Telecom in the Time of Crash

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Marginable OTC Stocks

List of Marginable OTC Stocks @ENTERTAINMENT, INC. ABACAN RESOURCE CORPORATION ACE CASH EXPRESS, INC. $.01 par common No par common $.01 par common 1ST BANCORP (Indiana) ABACUS DIRECT CORPORATION ACE*COMM CORPORATION $1.00 par common $.001 par common $.01 par common 1ST BERGEN BANCORP ABAXIS, INC. ACETO CORPORATION No par common No par common $.01 par common 1ST SOURCE CORPORATION ABC BANCORP (Georgia) ACMAT CORPORATION $1.00 par common $1.00 par common Class A, no par common Fixed rate cumulative trust preferred securities of 1st Source Capital ABC DISPENSING TECHNOLOGIES, INC. ACORN PRODUCTS, INC. Floating rate cumulative trust preferred $.01 par common $.001 par common securities of 1st Source ABC RAIL PRODUCTS CORPORATION ACRES GAMING INCORPORATED 3-D GEOPHYSICAL, INC. $.01 par common $.01 par common $.01 par common ABER RESOURCES LTD. ACRODYNE COMMUNICATIONS, INC. 3-D SYSTEMS CORPORATION No par common $.01 par common $.001 par common ABIGAIL ADAMS NATIONAL BANCORP, INC. †ACSYS, INC. 3COM CORPORATION $.01 par common No par common No par common ABINGTON BANCORP, INC. (Massachusetts) ACT MANUFACTURING, INC. 3D LABS INC. LIMITED $.10 par common $.01 par common $.01 par common ABIOMED, INC. ACT NETWORKS, INC. 3DFX INTERACTIVE, INC. $.01 par common $.01 par common No par common ABLE TELCOM HOLDING CORPORATION ACT TELECONFERENCING, INC. 3DO COMPANY, THE $.001 par common No par common $.01 par common ABR INFORMATION SERVICES INC. ACTEL CORPORATION 3DX TECHNOLOGIES, INC. $.01 par common $.001 par common $.01 par common ABRAMS INDUSTRIES, INC. ACTION PERFORMANCE COMPANIES, INC. 4 KIDS ENTERTAINMENT, INC. $1.00 par common $.01 par common $.01 par common 4FRONT TECHNOLOGIES, INC. -

Issue 23 November 2005 1 Submarine Telecoms Forum Is Published Bi-Monthly by WFN Strategies, L.L.C

DDefenseefense & Non-traditionaNon-traditional CableCable SystemsSystems – 4th4th AnnAnniiversaryversary IssueIssue November 2005 Issue 23 1 Submarine Telecoms Forum is published bi-monthly by WFN Strategies, L.L.C. The publication may not be reproduced or transmitted in any form, in whole or in part, without the Exordium permission of the publishers. NNovember’sovember’s iissuessue mmarksarks ourour ffourthourth aanniversarynniversary inin publishingpublishing SubmarineSubmarine TelecomsTelecoms Forum,Forum, andand thoughthough tthngshngs sstilltill aaren’tren’t aass rrosyosy aass theythey werewere inin thethe “build“build itit andand theythey willwill come”come” era,era, nornor willwill theythey probablyprobably everever Submarine Telecoms Forum is an independent com- bbee – tthingshings aarere stillstill ccertainlyertainly mmuchuch improved.improved. mercial publication, serving as a freely accessible forum for professionals in industries connected with submarine optical TThehe ffewew pprinciplesrinciples wwee establishedestablished inin thethe beginning,beginning, wewe continuecontinue toto holdhold dear.dear. WeWe promisedpromised then,then, andand fi bre technologies and techniques. ccontinueontinue ttoo ppromiseromise yyou,ou, oourur rreaders:eaders: Liability: while every care is taken in preparation of this 11.. TThathat wwee wwillill pproviderovide a wwideide rrangeange ooff iideasdeas aandnd iissues;ssues; publication, the publishers cannot be held responsible for the 22.That.That wwee wwillill sseekeek ttoo iincite,ncite, eentertainntertain -

