Годовой Отчет Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Committee of Ministers Secretariat Du Comite Des Ministres

SECRETARIAT GENERAL SECRETARIAT OF THE COMMITTEE OF MINISTERS SECRETARIAT DU COMITE DES MINISTRES Contact: Clare Ovey Tel: 03 88 41 36 45 Date: 06/06/2017 DH-DD(2017)611 Documents distributed at the request of a Representative shall be under the sole responsibility of the said Representative, without prejudice to the legal or political position of the Committee of Ministers. Meeting: 1288th meeting (June 2017) (DH) Communication from the applicant’s representatives (01/06/2017) in the case of JEHOVAH'S WITNESSES OF MOSCOW AND OTHERS v. Russian Federation (Application No. 302/02) Information made available under Rule 9.1 of the Rules of the Committee of Ministers for the supervision of the execution of judgments and of the terms of friendly settlements. * * * * * * * * * * * Les documents distribués à la demande d’un/e Représentant/e le sont sous la seule responsabilité dudit/de ladite Représentant/e, sans préjuger de la position juridique ou politique du Comité des Ministres. Réunion : 1288e réunion (juin 2017) (DH) Communication des représentants du requérant (01/06/2017) dans l’affaire JEHOVAH'S WITNESSES OF MOSCOW ET AUTRES c. Fédération de Russie (Requête n° 302/02) [anglais uniquement] Informations mises à disposition en vertu de la Règle 9.1 des Règles du Comité des Ministres pour la surveillance de l’exécution des arrêts et des termes des règlements amiables. PO Box 40 13893 Highway 7 (courier) Georgetown ON L7G 4T1 905-873-4545 905-873-4522 John M. Burns, LL.B. DGI [email protected] Also of the Bar of British Columbia 01 JUIN 2017 SERVICE DE L’EXECUTION DES ARRETS DE LA CEDH 30 May 2017 Department for the Execution of Judgments of the ECHR DGI - Directorate General of Human Rights and Rule of Law Council of Europe F-67075 STRASBOURG CEDEX FRANCE Re: Application no. -

Russian M&A Review 2017

Russian M&A review 2017 March 2018 KPMG in Russia and the CIS kpmg.ru 2 Russian M&A review 2017 Contents page 3 page 6 page 10 page 13 page 28 page 29 KEY M&A 2017 OUTLOOK DRIVERS OVERVIEW IN REVIEW FOR 2018 IN 2017 METHODOLOGY APPENDICES — Oil and gas — Macro trends and medium-term — Financing – forecasts sanctions-related implications — Appetite and capacity for M&A — Debt sales market — Cross-border M&A highlights — Sector highlights © 2018 KPMG. All rights reserved. Russian M&A review 2017 3 Overview Although deal activity increased by 13% in 2017, the value of Russian M&A Deal was 12% lower than the previous activity 13% year, at USD66.9 billion, mainly due to an absence of larger deals. This was in particular reflected in the oil and gas sector, which in 2016 was characterised by three large deals with a combined value exceeding USD28 billion. The good news is that investors have adjusted to the realities of sanctions and lower oil prices, and sought opportunities brought by both the economic recovery and governmental efforts to create a new industrial strategy. 2017 saw a significant rise in the number and value of deals outside the Deal more traditional extractive industries value 37% and utility sectors, which have historically driven Russian M&A. Oil and gas sector is excluded If the oil and gas sector is excluded, then the value of deals rose by 37%, from USD35.5 billion in 2016 to USD48.5 billion in 2017. USD48.5bln USD35.5bln 2016 2017 © 2018 KPMG. -

