Earnings Presentation First Quarter 2012

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Santiago, Chile RESULTADOS NEGOCIO COSTANERA CENTER PRINCIPALES HITOS CRECIMIENTO

Santiago, Chile RESULTADOS NEGOCIO COSTANERA CENTER PRINCIPALES HITOS CRECIMIENTO 01Resultados Negocio Chile & Argentina RESULTADOS NEGOCIO COSTANERA CENTER PRINCIPALES HITOS CRECIMIENTO Chile repite su positiva performance 2016 Resultados Cencosud Shopping Chile al cierre de Junio 2017 INGRESOS* VENTA VISITAS OCUPACIÓN (CLP$ BN) LOCATARIOS (MILLONES) (%) (CLP$ BN) 98,0% 97,9% 72,4 62,4 62,5 1.337 64,4 1.246 H1 2016 H1 2017 H1 2016 H1 2017 H1 2016 H1 2017 H1 2016 H1 2017 +12,4% +7,3% +0,1% -0,1 % *Excluye Ingresos por Alquiler de Empresas Relacionadas al grupo Cencosud. RESULTADOS NEGOCIO COSTANERA CENTER PRINCIPALES HITOS CRECIMIENTO DESACELERACIÓN ECONÓMICA EN ARGENTINA Impactó el poder de compra y visitas a los centros comerciales 2016 Resultados Cencosud Shopping Argentina al cierre de Junio 2017 INGRESOS* VENTA VISITAS OCUPACIÓN (ARS$ MM) LOCATARIOS (MILLONES) (%) (ARS$ BN) 97,4% 28,2 28,0 96,0% 817,1 18,6 689,9 15,6 H1 2016 H1 2017 H1 2016 H1 2017 H1 2016 H1 2017 H1 2016 H1 2017 +18,4% +19,0% -0,7% -1,4 % *Excluye Ingresos por Alquiler de Empresas Relacionadas al grupo Cencosud. RESULTADOS NEGOCIO COSTANERA CENTER PRINCIPALES HITOS CRECIMIENTO 02Costanera Center El mall de América Latina RESULTADOS NEGOCIO COSTANERA CENTER PRINCIPALES HITOS CRECIMIENTO COSTANERA CENTER ES EL Centro Comercial más relevante de América Latina Destino clave del turismo de compras en Chile: El “Miami” de América Latina según prensa extranjera. Más de 3,2 millones de visitas mensuales (5% de crecimiento contra 2016). Venta Locatarios +15% en 2017; Ingresos de alquiler +21%. Habilitación nuevas áreas comerciales. -

Costanera Center

SKIDATA Installations Shopping Centers Chile Costanera Center The Costanera Center is located in the up-and-coming business district of Santiago - unofficially known as “Sanhattan”. The complex, covering an area of 700,000 2m , includes the tallest skyscraper in Latin America, the “Gran Torre Santiago”, which is 300 meters high and has 64 floors, as well as the largest shopping center in the region with 300 stores, restaurants, a large cinema and a huge, high-quality supermarket. Every month, hundreds of thousands of visitors are welcomed to the center. After six years of construction, the Costanera Center finally opened its doors in 2012. The 5,700 available parking spaces, of which 3,500 are in the parking garages, are frequented by 12,000 vehicles daily. Additional parking facilities are currently in planning to meet the needs of hotel guests and the numerous companies which are moving into new offices in the “Gran Torre Santiago”. www.skidata.com Costanera Center Shopping Centers Chile Project description The owner and operator, Cencosud, was looking on which of the thousands of parking spaces his for an ultra-modern and reliable solution with a car is parked, he only needs to use one of the special focus on both design and functionality. SKIDATA automated pay stations. After reading Especially important was the ability to adapt the customer’s parking ticket, the system then to the current and future demands of the searches for the vehicle using its cameras. dynamic retail sector, particularly in light of the huge increase in the number of visitors For its regular customers, Cencosud offers a at peak shopping periods throughout the post-payment customer card (RFID-based), year, such as Christmas and Valentine’s Day. -

