When Drivers Are Not Going to Drive

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Coming Back Home After the Sun Rises: Returnee Entrepreneurs and Growth of High Tech Industries

G Model RESPOL-2772; No. of Pages 17 ARTICLE IN PRESS Research Policy xxx (2012) xxx–xxx Contents lists available at SciVerse ScienceDirect Research Policy jou rnal homepage: www.elsevier.com/locate/respol Coming back home after the sun rises: Returnee entrepreneurs and growth of high tech industries a,b c,∗ d Martin Kenney , Dan Breznitz , Michael Murphree a Department of Human and Community Development, University of California, Davis, United States b Berkeley Roundtable on the International Economy, United States c The Scheller College of Business, Georgia Institute of Technology, United States d Sam Nunn School of International Affairs, Georgia Institute of Technology, United States a r t i c l e i n f o a b s t r a c t Article history: Recently, the role of returnees in the economic development of various East Asian nations has received Received 6 November 2011 much attention. The early literature on the relocation of the most highly trained individuals from a devel- Received in revised form 30 July 2012 oping nation to a developed nation viewed the phenomena as a “brain drain.” Since the 1990s, a new Accepted 4 August 2012 strand of thinking has suggested that for developing nations this was actually a positive phenomenon; as Available online xxx these expatriates studied and then worked abroad, they absorbed technical expertise, managerial, and entrepreneurial skills. These theories stipulated that these expatriates then returned home, and ignited Keywords: a virtuous circle of technological entrepreneurship leading to rapid economic development. Much of this High skilled immigrants Innovation literature gives returnees a critical role in the home country’s take-off period of the local information and communications technology (ICT) industry. -

2018, but We Are Not Done by Any Means

Dear Shareholders, Today, we are pleased to review a year which includes numerous positive fundamental developments. At Himax Technologies, we pride ourselves not only on defending our position as the market leader in our sector, in terms of quality, reliability, and execution, but also on our ability to pair aggressive development aspirations with creating long-term shareholder value. In this regard, we believe we have accomplished a great deal in 2018, but we are not done by any means. 2018 was a year of new developments in our technology sector and our markets. At Himax Technologies, we have successfully leveraged our strengths to navigate both market dynamics as well as company specific opportunities to deliver a solid year of growth for shareholders. Further, we proactively initiated and executed several strategic initiatives to strengthen our operation and streamline R&D investments. We believe these proactive strategies reinforced our status in the marketplace and further strengthened our ability to defend our position as a market leader. Additionally, our execution in 2018 positions us for future growth well beyond 2018. Despite a challenging global economic environment, we are more optimistic about the opportunities ahead as several of our industry-leading technologies are at or nearing key inflection points. As a result, we expect to enter a period of substantial growth in the near future. Now, let me briefly go through each of our major business segments. Being a global leader in the display driver IC (DDIC) segment, we have been benefiting from China’s continued capacity expansion of its panel manufacturing as well as the Chinese smartphone makers’ rapid overseas expansion. -

Drive for Better Vision

Drive for better vision 2011 Annual Report Dear Shareholders, 2011 was a year of transition for Himax as we made significant progress in expanding our sales and customer base for our small and medium-sized driver IC and non-driver businesses. The small-medium driver segment has become our single largest revenue contributor, overtaking the large panel driver business. Revenues from the non-driver businesses exceeded 10% of total revenues in 2011, also the first time in our history. Seeing strong fundamentals across many of our product lines, we are confident that we are in a position to deliver positive revenue and earnings growth in 2012. Our 2011 revenues totaled $633 million, representing a slight 1.5% decline from the previous year due to the drop-off in the large-panel driver category. This was mainly because of our loss of market share in one of our major customers who decided to diversify their driver IC supply base. However, we see significant growth opportunities in China, where panel manufacturers are aggressively expanding their large panel capacity. Small and medium-sized drivers grew strongly in 2011, thanks mainly to phenomenal demand in smartphones, which tend to require better displays and thus higher end driver ICs. We enjoy a strong position in the smartphone sector as a result of our leading technologies, competitive products and solid customer base. We expect the strong growth momentum for small and medium-sized drivers to continue into 2012, driven by growing markets such as smartphones, tablets and displays used in the automotive industry. Non-driver product sales increased even further in 2011 with several product segments experiencing significant shipment and revenue growth from last year. -

