrier Reverse Convertibles The Return Monitor provides an overview of UBS Barrier Reverse Convertibles (BRCs) offering attractive potential returns. All selected BRCs are listed on the SIX Structured Products Exchange and tradeable on each trading day under normal market conditions. In focus are products that have at least three months left until maturity and an intact barrier. The three categories examined are: Attractive sideways return, high barrier distance and underlyings with a Buy Rating by UBS Research. Further information can be found on: ubs.com/renditemonitor Attractive sideways return Barrier distance Coupon p.a. Underlying Ask Currency Expiry Valor Sideways return p.a. (worst performer) 5.50% Bayer / Novartis / Roche / Sanofi 74.30 CHF 14/08/2020 A 39945568 15.1% 30.6% 8.00% CENTRICA PLC / E.ON / Electricite de France 78.70 EUR 10/08/2020 A 42686847 18.7% 28.2% 9.00% Credit Suisse / Deutsche Bank 82.10 CHF 13/07/2020 A 42078534 15.8% 26.3% 9.75% Enel / Fiat Chrysler / UniCredit 85.20 EUR 29/06/2020 39167120 28.3% 23.9% 9.00% Hewlett-Packard / IBM 93.27 USD 06/07/2020 A 42271711 31.2% 15.1% High barrier distance Barrier distance Coupon p.a. Underlying Ask Currency Expiry Valor Sideways return p.a. (worst performer) 12.00% Alcoa Corporation / US STEEL CORP 96.32 USD 12/06/2020 A 44506090 47.5% 15.3% 7.75% Colgate-Palmolive / Estée Lauder / L'Oréal 98.55 USD 22/06/2020 A 41905920 43.9% 15.4% 10.00% Nike / Under Armour Inc. -

Internal Combustion Engines Collection of Stationary

ASME International THE COOLSPRING POWER MUSEUM COLLECTION OF STATIONARY INTERNAL COMBUSTION ENGINES MECHANICAL ENGINEERING HERITAGE COLLECTION Coolspring Power Museum Coolspring, Pennsylvania June 16, 2001 The Coolspring Power Museu nternal combustion engines revolutionized the world I around the turn of th 20th century in much the same way that steam engines did a century before. One has only to imagine a coal-fired, steam-powered, air- plane to realize how important internal combustion was to the industrialized world. While the early gas engines were more expensive than the equivalent steam engines, they did not require a boiler and were cheap- er to operate. The Coolspring Power Museum collection documents the early history of the internal- combustion revolution. Almost all of the critical components of hundreds of innovations that 1897 Charter today’s engines have their ori- are no longer used). Some of Gas Engine gins in the period represented the engines represent real engi- by the collection (as well as neering progress; others are more the product of inventive minds avoiding previous patents; but all tell a story. There are few duplications in the collection and only a couple of manufacturers are represent- ed by more than one or two examples. The Coolspring Power Museum contains the largest collection of historically signifi- cant, early internal combustion engines in the country, if not the world. With the exception of a few items in the collection that 2 were driven by the engines, m Collection such as compressors, pumps, and generators, and a few steam and hot air engines shown for comparison purposes, the collection contains only internal combustion engines. -

