The Furniture Industry in Germany Scenario

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

"Hello, Dolly!" at Auditorium Theatre, Jan. 27

AUDITORIUM THEATRE ROCHESTER JANUARY 27 BROAD'lMAY TO FEBRUARY 1 THEATRE LEAGUE 1969 YVONNE DECARLO m HELLO, gOLL~I llng1na1ly D1rected and ChoreogrJphPd by GOWER CHDIPIOII Th1s Pr oductiOn D1rected by LUCIA VICTOR ~tenens FEATURING OUR SATURDAY NITE SPECIAL Prime Rib of Beef Au Jus Baked Potato with Sour Cream & Chives Vegetable - Salad - Coffee $3.95 . ALSO MANY OTHER DELICIOUS ITEMS Stop in for dinner before the show or after the show for a late evening anack SERVING 7 DAYS & NITES FROM 11 A.M. till 2 A.M. 1501 UNIVERSITY AVE . EXTENSION PLENTY OF FlEE PAIICING For Reservations Call: 271-9635 or 271-9494 PARTY AND BANQUET ACCOMMODATIONS Consult Us For Your Banquets And Part i es . • • we w i ll be glad to hove you . Wm. Fisher, Budd Filippo & Ken Gaston proudly present YVONNE DE CARLO in The New York Critics Circle & Tony Award Winn1ng Mus1cal "HELLO, DOLLVI 11 Book IJy Music & Lyrics by MICHAEL STEW ART JERRY HERMAN Based on the originc~l play by Thornton Wilder also starring DON DE LEO with Kathleen Devine George Cavey Rick Grimaldi Suzanne Simon David Gary Althea Rose Edie Pool Norman Fredericks Settings Designed by Lighting Consultant Costumes by Oliver Smith Gerald Richland freddy Wittop Dance & Incidental Music Orchestration by Arrangements by Musical Dirt!cliun by Phillip J. Lang Peter Howard Gil Bowers [)ances Staged for this Production hy Jack Craig Original Choreography & Direction by GOWER CHAMPION This Production Staged by Lucia Victor PHIL'S PANTRYS J A Y ' S "REAL DELICATESSENS" Fresh Sliced Cold Meats D I N E R Home Made Salads & Baked Beans lWO LOCAnONS 2612 W. -

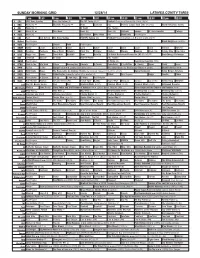

Sunday Morning Grid 12/28/14 Latimes.Com/Tv Times

SUNDAY MORNING GRID 12/28/14 LATIMES.COM/TV TIMES 7 am 7:30 8 am 8:30 9 am 9:30 10 am 10:30 11 am 11:30 12 pm 12:30 2 CBS CBS News Sunday Face the Nation (N) The NFL Today (N) Å Football Chargers at Kansas City Chiefs. (N) Å 4 NBC News (N) Å Meet the Press (N) Å News 1st Look Paid Premier League Goal Zone (N) (TVG) World/Adventure Sports 5 CW News (N) Å In Touch Paid Program 7 ABC News (N) Å This Week News (N) News (N) Outback Explore St. Jude Hospital College 9 KCAL News (N) Joel Osteen Mike Webb Paid Woodlands Paid Program 11 FOX Paid Joel Osteen Fox News Sunday FOX NFL Sunday (N) Football Philadelphia Eagles at New York Giants. (N) Å 13 MyNet Paid Program Black Knight ›› (2001) 18 KSCI Paid Program Church Faith Paid Program 22 KWHY Como Local Jesucristo Local Local Gebel Local Local Local Local Transfor. Transfor. 24 KVCR Painting Dewberry Joy of Paint Wyland’s Paint This Painting Kitchen Mexico Cooking Chefs Life Simply Ming Ciao Italia 28 KCET Raggs Play. Space Travel-Kids Biz Kid$ News Asia Biz Ed Slott’s Retirement Rescue for 2014! (TVG) Å BrainChange-Perlmutter 30 ION Jeremiah Youssef In Touch Hour Of Power Paid Program 34 KMEX Paid Program Al Punto (N) República Deportiva (TVG) 40 KTBN Walk in the Win Walk Prince Redemption Liberate In Touch PowerPoint It Is Written B. Conley Super Christ Jesse 46 KFTR Tu Dia Tu Dia Happy Feet ››› (2006) Elijah Wood. -