Download Date 30/09/2021 09:11:11

Index revisions, market quality and the cost of equity capital. Item Type Thesis Authors Aldaya, Wael H. Rights <a rel="license" href="http://creativecommons.org/licenses/ by-nc-nd/3.0/"><img alt="Creative Commons License" style="border-width:0" src="http://i.creativecommons.org/l/by- nc-nd/3.0/88x31.png" /></a><br />The University of Bradford theses are licenced under a <a rel="license" href="http:// creativecommons.org/licenses/by-nc-nd/3.0/">Creative Commons Licence</a>. Download date 30/09/2021 09:11:11 Link to Item http://hdl.handle.net/10454/5687 University of Bradford eThesis This thesis is hosted in Bradford Scholars – The University of Bradford Open Access repository. Visit the repository for full metadata or to contact the repository team © University of Bradford. This work is licenced for reuse under a Creative Commons Licence. Index revisions, market quality and the cost of equity capital Wael Hamdi Aldaya Submitted for the degree of Doctor of Philosophy School of Management University of Bradford 2012 i ABSTRACT Wael Hamdi AlDAYA Index revisions, market quality and the cost of equity capital Keywords: Index revisions, stock liquidity, cost of capital, market quality, price efficiency. This thesis examines the impact of FTSE 100 index revisions on the various aspects of stock market quality and the cost of equity capital. Our study spans over the period 1986–2009. Our analyses indicate that the index membership enhances all aspects of liquidity, including trading continuity, trading cost and price impact. We also show that the liquidity premium and the cost of equity capital decrease significantly after additions, but do not exhibit any significant change following deletions. -

Admission Document Prepared in Accordance with the AIM Rules

233582 Gold Cover Spread 8mm Spine 07/10/2014 14:06 Page 1 Placing and Admission to AIM Gamma Communications plc Nominated AdviserAdviser,, Broker & Sole Bookrunner Perivan Financial Print 233582 233582 Gold pp001-pp004 07/10/2014 14:06 Page 1 THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to the contents of this document or as to what action you should take you should consult your stockbroker, bank manager, solicitor, accountant or other independent financial adviser authorised under the Financial Services and Markets Act 2000 (“FSMA”) who specialises in advising on the acquisition of shares and other securities. This document comprises an admission document prepared in accordance with the AIM Rules. Application will be made for the Ordinary Shares to be admitted to trading on AIM. It is expected that Admission will become effective and that trading in the Ordinary Shares on AIM will commence at 8.00 a.m. on 10 October 2014. The Ordinary Shares are not dealt on any other recognised investment exchange and it is emphasised that no application has been, or is being, made for the Ordinary Shares to be admitted to any such exchange. This document is not an approved prospectus for the purposes of section 85 of FSMA, has not been prepared in accordance with the Prospectus Rules published by the Financial Conduct Authority (“FCA”) and a copy of it has not been, and will not be, delivered to the UK Listing Authority in accordance with the Prospectus Rules or delivered to or approved by any other authority which could be a competent authority for the purposes of the Prospectus Directive. -

Worldcom1 Ethics Case Study

fWorldCom1 By Dennis Moberg (Santa Clara University) and Edward Romar (University of Massachusetts- Boston) An update for this case is available. 2002 saw an unprecedented number of corporate scandals: Enron, Tyco, Global Crossing. In many ways, WorldCom is just another case of failed corporate governance, accounting abuses, and outright greed. But none of these other companies had senior executives as colorful and likable as Bernie Ebbers. A Canadian by birth, the 6 foot, 3 inch former basketball coach and Sunday School teacher emerged from the collapse of WorldCom not only broke but with a personal net worth as a negative nine-digit number.2 No palace in a gated community, no stable of racehorses or multi-million dollar yacht to show for the telecommunications giant he created. Only debts and red ink--results some consider inevitable given his unflagging enthusiasm and entrepreneurial flair. There is no question that he did some pretty bad stuff, but he really wasn't like the corporate villains of his day: Andy Fastow of Enron, Dennis Koslowski of Tyco, or Gary Winnick of Global Crossing.3 Personally, Bernie is a hard guy not to like. In 1998 when Bernie was in the midst of acquiring the telecommunications firm MCI, Reverend Jesse Jackson, speaking at an all-black college near WorldCom's Mississippi headquarters, asked how Ebbers could afford $35 billion for MCI but hadn't donated funds to local black students. Businessman LeRoy Walker Jr., was in the audience at Jackson's speech, and afterwards set him straight. Ebbers had given over $1 million plus loads of information technology to that black college. -