A N N U a L R E P O

ANNUAL2011 REPORT PIK Group Annual Report 2011 New Level of Development PIK Group at a glance Annual Report 2011 PIK Group 3 PIK Group at a glance RESPONSIBILITY STATEMENT We are a leading residential real estate developer in Russia, with OUR CORE ACTIVITIES ARE: BUSINESS HIGHLIGHTS a particular strategic focus on the Moscow Metropolitan Area. The development of residential Each of the Directors confirms that, to the best of his or real estate properties and sales A LEADING MASS MARKET RESIDENTIAL her knowledge: Our principal activity is the development, construction and sale of completed units. DEVELOPER IN RUSSIA WITH 17 YEAR (a) the financial statements, prepared in accordance of mass-market residential properties in the Russian real estate market. TRACK RECORD 1 with International Financial Reporting Standards and The construction of reinforced concrete panel housing, the requirements of Cypriot Companies Law, Cap. FINANCIAL FIGURES 113, in each case included in this Annual Report, give production and assembly of a true and fair view of the assets, liabilities, financial prefabricated panel residential position and profit and losses of the Company and buildings, including construction Around 10.5% market share1 in Moscow Metropolitan Area the undertakings included in the consolidation taken at our development sites and (MMA)2 in 2011 as a whole; and 46.0 bn RUR 9.4 bn RUR 11.7 bn RUR construction services provided Over 12 mln sqm of net selling area (NSA) completed since (b) the Management Report included in this Annual Revenue -

Bank of Russia

12 Neglinnaya Street, Moscow, 107016 Russia 8 800 300-30-00 www.cbr.ru News List of credit institutions with appointed authorised representatives of the Bank of Russia 10 December 2020 Press release As of 1 December 2020, authorised representatives of the Bank of Russia, acting in compliance with Article 76 of Federal Law No. 86-FZ, dated 10 July 2002, ‘On the Central Bank of the Russian Federation (Bank of Russia)’ were appointed to 112 credit institutions. No. List of credit institutions with appointed authorised representatives of the Bank of Russia Reg. No. Central Federal District Moscow and the Moscow Region 1. AO UniCredit Bank 1 2. BCS Bank AO 101 3. CentroCredit Bank 121 4. JSC RN Bank 170 5. HCF Bank 316 6. Bank GPB (JSC) 354 7. Bank IPB (JSC) 600 8. JSC Post Bank 650 9. PJSC Moscow Industrial bank 912 10. VTB Bank (PJSC) 1000 11. PJSC Plus Bank 1189 12. AO ALFA-BANK 1326 13. Vozrozhdenie Bank 1439 14. Sberbank 1481 15. Timer Bank (JSC) 1581 16. SDM-Bank PJSC 1637 17. PJSC MOSOBLBANK 1751 18. Inbank, Ltd 1829 19. FORA-BANK 1885 20. Joint stock Company commercial bank Lanta-Bank 1920 21. CREDIT BANK OF MOSCOW 1978 22. Peresvet Bank (PJSC) 2110 23. Cetelem Bank Llc 2168 24. Bank Otkritie Financial Corporation (Public Joint-Stock Company) 2209 25. TRANSKAPITALBANK 2210 26. Banca Intesa 2216 27. QIWI Bank (JSC) 2241 28. PJSC MTS Bank 2268 29. PJSC ROSBANK 2272 30. PJSC BANK URALSIB 2275 31. JSC Russian Standard Bank 2289 32. Absolut Bank (PAO) 2306 33. -

IMPORTANT NOTICE IMPORTANT: You Must Read the Following Before Continuing

IMPORTANT NOTICE IMPORTANT: You must read the following before continuing. The following applies to the document following this page, and you are therefore advised to read this carefully before reading, accessing or making any other use of the attached document. In accessing the attached document you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from us as a result of such access. NOTHING IN THE FOLLOWING DOCUMENT CONSTITUTES AN OFFER OF SECURITIES FOR SALE IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. ANY SECURITIES TO BE ISSUED WILL NOT BE REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE “SECURITIES ACT”), OR THE SECURITIES LAWS OF ANY STATE OF THE UNITED STATES OR OTHER JURISDICTION, AND THE SECURITIES MAY NOT BE OFFERED OR SOLD WITHIN THE UNITED STATES OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS (AS DEFINED IN REGULATION S UNDER THE SECURITIES ACT), EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIES LAWS. THE FOLLOWING DOCUMENT MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER, AND IN PARTICULAR, MAY NOT BE FORWARDED TO ANY U.S. PERSON OR TO ANY U.S. ADDRESS. ANY FORWARDING, DISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER JURISDICTIONS. -