Ausgabe 4/2013

Magazin Unsere Wirtschaft Ausgabe 5/2013 Region Region Beilage 150 Jahre LASCO Umformtechnik Trauer um Frohnlacher Erfolgs- Konjunktur der regionalen in Coburg gefeiert unternehmer Willi Schillig Wirtschaft nimmt Fahrt auf Ausbildungsmarketing wird intensiver 2 Inhalt Region Andrang zur IHK-Berufsbildungsmesse 4 erreicht Kapazitätsgrenzen des Kongresshauses Wirtschaftsminister Zeil betont Bedeutung 7 der Thüringer Strombrücke IHK-Präsident Friedrich Herdan verzichtete 11 auf Empfänge zum 70. Geburtstag Langjähriger Brose-Manager Jakob 12 Faßbender vollendet 80. Lebensjahr Trauer um Frohnlacher Erfolgsunternehmer, 14 Sportsmann und Mäzen Willi Schillig „Get Connected Tour“ von Studierenden zu 15 heimischen Unternehmen erneut ein Erfolg Wirtschaftsjunioren Preisgekrönter „BusinessFührerschein“ feiert als 17 Ferien-Trainingscamp für Schüler Premiere Rauschende Party zur 40-Jahr-Feier der 21 Festakt zum 150-jährigen Bestehen von LASCO Umformtechnik GmbH Coburger Junioren vorbereitet 8–9 Statement zu Tradition, Passion und Vision Standortpolitik Best-Practice-Beispiel agifl ex im Blickpunkt 19 Mit mehr als 400 geladenen Gästen aus Stammsitz Coburg wurde deutlich, dass des „Tags der Logistik“ im IHK-Bezirk Wirtschaft, Politik und gesellschaftlichem der Maschinenbauer mit der längsten Leben des In- und Auslandes hat LASCO Tradition in der Vestestadt besser auf- Aus- und Weiterbildung Umformtechnik den 150. Jahrestag sei- gestellt ist als je zuvor. Gratulanten zoll- Zwei neue und ein modernisierter Ausbildungs- 22 ner Gründung gefeiert. Im Rahmen des ten viel Respekt, Lob und Anerkennung beruf erweitern Berufsfamilie Metall Festaktes im Herz der Produktion am für Leistung und Kontinuität. Zertifi kate für Wirtschafts- und Handelsfachwirte 23 belohnen intensive Weiterbildungsanstrengungen 16 Zum 25. Mal Coburger Designtage Innovation und Umwelt Bayerns Wirtschaftsminister überzeugt sich vom 24 Showbühne für den aufstrebenden Design-Standort Fortschritt von BestSens auf dem Weg in den Markt Die Coburger Designtage feiern in die- sem Jahr 25. -