2018 Cod International Conference Chile Table of Contents

2018 COD INTERNATIONAL CONFERENCE CHILE TABLE OF CONTENTS Remarks 4 Introduction 4 Welcome to Chile 5 Thank You 6 AIA Board 8 Organizing Team 10 Seminar 12 Architecture Tour / Architects 14 Downtown 18 Campus 50 Modern Architecture 62 Contemporary Architecture 70 Additional Reading 98 2 AIA COD Conference, Santiago 2018 3 THE AIA COMMITTEE ON DESIGN 2018 COD THEME The AIA Committee on Design (COD) was The theme for the AIA Conference on founded to promote design excellence Architecture 2018 is Blueprint for Better among members of the AIA, the broader Cities. During 2018, the AIA Committee on design community, and the public at Design will visit Vancouver BC; New York; large, both nationally and internationally. and Santiago, Chile. What better places to The committee goals are to examine and visit to learn about the Blueprint for Better promote knowledge of contemporary Cities? Studying these three great cities design issues, to compare current design gives us the opportunity to delve into the and historic precedents, to learn from the important issues of planning, urban design, contrast or progression of ideas, and to architecture, and the significance of design! advocate leadership roles for architects These cities display excellence in design at within the fields of design and planning. As all levels, from the smallest scale to mega one of the largest interest areas within the developments. Our journey will expose us family of the AIA Knowledge Communities, to design excellence and the importance of the COD is the standard bearer for design design in our lives. in the Institute. The committee makes recommendations for Gold Medalists, Firm Awards, Honorary Fellows, and Institute Honor Awards. -

Q1-2012 Presentation (PDF, 645

Costanera Center, Santiago, Chile, height: 300m 109 elevators, of which 77 Schindler 7000 Welcome to Schindler 86 Schindler escalators and moving walks Selected key figures as of March 31, 2012 April 19, 2012 Highlights in Q1/2012 Pleasing start into 2012 – 9.5% growth in order intake in LC (+5.4% in CHF); especially in Asia/Pacific, India and Americas – Strong order backlog of CHF 6 795 million (+7.8% in LC, +5.5% in CHF) – 7.3% growth in revenue in LC (+3.1% in CHF); negative FX impact of CHF 77 million – E&E EBIT of CHF 224 million; negative FX impact of CHF 12 million – E&E EBIT margin: 11.8% (Q1/2011: 11.5%) – Net profit of CHF 156 million slightly above Q1/2011 level (before one-time book-gain of CHF 31 million in Q1/2011) – Strong operating cashflow of CHF 331 million – LEAP on track – Introduction of new products on track © Schindler | Corporate Communications | Page 2 E&E: Good development in all KPIs January - March ∆% In CHF million Q1/2012 Q1/2011 ∆% in LC Orders received 2 193 2 081 +5.4 +9.5 Revenue 1 904 1 846 +3.1 +7.3 Operating profit (EBIT) 224 212 +5.7 +11.3 in % 11.8 11.5 31.03.12 31.12.11 Order backlog 6 795 6 438 + 5.5 +7.8 Headcount at end of period 44 314 44 387 –0.2 © Schindler | Corporate Communications | Page 3 Group: Key figures as of March 31, 2012 January - March In CHF million Q1/2012 Q1/20111 ∆ in % ∆% in LC Revenue 1 904 1 846 +3.1 +7.3 Operating profit (EBIT) 214 201 +6.5 +12.4 Net income from financing/investing activities 3 12 Profit before taxes 217 213 +1.9 Profit from continuing operations 156 152 -