In Re: Global Crossing, Ltd. Securities Litigation 02-CV-00910-Notice Of

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK ________________________________________________ x IN RE GLOBAL CROSSING, LTD. : Case No. 02 Civ. 910 (GEL) SECURITIES LITIGATION : ________________________________________________ x NOTICE OF PROPOSED CLASS ACTION PARTIAL SETTLEMENT, MOTION FOR ATTORNEYS' FEES AND FAIRNESS HEARING IN CONNECTION WITH THE ANDERSEN SETTLEMENT If You Bought or Exchanged Global Crossing Ltd. Securities or Asia Global Crossing Ltd. Securities between February 1, 1999 and December 8, 2003, you might be a member of the class in this action entitling you to receive relief in connection with a partial settlement of the action. A federal court authorized this Notice. This is not a solicitation from a lawyer. ■ On July 7, 2005, a settlement between the plaintiffs and Arthur Andersen LLP (the “Settlement”) was preliminarily approved by the Court in the action captioned above. The Settlement partially resolves a lawsuit over whether the prices of common stock, convertible preferred stock and bonds of Global Crossing and Asia Global Crossing were artificially inflated as a result of alleged fraudulent misrepresentations and non-disclosures and violations of federal securities laws. ■ The Settlement provides for a Settlement Fund of approximately $25 million, less fees and costs. The amount to be distributed among the class members will be divided between Global Crossing and Asia Global Crossing securities purchasers, with Global Crossing securities purchasers getting 92% of the amount and Asia Global Crossing securities purchasers getting the remaining 8%. ■ As explained below, this is the third partial settlement in this lawsuit. If you qualify and have not filed a claim in either of the prior settlements and would like to submit one, you may do so. -

Certificate of Service

CERTIFICATE OF SERVICE I, Charlotte R. Graham, hereby certify that the persons on the attached list were served copies ofthe Public Notice ofNetwork Change Under Rule 51.329(a) filed on the 26th day of July, 2002, with the Secretary, Federal Communications Commission. Such notification was provided via U.S. First Class Mail, postage prepaid, or by electronic transmission at least five business days in advance of filing with the Commission. ~Q.~ Charlotte R. Graham _ ..__._-------------------------------------- 1-800-Reconex 1-800-Reconex 1-800-Reconex Bill Braun Jennifer Loewen Dale Merten 2500 Industrial Ave. 2500 Industrial Avenue 2500 Industrial Avenue Hubbard, OR 97032 Hubbard, OR 97032 Hubbard, OR 97032 1-800-Reconex 2-Infinity Access America Jennifer Sikes Lex Long Dan Barnett 2500 Industrial Ave 4828 Loop Central Dr. 315 W. Oakland Ave. Hubbard, OR 97032 Ste. 100 Johnson City, TN 37601 Houston, TX 77081 Access America Access Long Distance Access Long Distance Jack Coker Tammy Hampton Christina Moody 138 Fairbanks Plaza 215 S. State Street 3753 Howard Hughes Pkwy Oakridge, TN 37830 Salt Lake City, UT 84111 Suite 131 Las Vegas, NV 89109 Access One (The Other Phone Company) ACN Communications ACT (Alternate Communications Kevin Griffo S. Meyer Technology) 3427 NW. 55th 32991 Hamilton Benjamin Bickham Ft. Lauderdale, FL 33309 Farmington Hills, MI 48334 6253 W. 800 N. Fountaintown, IN 46130 Adams Communications Adelphia Business Solutions Adelphia Business Solutions Jimmy Adams Rebecca Baldwin Stacey Chick P.O. Box 487 1221 Lamar Street 121 Champion Way Marianna, FL 324470487 Ste. 1175 Canonsburg, PA 15317 Houston, TX 770I0 Adelphia Business Solutions Adelphia Business Solutions Adelphia Business Solutions Rod Fletcher Richard Kindred Janet Livengood 121 Champion Way 500 Atrium Drive 3000 K St., NW. -