The Sand Canyon Review 2013

The Sand Canyon Review 2013 1 Dear Reader, The Sand Canyon Review is back for its 6th issue. Since the conception of the magazine, we have wanted to create an outlet for artists of all genres and mediums to express their passion, craft, and talent to the masses in an accessible way. We have worked especially hard to foster a creative atmosphere in which people can express their identity through the work that they do. I have done a lot of thinking about the topic of identity. Whether someone is creating a poem, story, art piece, or multimedia endeavor, we all put a piece of ourselves, a piece of who we are into everything we create. The identity of oneself is embedded into not only our creations but our lives. This year the goal ofThe Sand Canyon Review is to tap into this notion, to go beyond the words on a page, beyond the color on the canvas, and discover the artist behind the piece. This magazine is not only a collection of different artists’ identities, but it is also a part of The Sand Canyon Review team’s identity. On behalf of the entire SCR staff, I wish you a wonderful journey into the lives of everyone represented in these pages. Sincerely, Roberto Manjarrez, Managing Editor MANAGING EDITOR Roberto Manjarrez POETRY SELectION TEAM Faith Pasillas, Director Brittany Whitt Art SELectION TEAM Mariah Ertl, Co-Director Aurora Escott, Co-Director Nicole Hawkins Christopher Negron FIT C ION SELectION TEAM Annmarie Stickels, Editorial Director BILL SUMMERS VICTORIA CEBALLOS Nicole Hakim Brandon Gnuschke GRAphIC DesIGN TEAM Jillian Nicholson, Director Walter Achramowicz Brian Campell Robert Morgan Paul Appel PUBLIC RELATIONS The SCR STAFF COPY EDITORS Bill Summers Nicole Hakim COVER IMAGE The Giving Tree, Owen Klaas EDITOR IN CHIEF Ryan Bartlett 2013 EDITION3 Table of Contents Poetry Come My Good Country You Know 8 Mouse Slipping Through the Knot I Saw Sunrise From My Knees 10 From This Apartment 12 L. -

US, JAPANESE, and UK TELEVISUAL HIGH SCHOOLS, SPATIALITY, and the CONSTRUCTION of TEEN IDENTITY By

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by British Columbia's network of post-secondary digital repositories BLOCKING THE SCHOOL PLAY: US, JAPANESE, AND UK TELEVISUAL HIGH SCHOOLS, SPATIALITY, AND THE CONSTRUCTION OF TEEN IDENTITY by Jennifer Bomford B.A., University of Northern British Columbia, 1999 THESIS SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF ARTS IN ENGLISH UNIVERSITY OF NORTHERN BRITISH COLUMBIA August 2016 © Jennifer Bomford, 2016 ABSTRACT School spaces differ regionally and internationally, and this difference can be seen in television programmes featuring high schools. As television must always create its spaces and places on the screen, what, then, is the significance of the varying emphases as well as the commonalities constructed in televisual high school settings in UK, US, and Japanese television shows? This master’s thesis considers how fictional televisual high schools both contest and construct national identity. In order to do this, it posits the existence of the televisual school story, a descendant of the literary school story. It then compares the formal and narrative ways in which Glee (2009-2015), Hex (2004-2005), and Ouran koukou hosutobu (2006) deploy space and place to create identity on the screen. In particular, it examines how heteronormativity and gender roles affect the abilities of characters to move through spaces, across boundaries, and gain secure places of their own. ii TABLE OF CONTENTS Abstract ii Table of Contents iii Acknowledgement v Introduction Orientation 1 Space and Place in Schools 5 Schools on TV 11 Schools on TV from Japan, 12 the U.S., and the U.K. -