20-F Job: DP17787 20F Date: 6/3/2010 8:54 AM

DPW Company: HIMAX TECHNOLOGIES INC Submission Type: 20-F Job: DP17787_20F Date: 6/3/2010 8:54 AM Submission Data File Submission Information Field Name Data Form Type* 20-F Filer CIK* 0001342338 Filer CCC* ******** Filer File Number* Filer is Shell Company* No Filer is Voluntary Filer* No Filer is Well Known Seasoned Issuer* No Filer Accelerated Status* Accelerated Filer Period of Report* 12-31-09 Return Copy off Confirming Copy off Contact Name Harold Tin Contact Number 011-852-2533-3369 SROS NASD Notify via Website only off (End Submission Information) Documents Field Name Data Enclosed Document Count 11 Document Name dp17787_20f.htm Document Type* 20-F Document Description FORM 20F Document Name 1 p36.jpg Document Type* 1 GRAPHIC Document Description 1 Document Name 2 p45.jpg Document Type* 2 GRAPHIC Document Description 2 Document Name 3 p49.jpg Document Type* 3 GRAPHIC Document Description 3 Document Name 4 dp17787_ex0101.htm Document Type* 4 EX-1.1 Document Description 4 EXHIBIT 1.1 Document Name 5 dp17787_ex0402.htm Document Type* 5 EX-4.2 Document Description 5 EXHIBIT 4.2 Document Name 6 dp17787_ex0801.htm Document Type* 6 EX-8.1 Document Description 6 EXHIBIT 8.1 Document Name 7 dp17787_ex1201.htm Document Type* 7 EX-12.1 Document Description 7 EXHIBIT 12.1 Document Name 8 dp17787_ex1202.htm Document Type* 8 EX-12.2 Document Description 8 EXHIBIT 12.2 Document Name 9 dp17787_ex1301.htm Document Type* 9 EX-13.1 Document Description 9 EXHIBIT 13.1 Document Name 10 dp17787_ex1501.htm Document Type* 10 EX-15.1 Document Description 10 EXHIBIT 15.1 (End Documents) Notifications Field Name Data Email Address [email protected] Email Address 1 [email protected] Email Address 2 [email protected] (End Notifications) Generated by DPW Name : dp17787_20f.htm Type : 20-F Page : Description : FORM 20F Job : DP17787_20F Date : 6/3/2010 8:54 AM UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. -

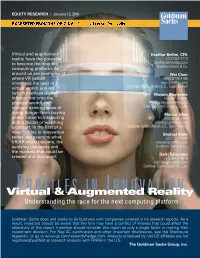

Virtual & Augmented Reality

EXCERPTED FROM THE ORIGINAL: See inside cover for details. FINANCIAL BACKING GLOBAL INTEREST SHIPPING OUT SELLING OUT INTEREST IN THE PAST READY TO BUILD A WAVE OF CONTENT ON THE WAY RETAIL VALUE HOME REDESIGN, REIMAGINED EASIER TO IMAGINE YOURSELF AT HOME Video • Jaunt The Ecosystem • NextVR Virtual Reality / Augmented Reality • VRSE • Oculus Story Studio • GoPro • IG Port Processors Games • TI Applications • Sony • Qualcomm • Ubisoft 3D Audio • STMicro Graphics • CCP Games • Nvidia • TI • Realtek • Oculus Story Studio • AMD • Wolfson • Himax • Tammeka Games • Qualcomm • Realtek • MediaTek • Pixel Titans • Intel • Capcom Augmented Reality Virtual Reality Engineering • Microsoft HoloLens • Facebook Oculus Head–mounted devices • Autodesk • Google Glass • Samsung Gear VR • Dassault Systèmes • Magic Leap • Google Cardboard • IrisVR • Atheer • HTC Vive • Visidraft • Osterhout Design • Sony PSVR • MakeVR Memory Group • Vuzix iWear (DRAM/SSD) • VR Union Claire • Micron Healthcare • Samsung • Psious • SK Hynix • zSpace • Toshiba • Conquer Mobile • 3D Systems Social • Altspace VR • High Fidelity • Podrift Commerce • Sixense {shopping} • Matterport {real estate} Display • Samsung • JDI Cameras • Himax • 360Heros • Crystal • GoPro Odyssey 3D Lenses • Nokia OZO • Wearality • Jaunt NEO • Zeiss • Matterport Pro 3D Components • Canon • Nikon Haptics • Largan • Alps Position/ Room Tracker • AAC • Hon Hai • Nidec • Pegatron • Flex • Jabil • HTC Motion Sensors • Leap Motion • InvenSense • TI • STMicro • Honeywell The Ecosystem Virtual Reality / Augmented -

