The Legal Ethics of Drafting Legal Opinions

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Confidentiality in Mediation: a Moral Reassessment

Journal of Dispute Resolution Volume 1992 Issue 1 Article 5 1992 Confidentiality in Mediation: A Moral Reassessment Kevin Gibson Follow this and additional works at: https://scholarship.law.missouri.edu/jdr Part of the Dispute Resolution and Arbitration Commons Recommended Citation Kevin Gibson, Confidentiality in Mediation: A Moral Reassessment, 1992 J. Disp. Resol. (1992) Available at: https://scholarship.law.missouri.edu/jdr/vol1992/iss1/5 This Article is brought to you for free and open access by the Law Journals at University of Missouri School of Law Scholarship Repository. It has been accepted for inclusion in Journal of Dispute Resolution by an authorized editor of University of Missouri School of Law Scholarship Repository. For more information, please contact [email protected]. Gibson: Gibson: Confidentiality in Mediation: A Moral Reassessment CONFIDENTIALITY IN MEDIATION: A MORAL REASSESSMENT Kevin Gibson* To whom you tell your secrets, to him you resign your liberty. Spanish Proverb I find the issue of confidentiality fascinating. When the Ethics Committee discussed confidentiality, we each had slightly different meanings. Labor mediators were most insistent on talking of confidentiality in absolute terms, but most flexible when it came to defining it. In the community field, confidentiality has so many facets. We have to break them down in our training sessions. The [Society of Professionalsin Dispute Resolution] standards address confidentiality as if we are all taking about the same thing when I think there are overt and subtle variations which need to be explored.' Albie Davis I. INTRODUCTION In maintaining client confidentiality, mediators may find a conflict between common morality and their role morality. -

Published Ethics Advisory Opinions (Guide, Vol. 2B, Ch

Guide to Judiciary Policy Vol. 2: Ethics and Judicial Conduct Pt. B: Ethics Advisory Opinions Ch. 2: Published Advisory Opinions § 210 Index § 220 Committee on Codes of Conduct Advisory Opinions No. 2: Service on Governing Boards of Nonprofit Organizations No. 3: Participation in a Seminar of General Character No. 7: Service as Faculty Member of the National College of State Trial Judges No. 9: Testifying as a Character Witness No. 11: Disqualification Where Long-Time Friend or Friend’s Law Firm Is Counsel No. 17: Acceptance of Hospitality and Travel Expense Reimbursements From Lawyers No. 19: Membership in a Political Club No. 20: Disqualification Based on Stockholdings by Household Family Member No. 24: Financial Settlement and Disqualification on Resignation From Law Firm No. 26: Disqualification Based on Holding Insurance Policy from Company that is a Party No. 27: Disqualification Based on Spouse’s Interest as Beneficiary of a Trust from which Defendant Leases Property No. 28: Service as Officer or Trustee of Hospital or Hospital Association No. 29: Service as President or Director of a Corporation Operating a Cooperative Apartment or Condominium No. 32: Limited Solicitation of Funds for the Boy Scouts of America No. 33: Service as a Co-trustee of a Pension Trust No. 34: Service as Officer or on Governing Board of Bar Association No. 35: Solicitation of Funds for Nonprofit Organizations, Including Listing of Judges on Solicitation Materials No. 36: Commenting on Legal Issues Arising before the Governing Board of a Private College or University No. 37: Service as Officer or Trustee of a Professional Organization Receiving Governmental or Private Grants or Operating Funds No. -