Fum FURT TO-NIGHT

AMUSEMENTS BROADWAY & 11TH ST, fuM FURT TO-NIGHT. 1Y SHOE GO. 1 : and S I'D K. UNION SQUARE, ACADEMY OF DESIGN Paintings Basement Salesroom. ACADEMY OF MUSIC.Last of the Rolians and Place West Four kUteentn Street Between Broadway University AMERIOAN Die Meistersinger 'ill BIJOU In Paradise BKOADWAY The Ghetto ."] CASINO The Rounders of iii The Great Department Store ex( I CRITERION The Girl from Maxim's 9,000 yards Silk, Shoes. i DALY'S The King's Musketeer of 2 to 16 clusively for We are New york's La rgest and Sellers DEWEY Vaudeville lengths yards c Buyers Ef)EN MUSEE World in Wax EMPIRE The Tyranny,of Tears consisting of Fancy TafFe FIFTH AVENUE BecRy Sharp The Korker of 14TH STREET A Young Wife tas,.in plaid, check, stripe GARRICK My Innocent Boy GARDEN Rupert of Hentzau ' Shoe, GRAND OPERA HOUSE.A Grip of Steel corded, floral, warp print HARLEM OPERA HOUSE Phroso I and a of novo HOUSEKEE PING HERALD SQUARE The Only Way ed, variety GOODS.I IIUBER'S MUSEUM Vaudeville I iC°r ^en> HURT1G A SEAMON'S Vaudeville designs. Light, medianj KEITH'S UNION SQUARE.... Vaudeville Pillow Tic! KNICKERBOCKER. ..Cyrano tie Bergerac and dark shades. Sheets, Cases, Muslins. <ings, Bnn;ets, Comfortables, Quilts, KOSTER <fc BIAL'S Vaudeville Table Linens, Fia " bread and butter '* LYCEUM Miss Hobbs Peai1 2,50 Towels, Towellings, nnels,.the among MAD. SQ. THEA. Why Smith Left Home Black, Ducliesse, Housekeepers' requirements.Of ea ch and all of these we show extraordinary MANHATTAN, de Brocades A Stranger in a Strange Land Soie, Taffetas, assortments of all qualities, and throiugh our great purchases for cash can and METROPOLIS The Sporting Duchess MURRAY HILL The Highest Bidder Gros grain, Faille and Ar do sell so low that frequently our seiiUngprices are belcw .hose competitors pay NEW YORK. -

Merkblatt Zur Beteiligung Der Bezirksschornsteinfegermeisterin

Merkblatt zur Beteiligung der Bezirksschornsteinfegermeisterin/ des Bezirksschornsteinfegermeisters Stadt Schmallenberg - Untere Bauaufsichtsbehörde - Nach der Vorschrift des § 43 Abs. 7 der Bauordnung für das Land Nordrhein-Westfalen (BauO NRW) muss die Bauherrin/der Bauherr sich bei der Errichtung oder Änderung von Schornsteinen sowie bei Anschluss von Feuerstätten an Schornsteine oder Abgas- leitung von der Bezirksschornsteinfegermeisterin/dem Bezirksschornsteinfegermeister (BZSM) bescheinigen lassen, dass der Schornstein oder die Abgasanlage sich in ei- nem ordnungsgemäßen Zustand befindet und für die angeschlossenen Feuerstätten geeignet ist. Bei der Errichtung von Schornsteinen soll der/dem BZSM Gelegenheit gegeben werden, vor Erteilung der Bescheinigung auch den Rohbauzustand zu be- sichtigen. Die Bescheinigung braucht der Bauaufsichtsbehörde nicht vorgelegt werden. Sollten Mängel festgestellt werden, wird die oder der BZSM dies der Bauaufsichtsbe- hörde von sich aus mitzuteilen. Mit Erteilung der Baugenehmigung erhält die/der für den Bezirk zuständige BZSM au- tomatisch hierüber eine Information durch die Bauaufsichtsbehörde. Eine Übersicht über die Bezirke und der/des jeweils zuständigen BZSM ist auf der Rückseite abge- druckt und kann jeweils aktuell auf der Internetseite des Hochsauerlandkreises unter www.hochsauerlandkreis.de (Dienstleistungen A - Z, Schornsteinfegerangelegenhei- ten, Kehrbezirksverzeichnis) abgerufen werden. 04/2011 Bezirke der Bezirksschornsteinfegermeister Kehrbezirk HSK 08 (Eslohe) Bezirksschornsteinfegermeister -