Expmlanatory Memorandum for the Quarterly Report

Irish Communications Market Quarterly Key Data Explanatory Memorandum Document No: 05/92a Date: 20th December 2005 An Coimisiún um Rialáil Cumarsáide Commission for Communications Regulation Abbey Court Irish Life Centre Lower Abbey Street Dublin 1 Ireland Telephone +353 1 804 9600 Fax +353 1 804 9680 Email [email protected] Web www.comreg.ie Contents Contents ..............................................................................................1 1 Executive Summary..........................................................................2 2 Questionnaire Issue ..........................................................................3 3 Primary Data ...................................................................................1 4 Secondary data ................................................................................5 4.1 PRICING DATA..........................................................................................5 4.2 COMPARATIVE DATA ...................................................................................6 5 Glossary..........................................................................................7 6 PPP Conversion Rates data ................................................................0 1 ComReg 05/92a 1 Executive Summary Following the publication of an annual market review in November 1999, ComReg’s predecessor- the ODTR- published its first Quarterly Review on 22nd March 2000. Since that date, ComReg has continued to collect primary statistical data from authorised operators on a quarterly -

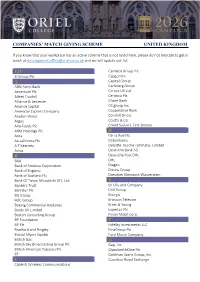

Matched Giving Company List

COMPANIES’ MATCH GIVING SCHEME UNITED KINGDOM If you know that your workplace has an active scheme that is not listed here, please do not hesitate to get in touch at [email protected] and we will update our list. 123 Camelot Group Plc 3i Group Plc Capgemini A Capital Group ABN Amro Bank Carlsberg Group Accenture Plc Cemex UK Ltd Alfred Dunhill Centrica Plc Alliance & Leicester Chase Bank Alliance Capital Citigroup Inc. American Express Company Cooperative Bank Anglian Water Cornhill Direct Argos Coutts & Co. Arla Foods Plc Credit Suisse | First Boston ARM Holdings Plc D Asda De La Rue Plc AstraZeneca Plc Debenhams A.T Kearney Deloitte Touche Tohmatsu Limited Aviva Deutsche Bank AG B Deutsche Post DHL BAA DHL Bank of America Corporation Diageo Bank of England Dixons Group Bank of Scotland Plc Dresdner Kleinwort Wasserstein Bank Of Tokyo-Mitsubishi UFJ, Ltd E Bankers Trust Eli Lilly and Company Barclays Plc EMI Group BG Group Energis BOC Group Ericsson Telecom Boeing Commercial Airplanes Ernst & Young Boots UK Limited Experian Plc Boston Consulting Group Exxon Mobil Corp. BP Foundation F BP Plc Fidelity Investments LLC Bradford and Bingley FirstGroup Plc Bristol-Myers Squibb Ford Motor Company British Gas G British Sky Broadcasting Group Plc Gap, Inc. British American Tobacco Plc GlaxoSmithKline Plc BT Goldman Sachs Group, Inc. C Guardian Royal Exchange Cable & Wireless Communications H Philips Halifax Phoenix Group Home Retail Group PPG Industries HSBC Bank Plc PricewaterhouseCoopers HSBC Holdings Plc Proctor & Gamble Co. I R IBM Reuters IDEO Robert Fleming & Co. Industrial Bank of Japan Rolls Royce J Royal Bank of Scotland Group Plc J P Morgan & Co Royal Dutch Shell Plc J Sainsbury Plc Royal London Mutual Insurance Society Limited Johnson & Johnson RSA Insurance Group Plc JPMorgan Chase Bank RWE npower Plc K S Kellogg’s Santander Group Kingfisher Plc Santander UK Plc KPMG LLP Schneider Electric L Schroders Plc Legal & General Group Plc Seaboard Corp. -