2020 Annual Report Dear Shareholders

2020 Annual Report Dear Shareholders, Looking back at 2020, it was a volatile year. The global economy and semiconductor industry were severely damaged by the outbreak of COVID-19 and overshadowed by the prolonged US-China trade tension. The market for electronics devices saw a strong turnaround in demand during the second half of 2020 fueled by new work-from-home and e-learning lifestyles. However, the demand surge also intensifed the ongoing capacity shortage in foundry, assembly and testing. Under these challenging conditions, Himax thrived, delivering strong business results with a much-improved product mix from our comprehensive product portfolio, diversifed customer base and long-term partnerships with suppliers. It was a fruitful year for Himax in 2020. We increased our market share and achieved record revenue and gross margin in the fourth quarter while maintaining our leadership positions in tablet and automotive. We also made signifcant progress in our promising ultralow power smart sensing solutions. For the longer term, we remain committed to investing across all our product segments to further solidify our leading position in the global marketplace. As we move forward, we are dedicated to high quality, strict reliability, and effcient execution to deliver shareholder value. Now let me review each of our major business segments in 2020. Starting with our driver business, despite the capacity shortage the overall display driver IC businesses demonstrated robust growth. Led by TDDI for tablet and smartphone, our small and medium-sized driver IC segment dominated this year’s strong growth. For our large display driver IC business, the prevailing work-from-home and distance education gave rise to strong growth in monitor and notebook businesses in 2020. -

HIMX Presentation

Human Interface and Display Technologies : HIMX August 2021 INVESTOR PRESENTATION Forward Looking Statements Factors that could cause actual events or results to differ materially from those described in this conference call include, but are not limited to, the effect of the Covid-19 pandemic on the Company’s business; general business and economic conditions and the state of the semiconductor industry; market acceptance and competitiveness of the driver and non- driver products developed by the Company; demand for end-use applications products; reliance on a small group of principal customers; the uncertainty of continued success in technological innovations; our ability to develop and protect our intellectual property; pricing pressures including declines in average selling prices; changes in customer order patterns; changes in estimated full-year effective tax rate; shortage in supply of key components; changes in environmental laws and regulations; changes in export license regulated by Export Administration Regulations (EAR); exchange rate fluctuations; regulatory approvals for further investments in our subsidiaries; our ability to collect accounts receivable and manage inventory and other risks described from time to time in the Company's SEC filings, including those risks identified in the section entitled "Risk Factors" in its Form 20-F for the year ended December 31, 2020 filed with the SEC, as may be amended. Images of devices depicted in this presentation may be representative of those in which Himax has specification, or for reference-only and may not be associated with actual bill-of-material or design-win in the displayed image. Any association of such, without a confirmed disclosure of such by the Company or the Company's customer are coincidental. -

Company Vendor ID (Decimal Format) (AVL) Ditest Fahrzeugdiagnose Gmbh 4621 @Pos.Com 3765 0XF8 Limited 10737 1MORE INC