FTSE Developed Europe

2 FTSE Russell Publications 19 August 2021 FTSE Developed Europe Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 1&1 AG 0.01 GERMANY Avast 0.03 UNITED Cnp Assurance 0.02 FRANCE 3i Group 0.14 UNITED KINGDOM Coca-Cola HBC AG 0.06 UNITED KINGDOM Aveva Group 0.05 UNITED KINGDOM A P Moller - Maersk A 0.1 DENMARK KINGDOM Coloplast B 0.19 DENMARK A P Moller - Maersk B 0.15 DENMARK Aviva 0.19 UNITED Colruyt 0.03 BELGIUM A2A 0.03 ITALY KINGDOM Commerzbank 0.07 GERMANY Aalberts NV 0.05 NETHERLANDS AXA 0.43 FRANCE Compagnie Financiere Richemont SA 0.55 SWITZERLAND ABB 0.51 SWITZERLAND B&M European Value Retail 0.06 UNITED Compass Group 0.33 UNITED KINGDOM ABN AMRO Bank NV 0.04 NETHERLANDS KINGDOM BAE Systems 0.21 UNITED Acciona S.A. 0.03 SPAIN Continental 0.14 GERMANY KINGDOM Accor 0.06 FRANCE ConvaTec Group 0.05 UNITED Baloise 0.06 SWITZERLAND Ackermans & Van Haaren 0.03 BELGIUM KINGDOM Banca Mediolanum 0.02 ITALY ACS Actividades Cons y Serv 0.06 SPAIN Covestro AG 0.1 GERMANY Banco Bilbao Vizcaya Argentaria 0.36 SPAIN Adecco Group AG 0.09 SWITZERLAND Covivio 0.04 FRANCE Banco Santander 0.58 SPAIN Adevinta 0.04 NORWAY Credit Agricole 0.14 FRANCE Bank Pekao 0.03 POLAND Adidas 0.63 GERMANY Credit Suisse Group 0.22 SWITZERLAND Bankinter 0.03 SPAIN Admiral Group 0.08 UNITED CRH 0.35 UNITED Banque Cantonale Vaudoise 0.02 SWITZERLAND KINGDOM KINGDOM Barclays 0.35 UNITED Adyen 0.62 NETHERLANDS Croda International 0.12 UNITED KINGDOM KINGDOM Aegon NV 0.06 NETHERLANDS Barratt Developments 0.09 UNITED Cts Eventim 0.03 GERMANY Aena SME SA 0.1 SPAIN KINGDOM Cyfrowy Polsat SA 0.02 POLAND Aeroports de Paris 0.03 FRANCE Barry Callebaut 0.07 SWITZERLAND Daimler AG 0.66 GERMANY Ageas 0.09 BELGIUM BASF 0.64 GERMANY Danone 0.37 FRANCE Ahold Delhaize 0.26 NETHERLANDS Bayer AG 0.53 GERMANY Danske Bank A/S 0.1 DENMARK AIB Group 0.02 IRELAND Bechtle 0.04 GERMANY Dassault Aviation S.A. -

Because Life Is Fluid

BECAUSE LIFE IS FLUID Geschäftsbericht 2019 Inhalt 3 Brief an die Aktionärinnen und Aktionäre 7 Sulzer auf einen Blick 7 Unser Unternehmen 8 Unsere Kennzahlen 10 Fokus 18 Lagebericht 19 Finanzbericht 26 Lagebericht Divisionen 38 Nachhaltige Entwicklung 39 Mensch und Gemeinschaft 41 Umwelt 44 Arbeitssicherheit 46 Corporate governance (English only) 47 Corporate structure and shareholders 48 Capital structure 49 Board of Directors 57 Executive Committee 58 Shareholder participation rights 59 Takeover and defense measures 60 Auditors 61 Risk management 63 Information policy 64 Compensation report (English only) 65 Letter to the shareholders 68 Special report 71 Compensation governance and principles 74 Compensation architecture for the CEO and EC members 83 Compensation of the Executive Committee for 2019 88 Compensation architecture for the Board of Directors 90 Compensation of the Board of Directors for 2019 93 Auditor’s report 94 Financial reporting (English only) 95 Consolidated financial statements 185 Financial statements of Sulzer Ltd Sulzer Geschäftsbericht 2019 – Brief an die Aktionärinnen und Aktionäre 3 Brief an die Aktionärinnen und Aktionäre Wir von Sulzer wissen: „Life is fluid“. Auf der ganzen Welt werden Flüssigkeiten und Gase im Rahmen kritischer Infrastrukturprojekte transportiert oder verarbeitet. Wir setzen unser Fachwissen im Bereich Fluid-Engineering ein, um tagtäglich das Leben von Millionen von Menschen positiv zu beeinflussen. So erfüllen unsere Pumpen eine zentrale Funktion in Wassersystemen weltweit und helfen, die wertvollste Ressource unseres Planeten über Hunderte von Kilometern zu den Menschen zu transportieren und so die Entwicklung boomender Städte voranzutreiben. Unsere Serviceteams stellen die zuverlässige Stromversorgung für wachsende Volkswirtschaften und eine wachsende Bevölkerung sicher – um letztlich den ständig steigenden Energiebedarf zu decken. -

