Pre-Transaction Global Crossing Corporate Structure

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hacking the Master Switch? the Role of Infrastructure in Google's

Hacking the Master Switch? The Role of Infrastructure in Google’s Network Neutrality Strategy in the 2000s by John Harris Stevenson A thesis submitteD in conformity with the requirements for the Degree of Doctor of Philosophy Faculty of Information University of Toronto © Copyright by John Harris Stevenson 2017 Hacking the Master Switch? The Role of Infrastructure in Google’s Network Neutrality Strategy in the 2000s John Harris Stevenson Doctor of Philosophy Faculty of Information University of Toronto 2017 Abstract During most of the decade of the 2000s, global Internet company Google Inc. was one of the most prominent public champions of the notion of network neutrality, the network design principle conceived by Tim Wu that all Internet traffic should be treated equally by network operators. However, in 2010, following a series of joint policy statements on network neutrality with telecommunications giant Verizon, Google fell nearly silent on the issue, despite Wu arguing that a neutral Internet was vital to Google’s survival. During this period, Google engaged in a massive expansion of its services and technical infrastructure. My research examines the influence of Google’s systems and service offerings on the company’s approach to network neutrality policy making. Drawing on documentary evidence and network analysis data, I identify Google’s global proprietary networks and server locations worldwide, including over 1500 Google edge caching servers located at Internet service providers. ii I argue that the affordances provided by its systems allowed Google to mitigate potential retail and transit ISP gatekeeping. Drawing on the work of Latour and Callon in Actor– network theory, I posit the existence of at least one actor-network formed among Google and ISPs, centred on an interest in the utility of Google’s edge caching servers and the success of the Android operating system. -

Telecom in the Time of Crash

INCIDENTAL PAPER Telecom in the Time of Crash Kas Kalba November 2002 Program on Information Resources Policy Center for Information Policy Research Harvard University The Program on Information Resources Policy is jointly sponsored by Harvard University and the Center for Information Policy Research. Chairman Managing Director Anthony G. Oettinger John C. B. LeGates Kas Kalba is President of Kalba International, Inc., a management consulting and research firm. He is writing a book on the telecom crash, from which this paper is derived, and has been a longstanding participant in PIRP activities. Copyright © 2002 by Kas Kalba. Not to be reproduced in any form without written consent from Kas Kalba, Kalba International. Inc., 23 Sandy Pond Road, Lincoln, 01773, USA. +1 (781) 259-9589. E-mail: [email protected] URL: http://www.kalbainternational.com ISBN 1-879716-85-2 I-02-2 November 2002 PROGRAM ON INFORMATION RESOURCES POLICY Harvard University Center for Information Policy Research Affiliates AT&T Corp. Nippon Telegraph & Telephone Corp Australian Telecommunications Users (Japan) Group PDS Consulting BellSouth Corp. PetaData Holdings, Inc. The Boeing Company Samara Associates Booz Allen Hamilton Skadden, Arps, Slate, Meagher & Flom Center for Excellence in Education LLP Commission of the European Sonexis Communities Strategy Assistance Services Critical Path TOR LLC CyraCom International United States Government: Ellacoya Networks, Inc. Department of Commerce Hanaro Telecom Corp. (Korea) National Telecommunications and Hearst Newspapers Information Administration Hitachi Research Institute (Japan) Department of Defense IBM Corp. National Defense University Korea Telecom Department of Health and Human Lee Enterprises, Inc. Services Lexis–Nexis National Library of Medicine John and Mary R. -