Cencosud Expects Revenues of Usd 22.5 Billion for 2013 and a 7.5

CENCOSUD EXPECTS REVENUES OF USD 22.5 BILLION FOR 1 2013 AND A 7.5% EBITDA MARGIN • As part of the plan to reduce leverage, Cencosud restricts its capex for 2013 to USD 731 million for organic growth. • Organic growth includes 58 store openings that represent almost a 5% increase in selling space. Santiago, February 19, 2013. - Cencosud defined its investment plan for 2013, which will reach USD 731 million with the following breakdown: • In Chile, total capex will be USD 242 million, including 17 new supermarkets, 1 Paris Store, 1 Easy and the conclusion of Costanera Center (USD 80 million capex). • For Brazil, we planned an investment amount of USD 116 million, which includes the opening of 15 new supermarkets. • In Peru, the total planned investment will be USD 80 million, which includes the opening of 10 supermarkets, 5 department stores and the development of a new Shopping Center of around 20,500 sqm selling space (Shopping Cerro Colorado in Arequipa). • For Argentina, the plan estimates approximately USD 23 million, for 5 supermarkets and 2 Easy stores. • Colombia’s organic capex will be USD 80 million, to open 1 supermarket, 1 Easy store and also includes the rebranding of the supermarket operation. • In addition, maintenance capex is planned at USD 90 million and IT expenditures at USD 100 million. Considering the aforementioned capital expenditures, Cencosud plans to generate total revenues of about USD 22.5 billion for 2013, with EBITDA of roughly USD 1,688 million, which results in a target EBITDA margin estimated in the order of 7.5%. -

Urban Shopping Malls and Sustainability Approaches in Chilean Cities: Relations Between Environmental Impacts of Buildings and Greenwashing Branding Discourses

sustainability Article Urban Shopping Malls and Sustainability Approaches in Chilean Cities: Relations between Environmental Impacts of Buildings and Greenwashing Branding Discourses Liliana De Simone 1,* and Mario Pezoa 2 1 Department of Applied Communications, Faculty of Communications, Pontificia Universidad Católica de Chile, Santiago 8320000, Chile 2 Department of Architecture, Universidad Diego Portales, Santiago 8320000, Chile; [email protected] * Correspondence: [email protected]; Tel.: +569-921-85528 Abstract: This article seeks to discuss the recent discrepancies between the environmental effects of large retail buildings located in urban centers and the media and corporate discourses that these retailers have on the environment and sustainability to the public and to local authorities. By using mixed methods of quantitative and qualitative data analysis of two of the biggest shopping centers in Santiago de Chile, this exploratory research seeks to inaugurate an interdisciplinary academic discussion on the relevance of comparing the media discourses about sustainability issued by urban developers and the physical effects that massive private buildings create in their surroundings. By using the retail resilience theoretical framework, this research seeks to understand the disruption Citation: De Simone, L.; Pezoa, M. in retail systems, both from socio-economic and environmental indicators. Comparing the environ- Urban Shopping Malls and mentally sensitive discourses promoted by Chilean retailers in advertising campaigns and corporate Sustainability Approaches in Chilean speeches with the environmental effects that large retail buildings brought to the surrounding ar- Cities: Relations between eas in terms of urban deforestation and increasing superficial temperature, this paper probes that Environmental Impacts of Buildings greenwashing campaign are not only used to impact corporate legitimacy with consumers and and Greenwashing Branding Discourses. -

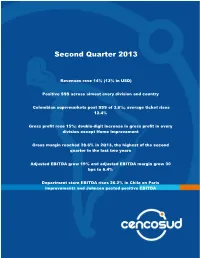

Second Quarter 2013

Second Quarter 2013 Revenues rose 14% (13% in USD) Positive SSS across almost every division and country Colombian supermarkets post SSS of 3.6%; average ticket rises 12.4% Gross profit rose 15%; double-digit increase in gross profit in every division except Home Improvement Gross margin reached 28.6% in 2Q13, the highest of the second quarter in the last two years Adjusted EBITDA grew 19% and adjusted EBITDA margin grew 30 bps to 6.4% Department store EBITDA rises 26.2% in Chile on Paris improvements and Johnson posted positive EBITDA wwww.cencosud.com Analysis by Business and Country ........................................... 13 Capex ...................................................................................... 21 Contents Financial Highlights 2Q13 .......................................................... 2 Balance Sheet Summary ......................................................... 22 Cencosud Key Events for 2Q13 ................................................. 2 Debt Amortization Schedule (USD million) ............................. 22 Retail Market Commentary....................................................... 3 Indebtedness .......................................................................... 22 Financial Results ....................................................................... 5 Cash Flow Summary ................................................................ 24 Overview 2Q13 ......................................................................... 5 Forward Looking Statements ................................................. -