The Issuance of a Third-Party Legal Opinion

In My Opinion... Ethical Considerations of Third-Party Legal Opinions by Lydia C. Stefanowicz he issuance of a third-party legal opinion First, the client should consent to the issuance of as a condition to closing has become such a the legal opinion. That consent may be express, as, for T common practice in certain types of business example, pursuant to an engagement letter, or implied. transactions, most notably financing transactions, that NJRPC Rule 1.2(a) states that a lawyer may take such lawyers rarely stop to consider the ethical considerations action on behalf of the client as is impliedly authorized related to this practice. The third-party legal opinion is to carry out the representation. Thus, when a client an expression of a lawyer’s professional judgment on executes a financing commitment letter or an agreement the matters covered therein relating to his or her client that requires the delivery of a third-party legal opin- and the subject transaction, as of the date of the opinion ion as a condition of closing, the client has implicitly letter, for the benefit of the opinion recipient. Since the consented to the issuance of the third-party legal opin- opinion recipient is not the lawyer’s client, such an ion on its behalf by its counsel in that transaction. opinion letter is commonly known as a ‘third-party legal However, when a lawyer is engaged to act as local opinion.’ In an adversarial legal system such as ours, a counsel in a transaction primarily for the purpose of situation where an attorney has, among other duties, a issuing a legal opinion in its jurisdiction, the lawyer- duty of loyalty and care to his or her client, as well as client relationship may be remote. -

Legal Opinions: Sample Opinion Letter No. 3: Commercial

LEGAL OPINIONS: SAMPLE OPINION LETTER NO. 3: GOMMERGIAL The $olicitors' Legal Opinions Gommittee was constituted for the purpose of reviewing materials previously published with respect to solicitors' opinions and preparing guides for the assistance of the profession, The menbers of our Gommittee at this time are: Sandra D. Sutherland, Q.G. (Ghair) Nicolaas Blom of McGarthy Tetrault LLP Paul D, Bradley of Lawson Lundell Hamish G. Gameron, Q,G. of Bull, Housser & Tupper Mitchell H. Gropper, Q.G. of Farris Vaughan Wills & Murphy Donald J. Haslam of Kornfeld Mackoff Silber Jacqueline Kelly of Davis & Gompany John O.E. Lundell of Lawson Lundell Mitchell McGormick of Fasken Martineau DuMoulin LLP lain Mant of Gampney & Murphy John Morrison of Lang Michener Lawrence & Shaw Robert Shouldice of Borden Ladner Gervais LLP Anne M. $tewart, Q,G. of Blake, Gassels & Graydon LLP David A. Zacks of Fraser Milner LLP Earlier Statements Our Gommittee has issued five earlier Statements concerning legal opinions, Those $tatements are listed under ltenr 'l under the heading "Reference Materials" included at the end of this Statement. Our Gommiftee has reviewed the five earlier Statementsn and confirms the principles set out therein. Our Gommittee continues to concur with the general practice that opinions from solicitorc for borrowers as to the validity, legality, binding effect or enforceability of standard form security documents are neither requested nor given except in unusual circumstances. This matter is set out in more detail, along with some examples -

Legal Opinion

[Translation] LEGAL OPINION given by Claude Rouiller Doctor of Laws and Attorney-at-Law Judge of the Administrative Tribunal of the International Labour Organization (ILOAT/TAOIT) President of the Board of Arbitration of the Swiss Exchange (SWx) Former President of the Swiss Federal Tribunal Associate Professor, University of Neuchâtel October 25, 2005 2 TABLE OF CONTENTS I. THE EXPERT 4 II. THE FRAMEWORK OF THE MANDATE 4 1. The mandate 4 2. The documents provided 6 3. Customary disclaimer 6 III. THE OVERALL LEGAL CONTEXT OF THE CONSULTATION 7 1. Preamble 7 2. The European Convention of November 16, 1989 7 3. The World Anti-Doping Agency and the World Anti-Doping Code 9 (a) The World Anti-Doping Agency 9 (b) The World Anti-Doping Code 11 4. The UNESCO Convention of October 19, 2005 14 (a) The adoption of the Convention and its preamble 14 (b) The Convention and the World Anti-Doping Code 14 IV. DISCUSSION 15 1. Preamble 15 (a) The rules under discussion 15 (b) The status quaestionis 16 2. The interpretation of Article 10.2 of the Code and the legal nature of the sanctions it provides for 17 (a) The interpretation of Article 10.2 of the Code 17 (b) The legal nature of the sanctions provided for 20 3. The content of the fundamental rights and general principles of autonomous Swiss law that could be applied by arbitrators reviewing the application of Article 10.2 of the Code and that could come into play in the context of a limited review by the Federal Tribunal 25 (a) Introductory note 25 (b) Personal liberty 26 3 (c) Economic liberty 28 (d) Brief outline of fundamental rights practice 29 (e) The relative practical similarities between the modalities of application of Article 36 Cst. -