Growth of the Internet

Growth of the Internet K. G. Coffman and A. M. Odlyzko AT&T Labs - Research [email protected], [email protected] Preliminary version, July 6, 2001 Abstract The Internet is the main cause of the recent explosion of activity in optical fiber telecommunica- tions. The high growth rates observed on the Internet, and the popular perception that growth rates were even higher, led to an upsurge in research, development, and investment in telecommunications. The telecom crash of 2000 occurred when investors realized that transmission capacity in place and under construction greatly exceeded actual traffic demand. This chapter discusses the growth of the Internet and compares it with that of other communication services. Internet traffic is growing, approximately doubling each year. There are reasonable arguments that it will continue to grow at this rate for the rest of this decade. If this happens, then in a few years, we may have a rough balance between supply and demand. Growth of the Internet K. G. Coffman and A. M. Odlyzko AT&T Labs - Research [email protected], [email protected] 1. Introduction Optical fiber communications was initially developed for the voice phone system. The feverish level of activity that we have experienced since the late 1990s, though, was caused primarily by the rapidly rising demand for Internet connectivity. The Internet has been growing at unprecedented rates. Moreover, because it is versatile and penetrates deeply into the economy, it is affecting all of society, and therefore has attracted inordinate amounts of public attention. The aim of this chapter is to summarize the current state of knowledge about the growth rates of the Internet, with special attention paid to the implications for fiber optic transmission. -

The Great Telecom Meltdown for a Listing of Recent Titles in the Artech House Telecommunications Library, Turn to the Back of This Book

The Great Telecom Meltdown For a listing of recent titles in the Artech House Telecommunications Library, turn to the back of this book. The Great Telecom Meltdown Fred R. Goldstein a r techhouse. com Library of Congress Cataloging-in-Publication Data A catalog record for this book is available from the U.S. Library of Congress. British Library Cataloguing in Publication Data Goldstein, Fred R. The great telecom meltdown.—(Artech House telecommunications Library) 1. Telecommunication—History 2. Telecommunciation—Technological innovations— History 3. Telecommunication—Finance—History I. Title 384’.09 ISBN 1-58053-939-4 Cover design by Leslie Genser © 2005 ARTECH HOUSE, INC. 685 Canton Street Norwood, MA 02062 All rights reserved. Printed and bound in the United States of America. No part of this book may be reproduced or utilized in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without permission in writing from the publisher. All terms mentioned in this book that are known to be trademarks or service marks have been appropriately capitalized. Artech House cannot attest to the accuracy of this information. Use of a term in this book should not be regarded as affecting the validity of any trademark or service mark. International Standard Book Number: 1-58053-939-4 10987654321 Contents ix Hybrid Fiber-Coax (HFC) Gave Cable Providers an Advantage on “Triple Play” 122 RBOCs Took the Threat Seriously 123 Hybrid Fiber-Coax Is Developed 123 Cable Modems -

Designated Agents for Local Exchange Carriers

Designated Agents for Local Exchange Carriers Document Processor Document Processor 321 Communications, Inc. Access Point, Inc. InCorp Services, Inc. Illinois Corporation Service Company 2501 Chatham Rd., Ste. 110 801 Adlai Stevenson Dr. Springfield IL 62704-7100 Springfield IL 62703-4261 Lisa Brown John Petrakis 321 Communications, Inc. Access2Go, Inc. Regulatory and Tax Consultants 4700 N. Prospect Rd. 3483 Satellite Blvd., Ste. 202 Peoria Heights IL 61616 Duluth GA 30096-5800 Document Processor Document Processor ACN Communication Services, Inc. 360networks (USA) inc. C T Corporation System C T Corporation System 208 S. LaSalle St. 208 S. LaSalle St. Chicago IL 60604 Chicago IL 60604 Doug Forster Document Processor ACN Communication Services, Inc. AboveNet Communications, Inc. Technologies Management, Inc. d/b/a AboveNet Media Networks PO Drawer 200 Illinois Corporation Service Company Winter Park FL 32790-0200 801 Adlai Stevenson Dr. Springfield IL 62703-4261 James W. Broemmer Jr Adams Telephone Co-Operative Robert Sokota PO Box 217 AboveNet Communications, Inc. Golden IL 62339 d/b/a AboveNet Media Networks 360 Hamilton Blvd. James W. Broemmer Jr White Plains NY 10601 Adams TelSystems, Inc. PO Box 217 Robert Neumann Golden IL 62339 Access Media 3, Inc. 900 Commerce Dr., Ste. 200 Gary Pieper Oak Brook IL 60523 Advanced Integrated Technologies Inc. PO Box 51 Brian McDermott Columbia IL 62236 Access Media 3, Inc. Synergies Law Group, PLLC Mark Lammert 1002 Parker St. Advanced Integrated Technologies Inc. Falls Church VA 22046 Compliance Solutions Inc. 740 Florida Central Pkwy., Ste. 2028 Document Processor Longwood FL 32750 Access One, Inc. Corporation Service Company Ronald Dougherty 422 N. -