Erfolgspremiere Für „Partnertage“ Der Polstermöbler 2 Inhalt

Magazin Unsere Wirtschaft Ausgabe 11/2020 Region Unternehmensförderung Aus- und Weiterbildung In der Coburger Wirtschaft kehrt Corona-Überbrückungshilfen Viele Nachzügler dank Hilfe von vorsichtiger Optimismus zurück ausgeweitet und vereinfacht Fachleuten noch in Ausbildung © Hagen Lehmann, Coburg Erfolgspremiere für „Partnertage“ der Polstermöbler 2 Inhalt Titelthema „Partnertage Oberfranken“: Geschäftslage unserer 4 Polstermöbel-Hersteller erfreulich stabil Konjunkturbericht Coburger Unternehmen wähnen sich im Herbst 7 größtenteils auf leichtem Erholungskurs © Feodora - stock-adobe.com Region Im achten Jahr des Dual Career Services 10 tritt auch der Landkreis der Initiative bei Arbeitsjubiläum: Beim Aufstieg des Familienunter- 11 nehmens war Roswitha Schumacher die Finanzchefi n 125-Jahr-Feier: Industrie- und Handelskammer 12 bereitet sich auf Jubiläumsjahr 2021 vor Aus- und Weiterbildung Nachvermittlungsaktion zum Beginn des neuen 13 Ausbildungsjahres durch Angebotsüberhang begünstigt Zwei Jahre berufsbegleitende Weiterbildung haben 14 sich für 13 neue Industriemeister gelohnt Existenzgründung und Unternehmensförderung 18 Existenzsicherung bei coronabedingten Umsatzausfällen Die neue Chefi n des „Münchner Hofbräu“ 19 in Coburg vertraut auf Großmutters Küche Staatliche Überbrückungshilfen ausgeweitet Sonderthema „Energieeffi zienz“ Die als Überbrückungshilfen für klei- umfassenden Zuschüsse sind verlängert Förderung für Unternehmensinvestionen 20 ne und mittelständische Unternehmen, und ausgeweitet worden. Zudem wur- wurde gebündelt, -

Purchaser Guide

PURCHASER GUIDE WELCOME TO ASCENT Tucked at the base of revered Camelback Mountain, Ascent is a new private residential enclave, AT THE PHOENICIAN® adjacent to The Phoenician®—one of Arizona’s premier luxury resort destinations. This community incorporates the Sonoran Desert landscape directly into its design, at the most enviable location in Scottsdale. ASCENT AT THE PHOENICIAN AN ICONIC RESORT DESTINATION Ascent is located next to The Phoenician® — a world class hotel property on the edge of Arizona’s Sonora Desert. For decades The Phoenician has guided guests through an evolving journey distinctly designed to nurture, inspire, and rejuvenate. Offering multiple experiences on one diverse property, the resort’s award-winning Luxury Collection includes The Phoenician, The Canyon Suites, The Phoenician Suites, and a full range of world-class amenities. SERENITY NEAR THE HEART OF SCOTTSDALE Tucked against the backdrop of Camelback Mountain, Ascent is steps from the amenities of The Phoenician® and in close proximity to the boutiques, restaurants, and galleries of Old Town Scottsdale and Fashion Square. Homes highlight desert contemporary design with outdoor living spaces and a private homeowner pool and fitness amenity on the south slope of Camelback Mountains. All images, renderings and specifications on this page are for illustrative and representation purposes only and subject to change without notice. PAGE 3 ASCENT AT THE PHOENICIAN WORLD CLASS DINING J&G Steakhouse, Mowry & Cotton, Thirsty Camel, Afternoon Tea – From classic French dishes to hand-crafted cocktails and poolside snacks, The Phoenician® has many innovative dining options to satisfy every mood – and every craving. A WORLD CLASS DESERT PROPERTY An iconic resort destination, The Phoenician® recently completed an extensive renovation. -

Schmallenberg 2030. Bad Fredeburg Städtebaulicher Rahmenplan Für Die Ortsmitte Teil a Grundlagen Und Analyse Teil B Ziele Und Rahmenkonzept