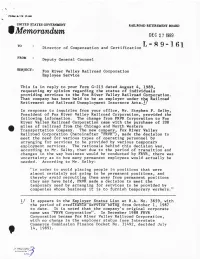

V.Memorandum OEC271989

F O R M 0-111 |7-ee> UNITED STATES GOVERNMENT RAILROAD RETIREMENT BOARD V .Memorandum OEC27 1989 TO Director of Compensation and Certification L " 8 9-161 FROM Deputy General Counsel SUBJECT: Fox River Valley Railroad Corporation Employee Service This is in reply to your Form G-215 dated August 4, 1989, requesting my opinion regarding the status of individuals providing services to the Fox River Valley Railroad Corporation. That company has been held to be an employer under the Railroad Retirement and Railroad Unemployment Insurance Acts.± 7 In response to inquiries from your office, Mr. Stephen P. Selby, President of Fox River Valley Railroad Corporation, provided the following information. The change from FRVR Corporation to Fox River Valley Railroad Corporation came with the purchase of 208 miles of railroad from the Chicago and North Western Transportation Company. The new company, Fox River Valley Railroad Corporation (hereinafter "FRVR '), made the decision to meet the need for various types of operating personnel by arranging for services to be provided by various temporary employment services. The rationale behind this decision was, according to Mr. Selby, that due to the period of transition and changes in the way business would be conducted by FRVR, there was uncertainty as to how many permanent employees would actually be needed. According to Mr. Selby: "in order to avoid placing people in positions that were almost certainly not going to be permanent positions, and thereby avoid recruiting them away from permanent positions they may have held, FRVR made a decision to meet the temporary need by arranging for services to be provided by companies whose business it is to furnish temporary workers." 1/ It appears in the Employer Status List at B .A. -

OPINIONSMATTERS of the UCC Opinions Report and Its Illustrative Opinion Editor’S Note Letter

Spring 2018 Volume 3 Number 1 OPINIONSThe Newsletter of the CommitteeMATTERS on Legal Opinions in Real Estate Transactions From the Chair Edward J. Levin, Editor-in-Chief On behalf of the Committee on Legal Opinions in Real Anthony D. Todero, Articles Editor Estate Transactions of the ABA Section of Real Property, Trust and Estate Law, it is my pleasure to present this issue of Opinions Matters, our Committee’s semiannual newslet- ter. The mission of the newsletter is to keep our members CONTENTS and other lawyers informed of developments in opinion practice, with a focus on real estate opinion practice. We From the Chair ..............................................1 monitor and report on actions and reports of various or- ganizations, such as the Legal Opinion Committee of the Editor’s Note .................................................2 ABA Business Law Section, the Working Group on Legal Opinions, and the TriBar Opinion Committee. A Primer: Legal Opinions in Loan Modifications, Assumptions, and Joinders..............................3 It is appropriate for this Spring issue that Opinions Mat- ters has a new set of editors. They have bravely agreed to Contract and Negligent Misrepresentation follow the tremendous work done for the initial four issues Claims Against Opinion Giver ...........................5 by Bill Dunn, Editor emeritus. I am privileged to introduce Ed Levin as the new Editor-in-Chief. Ed (an appropriate Risk Management for Legal Opinions: name in this context) has been an active leader and par- Limiting Who May Rely on Your Opinion Letters in ticipant in the RPTE Section for years, serving as Chair of HUD Multi-Family Housing Projects ..................6 our Committee and as Group Chair of the Real Estate Fi- nancing Group under which our Committee falls. -