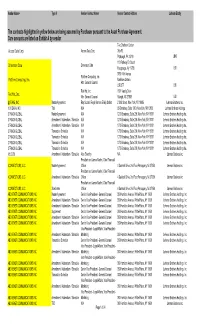

The Contracts Highlighted in Yellow Below Are Being Assumed by Purchaser Pursuant to the Asset Purchase Agreement. Cure Amounts Are Listed on Exhibit a by Vendor

Vendor Name+ Type II Vendor Contact Name Vendor Contact Address Lehman Entity The contracts highlighted in yellow below are being assumed by Purchaser pursuant to the Asset Purchase Agreement. Cure amounts are listed on Exhibit A by vendor. Two Chatham Center Access Data Corp. Access Data Corp. 24th FL Pittsburgh, PA 15219 LBHI 110 Parkway Dr. South Dimension Data Dimension Data Hauppauge, Ny 11788 LBI 3760 14th Avenue Platform Computing, Inc. Platform Computing, Inc. Markham Ontario Attn: General Counsel L3R 3T7 LBI Red Hat, Inc. 1801 Varsity Drive Red Hat, Inc. Attn: General Counsel Raleigh, NC 27606 LBI @STAKE, INC Master Agreement Ray Scutari, Royal Hansen, Emily Sebert 2 Wall Street, New York, NY 10005 Lehman Brothers, Inc. 1010 DATA, INC Trial N/A 65 Broadway, Suite 1010, New York, NY 10006 Lehman Brothers Holdings 2 TRACK GLOBAL Master Agreement N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Amendment / Addendum / Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Amendment / Addendum / Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Transaction Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Transaction Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Transaction Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Transaction Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. -

Worldcom1 Ethics Case Study

fWorldCom1 By Dennis Moberg (Santa Clara University) and Edward Romar (University of Massachusetts- Boston) An update for this case is available. 2002 saw an unprecedented number of corporate scandals: Enron, Tyco, Global Crossing. In many ways, WorldCom is just another case of failed corporate governance, accounting abuses, and outright greed. But none of these other companies had senior executives as colorful and likable as Bernie Ebbers. A Canadian by birth, the 6 foot, 3 inch former basketball coach and Sunday School teacher emerged from the collapse of WorldCom not only broke but with a personal net worth as a negative nine-digit number.2 No palace in a gated community, no stable of racehorses or multi-million dollar yacht to show for the telecommunications giant he created. Only debts and red ink--results some consider inevitable given his unflagging enthusiasm and entrepreneurial flair. There is no question that he did some pretty bad stuff, but he really wasn't like the corporate villains of his day: Andy Fastow of Enron, Dennis Koslowski of Tyco, or Gary Winnick of Global Crossing.3 Personally, Bernie is a hard guy not to like. In 1998 when Bernie was in the midst of acquiring the telecommunications firm MCI, Reverend Jesse Jackson, speaking at an all-black college near WorldCom's Mississippi headquarters, asked how Ebbers could afford $35 billion for MCI but hadn't donated funds to local black students. Businessman LeRoy Walker Jr., was in the audience at Jackson's speech, and afterwards set him straight. Ebbers had given over $1 million plus loads of information technology to that black college. -