Costanera Center Relevant Accomplishments Growth

Santiago, Chile FINANCIAL PERFORMANCE COSTANERA CENTER RELEVANT ACCOMPLISHMENTS GROWTH 01Financial Performance Chile & Argentina FINANCIAL PERFORMANCE COSTANERA CENTER RELEVANT ACCOMPLISHMENTS GROWTH Chile repeats its positive performance 2016 Cencosud Shopping Chile Results by June 30th 2017 REVENUES* TENANT SALES VISITS OCCUPANCY (%) (CLP$ BN) (CLP$ BN) (MILLIONS) 98,0% 97,9% 72,4 62,4 62,5 1.337 64,4 1.246 H1 2016 H1 2017 H1 2016 H1 2017 H1 2016 H1 2017 H1 2016 H1 2017 +12,4% +7,3% +0,1% -0,1 % *Excludes Related Party Rental Revenue FINANCIAL PERFORMANCE COSTANERA CENTER RELEVANT ACCOMPLISHMENTS GROWTH ECONOMIC DOWNTURN IN ARGENTINA Impact in purchasing power and visits to Shopping Centers 2016 Cencosud Shopping Argentina Results by June 30th 2017 REVENUES* TENANT SALES VISITS OCCUPANCY (ARS$ M) (ARS$ BN) (MILLIONS) (%) 97,4% 28,2 28,0 96,0% 817,1 18,6 689,9 15,6 H1 2016 H1 2017 H1 2016 H1 2017 H1 2016 H1 2017 H1 2016 H1 2017 +18,4% +19,0% -0,7% -1,4 % *Excludes Related Party Rental Revenue FINANCIAL PERFORMANCE COSTANERA CENTER RELEVANT ACCOMPLISHMENTS GROWTH 02Costanera Center Latin America’s Shopping Center FINANCIAL PERFORMANCE COSTANERA CENTER RELEVANT ACCOMPLISHMENTS GROWTH COSTANERA CENTER HAS BECOME Latin America´s most relevant Shopping Center Key destination for Shopping tourism in Chile: Cataloged as Latin America’s Miami by international press. Over 3.2 million visits monthly (5% increase against 2016). Tenant sales +15% during 2017; Rental Revenue +21%. Release of new leasable areas. FINANCIAL PERFORMANCE COSTANERA CENTER RELEVANT ACCOMPLISHMENTS GROWTH CITY’S MAIN ATTRACTION CERTIFICADO de Sky Costanera, an EXCELENCIA experience on the heights Highest viewpoint in Latin America, at 300 mts height Santiago’s number 1 tourist attraction, rated by Tripadvisor and the National Council of Tourism Over 500.000 annual visits. -