An Overview of Russian Ipos

www.pwc.ru/capital-markets An overview of Russian IPOs: 2005 to 2014 Listing centres, investment banks, legal counsels, auditors and issuers’ jurisdictions IPOs by listing centre (2005 – September 2014) IPOs on LSE by markets Number of IPOs Total (2005 – September 2014*) Listing centre Sept 2005 2006 2007 2008 2009 2010 2011 2012 2013 No. % 2014 Main Market (Premium) London Stock Exchange (LSE) 11 19 15 3 2 3 7 5 1 1 67 57 2 Moscow Exchange 3 7 14 3 1 7 - - 2 - 37 32 Alternative NASDAQ (US) - 1 - - - - 1 1 1 - 4 3 Investment 17 Deutsche Börse - 1 1 - - - 1 - - - 3 2 Market (AIM) NASDAQ OMX (Europe) - - 2 - - - - - - - 2 2 Hong Kong Stock Exchange (HKEX) - - - - - 2 - - - - 2 2 NYSE - - - - - - - 1 1 - 2 2 Number of IPOs* 14 28 32 6 3 12 9 7 5 1 117 100 * The overview contains a selection of Russian IPOs and may not be a full list of deals for the period. Issuers with IPOs on LSE subsequently moved to premium listing 48 Main Market (GDRs**) Issuer Original market / year Premium listing year Polyus Gold Main Market (GDRs) / 2006 2012 *Of the total 67 IPOs on LSE Polymetal International Main Market (GDRs) / 2007 2011 **Global Depositary Receipts EVRAZ Main Market (GDRs) / 2005 2011 AFI Development Main Market (GDRs) / 2007 2010 Raven Russia AIM / 2005 2010 IPOs by industry and listing centre (2005 – September 2014) 15 14 14 LSE Moscow Exchange NASDAQ (US) NASDAQ OMX (Europe) Deutsche Borse HKEX NYSE 2 1 2 1 11 4 10 10 4 2 2 1 8 1 3 6 6 12 2 7 1 5 Number of IPOs 9 4 4 4 8 8 5 1 3 3 1 5 5 5 5 1 1 4 2 3 3 1 2 1 1 1 Metals & Mining Financial -

HEDGE EFFECTIVENESS of the RTS INDEX FUTURES Anastasia Musorgina a Thesis Submitted to the University of North Carolina in Part

HEDGE EFFECTIVENESS OF THE RTS INDEX FUTURES Anastasia Musorgina A Thesis Submitted to the University of North Carolina in Partial Fulfillment of the Requirements for the Degree of Master of Business Administration Cameron School of Business University of North Carolina Wilmington 2011 Approved by Advisory Committee Nivine Richie Rob Burrus Cetin Ciner Chair Accepted by _____________________________ Dean, Graduate School TABLE OF CONTENTS ABSTRACT ............................................................................................................................. iii DEDICATION .......................................................................................................................... iv ACKNOWLEDGEMENTS ....................................................................................................... v LIST OF TABLES .................................................................................................................... vi LIST OF FIGURES ................................................................................................................. vii INTRODUCTION ..................................................................................................................... 1 Hedging .................................................................................................................................. 1 Russian Derivatives Market ................................................................................................... 2 Moscow Interbank Currency Exchange ................................................................................ -