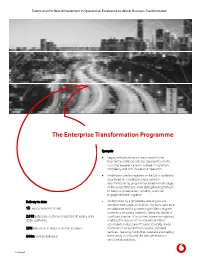

The Enterprise Transformation Programme

Submission for Best Achievement in Operational Excellence to deliver Business Transformation The Enterprise Transformation Programme Synopsis Legacy infrastructure is a major issue for the telecommunications industry. It presents a risk to customer experience and is a driver of significant complexity and cost for network operators. Vodafone is the first operator in the UK to tackle this issue head on; creating a unique network decommissioning programme tasked with all stages of the project lifecycle, from data gathering through to network power-down, including customer engagement and migration. Delivery to date: Underpinned by a proprietary data engine and workflow tool known as Kosmos, the team have built 15 Legacy networks closed an adaptable, evolving operating model to migrate customers off legacy networks. Using this model, a 2,018 Enterprise customers migrated off legacy onto significant number of customers have now migrated, stable platforms. enabling the closure of 15 networks and their associated products and IT stacks. Critically, these 29% Reduction in major customer incidents customers now benefit from reliable, standard services - reducing risk to their business and making £44m Savings delivered them ready to consume the next generation of connectivity solutions. C2 General “If we could walk away from the contract, we would. I don’t think Vodafone truly understands how precarious the relationship is” – Large utility customer, 2015. In 2012 Vodafone, traditionally a leader in mobile telecommunications, acquired Cable & Wireless Worldwide (CWW). The rationale behind the acquisition was to build a global fixed line communications powerhouse to meet the demands of an Enterprise market seeking fixed and mobile services, as well as IT, from a trusted communications partner. -

The End of Bankruptcy

University of Chicago Law School Chicago Unbound Coase-Sandor Working Paper Series in Law and Coase-Sandor Institute for Law and Economics Economics 2002 The ndE of Bankruptcy Robert K. Rasmussen Douglas G. Baird Follow this and additional works at: https://chicagounbound.uchicago.edu/law_and_economics Part of the Law Commons Recommended Citation Robert K. Rasmussen & Douglas G. Baird, "The ndE of Bankruptcy" (John M. Olin Program in Law and Economics Working Paper No. 173, 2002). This Working Paper is brought to you for free and open access by the Coase-Sandor Institute for Law and Economics at Chicago Unbound. It has been accepted for inclusion in Coase-Sandor Working Paper Series in Law and Economics by an authorized administrator of Chicago Unbound. For more information, please contact [email protected]. CHICAGO JOHN M. OLIN LAW & ECONOMICS WORKING PAPER NO. 173 (2D SERIES) The End of Bankruptcy Douglas G. Baird and Robert K. Rasmussen THE LAW SCHOOL THE UNIVERSITY OF CHICAGO This paper can be downloaded without charge at: The Chicago Working Paper Series Index: http://www.law.uchicago.edu/Lawecon/index.html The Social Science Research Network Electronic Paper Collection: http://ssrn.com/abstract_id=359241 The End of Bankruptcy Douglas G. Baird* & Robert K. Rasmussen** ABSTRACT The law of corporate reorganizations is conventionally justified as a way to preserve a firm’s going-concern value: Specialized assets in a particular firm are worth more together in that firm than anywhere else. This paper shows that this notion is mistaken. Its flaw is that it lacks a well- developed understanding of the nature of a firm. -

Worldcom's Bankruptcy Crisis

Center for Ethical Organizational Cultures Auburn University http://harbert.auburn.edu WorldCom’s Bankruptcy Crisis INTRODUCTION The story of WorldCom began in 1983 when businessmen Murray Waldron and William Rector sketched out a plan to create a long-distance telephone service provider on a napkin in a coffee shop in Hattiesburg, Miss. Their new company, Long Distance Discount Service (LDDS), began operating as a long distance reseller in 1984. Early investor Bernard Ebbers was named CEO the following year. Through acquisitions and mergers, LDDS grew quickly over the next 15 years. The company changed its name to WorldCom, achieved a worldwide presence, acquired telecommunications giant MCI, and eventually expanded beyond long distance service to offer the whole range of telecommunications services. WorldCom became the second-largest long-distance telephone company in America, and the firm seemed poised to become one of the largest telecommunications corporations in the world. Instead, it became the largest bankruptcy filing in U.S. history at the time and another name on a long list of those disgraced by the accounting scandals of the early 21st century. ACCOUNTING FRAUD AND ITS CONSEQUENCES Unfortunately for thousands of employees and shareholders, WorldCom used questionable accounting practices and improperly recorded $3.8 billion in capital expenditures, which boosted cash flows and profit over all four quarters in 2001 as well as the first quarter of 2002. This disguised the firm’s actual net losses for the five quarters because capital expenditures can be deducted over a longer period of time, whereas expenses must be subtracted from revenue immediately. WorldCom also spread out expenses by reducing the book value of assets from acquired companies and simultaneously increasing the value of goodwill.