Nombre Fantasia STA ISABEL PROV BILBAO STA ISABEL VITACURA

Nombre Fantasia STA ISABEL PROV BILBAO STA ISABEL VITACURA STA ISABEL CV.QUILPUE SANTA ISABEL LA REINA STA ISABEL G.AVENIDA EXP LIDER ESTORIL STA ISABEL VINA DEL MAR MONTSERRAT (MATRIZ) MONTSERRAT QTA.NORMAL MONTSERRAT LA FLORIDA MONTSERRAT IRARRAZAVAL STA ISABEL ARLEGUI STA ISABEL V ALEMANA STA ISABEL EL BELLOTO STA ISABEL LC QUILPUE STA ISABEL URUGUAY 350 STA ISABEL PQUILLOTA. MONTSERRAT MONJITAS MONTSERRAT INDEPENDENCI MONTSERRAT CORDILLERA STA ISABEL LA CALERA P SANTA ISABEL RENCA HIP LIDER VINA DEL MAR EXP LIDER MAIPU HIP LIDER LA FRONTERA EXP LIDER QUILPUE EXP LIDER NORTE GRANDE HIP LIDER MACUL EXP LIDER GRECIA HIP LIDER V. MACKENNA EXP LIDER GRAN AVENIDA EXP LIDER PLAZA EGANA EXP LIDER LATADIA EXP LIDER PLAZA ITALIA EXP LIDER APOQUINDO EXP LIDER TOBALABA HIP LIDER BUENAVENTURA EXP LIDER NORTE GRANDE2 MONTSERRAT GRECIA HIP LIDER VESPUCIO SUR STA ISABEL COQUIMBO SANTA ISABEL CONCHALI STA ISABEL TEMUCO NERUD SANTA ISABEL RENACA STA ISABEL LA CALERA Z EXP LIDER COLON STA ISABEL VILLAN VINA HIP LIDER NUNOA EXP LIDER LA DEHESA STA ISABEL P.M.VALPO STA ISABEL TEMUCO BULNE MONTSERRAT A.SILVA C. EXP LIDER TOMAS MORO HIP LIDER ALAMEDA HIP LIDER PUENTE ALTO MONTSERRAT RENCA HIP LIDER MAIPU STA ISABEL 1 PON.VINA STA ISABEL CHILLAN ROBL STA ISABEL SN FELIPE 1 SANTA ISABEL LOS ANDES SANTA ISABEL PROVIDENCIA HIP LIDER DEPARTAMENTAL STA ISABEL MACUL PENALO SANTA ISABEL MELIPILLA STA ISABEL V.MCKNA HIP LIDER INDEPENDENCIA EXP LIDER MANUEL MONTT MONTSERRAT PAJARITOS SANTA ISABEL QTA NORMAL SANTA ISABEL PEDRO A CERD HIP LIDER IQUIQUE EXP LIDER KENNEDY SANTA ISABEL PTE ALTO STA ISABEL PZA TREBOL HIP LIDER TALCA SANTA ISABEL MANQUEHUE STA ISABEL CONC P. -

DIRECTORY March 18–21, 2013 Espacio Riesco Convention Center Santiago, Chile

March 18–21, 2013 Espacio Riesco Convention Center Santiago, Chile DIRECTORY March 18–21, 2013 Espacio Riesco Convention Center Santiago, Chile The Globalization of Latin American Retail ICSC’s RECon Latin America is the most important retail real estate event of the year in the region. This event offers an in-depth look at what’s happening in the industry in Latin America. A can’t miss opportunity to interface directly with key decision-makers and learn from them. The Conference includes educational sessions about the issues and trends affecting the industry in the region and globally. Topics will be varied and will address the challenges, trends and opportunities the industry is facing in this thriving region. Keynote speakers will mix with panel sessions in the most educational event in Latin America. (Simultaneous translation into Spanish/ English will be provided.) RECon Latin America’s Deal Making and Trade Exposition provide the per- fect venue for exhibitors to increase their visibility and meet with industry leaders in the region. The Deal Making and Trade Exposition will include 31 exhibitors providing the opportunity for owners, developers, brokers, financial institutions and retailers to come together to conduct business. The Trade Exposition is a one stop shopping area devoted to the industry’s latest and most innovative products and services. RECon Latin America will also feature the presentation of the 2013 Latin American Shopping Center Awards, Next Generation Program & Reception, Certification Breakfast Mixer, Gala Dinner, tour of Santiago's innovative shopping centers and plenty of networking opportunities. “RECon Latin America is the most relevant event to meet retail industry deal makers and thought-leaders across the diverse region which is Latin America.” Jordan C. -

ANNUAL REPORT Worldreginfo - F6e3cf56-D7ff-474F-B24c-Dfcd0d833522 Annual Report 2013 2