Schmallenberg 2030. Bad Fredeburg Städtebaulicher Rahmenplan für die Ortsmitte Teil A Grundlagen und Analyse Teil B Ziele und Rahmenkonzept 1 Schmallenberg 2030. Bad Fredeburg Städtebaulicher Rahmenplan für die Ortsmitte Teil A Grundlagen und Analyse Teil B Leitbild und Ziele Auftraggeber Stadt Schmallenberg Bearbeitung pp a|s pesch partner architekten stadtplaner Hörder Burgstraße 11 44263 Dortmund www.pesch-partner.de in Zusammenarbeit mit der Stadt Schmallenberg Juni 2015 Aus Gründen der besseren Lesbarkeit wird auf die gleichzeitige Verwendung männlicher und weiblicher Sprachformen verzichtet. Sämtliche Personen- bezeichnungen gelten gleichwohl für beiderlei Geschlecht. 2 INHALT 1 Zur Aufgabe 05 Teil A Grundlagen und Analyse 2 Rahmenbedingungen 07 2.1 Bad Fredeburg | Ein Überblick 07 2.2 Schmallenberg 2030 | Ziele der Stadtentwicklung 09 2.3 Themen, Planungen und Umsetzungsstand 09 3 Die Ortsmitte von Bad Fredeburg | Stärken, Schwächen, Herausforderungen 14 3.1 Historische Entwicklung und Ortsgrundriss 14 3.2 Ortsbild und Freiraum 17 3.3 Nutzungen 25 3.4 Verkehr: Straßen, Wege, Plätze 30 Teil B Ziele und Rahmenkonzept 4 Leitbild und Ziele: Die Zukunft der Ortsmitte 33 4.1 Beteiligung 33 4.2 Sechs Leitsätze zur Entwicklung der Ortsmitte 34 5 Städtebauliches Konzept 5.1 Konzept Stadt- und Freiraum | „Die Ortsmitte und die Landschaft entwickeln und verbinden“ 5.2 Nutzungskonzept | „Die Vielfalt erhalten“ 5.3 Verkehrskonzept | „Die Mobilität gestalten“ 5.4 Konzept Umsetzung und Beteiligung 5.5 Schlüsselprojekte Teil C Handlungsprogramm 6 Maßnahmen- und Durchführungskonzept 7 Projektblätter 3 4 1 ZUR AUFGABE Eine Schlüsselfunktion für die Gesamtentwicklung Schmallenbergs übernehmen die beiden Kernorte Schmallenberg und Bad Fredeburg. Daher schlägt das im Februar 2012 vom Rat der Stadt beschlossene Integrierte Stadtentwicklungskonzept die Erarbeitung von Rahmenplänen für die beiden Kernorte vor. -

Ortszuordnung Zu Brennwertbezirken Bayernwerk AG

Ortszuordnung zu Brennwertbezirken Bayernwerk AG Temperatur- DWD Stations-ID messstelle Stations- meteomedia- Postleitzahl Ort Vorgelagerter Netzbetreiber Brennwertbezirk Netzkopplungspunkt 1 Netzkopplungspunkt 2 Netzkopplungspunkt 3 Netzkopplungspunkt 4 Stationsbetreiber kennung Lieferungen 91325 Adelsdorf Open Grid Regional 1 BAG Waidhaus Adelsdorf Höchstadter Str. Coburg meteomedia 106700 91334 Hemhofen Open Grid Regional 1 BAG Waidhaus Adelsdorf Höchstadter Str. Coburg meteomedia 106700 91334 Zeckern Open Grid Regional 1 BAG Waidhaus Adelsdorf Höchstadter Str. Coburg meteomedia 106700 95659 Arzberg Open Grid Regional 1 BAG Waidhaus Arzberg Rosenbühl Hof DWD 10685 106850 95659 Oschwitz - Arzberg Open Grid Regional 1 BAG Waidhaus Arzberg Rosenbühl Hof DWD 10685 106850 95659 Röthenbach - Arzberg Open Grid Regional 1 BAG Waidhaus Arzberg Rosenbühl Hof DWD 10685 106850 95659 Rosenbühl - Arzberg Open Grid Regional 1 BAG Waidhaus Arzberg Rosenbühl Hof DWD 10685 106850 95659 Sandmühle - Arzberg Open Grid Regional 1 BAG Waidhaus Arzberg Rosenbühl Hof DWD 10685 106850 95659 Schlottenhof - Arzberg Open Grid Regional 1 BAG Waidhaus Arzberg Rosenbühl Hof DWD 10685 106850 95659 Schacht - Arzberg Open Grid Regional 1 BAG Waidhaus Arzberg Rosenbühl Hof DWD 10685 106850 91275 Auerbach i.d.OPf. Open Grid Regional 1 BAG Waidhaus Auerbach in der Opf. Rosenh. Str. Weiden DWD 10688 106880 91275 Michelfeld Open Grid Regional 1 BAG Waidhaus Auerbach in der Opf. Rosenh. Str. Weiden DWD 10688 106880 91275 Neumühle Open Grid Regional 1 BAG Waidhaus Auerbach in der Opf. Rosenh. Str. Weiden DWD 10688 106880 91275 Rosenhof Open Grid Regional 1 BAG Waidhaus Auerbach in der Opf. Rosenh. Str. Weiden DWD 10688 106880 91275 Sand Open Grid Regional 1 BAG Waidhaus Auerbach in der Opf. -