Russia & Cis' Largest Virtual Capital Markets Event

REGISTER YOUR PLACE TODAY AT WWW.BONDSLOANSRUSSIA.COM RUSSIA & CIS’ LARGEST VIRTUAL CAPITAL MARKETS EVENT 500+ 40+ 250+ 100+ 2,100+ SENIOR WORLD CLASS SOVEREIGN, CORPORATE INVESTORS CONTACTS AVAILABLE TO ATTENDEES SPEAKERS & FI BORROWERS NETWORK WITH ONLINE It’s great to have Bonds & Loans with us in all times - good and bad. Our team has particularly enjoyed the networking opportunities, the program is excellent too, and you’ve proved once again your reputation of the leading capital markets event in Russia. Dmitri Surkov, Global Head of Revenue Management, Fitch Ratings Gold Sponsor: Silver Sponsors: Bronze Sponsors: Corporate Sponsors: www.BondsLoansRussia.com BRINGING GLOBAL FINANCE LEADERS TOGETHER WITH THE RUSSIA & CIS CAPITAL MARKETS COMMUNITY Meet senior decision-makers from Russia & the CIS sovereigns, corporates and banks; share knowledge; debate; network; and move your business forward in the current economic climate without having to travel. 500+ 40+ 250+ SENIOR WORLD CLASS SOVEREIGN, CORPORATE 100+ ATTENDEES SPEAKERS & FI BORROWERS INVESTORS Access top market practitioners from Industry leading speakers will share Hear first-hand how local and international Leverage our concierge across the globe who are active in “on-the-ground” market intelligence industry leaders are navigating Russia & the meeting service the Russia & CIS markets, including: and updates on Russia & the CIS’s CIS’s current economic climate/what they to engage with global senior borrowers, investors, bankers & economic backdrop. Gain actionable expect in -

Industrial Framework of Russia. the 250 Largest Industrial Centers Of

INDUSTRIAL FRAMEWORK OF RUSSIA 250 LARGEST INDUSTRIAL CENTERS OF RUSSIA Metodology of the Ranking. Data collection INDUSTRIAL FRAMEWORK OF RUSSIA The ranking is based on the municipal statistics published by the Federal State Statistics Service on the official website1. Basic indicator is Shipment of The 250 Largest Industrial Centers of own production goods, works performed and services rendered related to mining and manufacturing in 2010. The revenue in electricity, gas and water Russia production and supply was taken into account only regarding major power plants which belong to major generation companies of the wholesale electricity market. Therefore, the financial results of urban utilities and other About the Ranking public services are not taken into account in the industrial ranking. The aim of the ranking is to observe the most significant industrial centers in Spatial analysis regarding the allocation of business (productive) assets of the Russia which play the major role in the national economy and create the leading Russian and multinational companies2 was performed. Integrated basis for national welfare. Spatial allocation, sectorial and corporate rankings and company reports was analyzed. That is why with the help of the structure of the 250 Largest Industrial Centers determine “growing points” ranking one could follow relationship between welfare of a city and activities and “depression areas” on the map of Russia. The ranking allows evaluation of large enterprises. Regarding financial results of basic enterprises some of the role of primary production sector at the local level, comparison of the statistical data was adjusted, for example in case an enterprise is related to a importance of large enterprises and medium business in the structure of city but it is located outside of the city border. -

Russian Ecm November 6, 2006

1 Russian ecm November 6, 2006 1. Investment banks index wars 2. 35 companies will raise $19bn in 2007, Deutsche Bank 3. RTS to launch a Russian NASDAQ 4. Market players to be licensed 5. Gazprombank finally to sell off media, petrochemical assets in IPO 6. Owner of the Chelyabinsk zinc plant (CZP) will sell 3% of their shares 7. Chemical firm share price collapses after dilutive share issue 8. Dymov Sausage to IPO 9. Eastern Property Holdigns increases capital by $125m 10. Far Eastern Sea Shipping Company will IPO 11. Mosenergo places in favour of Gazprom 12. OGK-5 sale a big success 13. Pharmaceutical producer to IPO 14. Pipemaker TMK IPOs 15. Russian commodity exchange plans to launch wheat futures 16. Severstal sets IPO price 17. Sistema-Hals IPO price range set 18. Uralkaliy decreases 9-month dividends by a third following flood 19. Uranium company to IPO 20. WBD owners sell small stake Investment banks index wars Monday, November 6, 2006 A veritable war of indexes is breaking out as Two of Russia's top investment banks launched new indexes, better to track Russia's increasingly sophisticated growth, that will compete with the proliferating number of indexes tracking Russia. Renaissance Capital has teamed up with emerging market gurus Morgan Stanley that puts together the widely quoted MSCI index - a benchmark for emerging market stock market preformace - to produce the MSCI http://businessneweurope.eu 2 Renaissance Index of TOP Liquid Russian Stocks (the MSCI Rencap Index, for short). Likewise, Troika Dialog launched a third tier index that tracks 50 companies that are on the up and up but currently fall below all the investment bank's radar screens. -