ANNUAL REPORT WorldReginfo - f6e3cf56-d7ff-474f-b24c-dfcd0d833522 Annual Report 2013 2 CONTENTS CHAIRMAN´S LETTER HOW WE DO IT AWARDS 2013 01 Chairman´s Letter / 03 04 Our Strenghts / 55 07 Cencosud Awards / 150 Retail Industry / 58 Jumbo Awards / 152 Our Team / 68 Organizational Structure / 74 CORPORATE GOVERNANCE Risk Factors / 75 08 Directors / 155 Legal Frameworks / 117 Board of Directors Compensation / 165 CENCOSUD AT A GLANCE Trademarks and Patents / 124 Management / 167 02 Our Mission / 07 Contracts and Licences / 125 Compenssation of the senior Our Milestones 2013 / 08 Suppliers and Customers / 126 management / 173 Material Events 2013 / 09 Executive stock option plans / 174 Operational Highlights / 12 CSR 05 Chile / 129 Argentina / 136 INFORMATION TO SHAREHOLDERS Colombia / 142 09 Property and Shares / 176 Ownerships Structure / 177 WHAT WE DO Stock Exchange Transactions / 180 03 Our History / 24 PRIVATE LABELS Our Dividends / 182 Our Ambition / 26 06 Private Labels / 146 Main Properties / 183 Our Business / 27 Unproductive Land / 192 2014 Investment Plan / 53 Allies and subsidiaries / 193 Corporate Structure / 223 Statement of responsability / 224 Additional Information / 227 WorldReginfo - f6e3cf56-d7ff-474f-b24c-dfcd0d833522 Annual Report 2013 3 CHAIRMAN´S letter It is with great pride that I present our Annual Report and Fi- since its inception 50 years ago. nancial Statements for the year ended on December 31st, 2013, a period in which we celebrated our fiftieth year since the opening of During 2013 our major focus has been the consolidation of ope- our first store “Las Brisas” in the city of Temuco, Chile. The jour- rations following our recent and aggressive expansion these last few ney over these last five decades has been exciting, characterized years. -

Directorio on Tour Ene 20

DIRECTORIO DE TIENDAS EXCLUSIVELY FOR TOURISTS Guia de descontos · Exclusivo turistas Guía de descuentos · Exclusivo para turistas HORARIOS DE ATENCIÓN Centre Trading Hours SHOPPING CENTER Shopping Center Lun a dom: 10:30 - 21:00 hrs. PATIO DE COMIDAS Food Court Lun a dom: 11:30 - 22:00 hrs. GRANDES TIENDAS Department Store Lun a dom: 10:30 - 20:30 hrs. RESTAURANTES SABORES Gourmet Restaurant Lun a dom: 11:00 - 00:00 hrs. SERVICIOS Services SERVICIO DE TAXI OFICIAL OFFICIAL TAXI SERVICE EN EL NIVEL -1 DE ESTACIONAMIENTO ON LEVEL -1 PARKING ASCENSORES ANDRÉS BELLO // ASCENSORES VITACURA ELEVATORS ANDRÉS BELLO // ELEVATORS VITACURA UBICACIÓN CASA CHANGE HOUSE DE CAMBIO LOCATION AMBAS EN PLANTA BAJA BOTH ON GROUND FLOOR CAMEX local 103 // AFEX LOCAL 212 // AFEX módulo 6036 CAMEX shop 103 // AFEX shop 212 // AFEX module 6036 WIFI GRATIS FREE WIFI CONEXIÓN SIN CLAVE CONNECTION WITHOUT CONÉCTATE A LA RED: mimallcencosud PASSWORD CONNECT TO THE NETWORK: mimallcencosud SERVICIOS Services SALA DE LACTANCIA Nivel 2, costado Banana Republic Breast Feeding Room: level 2, next to Banana Republic POLICLÍNICO Nivel 2, costado Sala de Lactancia First Aid: level 2, next to Lactation Room SERVICIO AL CLIENTE Nivel 1, acceso Vitacura. Customer Service: level 1, Vitacura access PRÉSTAMO DE COCHES Y SILLAS DE RUEDAS Nivel 1, módulo servicio al cliente. Stroller and Wheelchair Rentals: level 1 in front of customer services SERVICIO AL CLIENTE PARKING Nivel -1, ascensores Andrés Bello Parking Customer Service: level -1, tower 1 BAÑO NIÑOS Y MUDADOR Niveles PB, 2, 3, 4 y 5. Children Restrooms and Diaper Changing Station: levels ground floor, 2, 3, 4 and 5 CAJEROS AUTOMÁTICOS Todos los niveles.