Vendor ID Company (Decimal Format) (AVL) DiTEST Fahrzeugdiagnose GmbH 4621 @pos.com 3765 0XF8 Limited 10737 1MORE INC. 12048 360fly, Inc. 11161 3C TEK CORP. 9397 3D Imaging & Simulations Corp. (3DISC) 11190 3D Systems Corporation 10632 3DRUDDER 11770 3eYamaichi Electronics Co., Ltd. 8709 3M Cogent, Inc. 7717 3M Scott 8463 3T B.V. 11721 4iiii Innovations Inc. 10009 4Links Limited 10728 4MOD Technology 10244 64seconds, Inc. 12215 77 Elektronika Kft. 11175 89 North, Inc. 12070 Shenzhen 8Bitdo Tech Co., Ltd. 11720 90meter Solutions, Inc. 12086 A‐FOUR TECH CO., LTD. 2522 A‐One Co., Ltd. 10116 A‐Tec Subsystem, Inc. 2164 A‐VEKT K.K. 11459 A. Eberle GmbH & Co. KG 6910 a.tron3d GmbH 9965 A&T Corporation 11849 Aaronia AG 12146 abatec group AG 10371 ABB India Limited 11250 ABILITY ENTERPRISE CO., LTD. 5145 Abionic SA 12412 AbleNet Inc. 8262 Ableton AG 10626 ABOV Semiconductor Co., Ltd. 6697 Absolute USA 10972 AcBel Polytech Inc. 12335 Access Network Technology Limited 10568 ACCUCOMM, INC. 10219 Accumetrics Associates, Inc. 10392 Accusys, Inc. 5055 Ace Karaoke Corp. 8799 ACELLA 8758 Acer, Inc. 1282 Aces Electronics Co., Ltd. 7347 Aclima Inc. 10273 ACON, Advanced‐Connectek, Inc. 1314 Acoustic Arc Technology Holding Limited 12353 ACR Braendli & Voegeli AG 11152 Acromag Inc. 9855 Acroname Inc. 9471 Action Industries (M) SDN BHD 11715 Action Star Technology Co., Ltd. 2101 Actions Microelectronics Co., Ltd. 7649 Actions Semiconductor Co., Ltd. 4310 Active Mind Technology 10505 Qorvo, Inc 11744 Activision 5168 Acute Technology Inc. 10876 Adam Tech 5437 Adapt‐IP Company 10990 Adaptertek Technology Co., Ltd. 11329 ADATA Technology Co., Ltd. -

UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F (Mark One) REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR _ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2014 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from ________________ to ________________ OR SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of event requiring this shell company report Commission file number: 000-51847 HIMAX TECHNOLOGIES, INC. (Exact name of Registrant as specified in its charter) Not Applicable (Translation of Registrant’s name into English) CAYMAN ISLANDS (Jurisdiction of incorporation or organization) NO. 26, ZIH LIAN ROAD SINSHIH DISTRICT, TAINAN CITY 74148 TAIWAN, REPUBLIC OF CHINA (Address of principal executive offices) Jackie Chang Chief Financial Officer Telephone: +886-2-2370-3999 E-mail: [email protected] Facsimile: +886-2-2314-0877 10F, No. 1, Xiangyang Road Taipei 10046 Taiwan, Republic of China (Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Ordinary Shares, par value $0.3 per ordinary share The NASDAQ Global Select Market Inc.* * Not for trading, but only in connection with the listing on the NASDAQ Global Select Market, Inc. -