US Sanctions on Russia

U.S. Sanctions on Russia Updated January 17, 2020 Congressional Research Service https://crsreports.congress.gov R45415 SUMMARY R45415 U.S. Sanctions on Russia January 17, 2020 Sanctions are a central element of U.S. policy to counter and deter malign Russian behavior. The United States has imposed sanctions on Russia mainly in response to Russia’s 2014 invasion of Cory Welt, Coordinator Ukraine, to reverse and deter further Russian aggression in Ukraine, and to deter Russian Specialist in European aggression against other countries. The United States also has imposed sanctions on Russia in Affairs response to (and to deter) election interference and other malicious cyber-enabled activities, human rights abuses, the use of a chemical weapon, weapons proliferation, illicit trade with North Korea, and support to Syria and Venezuela. Most Members of Congress support a robust Kristin Archick Specialist in European use of sanctions amid concerns about Russia’s international behavior and geostrategic intentions. Affairs Sanctions related to Russia’s invasion of Ukraine are based mainly on four executive orders (EOs) that President Obama issued in 2014. That year, Congress also passed and President Rebecca M. Nelson Obama signed into law two acts establishing sanctions in response to Russia’s invasion of Specialist in International Ukraine: the Support for the Sovereignty, Integrity, Democracy, and Economic Stability of Trade and Finance Ukraine Act of 2014 (SSIDES; P.L. 113-95/H.R. 4152) and the Ukraine Freedom Support Act of 2014 (UFSA; P.L. 113-272/H.R. 5859). Dianne E. Rennack Specialist in Foreign Policy In 2017, Congress passed and President Trump signed into law the Countering Russian Influence Legislation in Europe and Eurasia Act of 2017 (CRIEEA; P.L. -

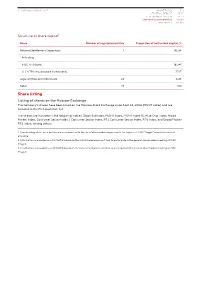

Share Listing

Annual Report 2018 | MAGNIT MAGNIT TODAY 3-11 99 STRATEGIC REPORT 13-27 PERFORMANCE REVIEW 29-53 CORPORATE GOVERNANCE 55-113 APPENDICES 115-189 Structure of share capital1 Name Number of registered entities Proportion of authorized capital, % National Settlement Depositary 1 95.54 Including: PJSC VTB Bank 18.342 LLC VTB Infrastructure Investments 7.723 Legal entities and individuals 24 4.46 Total: 25 100 Share listing Listing of shares on the Moscow Exchange The Company’s shares have been listed on the Moscow Stock Exchange since April 24, 2006 (MGNT ticker) and are included in the first quotation list. The shares are included in the following indices: Stock Subindex, MOEX Index, MOEX Index 10, Blue Chip Index, Broad Market Index, Consumer Sector Index / Consumer Sector Index, RTS Consumer Sector Index, RTS Index, and Broad Market RTS Index, among others. 1. Shareholding structure is provided in accordance with the list of shareholders registered in the register of PJSC “Magnit” shareholders as of 31.12.2018 2. Information is provided as of 12.11.2018 based on the list of shareholders entitled to participate in the general shareholders meeting of PJSC “Magnit 3. Information is provided as of 12.11.2018 based on the list of shareholders entitled to participate in the general shareholders meeting of PJSC “Magnit 100 101 Weight of shares in indices Ticker Index name Weight in index, % RDXUSD Russian Depositary Index USD 2.85 RDX Russian Depositary Index EUR 2.85 NU137529 MSCI EM IMI (VRS Taxes) Net Return USD Index 0.09 RIOB FTSE Russia IOB