Dividend and Compensation Payments in Light of Covid-19 Pandemic

DIVIDEND AND COMPENSATION PAYMENTS IN LIGHT OF COVID-19 PANDEMIC Information as of 18 November 2020 Annual General Meeting 2019 dividend Company Index Short-time work Board compensation Executive compensation (2020) (paid 2020) ABB SMI unchanged (26.03.2020) unchanged CHF 0.80 - 10% reduction of board compensation for the duration of the 10% reduction of salary for the duration of the crisis crisis Adecco SMI unchanged (16.04.2020) unchanged CHF 2.50 yes - - Aevis Other unchanged (30.04.2020) cancelled - - - Alcon SMI unchanged (06.05.2020) postponed to 2021 - - - Also Other unchanged (24.03.2020) unchanged CHF 3.25 - - - ams SMIM unchanged (03.06.2020) - - - - APG/SGA Other unchanged (14.05.2020) cancelled (from CHF 11.00) yes - 20% reduction of base salary Aryzta Other postponed to 15.12.2020 postponed yes 30% reduction of fees for 3 months 30% reduction salary reduction for 3 months (15% for wider leadership team) Autoneum Other unchanged (25.03.2020) cancelled yes - 10% reduction of base salary Baloise SMIM unchanged (24.04.2020) unchanged CHF 6.40 - - - Barry Callebaut SMIM unchanged (09.12.2020) - - - - BB Biotech SMIM unchanged (19.03.2020) unchanged CHF 3.40 - - - Bobst Other unchanged (07.04.2020) unchanged CHF 1.50 - - - Bossard Other unchanged (08.04.2020) reduced by 50% to CHF 2.00 4% reduction of compensation 4% salary reduction Bucher Industries SMIM unchanged (24.04.2020) unchanged CHF 8.00 yes (mainly FR and IT) - - BVZ Other unchanged (16.04.2020) reduced to CHF 7.50 - - - Calida Group Other brought forward to cancelled -

Results Zrating Study 2019 on Corporate Governance

Zurich, 12 September 2019 Media release Results zRating Study 2019 on Corporate Governance Zürich, 12 September 2019 – Sunrise once again scores highest in this year’s corporate governance ranking followed by Swisscom (81 points) and Lonza (78 points). Due to amendments to the Articles of Association, also induced by activist shareholders, and changes in practices, companies have improved their corporate governance. For the eleventh time since 2009, the zRating Study on corporate governance in Swiss public companies has been published. zRating summarizes the situation regarding shareholders' rights in a company and draws attention to possible conflicts between shareholders and managers. zRating evaluates corporate governance holistically based on 62 criteria from the categories «Shareholders and Capital Structure», «Shareholders' Rights», «Composition Board of Directors/Management and Information Policy», and «Compensation and participation models». The criteria are weighted in a scoring model and evaluated with points. The total maximum of points is 100. 174 listed Swiss companies are analyzed based on Annual Reports 2018 and decisions at General Meetings 2019. Further improvements through amendments to the Articles of Association Once again Sunrise takes first place with 86 points. They had already gained a large lead thanks to amendments to the Articles of Association at the annual general meetings (AGM) in 2017 and 2018, and in 2019 Sunrise was also able to score in the new criteria. Second place went to Swisscom with 81 points and third place to Lonza with 78 points. This year, the boards of directors of Mobilezone, Peach Property and Starrag in particular proposed amendments to the Articles of Association that strengthened shareholders' participation rights. -