Sessiontitle

PROGRAM 2014 SID INTERNATIONAL SYMPOSIUM June 3-6, 2014 (Tuesday – Friday) San Diego Convention Center San Diego, California, USA Session 1: Annual SID Business Meeting Tuesday, June 3 / 8:00 – 8:20 am / Room 6A Session 2: Opening Remarks / Keynote Addresses Tuesday, June 3 / 8:20 – 10:20 am / Room 6B 2.1: Keynote 1: Trends in China’s Display Industry and BOE’s Role Mr. Dongsheng Wang, Chairman, BOE Technology Group Co., Beijing, China 2:2: Keynote 2: The Role of Materials in New Display Technology Developments Dr. Michael Heckmeier, Senior VP, Liquid Crystals Research and Development, Merck, Darmstadt, Germany 2.3: Keynote 3: Toward an Immersive Image Experience Dr. Kazumasa Nomoto, Senior GM, Display Device Development Division, R&D Platform, Sony Corp., Kanagawa, Japan Session 3: Oxide TFTs vs. LTPS I (Oxide vs. LTPS/Active-Matrix Devices) Tuesday, June 3 / 10:50 am – 12:10 pm / Room 6A Chair: Arokia Nathan, University of Cambridge Co-Chair: Yoshitaka Yamamoto, Semiconductor Energy Laboratory Co., Ltd. 3.1: Invited Paper: Oxide versus LTPS TFTs for Active-Matrix Displays Jin Jang, Kyung Hee University, Seoul, South Korea 3.2: Invited Paper: Application of Rotation Magnet Sputtering Technology to a-IGZO Film Depositions Tetsuya Goto, Tohoku University, Sendai, Japan 3.3: Invited Paper: Future Possibility of C-Axis-Aligned Crystalline Oxide Semiconductor: Comparison with Low-Temperature Polysilicon Shunpei Yamazaki, Semiconductor Energy Laboratory Co., Ltd., Kanagawa, Japan 3.4L: Late-News Paper: Advanced ELA for Large-Sized AMOLED Displays Minhwan Choi, Samsung Display Co., Ltd., Kyunggi-do, South Korea Session 4: Display Manufacturing: LCD Materials (Display Manufacturing) Tuesday, June 3 / 10:50 am – 12:10 pm / Room 6B Chair: Chiwoo Kim, Samsung Display Co., Ltd. -

Add Subtitle (With Indentation)

Examining China’s Semiconductor Self-Sufficiency 17 November 2020 Present and Future Prospects Equity Research Asia Pacific Research Analyst Randy Abrams, [email protected] DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Examining China’s Semiconductor Self-Sufficiency Present and Future Prospects China building a domestic tech supply chain, although semis have lagged Domestic market is 60% of IC consumption, but only 25% of end demand Policy support through the IC fund, grants, tax breaks, Sci-Tech listings China suppliers having varying traction taking share: gaining in some IC categories and back-end, mixed in foundry and lagging in equipment Domestic investment poised to continue in-spite of US resistance High valuations a cheap source of funding for domestic suppliers CREDIT SUISSE, Equity Research, Asia Pacific 2 China building out its tech and semi ecosystem Semi Semi Cap Components Materials Equipment TV Brands Substrate: Access, Exposure: SMEE Panel: BOE, Tianma, CEC Panda, Fastprint, SCC Deposition: Naura, CSOT TV: Skyworth, Wafer: AST, Ferrotech Casing: BYDE, -

Global Supply Chain Operation in the APEC Region: Case Study of the Electrical and Electronics Industry

Global Supply Chain Operation in the APEC Region: Case Study of the Electrical and Electronics Industry APEC Policy Support Unit July 2013 Prepared by: Christopher Wood James Tetlow Washington CORE Email: [email protected] Produced for: Asia-Pacific Economic Cooperation Policy Support Unit Asia-Pacific Economic Cooperation Secretariat 35 Heng Mui Keng Terrace Tel: (65) 6891-9500 Fax: (65) 6891-9690 Email: [email protected] Website: www.apec.org APEC#213-SE-01.12. This work is licensed under the Creative Commons Attribution-NonCommercial- ShareAlike 3.0 Singapore License. To view a copy of this license, visit http://creativecommons.org/licenses/byb -nc-sa/3.0/sg/. The views expressed in this paper are those of the authors and do not necessarily represent those of APEC Member Economies and APEC Fora. The authors thank Denis Hew, Akhmad Bayhaqi and Bernadine Zhang Yuhua from the APEC Policy Support Unit to provide comments to the draft. The author also could like to thank the Commmiittee on Trade and Investment as well as APEC member economies for providing support and comments. Executive Summary i EXECUTIVE SUMMARY This study, conducted on behalf of the Asia-Pacific Economic Cooperation (APEC) Policy Support Unit (PSU) aims to provide a detailed understanding of current electrical and electronics (E&E) industry supply chain operations, strategies, and challenges, and suggest approaches APEC might adopt to make these supply chains and others more efficient and better contribute to economic integration in the region. Primary study findings include the following: Regarding the overall characteristics of E&E supply chains in the APEC region, as covered in Chapter 1, final assembly of consumer electronics has become increasingly centered on Asia, particularly China since 2001.