Takeaways Fall 2015 P. 5

FALL 2015 LEGAL EMPLOYMENT INFORMATION YOU CAN APPLY TO YOUR BUSINESS NEW LAWS TARGET PREHIRE PROCESS, TAKEAWAYS provides highlights of the most significant New York, New Jersey ENHANCE WAGE LAW PROTECTIONS and Connecticut legal developments New York City Prohibits Criminal History from the past quarter, together with action items for your business. These Inquiries include new laws, court cases and New York City has now adopted its own version of a ban-the-box administrative decisions on wage law, the Fair Chance Act, which takes effective October 27, 2015. issues, discrimination protections, The new law is broader than most in that it will preclude employers limits on criminal history checks and from inquiring about criminal history of job applicants at any time prior to extending them a job offer....(see pg. 3) new federal agency pronouncements. Levy Employment Law, LLC helps Connecticut Enhances Wage Law Protections businesses identify and resolve workplace Two new Connecticut laws, one protecting employees’ inquiries into issues before they result in litigation. and discussions of their colleagues’ wages, and the other doubling the damages available for most violations of the state’s wage and We leverage HR best practices to mitigate hour laws, collectively expand employees’ rights and protections risk for employers by: with regard to wage law violations....(see pg. 3) designing and building Human Resources policies with supporting Jersey City Penalizes Employers for Wage systems, Nonpayment training HR staff, line managers and employees, Effective October 1, 2015, Jersey City employers found guilty, liable troubleshooting workplace or responsible for violating federal, state or local wage laws will face concerns, and nonissuance or nonrenewal of their license to do business in the city defending charges filed with the unless they provide proof that they have cured their wage law EEEOC and state and local violation(s) within 90 days of the final judicial or administrative administrative agencies. -

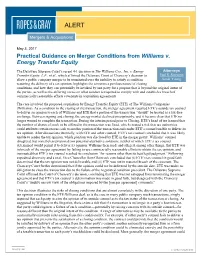

Practical Guidance on Merger Conditions from Williams V. Energy Transfer Equity

ALERT Mergers & Acquisitions May 3, 2017 Practical Guidance on Merger Conditions from Williams v. Energy Transfer Equity The Delaware Supreme Court’s recent 4-1 decision in The Williams Cos., Inc. v. Energy Attorneys Transfer Equity, L.P., et al., which affirmed the Delaware Court of Chancery’s decision to Paul S. Scrivano allow a public company merger to be terminated over the inability to satisfy a condition Sarah Young requiring the delivery of a tax opinion, highlights the sometimes perilous nature of closing conditions, and how they can potentially be invoked by one party for a purpose that is beyond the original intent of the parties, as well as the differing views on what conduct is required to comply with and establish a breach of commercially reasonable efforts covenants in acquisition agreements. The case involved the proposed acquisition by Energy Transfer Equity (ETE) of The Williams Companies (Williams). As a condition to the closing of the transaction, the merger agreement required ETE’s outside tax counsel to deliver an opinion to each of Williams and ETE that a portion of the transaction “should” be treated as a tax-free exchange. Between signing and closing, the energy market declined precipitously, and it became clear that ETE no longer wanted to complete the transaction. During the interim period prior to Closing, ETE’s head of tax learned that the number of shares of stock to be offered in the transaction was fixed, which created a risk that tax authorities could attribute certain excess cash to another portion of the transaction and render ETE’s counsel unable to deliver its tax opinion. -