Ergebnisliste Bayernpokal 2016 Im 4Er Und 6Er Kunstrad Und Einrad

Ergebnisliste Bayernpokal 2016 im 4er und 6er Kunstrad und Einrad am 19.06.2016 in der Frankenland-Halle, Am Sportplatz 14, 96237 Ebersdorf bei Coburg 4er Einrad U13 weiblich aufg. ausg. Isabell Heinisch / Minu-Lucy Hornung / Anna Kichhof / Amelie 1 RKV Solidarität Schweinfurt 1 88,30 80,38 Schiwa 2 Bianca Gräsl / Karla Keller / Emilia Melissa / Annika Schuster RSV Solidarität Rimpar e.V. 65,80 62,93 3 Michelle Scharf / Julia Mahr / Finja Melzer / Lea Ultsch RSV Soli Reuth 1 64,00 62,45 4 Anouk Drexler / Johanna Herrle / Johanna Stangl / Sarah Meyr RV Burgheim 1 69,30 61,38 Lina Winkelmann / Johanna Kürten / Selina Litz / Leah 5 RKV Herzogenaurach 3 62,80 56,09 Gonzalez 6 Maja Waldhauser / Alice Petukhov / Jule Pötzl / Julie Mennerat RKV Herzogenaurach 4 60,50 55,13 7 Jule Winter / Helene Gebhardt / Leni Rether / Kim Kratzer RKV Solidarität Schweinfurt 2 66,80 52,43 8 Leah Horcher / Denise Hunger / Ines Schrempf / Nicole Müller RSV Solidarität Frohnlach 3 66,70 50,38 Luisa Tschall / Pauline Lange / Annemarie Hellmann / Franca 9 Soli Waldbüttelbrunn 6 61,20 39,48 Bühlmeier 10 Marie Da Sois / Anna Gagel / Soffi Leistner / Antonia Scheler RSV Solidarität Frohnlach 4 53,90 38,08 Magdalena Artner / Rebecca Barth / Theresa Mayr / Anita 11 RV Burgheim 2 54,60 36,55 Nikolla 12 Nina Körber / Felicitas Kürten / Laura Ciliax / Hannah Kocks RKV Herzogenaurach 5 42,60 22,13 Marie Hackel / Angelina Spiegel / Katharina Mertel / Sarah Zürn Soli Waldbüttelbrunn 5 60,50 Ausfall Hannah Schober / Konstanze Hayden / Selina Litz / Kim Kreß RKV Herzogenaurach 2 62,80 Ausfall Luisa Gubernator / Sophia Hümmer / Antonia Weidenhammer / Soli Waldbüttelbrunn 4 70,90 Ausfall Emily Fries 6er Kunstrad Elite aufg.