In Re: Global Crossing, Ltd. Securities Litigation 02-CV-00910-Notice Of

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK ________________________________________________ x IN RE GLOBAL CROSSING, LTD. : Case No. 02 Civ. 910 (GEL) SECURITIES LITIGATION : ________________________________________________ x NOTICE OF PROPOSED CLASS ACTION PARTIAL SETTLEMENT, MOTION FOR ATTORNEYS' FEES AND FAIRNESS HEARING IN CONNECTION WITH THE ANDERSEN SETTLEMENT If You Bought or Exchanged Global Crossing Ltd. Securities or Asia Global Crossing Ltd. Securities between February 1, 1999 and December 8, 2003, you might be a member of the class in this action entitling you to receive relief in connection with a partial settlement of the action. A federal court authorized this Notice. This is not a solicitation from a lawyer. ■ On July 7, 2005, a settlement between the plaintiffs and Arthur Andersen LLP (the “Settlement”) was preliminarily approved by the Court in the action captioned above. The Settlement partially resolves a lawsuit over whether the prices of common stock, convertible preferred stock and bonds of Global Crossing and Asia Global Crossing were artificially inflated as a result of alleged fraudulent misrepresentations and non-disclosures and violations of federal securities laws. ■ The Settlement provides for a Settlement Fund of approximately $25 million, less fees and costs. The amount to be distributed among the class members will be divided between Global Crossing and Asia Global Crossing securities purchasers, with Global Crossing securities purchasers getting 92% of the amount and Asia Global Crossing securities purchasers getting the remaining 8%. ■ As explained below, this is the third partial settlement in this lawsuit. If you qualify and have not filed a claim in either of the prior settlements and would like to submit one, you may do so. -

Certificate of Service

CERTIFICATE OF SERVICE I, Charlotte R. Graham, hereby certify that the persons on the attached list were served copies ofthe Public Notice ofNetwork Change Under Rule 51.329(a) filed on the 26th day of July, 2002, with the Secretary, Federal Communications Commission. Such notification was provided via U.S. First Class Mail, postage prepaid, or by electronic transmission at least five business days in advance of filing with the Commission. ~Q.~ Charlotte R. Graham _ ..__._-------------------------------------- 1-800-Reconex 1-800-Reconex 1-800-Reconex Bill Braun Jennifer Loewen Dale Merten 2500 Industrial Ave. 2500 Industrial Avenue 2500 Industrial Avenue Hubbard, OR 97032 Hubbard, OR 97032 Hubbard, OR 97032 1-800-Reconex 2-Infinity Access America Jennifer Sikes Lex Long Dan Barnett 2500 Industrial Ave 4828 Loop Central Dr. 315 W. Oakland Ave. Hubbard, OR 97032 Ste. 100 Johnson City, TN 37601 Houston, TX 77081 Access America Access Long Distance Access Long Distance Jack Coker Tammy Hampton Christina Moody 138 Fairbanks Plaza 215 S. State Street 3753 Howard Hughes Pkwy Oakridge, TN 37830 Salt Lake City, UT 84111 Suite 131 Las Vegas, NV 89109 Access One (The Other Phone Company) ACN Communications ACT (Alternate Communications Kevin Griffo S. Meyer Technology) 3427 NW. 55th 32991 Hamilton Benjamin Bickham Ft. Lauderdale, FL 33309 Farmington Hills, MI 48334 6253 W. 800 N. Fountaintown, IN 46130 Adams Communications Adelphia Business Solutions Adelphia Business Solutions Jimmy Adams Rebecca Baldwin Stacey Chick P.O. Box 487 1221 Lamar Street 121 Champion Way Marianna, FL 324470487 Ste. 1175 Canonsburg, PA 15317 Houston, TX 770I0 Adelphia Business Solutions Adelphia Business Solutions Adelphia Business Solutions Rod Fletcher Richard Kindred Janet Livengood 121 Champion Way 500 Atrium Drive 3000 K St., NW. -

NASD Notice to Members 99-46

Executive Summary $250, and two or more Market NASD Effective July 1, 1999, the maximum Ma k e r s . Small Order Execution SystemSM (S O E S SM ) order sizes for 336 Nasdaq In accordance with Rule 4710, Nas- Notice to National Market® (NNM) securities daq periodically reviews the maxi- will be revised in accordance with mum SOES order size applicable to National Association of Securities each NNM security to determine if Members Dealers, Inc. (NASD®) Rule 4710(g). the trading characteristics of the issue have changed so as to warrant For more information, please contact an adjustment. Such a review was 99-46 ® Na s d a q Market Operations at conducted using data as of March (203) 378-0284. 31, 1999, pursuant to the aforemen- Maximum SOES Order tioned standards. The maximum Sizes Set To Change SOES order-size changes called for Description by this review are being implemented July 1, 1999 Under Rule 4710, the maximum with three exceptions. SOES order size for an NNM security is 1,000, 500, or 200 shares, • First, issues were not permitted to depending on the trading characteris- move more than one size level. For Suggested Routing tics of the security. The Nasdaq example, if an issue was previously ® Senior Management Workstation II (NWII) indicates the categorized in the 1,000-share maximum SOES order size for each level, it would not be permitted to Ad v e r t i s i n g NNM security. The indicator “NM10,” move to the 200-share level, even if Continuing Education “NM5,” or “NM2” displayed in NWII the formula calculated that such a corresponds to a maximum SOES move was warranted. -