Voting Report 2020

Exercising of Shareholder Rights – Information December 2020 As a result of the adoption of the “Popular Initiative against Fat-Cat Salaries” in 2014, pension funds have an obligation to exercise shareholder rights in the interests of the insured persons and to disclose how the pension funds voted. This regulation applies for public limited companies with registered office in Switzerland and whose shares are listed on a domestic or foreign stock exchange. The Foundation Board of the PensFlex Collective Foundation has incorporated the corresponding regulations into the Art. 3.5 of the Organisational Rules or Art. 4 of the Rules on Investment. A list of the voting record of the PensFlex Collective Foundation in the year 2020 is shown below. Voting Report for PensFlex Sammelstiftung Kauffmannweg 16 6003 Luzern This report summarizes voting behaviour according to the following specifications: Time period: 01.01.2020 - 31.12.2020 Agenda items: Summary of all items on the agenda, i.e. not only the items requiring a vote according to Art. 22 para. 1 ORAb. The voting rights were exercised for the following companies: Perrot Duval 06.02.2020 Kardex 14.04.2020 Novartis 28.02.2020 Tornos 15.04.2020 Dätwyler 11.03.2020 Georg Fischer 15.04.2020 Roche 17.03.2020 Sulzer 15.04.2020 BB Biotech 19.03.2020 Evolva 15.04.2020 Schindler 19.03.2020 Mikron 15.04.2020 Swiss Prime Site 24.03.2020 Ascom 15.04.2020 Implenia 24.03.2020 Kudelski 15.04.2020 Bellevue 24.03.2020 Adecco 16.04.2020 SGS 24.03.2020 Rieter 16.04.2020 ALSO 24.03.2020 Cembra Money Bank 16.04.2020 -

Serving Our Customers: 100 Years of Knowledge Transfer Sulzer Technical Review 3/2019

4 Serving our customers: 100 years of knowledge transfer Sulzer Technical Review 3/2019 Serving our customers: 100 years of knowledge transfer How does a company like Sulzer succeed in asserting itself on the market for over 185 years, continuously creating innovative products? What influence does the transfer of knowledge have, and how does the curiosi- ty of employees influence knowledge transfer? What will the knowledge transfer of the future look like? In 1919 — 85 years after the company was founded — Sulzer’s first customer magazine was published in French. Since then, the Sulzer Technical Review has provided technical informa- tion on Sulzer’s current product range without interruption. The magazine’s 100th anniversary gives us a glimpse into the history of Sulzer as well as the future of knowledge transfer. Networks for knowledge transfer in pre-industrial times Professional networks are not an invention of our contemporary age. In earlier centuries in Johann Jakob Sulzer (1806–1883) Europe, craftsmen acquired knowledge within the family business, then moved on foot from shop to shop to learn additional skills. Before the Sulzer brothers (Fig. 1) established their new foundry (Fig. 2) in Winterthur in 1834, they collected technical and craft expertise in Switzer- land, France and the Kingdom of Bavaria through apprenticeships. Johann Jakob Sulzer’s journey led him from Bern and Lyon to Paris between 1827 and 1830. Salomon Sulzer apprenticed in Munich, Ulm and Guebwiller in Alsace. Salomon Sulzer (1809–1869) Fig. 1 The two founders of the Sulzer company. Fig. 2 The building where the Sulzer company Fig. -

Energy-Efficient Solutions Who We Are and How We Are Doing

The Company 2010 Energy-efficient solutions Who we are and how we are doing Sulzer is a global partner with reliable and sustainable solutions for performance-critical applications. We specialize in industrial machinery and equipment, surface technology, and rotating equipment maintenance. Combining engineering and application expertise, our innovative solutions add value and strengthen the competitive position of our customers. Sulzer is a leading provider in its key markets: oil and gas, hydrocarbon processing, power generation, automotive, aviation, and pulp and paper. We serve clients worldwide through a network of over 160 locations. Our key markets Oil and gas Hydrocarbon Power processing generation Automotive Aviation Pulp and paper See page 3 for more market information Sulzer | The Company 2010 1 Highlights in 2010 Sales Operating income CHF 3 184m CHF 406m (2009: CHF 3 350m) (2009: CHF 368m) Net income 1) Dividend CHF 300m CHF 3.00 (proposed) (2009: CHF 270m) (2009: CHF 2.80) • Sulzer’s order intake increased, driven by acquisitions and the recovery of early-cycle markets. Sales were still impacted by the strong order intake reduction in 2009. • With a return on sales of 12.8% and a return on capital employed of 28.1%, Sulzer proved its ability to adapt fast to changed market conditions. • Sulzer’s global presence was further strengthened with a major new manufacturing plant in China and facility expansions in Brazil, India, Russia, and Indonesia. Sulzer India Ltd. was taken private. • The service businesses of Sulzer Turbo Services and Sulzer Metco were expanded with the acquisitions of Dowding & Mills and Bekaert’s diamond-like coating activities.