Archived Content Contenu Archivé

ARCHIVED - Archiving Content ARCHIVÉE - Contenu archivé Archived Content Contenu archivé Information identified as archived is provided for L’information dont il est indiqué qu’elle est archivée reference, research or recordkeeping purposes. It est fournie à des fins de référence, de recherche is not subject to the Government of Canada Web ou de tenue de documents. Elle n’est pas Standards and has not been altered or updated assujettie aux normes Web du gouvernement du since it was archived. Please contact us to request Canada et elle n’a pas été modifiée ou mise à jour a format other than those available. depuis son archivage. Pour obtenir cette information dans un autre format, veuillez communiquer avec nous. This document is archival in nature and is intended Le présent document a une valeur archivistique et for those who wish to consult archival documents fait partie des documents d’archives rendus made available from the collection of Public Safety disponibles par Sécurité publique Canada à ceux Canada. qui souhaitent consulter ces documents issus de sa collection. Some of these documents are available in only one official language. Translation, to be provided Certains de ces documents ne sont disponibles by Public Safety Canada, is available upon que dans une langue officielle. Sécurité publique request. Canada fournira une traduction sur demande. D. J. DUNCAN & ASSOCIATES LTD. 1S-0 6 1 the Crown. R(11 Copyright of this document does not belong to author for — the must be obtained fro m ROM' authorization 19s1 any intended use. present document n' appartiennent Les droits d'auteur du du contenu du present pas à l'État. -

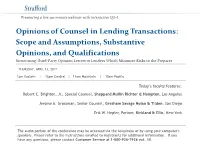

Scope and Assumptions, Substantive Opinions, and Qualifications Structuring Third-Party Opinion Letters to Lenders Which Minimize Risks to the Preparer

Presenting a live 90-minute webinar with interactive Q&A Opinions of Counsel in Lending Transactions: Scope and Assumptions, Substantive Opinions, and Qualifications Structuring Third-Party Opinion Letters to Lenders Which Minimize Risks to the Preparer THURSDAY, APRIL 13, 2017 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific Today’s faculty features: Robert C. Brighton, Jr., Special Counsel, Sheppard Mullin Richter & Hampton, Los Angeles Jerome A. Grossman, Senior Counsel, Gresham Savage Nolan & Tilden, San Diego Erik W. Hepler, Partner, Kirkland & Ellis, New York The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. Tips for Optimal Quality FOR LIVE EVENT ONLY Sound Quality If you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory, you may listen via the phone: dial 1-866-873-1442 and enter your PIN when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem. If you dialed in and have any difficulties during the call, press *0 for assistance. Viewing Quality To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again. Continuing Education Credits FOR LIVE EVENT ONLY In order for us to process your continuing education credit, you must confirm your participation in this webinar by completing and submitting the Attendance Affirmation/Evaluation after the webinar. -

Mediation Ethics Mcguirewoods LLP Hypotheticals and Analyses T

Mediation Ethics McGuireWoods LLP Hypotheticals and Analyses T. Spahn (4/20/15) Master MEDIATION ETHICS Hypotheticals and Analyses* Thomas E. Spahn McGuireWoods LLP Copyright 2015 * These analyses primarily rely on the ABA Model Rules, which represent a voluntary organization's suggested guidelines. Every state has adopted its own unique set of mandatory ethics rules, and you should check those when seeking ethics guidance. For ease of use, these analyses and citations use the generic term "legal ethics opinion" rather than the formal categories of the ABA's and state authorities' opinions -- including advisory, formal and informal. 64649012_2 Mediation Ethics McGuireWoods LLP Hypotheticals and Analyses T. Spahn (4/20/15) Master TABLE OF CONTENTS Hypo No. Subject Page (A) Before Mediations: Mediators 1 Disclosure of Conflicts of Interest ............................................................ 1 2 Unauthorized Practice of Law Issues ....................................................... 5 (B) Before Mediations: Lawyers 3 Law Firms Offering Mediation Services through the Firm or Subsidiaries ................................................................................................ 8 4 Multijurisdictional Practice Issues ............................................................ 25 5 Limited Representations ............................................................................ 34 6 Collaborative Lawyering ............................................................................ 41 7 Availability of Work Product Protection