LIST of SECTION 13F SECURITIES ** PAGE 1 RUN TIME:09:57 Ivmool

RUN DATE:06/29/00 ** LIST OF SECTION 13F SECURITIES ** PAGE 1 RUN TIME:09:57 IVMOOl CUSIP NO. ISSUER NAME ISSUER DESCRIPTION STATUS B49233 10 7 ICOS VISION SYS CORP N V ORD B5628B 10 4 * LERNOUT & HAUSPIE SPEECH PRODS COM B5628B 90 4 LERNOUT & HAUSPIE SPEECH PRODS CALL B5628B 95 4 LERNOUT 8 HAUSPIE SPEECH PRODS PUT D1497A 10 1 CELANESE AG ORD D1668R 12 3 * DAIMLERCHRYSLER AG ORD D1668R 90 3 DAIMLERCHRYSLER AG CALL D1668R 95 3 DAIMLERCHRYSLER AG PUT F9212D 14 2 TOTAL FINA ELF S A WT EXP 080503 G0070K 10 3 * ACE LTD ORD G0070K 90 3 ACE LTD CALL G0070K 95 3 ACE LTD PUT GO2602 10 3 * AMDOCS LTD ORD GO2602 90 3 AMDOCS LTD CALL GO2602 95 3 AMDOCS LTD PUT GO2995 10 1 AMERICAN SAFETY INS GROUP LTD ORD G0352M 10 8 * AMWAY ASIA PACIFIC LTD COM DELETED G0352M 90 8 AMWAY ASIA PACIFIC LTD CALL DELETED G0352M 95 8 AMWAY ASIA PACIFIC LTD PUT DELETED GO3910 10 9 * ANNUITY AND LIFE RE HLDGS ORD GO3910 90 9 ANNUITY AND LIFE RE HLDGS CALL GO3910 95 9 ANNUITY AND LIFE RE HLDGS PUT GO4074 10 3 APEX SILVER MINES LTD ORD GO4074 11 1 APEX SILVER MINES LTD WT EXP 110402 GO4450 10 5 ARAMEX INTL LTD ORD GO5345 10 6 ASIA PACIFIC RES INTL HLDG LTD CL A G0535E 10 6 ASIA PACIFIC WIRE & CABLE CORP ORD GO5354 10 8 ASIACONTENT COM LTD CL A ADDED G1368B 10 2 BRILLIANCE CHINA AUTO HLDG LTD COM DELETED 620045 20 2 CENTRAL EUROPEAN MEDIA ENTRPRS CL A NEW G2107X 10 8 CHINA TIRE HLDGS LTD COM G2108N 10 9 * CHINADOTCOM CORP CL A G2108N 90 9 CHINADOTCOM CORP CALL G2lO8N 95 9 CHINADOTCOM CORP PUT 621082 10 5 CHINA YUCHAI INTL LTD COM 623257 10 1 COMMODORE HLDGS LTD ORD 623257 11 -

ZILLOW GROUP, INC. (Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 14A (Rule 14a-101) INFORMATION REQUIRED IN PROXY STATEMENT SCHEDULE 14A INFORMATION Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 (Amendment No. ) Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐ Check the appropriate box: ☐ Preliminary Proxy Statement ☐ Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) ☒ Definitive Proxy Statement ☐ Definitive Additional Materials ☐ Soliciting Material under § 240.14a-12 ZILLOW GROUP, INC. (Name of Registrant as Specified in its Charter) N/A (Name of Person(s) Filing Proxy Statement, if Other Than the Registrant) Payment of Filing Fee (Check the appropriate box): ☒ No fee required. ☐ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: ☐ Fee paid previously with preliminary materials. ☐ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing.